You might also like

- Credit Repair Letters To Remove Debt StrawmanDocument75 pagesCredit Repair Letters To Remove Debt StrawmanRon Mowles98% (220)

- SMChap 018Document32 pagesSMChap 018testbank100% (8)

- Clarkson Lumber Cash Flows and Pro FormaDocument6 pagesClarkson Lumber Cash Flows and Pro FormaArmaan ChandnaniNo ratings yet

- Acct Statement - XX1046 - 22042022Document52 pagesAcct Statement - XX1046 - 22042022amitNo ratings yet

- Summary of William H. Pike & Patrick C. Gregory's Why Stocks Go Up and DownFrom EverandSummary of William H. Pike & Patrick C. Gregory's Why Stocks Go Up and DownNo ratings yet

- Payout Policy IIDocument20 pagesPayout Policy IIy1301401755No ratings yet

- 4.financing & Dividend PoliciesDocument11 pages4.financing & Dividend PoliciesSuja mkNo ratings yet

- Corporate Finance Chapter6Document20 pagesCorporate Finance Chapter6Dan688No ratings yet

- Dividends and Share Repurchases: Basics: Presenter's Name Presenter's Title DD Month YyyyDocument20 pagesDividends and Share Repurchases: Basics: Presenter's Name Presenter's Title DD Month YyyyPRAKNo ratings yet

- Chapter Nineteen: Dividends and Other PayoutsDocument37 pagesChapter Nineteen: Dividends and Other PayoutsiisrasyidiNo ratings yet

- Dividend Decisions: Unit 5Document41 pagesDividend Decisions: Unit 5Fara HameedNo ratings yet

- Merger Acquisition (MA) Ch9 Accounting and PaymentsDocument13 pagesMerger Acquisition (MA) Ch9 Accounting and PaymentsTanNo ratings yet

- Dividends and Share Repurchases: Basics: Presenter's Name Presenter's Title DD Month YyyyDocument20 pagesDividends and Share Repurchases: Basics: Presenter's Name Presenter's Title DD Month YyyyKavin Ur FrndNo ratings yet

- Solution Manual For Core Concepts of Accounting Raiborn 2nd EditionDocument18 pagesSolution Manual For Core Concepts of Accounting Raiborn 2nd EditionJacquelineFrancisfpgs100% (36)

- MOD004491 Corporate Finance Dividend Policy: Anglia Ruskin University DR Handy Tan Handy - Tan@anglia - Ac.ukDocument27 pagesMOD004491 Corporate Finance Dividend Policy: Anglia Ruskin University DR Handy Tan Handy - Tan@anglia - Ac.ukDaryl Khoo Tiong JinnNo ratings yet

- Intermediate: AccountingDocument80 pagesIntermediate: AccountingPhạm Lê Thùy LinhNo ratings yet

- Topic 8 Dividends and Dividend PolicyDocument42 pagesTopic 8 Dividends and Dividend PolicyNajwa Alyaa binti Abd WakilNo ratings yet

- Dividend Decision and Stock Dividend-Repurchase-SplitDocument56 pagesDividend Decision and Stock Dividend-Repurchase-SplitA MerchantNo ratings yet

- Dividend DecisionsDocument48 pagesDividend DecisionsankitaNo ratings yet

- Financial Management Chapter TwoDocument45 pagesFinancial Management Chapter TwobikilahussenNo ratings yet

- Taxation of Business Entities 6th Edition Spilker Solutions ManualDocument31 pagesTaxation of Business Entities 6th Edition Spilker Solutions Manualpricking.carryallmbtgco100% (17)

- Changes in A PartnershipDocument18 pagesChanges in A PartnershipHadi HarizNo ratings yet

- Unit 9Document16 pagesUnit 9Wgt ChampNo ratings yet

- Dividend Decision and Stock Dividend-Repurchase-SplitDocument56 pagesDividend Decision and Stock Dividend-Repurchase-SplitRoshniNo ratings yet

- Financing Resources - Valuation of Stocks L4AEDocument57 pagesFinancing Resources - Valuation of Stocks L4AETacitus KilgoreNo ratings yet

- Determinants of DividendsDocument9 pagesDeterminants of DividendsyashchauhanNo ratings yet

- Chapter 13 SolutionsDocument45 pagesChapter 13 Solutionsaboodyuae2000No ratings yet

