You might also like

- Annex 5-REGISTER OF CASH RECEIPTS, DEPOSITS AND OTHER RELATED FINANCIALDocument3 pagesAnnex 5-REGISTER OF CASH RECEIPTS, DEPOSITS AND OTHER RELATED FINANCIALVermon JayNo ratings yet

- RCRDDocument2 pagesRCRDjplaurel barangayNo ratings yet

- Module 2Document41 pagesModule 2Sujata SarkarNo ratings yet

- CPW FormsDocument163 pagesCPW Formssurendra kumarNo ratings yet

- W.E.F. - To - Certified That This Cash Book Contains - Pages Numbered From 1 ToDocument6 pagesW.E.F. - To - Certified That This Cash Book Contains - Pages Numbered From 1 Torfvz6sNo ratings yet

- General Form 74ADocument2 pagesGeneral Form 74ALordz Espina100% (1)

- Ncert Solu Class 11 Accountancy Chapter 8Document112 pagesNcert Solu Class 11 Accountancy Chapter 8Arif Shaikh100% (1)

- Financial Accounting E-Learning Notes on Bank AccountsDocument32 pagesFinancial Accounting E-Learning Notes on Bank AccountsFaith OzuahNo ratings yet

- Notes On Daily TransactionsDocument51 pagesNotes On Daily TransactionsCyndy NgwenNo ratings yet

- Checks and Contents of A BankDocument16 pagesChecks and Contents of A BankRaymond L. Dela CostaNo ratings yet

- DDO - Presentation PDFDocument15 pagesDDO - Presentation PDFalishehzadNo ratings yet

- Barangay ManualDocument104 pagesBarangay ManualRosemarie Guinayen Perez-MalagueñaNo ratings yet

- FABM2 Chapter5Document7 pagesFABM2 Chapter5johnleegiba09No ratings yet

- Adobe Scan Aug 11, 2023Document11 pagesAdobe Scan Aug 11, 2023Piya SabooNo ratings yet

- Chapter 5Document9 pagesChapter 5Chico, Angela Mae M.No ratings yet

- Pay-in-slip document explainedDocument7 pagesPay-in-slip document explainedS1626No ratings yet

- Journalizing TransactionsDocument38 pagesJournalizing TransactionsPratyush mishraNo ratings yet

- Worksheet 4.1 Introducing Bank ReconciliationDocument4 pagesWorksheet 4.1 Introducing Bank ReconciliationHan Nwe Oo100% (1)

- General Form No. 74 (A)Document5 pagesGeneral Form No. 74 (A)Shmily MendozaNo ratings yet

- Barangay Accounting System Manual: For Use by City/ Municipal AccountantsDocument104 pagesBarangay Accounting System Manual: For Use by City/ Municipal Accountantsemman neriNo ratings yet

- The Cash BookDocument22 pagesThe Cash Bookrdeepak99No ratings yet

- © Ncert Not To Be Republished: Recording of Transactions-IIDocument59 pages© Ncert Not To Be Republished: Recording of Transactions-IIIas Aspirant AbhiNo ratings yet

- Bank Reconciliation StatementDocument27 pagesBank Reconciliation Statementkimuli FreddieNo ratings yet

- Cash and ReceivablesDocument74 pagesCash and ReceivablesChitta LeeNo ratings yet

- FA - Chapter 7Document14 pagesFA - Chapter 7bias miaNo ratings yet

- Ncert Fm-Ac-xi Chapter 4Document59 pagesNcert Fm-Ac-xi Chapter 4shaannivasNo ratings yet

- Application Form For Change in Bank Account DetailsDocument1 pageApplication Form For Change in Bank Account DetailsARNo ratings yet

- Books of Original Entry Part 2Document8 pagesBooks of Original Entry Part 2Shavane DavisNo ratings yet

- Acc205 Bills of ExchangeDocument16 pagesAcc205 Bills of ExchangeCOLLET GAOLEBENo ratings yet

- Format of The Petty Cash BookDocument49 pagesFormat of The Petty Cash BookNa Ni63% (8)

- Disbursement Voucher (DV) : InstructionsDocument2 pagesDisbursement Voucher (DV) : InstructionsErica DascoNo ratings yet

- Untitled Document-1Document3 pagesUntitled Document-1Bryan JamaludeenNo ratings yet

