You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5819)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1092)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (845)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (348)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Risk and ReturnDocument88 pagesRisk and ReturnRatul HasanNo ratings yet

- Genuine Leathers Pvt. LTD: Business Plan ProposalDocument6 pagesGenuine Leathers Pvt. LTD: Business Plan ProposalRondex Corpuz PabloNo ratings yet

- College of Accountancy Business Economics and International Hospitality ManagementDocument13 pagesCollege of Accountancy Business Economics and International Hospitality ManagementLENLYN FALAMIGNo ratings yet

- The Technical Group 3Document2 pagesThe Technical Group 3LENLYN FALAMIGNo ratings yet

- PM Bok Summary 6Document53 pagesPM Bok Summary 6LENLYN FALAMIGNo ratings yet

- MODULE MGT 202 Good GovernanceDocument24 pagesMODULE MGT 202 Good GovernanceLENLYN FALAMIGNo ratings yet

- Tax 301 Module 1Document39 pagesTax 301 Module 1LENLYN FALAMIGNo ratings yet

- FINALDocument12 pagesFINALLENLYN FALAMIGNo ratings yet

- Constitutional Uniformity and Equality in State TaxationDocument873 pagesConstitutional Uniformity and Equality in State TaxationLENLYN FALAMIGNo ratings yet

- Impact of Human Resourcesnmanagement On Business Performance - A Review of LiteratureDocument17 pagesImpact of Human Resourcesnmanagement On Business Performance - A Review of LiteratureLENLYN FALAMIGNo ratings yet

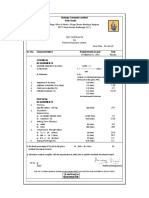

- Ambuja Cements Limited Unit: DadriDocument1 pageAmbuja Cements Limited Unit: DadriVishal Sharma100% (1)

- Assignment2 - ICMB319Document13 pagesAssignment2 - ICMB319CHANBOON WATAWANITKULNo ratings yet

- Lecture 10 Introduction To Macro EconomicsDocument49 pagesLecture 10 Introduction To Macro EconomicsDevyansh GuptaNo ratings yet

- TC-18-26 - Laboratory Performance Testing of Warm-Mix Asphalt Mixtures For Airport Pavements - 071718Document51 pagesTC-18-26 - Laboratory Performance Testing of Warm-Mix Asphalt Mixtures For Airport Pavements - 071718gorefest123No ratings yet

- 1 The Dynamic Environment of International TradeDocument14 pages1 The Dynamic Environment of International TradeJamilla Danao Aguado100% (1)

- Chess Score Sheet PDFDocument1 pageChess Score Sheet PDFChristian C. MendizabelNo ratings yet

- Making Reservations: Name? (Tentu Saja Anda Bisa, Pak. Bolehkah Saya Tahu Reservasi Ini Atas NamaDocument17 pagesMaking Reservations: Name? (Tentu Saja Anda Bisa, Pak. Bolehkah Saya Tahu Reservasi Ini Atas NamaSyafnaqbanddariminang CihuyNo ratings yet

- Republic of The Philippines: Escolastica Romero District HospitalDocument13 pagesRepublic of The Philippines: Escolastica Romero District HospitalRames Ely GJNo ratings yet

- BUSN 5041 - M1 - Ch02Document28 pagesBUSN 5041 - M1 - Ch02Busn DNo ratings yet

- Tech. DataDocument15 pagesTech. DataNavnit VishnoiNo ratings yet

- Extra Large Great Icosahedron PDFDocument60 pagesExtra Large Great Icosahedron PDFДенис СмирновNo ratings yet

- Option Chain AnalysisDocument14 pagesOption Chain AnalysisSantosh ThakurNo ratings yet

- Comparison of The Use of Traditional and Low Waste Formwork Systems in Hong KongDocument8 pagesComparison of The Use of Traditional and Low Waste Formwork Systems in Hong KongMwesigwa DaniNo ratings yet

- Training Activity Matrix TemplateDocument3 pagesTraining Activity Matrix TemplateIrish Jane TabelismaNo ratings yet

- Briefer - PS Depot - Revised - 3Document49 pagesBriefer - PS Depot - Revised - 3EarthAngel OrganicsNo ratings yet

- UntitledDocument19 pagesUntitledJonathan HansenNo ratings yet

- Construction Management Chapter 2Document92 pagesConstruction Management Chapter 2thapitcherNo ratings yet

- Avoid Common Mistakes in Completing The BMCDocument3 pagesAvoid Common Mistakes in Completing The BMCdiptiNo ratings yet

- ? Among The Given, Identify The Relevant Cost in Insourcing vs. Outsourcing DecisionDocument2 pages? Among The Given, Identify The Relevant Cost in Insourcing vs. Outsourcing DecisionJerome Eziekel Posada PanaliganNo ratings yet

- Theory of Urban DesignDocument27 pagesTheory of Urban DesignLawrence Babatunde OgunsanyaNo ratings yet

- SOVEM20-00068 - MY DUNGEON Sales Terms and ConditionsDocument7 pagesSOVEM20-00068 - MY DUNGEON Sales Terms and ConditionsC J Moscoso MadronaNo ratings yet

- A Horse and Two GoatsDocument16 pagesA Horse and Two Goatsgatikalmal3No ratings yet

- Motorvehicle Sales AgreementDocument2 pagesMotorvehicle Sales AgreementMambo Joshua100% (1)

- Raju N Print Udyam Registration CertificateDocument3 pagesRaju N Print Udyam Registration CertificateOmkar kaleNo ratings yet

- Shopping For Clothes - Exercises 4 PDFDocument2 pagesShopping For Clothes - Exercises 4 PDFelif nutNo ratings yet

- Electric Water Heater CalculationDocument3 pagesElectric Water Heater CalculationAkhil VijaiNo ratings yet

- Chapter 9 SUMMARY SECTION CDocument4 pagesChapter 9 SUMMARY SECTION ClalesyeuxNo ratings yet

- Managerial Economics - Lecture 3Document18 pagesManagerial Economics - Lecture 3Fizza MasroorNo ratings yet