- Topic 10 Dividend Policy (Chapter 16, Brealey) : Information Content of Stock RepurchasesDocument8 pagesTopic 10 Dividend Policy (Chapter 16, Brealey) : Information Content of Stock RepurchasesHashashahNo ratings yet

- 6 Dividend DecisionDocument31 pages6 Dividend Decisionambikaantil4408No ratings yet

- Sharing Firm WealthDocument3 pagesSharing Firm WealthJohn Jasper50% (2)

- 2.6. Retained EarningsDocument5 pages2.6. Retained EarningsKPoPNyx Edits100% (1)

- 1 What Are Corporate Actions?: CreditorsDocument14 pages1 What Are Corporate Actions?: Creditorsstudenthc100% (1)

- WK 9 Equity 2 Slides Per PageDocument25 pagesWK 9 Equity 2 Slides Per PageThùy Linh Lê ThịNo ratings yet

- Dividend Policy: Chapter Learning ObjectivesDocument8 pagesDividend Policy: Chapter Learning ObjectivesDINEO PRUDENCE NONGNo ratings yet

- Dividend PolicyDocument28 pagesDividend PolicySid Tushaar SiddharthNo ratings yet

- Ividend Ecisions: Learning OutcomesDocument48 pagesIvidend Ecisions: Learning OutcomesPranay GNo ratings yet

- Thomas FAM Ch02 Student AccessibleDocument73 pagesThomas FAM Ch02 Student AccessibleNeel PeswaniNo ratings yet

- Ch. 16 - Distribution To ShareholdersDocument28 pagesCh. 16 - Distribution To ShareholdersLara FloresNo ratings yet

- Dividend Policy - Textbook SlidesDocument34 pagesDividend Policy - Textbook SlidesIfah RazNo ratings yet

- Chapter 7Document24 pagesChapter 7ClaraNo ratings yet

- Spilker TBE 15e PPT CH04 AccessibleDocument50 pagesSpilker TBE 15e PPT CH04 AccessibleJulio AlanisNo ratings yet

- Session 9 DividendDocument15 pagesSession 9 DividendEmilyNo ratings yet

- Dividend PolicyDocument9 pagesDividend PolicyAbdulkarim Hamisi KufakunogaNo ratings yet

- Shareholders EquityDocument10 pagesShareholders Equityearling haalandNo ratings yet

- FM-Sessions 23 - 24 Dividend Policy-CompleteDocument72 pagesFM-Sessions 23 - 24 Dividend Policy-CompleteSaadat ShaikhNo ratings yet

- Chapter 13Document13 pagesChapter 13Mondy MondyNo ratings yet

- Dividend Decisions-1Document24 pagesDividend Decisions-1TIBUGWISHA IVANNo ratings yet

- Valuation Concepts Module 8 PDFDocument8 pagesValuation Concepts Module 8 PDFJisselle Marie CustodioNo ratings yet

- Fin440 Chapter 17Document21 pagesFin440 Chapter 17Md. Shaikat Alam Joy 1421759030No ratings yet

- DividendsDocument27 pagesDividendsSadia R ChowdhuryNo ratings yet

- Sources of Capital: Owners' Equity: Mcgraw-Hill/IrwinDocument29 pagesSources of Capital: Owners' Equity: Mcgraw-Hill/IrwinKumarRohitNo ratings yet

- Chapter 4 Stock Valuation (Student)Document10 pagesChapter 4 Stock Valuation (Student)Nguyễn Thái Minh ThưNo ratings yet

- Sources of Capital: Owners' Equity: Mcgraw-Hill/IrwinDocument29 pagesSources of Capital: Owners' Equity: Mcgraw-Hill/IrwinNileshAgarwalNo ratings yet

- DividendDocument34 pagesDividendquoteNo ratings yet

- Chapter 19 Dividend Other PayoutDocument23 pagesChapter 19 Dividend Other PayoutiisrasyidiNo ratings yet

- 9 Dividend Policy, Share Repurchases and Other PayoutsDocument9 pages9 Dividend Policy, Share Repurchases and Other PayoutsAnna CharlotteNo ratings yet

- Paying Zero TaxesDocument23 pagesPaying Zero TaxesHappyGhostNo ratings yet

- Financial Management:: Prepared byDocument19 pagesFinancial Management:: Prepared byHimanshu MehraNo ratings yet