- UntitledDocument14 pagesUntitledMary FolawumiNo ratings yet

- Lesson Chapter 5Document52 pagesLesson Chapter 5Melessa PescadorNo ratings yet

- AnnexDocument1 pageAnnexBelia Fe Abbalnog OlivianoNo ratings yet

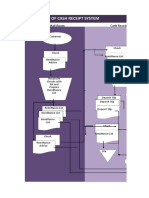

- Flowchart of a Cash Receipts SystemDocument17 pagesFlowchart of a Cash Receipts SystemStephanie Diane SabadoNo ratings yet

- Act1 Cash ReceiptsDocument17 pagesAct1 Cash ReceiptsStephanie Diane SabadoNo ratings yet

- Financial Accounting Chapter 4Document59 pagesFinancial Accounting Chapter 4abhinav2018No ratings yet

- Bank Reconciliation and Steps in Bank ReconciliationDocument15 pagesBank Reconciliation and Steps in Bank ReconciliationGrace AncajasNo ratings yet

- Posting to Ledger & Trial BalanceDocument19 pagesPosting to Ledger & Trial Balancemacs emsNo ratings yet

- State Whether The Following Statements Are TRUE or FALSE 1. Total of Payments Side Can Be Greater Than Total of Receipts Side IDocument1 pageState Whether The Following Statements Are TRUE or FALSE 1. Total of Payments Side Can Be Greater Than Total of Receipts Side Iminharahmath55No ratings yet

- Appendix 37 - Instructions - RADAIDocument2 pagesAppendix 37 - Instructions - RADAIhehehedontmind meNo ratings yet

- LECT22s BANK RECONCILIATION StudentDocument10 pagesLECT22s BANK RECONCILIATION StudentLalaland Acads100% (1)

- Chapter 5 Special Books Updated PDFDocument36 pagesChapter 5 Special Books Updated PDFmayank guptaNo ratings yet

- Bank Reconciliation StatementsDocument6 pagesBank Reconciliation StatementsTawanda Tatenda Herbert0% (1)

- Audit ProgramsDocument492 pagesAudit ProgramsNa-na Bucu100% (7)

- Accounting For Current Assets - Cash and ReceivablesDocument17 pagesAccounting For Current Assets - Cash and ReceivablesvladsteinarminNo ratings yet

- Nach ECS Direct Debit Mandate Instruction FormDocument2 pagesNach ECS Direct Debit Mandate Instruction Formsiva nunnaNo ratings yet

- Campos - Chapter 5Document36 pagesCampos - Chapter 5cmv mendoza50% (2)

- Prepare The Cash BookDocument4 pagesPrepare The Cash BookShaloom TV100% (1)

- Bank Reconciliation - 0Document16 pagesBank Reconciliation - 0Job CastonesNo ratings yet

- Financial Accounting and Reporting: Cash and Cash Equivalent CashDocument4 pagesFinancial Accounting and Reporting: Cash and Cash Equivalent CashJAPNo ratings yet

- Chapter 10: Cash and Financial InvestmentsDocument13 pagesChapter 10: Cash and Financial Investmentsdes arellanoNo ratings yet

- Assignment 1571213669 SmsDocument13 pagesAssignment 1571213669 SmsJayasuriya SNo ratings yet

- Cash Book RulesDocument33 pagesCash Book RulesNarasimha Murthy InampudiNo ratings yet

- FABM2 Wk8Document6 pagesFABM2 Wk8john lester pangilinanNo ratings yet

- Cash Drill & Disbursement Procedure: A Talk by GcroutDocument32 pagesCash Drill & Disbursement Procedure: A Talk by GcroutHimanshu ShrivastavaNo ratings yet

- 1.maintenance of AccountsDocument32 pages1.maintenance of AccountsShahid ShafiNo ratings yet

- Department of Accounting and FinanceDocument3 pagesDepartment of Accounting and FinanceShahid ShafiNo ratings yet

- CS101 Assignment #02 Introduction to Computing (20 MarksDocument2 pagesCS101 Assignment #02 Introduction to Computing (20 MarksShahid ShafiNo ratings yet

- Spring 2021 - ENG201 - 1Document2 pagesSpring 2021 - ENG201 - 1Shahid ShafiNo ratings yet

- Chapter - 1 Basics of Financial AccountingDocument64 pagesChapter - 1 Basics of Financial AccountingSayeda Laiba100% (1)

- Mgt101 - 2 - Recording Financial Information - Accounting EquationDocument38 pagesMgt101 - 2 - Recording Financial Information - Accounting EquationShahid ShafiNo ratings yet

- CS101 Assignment #02 Introduction to Computing (20 MarksDocument2 pagesCS101 Assignment #02 Introduction to Computing (20 MarksShahid ShafiNo ratings yet

