You might also like

- Bsbfim601 Manage Finances Monitor and Review BudgetDocument7 pagesBsbfim601 Manage Finances Monitor and Review BudgetAli Butt100% (7)

- Profitability RatiosDocument3 pagesProfitability RatiosJohn Muema100% (1)

- Summer Project On COAL INDIADocument77 pagesSummer Project On COAL INDIADippak ChabraNo ratings yet

- Financial Results With Results Press Release & Limited Review Report For June 30, 2015 (Company Update)Document10 pagesFinancial Results With Results Press Release & Limited Review Report For June 30, 2015 (Company Update)Shyam SunderNo ratings yet

- Directors' Report: Larsen & Toubro Infotech LimitedDocument33 pagesDirectors' Report: Larsen & Toubro Infotech LimitedNirmal Rintu RaviNo ratings yet

- Financial and Managerial Accounting DifferencesDocument5 pagesFinancial and Managerial Accounting Differencessus meetaNo ratings yet

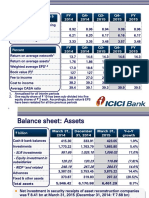

- Analysis of Income Statement of The Allahabad BankDocument18 pagesAnalysis of Income Statement of The Allahabad BankLofidNo ratings yet

- 2021 Annual ReportDocument64 pages2021 Annual ReportBBNo ratings yet

- Kawasaki Reports Higher Profits in Q1 2015Document17 pagesKawasaki Reports Higher Profits in Q1 2015Tyasmara NugrahaNo ratings yet

- July 31, 2018 Honda Motor Co., Ltd. Reports Consolidated Financial Results For The Fiscal First Quarter ENDED JUNE 30, 2018Document17 pagesJuly 31, 2018 Honda Motor Co., Ltd. Reports Consolidated Financial Results For The Fiscal First Quarter ENDED JUNE 30, 2018Black Star11No ratings yet

- Financial Statement Analysis: Prof. Vivek BhatiaDocument48 pagesFinancial Statement Analysis: Prof. Vivek BhatiaManan GuptaNo ratings yet

- Infosys Q1 2002Document64 pagesInfosys Q1 2002GouthamNo ratings yet

- Finance Department Analysis of Dabur LimitedDocument15 pagesFinance Department Analysis of Dabur LimitedradhikaNo ratings yet

- Zuying. XueDocument9 pagesZuying. XueAbiot Asfiye GetanehNo ratings yet

- Projected Financial StatementDocument8 pagesProjected Financial StatementRicaNo ratings yet

- DCW Ltd cost structure analysis reveals 13.2% contribution marginDocument2 pagesDCW Ltd cost structure analysis reveals 13.2% contribution marginDurgit KumarNo ratings yet

- Lloyds Bank Q1 2019 interim resultsDocument6 pagesLloyds Bank Q1 2019 interim resultssaxobobNo ratings yet

- A2Z Annual Report 2018Document216 pagesA2Z Annual Report 2018Siddharth ShekharNo ratings yet

- Cost Ii CH 3Document8 pagesCost Ii CH 3TESFAY GEBRECHERKOSNo ratings yet

- Key Ratios: Movement in Yield, Costs & Margins (Percent) FY 2014 Q4-2014 Q3 - 2015 Q4 - 2015 FY 2015Document5 pagesKey Ratios: Movement in Yield, Costs & Margins (Percent) FY 2014 Q4-2014 Q3 - 2015 Q4 - 2015 FY 2015Abhimanyu SahniNo ratings yet

- Baraka Power q1 Sep 2015Document21 pagesBaraka Power q1 Sep 2015Sibiya ZamanNo ratings yet

- Investor Presentation Mar21Document34 pagesInvestor Presentation Mar21Sanjay RainaNo ratings yet

- HUL Directors Report Ar 2013 14Document24 pagesHUL Directors Report Ar 2013 14Lakshmi MNo ratings yet

- Mgm China Holdings Limited 美 高 梅 中 國 控 股 有 限 公 司Document7 pagesMgm China Holdings Limited 美 高 梅 中 國 控 股 有 限 公 司Suix Leon LeeNo ratings yet

- IOB Reports 241% Rise in Net Profit at Rs. 434 Crore for Q4Document2 pagesIOB Reports 241% Rise in Net Profit at Rs. 434 Crore for Q4Sivashanmugam ThamizhselvanNo ratings yet