- Peirson12e SM CH11Document8 pagesPeirson12e SM CH11Corry CarltonNo ratings yet

- Sweda Arifah (1862201120)Document7 pagesSweda Arifah (1862201120)Sweda ArifahNo ratings yet

- Buckwold12e Solutions Ch11Document40 pagesBuckwold12e Solutions Ch11Fang YanNo ratings yet

- DividendsDocument12 pagesDividendsAhmed Abdelkader YossifNo ratings yet

- Module 2 - Internal Control-1Document20 pagesModule 2 - Internal Control-1Melvin JustinNo ratings yet

- DD IntroductionDocument10 pagesDD IntroductionKishore KumarNo ratings yet

- $CMRY Equity Research ReportDocument10 pages$CMRY Equity Research ReportAzka RifkyNo ratings yet

- DPC Assignment 3Document10 pagesDPC Assignment 3siddhant vyasNo ratings yet

- 2018 Audited Financial StatementDocument175 pages2018 Audited Financial StatementTULIO, Jeremy I.No ratings yet

- PG & Research Department of Economics Subject Name PUBLIC FINANCES Staff Name Dr. R.Malathi Class: Iii B.A EconomicsDocument32 pagesPG & Research Department of Economics Subject Name PUBLIC FINANCES Staff Name Dr. R.Malathi Class: Iii B.A EconomicsManishNo ratings yet

- Quiz Bank Recon and Proof of CashDocument3 pagesQuiz Bank Recon and Proof of CashAlexander ONo ratings yet

- Vishmay BCA Syllabus Semester IDocument22 pagesVishmay BCA Syllabus Semester IAmay JaiswalNo ratings yet

- Tender NoticeDocument1 pageTender NoticeAshar OpNo ratings yet

- Performance AppraisalsDocument91 pagesPerformance AppraisalsPradeep BhatiaNo ratings yet

- AIB 27th Annual Report 2021..22 CompressedDocument177 pagesAIB 27th Annual Report 2021..22 Compressedfayeraleta2024No ratings yet

- Lesson 7 - Accounting CycleDocument35 pagesLesson 7 - Accounting CycleEyyyNo ratings yet

- Consumer Cards Overview Side by SideDocument6 pagesConsumer Cards Overview Side by SidewewaewaNo ratings yet

- Joy and Jolly Day Care CentreDocument20 pagesJoy and Jolly Day Care CentreSsemakula FrankNo ratings yet

- Economic Policy ManagementDocument11 pagesEconomic Policy ManagementMuhammad Anisuzzaman LitonNo ratings yet

- Item 1. BusinessDocument222 pagesItem 1. BusinessVashirAhmadNo ratings yet

- Final Exam - Comprehensive - 10.24.16Document5 pagesFinal Exam - Comprehensive - 10.24.16YamateNo ratings yet

- TX Promissory Note - SampleDocument2 pagesTX Promissory Note - Sampleapi-80072288No ratings yet

- Chapter 2Document10 pagesChapter 2Yasin IsikNo ratings yet

- InternshipDocument2 pagesInternshipChelsi Christine TenorioNo ratings yet

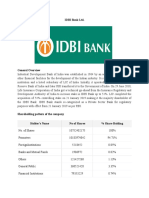

- IDBI Bank LTDDocument3 pagesIDBI Bank LTDSololoNo ratings yet

- Tugas 5 - Teori Akuntansi KontemporerDocument2 pagesTugas 5 - Teori Akuntansi Kontemporerfelica werdhaNo ratings yet

- To Print JournalDocument5 pagesTo Print JournalDiana Grace SierraNo ratings yet

- PGP-IBM Batch 2010-12 With 2011-13 PlacementDocument27 pagesPGP-IBM Batch 2010-12 With 2011-13 Placementsenjaliya11No ratings yet

- Final DrillDocument19 pagesFinal DrillKurumi 06No ratings yet

- Uniform Fraudulant Transfer Act - Ufta84Document40 pagesUniform Fraudulant Transfer Act - Ufta84Richarnellia-RichieRichBattiest-CollinsNo ratings yet

- ICAP Syllabus ChangeDocument3 pagesICAP Syllabus ChangeMuneer DhamaniNo ratings yet