- Mgt101-3 - Double Entry Bookkeeping System - Rules of Dr. and CRDocument55 pagesMgt101-3 - Double Entry Bookkeeping System - Rules of Dr. and CRShahid ShafiNo ratings yet

- Target's $300M Investment ProcessDocument55 pagesTarget's $300M Investment Processjk kumarNo ratings yet

- CDC Halves Social Distance Guidance For K-12 Classrooms: Divisive Meetings Test U.S. Ties To BeijingDocument52 pagesCDC Halves Social Distance Guidance For K-12 Classrooms: Divisive Meetings Test U.S. Ties To BeijingRomel Gamboa SanchezNo ratings yet

- Ducast UAE Manhole Cover Product InformationDocument1 pageDucast UAE Manhole Cover Product InformationSohail YounisNo ratings yet

- Understanding the Real Estate Cycle in the PhilippinesDocument39 pagesUnderstanding the Real Estate Cycle in the PhilippinesRoxanne Mae SinayNo ratings yet

- Utopian CitiesDocument9 pagesUtopian CitiesMichaela ConstantinoNo ratings yet

- Boettke-The Elgar Companion To Austrian EconomicsDocument646 pagesBoettke-The Elgar Companion To Austrian EconomicsrochalieberNo ratings yet

- Assignment On "Analysis of Gafla Movie Scam": Submitted By: - Enrollment No. NameDocument14 pagesAssignment On "Analysis of Gafla Movie Scam": Submitted By: - Enrollment No. NameDhrupal TripathiNo ratings yet

- Physical Delivery Guide: Page 1 of 79Document79 pagesPhysical Delivery Guide: Page 1 of 79maheshNo ratings yet

- Capital Budgeting V2 - Click Read Only To View DocumentDocument40 pagesCapital Budgeting V2 - Click Read Only To View DocumentSamantha Meril PandithaNo ratings yet

- Public Econ BookDocument172 pagesPublic Econ BookSuhas KandeNo ratings yet

- AA 5-Exercise 3 Page 91Document8 pagesAA 5-Exercise 3 Page 91Gil Diane AlcontinNo ratings yet

- GROUP 1 - Top-Down AnalysisDocument26 pagesGROUP 1 - Top-Down AnalysisSukma Wardha0% (1)

- Environment Market Grade 9Document26 pagesEnvironment Market Grade 9Antonio Jarligo CompraNo ratings yet

- Andert Egger Hanggi Leitner City DirectoriesDocument52 pagesAndert Egger Hanggi Leitner City Directoriesapi-327987435No ratings yet

- Financial Analysis of Investment Projects: January 1999Document9 pagesFinancial Analysis of Investment Projects: January 1999Nicolae NistorNo ratings yet

- Commune/Sangkat Fund and Local Development Case of CambodiaDocument7 pagesCommune/Sangkat Fund and Local Development Case of Cambodiahayatudin jusufNo ratings yet

- Lesson 3 The Firm and Its EnvironmentDocument105 pagesLesson 3 The Firm and Its EnvironmentShunuan HuangNo ratings yet

- ICD Tan Cang - Long Binh ReportDocument9 pagesICD Tan Cang - Long Binh ReportdangNo ratings yet

- Survey QuestionnaireDocument2 pagesSurvey QuestionnaireJess Jess100% (1)

- Begum Rukshani Mohamed Refai Batch 42Document24 pagesBegum Rukshani Mohamed Refai Batch 42Rukshani RefaiNo ratings yet

- Case StudyDocument28 pagesCase StudyNCP Shem ManaoisNo ratings yet

- NPO Accounting Activity May 26 2021Document5 pagesNPO Accounting Activity May 26 2021Cassie PeiaNo ratings yet

- wg11 TextilesDocument390 pageswg11 Textilesjpsingh75No ratings yet

- Chapter 19 SolutionsDocument34 pagesChapter 19 SolutionsRachel Rajanayagam100% (1)

- History: Carrefour (Document2 pagesHistory: Carrefour (Anonymous 9nwVyCj4UNo ratings yet

- Ch-5 MONEYDocument6 pagesCh-5 MONEYYoshita ShahNo ratings yet

- 06 Actvity 1 1Document4 pages06 Actvity 1 14mpspxd5msNo ratings yet

- Revised Transfer Guidelines-17-01-2019Document17 pagesRevised Transfer Guidelines-17-01-2019network SecurityNo ratings yet

- Final Exam Study GuideDocument9 pagesFinal Exam Study GuideDognimin Aboudramane KonateNo ratings yet

- 8RNKGT TicketsDocument2 pages8RNKGT TicketsAhsan AliNo ratings yet