- Announcement of The Results For The Three Months Ended March 31, 2023Document27 pagesAnnouncement of The Results For The Three Months Ended March 31, 2023charles shawNo ratings yet

- Furnmart Ltd. (FURNMART-BW) - Interim Report For Period End 31-Jan-2018 (English) PDFDocument1 pageFurnmart Ltd. (FURNMART-BW) - Interim Report For Period End 31-Jan-2018 (English) PDFmisterbeNo ratings yet

- FA Assignment - 2Document1 pageFA Assignment - 2Sidhant ThakurNo ratings yet

- Project A Pact215Document11 pagesProject A Pact215ALYSSA PERALTANo ratings yet

- pvatepla-q3-2023-enDocument14 pagespvatepla-q3-2023-enrogercabreNo ratings yet

- What Is A Profit and Loss (P&L) Statement - InvestopediaDocument16 pagesWhat Is A Profit and Loss (P&L) Statement - InvestopediaFrancisco Del PuertoNo ratings yet

- 2023 Annual Financial Report EDocument94 pages2023 Annual Financial Report Ehimanshuchikiboy05No ratings yet

- Final Account GA2Document14 pagesFinal Account GA2Ashwin KushwahNo ratings yet

- Final Exam On Accounting For Decision MakingDocument17 pagesFinal Exam On Accounting For Decision MakingSivasakti MarimuthuNo ratings yet

- Umeme submits 2016 tariff review applicationDocument22 pagesUmeme submits 2016 tariff review applicationEdgar MugaruraNo ratings yet

- Ajooni BiotechDocument21 pagesAjooni BiotechSunny RaoNo ratings yet

- Ucal Fuel AR 2018Document144 pagesUcal Fuel AR 2018Puneet367No ratings yet

- GTL Analyst Presentation: Safe HarborDocument17 pagesGTL Analyst Presentation: Safe Harborvsekar_1No ratings yet

- Mount Sinai Q1 2020 Financial StatementsDocument21 pagesMount Sinai Q1 2020 Financial StatementsJonathan LaMantiaNo ratings yet

- Ashok Leyland Limited Regd. Office:1 Sardar Patel Road, Guindy, Chennai - 600 032Document2 pagesAshok Leyland Limited Regd. Office:1 Sardar Patel Road, Guindy, Chennai - 600 032Kumaresh SalemNo ratings yet

- 2022 Annual Financial Report EDocument94 pages2022 Annual Financial Report EKashav KaseraNo ratings yet

- 2018 EMBA - Exam Paper With SolutionsDocument11 pages2018 EMBA - Exam Paper With SolutionsahmedNo ratings yet

- InfoEdge Annual Report 2023 1Document1 pageInfoEdge Annual Report 2023 1Aditya RoyNo ratings yet

- Q1 20 - DhunseriDocument4 pagesQ1 20 - Dhunserica.anup.kNo ratings yet

- 634085163601250000financial Highlights0310-Correcte-1Document2 pages634085163601250000financial Highlights0310-Correcte-1arunnair1985No ratings yet

- Quantitative Methods II: Submitted byDocument7 pagesQuantitative Methods II: Submitted byKavisha singhNo ratings yet

- Annual Report SIB 2019-20Document189 pagesAnnual Report SIB 2019-20SREE RAMNo ratings yet

- Kawasaki Heavy Industries Reports 36% Increase in Operating Income for Q1Document6 pagesKawasaki Heavy Industries Reports 36% Increase in Operating Income for Q1Tyasmara NugrahaNo ratings yet

- Inari Financial Result Q1 FY2024Document17 pagesInari Financial Result Q1 FY2024GZHNo ratings yet

- Directors' Report: 1. HighlightsDocument15 pagesDirectors' Report: 1. Highlightshimadri.banerji60No ratings yet

- Chapter 3Document41 pagesChapter 3MohamedYahiaNo ratings yet

- Dir ReportDocument34 pagesDir ReportRupasinghNo ratings yet

- Indigo Income STMT 1Document1 pageIndigo Income STMT 1deepzNo ratings yet

- Date of Report Tuesday, April 29, 2008 SRF Limited - Quick & Dirty Analysis Analyst Dhananjayan J ContactDocument11 pagesDate of Report Tuesday, April 29, 2008 SRF Limited - Quick & Dirty Analysis Analyst Dhananjayan J Contactapi-3702531No ratings yet

- CHB Mar19 PDFDocument14 pagesCHB Mar19 PDFSajeetha MadhavanNo ratings yet

- HUL Financial AnalysisDocument27 pagesHUL Financial AnalysisSachin SinghNo ratings yet

- Appendix 4E and Annual Report FY20Document79 pagesAppendix 4E and Annual Report FY20Gursheen KaurNo ratings yet

- NAV-Questions-25 7 20Document43 pagesNAV-Questions-25 7 20anubhav pathakNo ratings yet

- Indian Oil Corporation Project 2Document30 pagesIndian Oil Corporation Project 2Rishika GoelNo ratings yet

- Statement of Comprehensive IncomeDocument11 pagesStatement of Comprehensive IncomeKhiezna PakamNo ratings yet

- Le Jugement Dans Son IntégralitéDocument23 pagesLe Jugement Dans Son IntégralitéDefimediagroup Ldmg100% (1)

- KHUSHAL LOBINE-letter Resignation PMSDDocument2 pagesKHUSHAL LOBINE-letter Resignation PMSDL'express MauriceNo ratings yet

- CERTIFICATE OF AUDIT & REPORT 2022-23 MauritiusDocument595 pagesCERTIFICATE OF AUDIT & REPORT 2022-23 MauritiusLe Mauricien100% (2)

- Rapport Human RightsDocument25 pagesRapport Human RightsL'express MauriceNo ratings yet

- DPP V The StateDocument15 pagesDPP V The StateL'express MauriceNo ratings yet

- Common Letter of Parliamentary, Extra-Parliamentary Parties, & Social Movements of Mauritius 22-05-23 8.00 P.MDocument2 pagesCommon Letter of Parliamentary, Extra-Parliamentary Parties, & Social Movements of Mauritius 22-05-23 8.00 P.ML'express Maurice100% (1)

- Audit Sur La Restauration Et La Sécurité: Alerte Rouge Dans Les HôpitauxDocument5 pagesAudit Sur La Restauration Et La Sécurité: Alerte Rouge Dans Les HôpitauxL'express MauriceNo ratings yet

- DPP V The StateDocument15 pagesDPP V The StateL'express MauriceNo ratings yet

- Weather Outlook - MRU and ROD - PRESS - 21 January 2024 SN 01 UpdatedDocument2 pagesWeather Outlook - MRU and ROD - PRESS - 21 January 2024 SN 01 UpdatedL'express MauriceNo ratings yet

- Le DPP S'insurge Contre Les Insinuations Malveillantes de GobinDocument1 pageLe DPP S'insurge Contre Les Insinuations Malveillantes de GobinL'express Maurice100% (1)

- Bhadain V ICAC (Application Under Article 806 of The Code de Procedure Civile) 190423Document18 pagesBhadain V ICAC (Application Under Article 806 of The Code de Procedure Civile) 190423L'express MauriceNo ratings yet

- Mauritius 2022 Human Rights ReportDocument22 pagesMauritius 2022 Human Rights ReportL'express MauriceNo ratings yet

- Statement - 04 AprilDocument5 pagesStatement - 04 AprilL'express MauriceNo ratings yet

- Météo: Des Averses Orageuses Et Des Rafales Jusqu'à 70 KM/H Attendues VendrediDocument1 pageMétéo: Des Averses Orageuses Et Des Rafales Jusqu'à 70 KM/H Attendues VendrediL'express MauriceNo ratings yet

- MétéoDocument1 pageMétéoL'express MauriceNo ratings yet

- Négociations Sur Les Chagos: Mauritius Global Diaspora Tire La Sonnette D'alarmeDocument3 pagesNégociations Sur Les Chagos: Mauritius Global Diaspora Tire La Sonnette D'alarmeL'express MauriceNo ratings yet

- PNQ 15 November 2022Document1 pagePNQ 15 November 2022L'express MauriceNo ratings yet

- Teeluckdharry K V Lam Shang Leen P Ors 2022Document14 pagesTeeluckdharry K V Lam Shang Leen P Ors 2022L'express Maurice100% (1)

- Coffres-Forts : Ramgoolam Face À Un Nouveau Procès, Lisez Le JugementDocument22 pagesCoffres-Forts : Ramgoolam Face À Un Nouveau Procès, Lisez Le JugementDefimediagroup Ldmg100% (1)

- List of Orators For Monday 13 June 2022Document1 pageList of Orators For Monday 13 June 2022L'express MauriceNo ratings yet

- Communique 010722 - EmployeesDocument1 pageCommunique 010722 - EmployeesL'express Maurice100% (3)

- Communique 010722 - Self - Employed IndividualsDocument1 pageCommunique 010722 - Self - Employed IndividualsL'express MauriceNo ratings yet

- Electoral CommissionerDocument3 pagesElectoral CommissionerL'express MauriceNo ratings yet

- Prize Money - RM 1Document1 pagePrize Money - RM 1L'express MauriceNo ratings yet

- Greener Port-Louis For A Healthier Urban HeartDocument7 pagesGreener Port-Louis For A Healthier Urban HeartL'express MauriceNo ratings yet

- UricekDocument1 pageUricekL'express MauriceNo ratings yet

- Public Service Excellence Award 2021: Awards Category Project Description Ministries/DepartmentsDocument3 pagesPublic Service Excellence Award 2021: Awards Category Project Description Ministries/DepartmentsL'express MauriceNo ratings yet

- Comm New Subsidies 29ap22Document1 pageComm New Subsidies 29ap22L'express MauriceNo ratings yet

- (Document) Competition Commission: Deux Fournisseurs de Gaz Médicaux Écopent D'une Amende de Rs 3,6 MDocument3 pages(Document) Competition Commission: Deux Fournisseurs de Gaz Médicaux Écopent D'une Amende de Rs 3,6 ML'express MauriceNo ratings yet

- Bibi Saf Eena Lo Tun (MRS) Clerk of The National Assembly Parliament House Port LouisDocument1 pageBibi Saf Eena Lo Tun (MRS) Clerk of The National Assembly Parliament House Port LouisL'express MauriceNo ratings yet

- Energy (R) Evolution: A Sustainable Energy Outlook For CanadaDocument120 pagesEnergy (R) Evolution: A Sustainable Energy Outlook For Canadarto2951100% (1)

- Wind Power PDFDocument3 pagesWind Power PDFBalan PalaniappanNo ratings yet

- Benefits of Renewable Energy UseDocument8 pagesBenefits of Renewable Energy Usegeronimo stiltonNo ratings yet

- Electricity Pricing Theory and Case StudyDocument401 pagesElectricity Pricing Theory and Case StudyFulki Kautsar SNo ratings yet

- B.Tech 3-1 - R16Document18 pagesB.Tech 3-1 - R16Advala SaikumarNo ratings yet

- Hybrid Solar Thermal Integration at Existing Fossil Generation FacilitiesDocument29 pagesHybrid Solar Thermal Integration at Existing Fossil Generation FacilitiesBassoma IbtissamNo ratings yet

- Note On Power Generation Capacity Addition in Andhra PradeshDocument39 pagesNote On Power Generation Capacity Addition in Andhra PradeshHkStocksNo ratings yet

- Naval Ship Prpulsion PDFDocument228 pagesNaval Ship Prpulsion PDFenaceceltenaceNo ratings yet

- Ilaria Peretti 200510Document17 pagesIlaria Peretti 200510Jawad WaheedNo ratings yet

- Renewable Energy ApplicationsDocument10 pagesRenewable Energy ApplicationsSuny DaniNo ratings yet

- Powering Up The Smart Grid: A Northwest Initiative For Job Creation, Energy Security and Clean, Affordable ElectricityDocument31 pagesPowering Up The Smart Grid: A Northwest Initiative For Job Creation, Energy Security and Clean, Affordable ElectricitySeshu KumarNo ratings yet

- 6 Marks Questions (Examples)Document25 pages6 Marks Questions (Examples)shelleyallynNo ratings yet

- Kentucky's Climate Action PlanDocument158 pagesKentucky's Climate Action PlanEarth Charter IndianaNo ratings yet

- PV Project Export Sales Record List (Part)Document5 pagesPV Project Export Sales Record List (Part)TOm TOmNo ratings yet

- Future Cities Feasibility Studies - Interim ReportDocument71 pagesFuture Cities Feasibility Studies - Interim ReportnihatmuratNo ratings yet

- Islanded Distribution Network Control with DGs and ESSDocument62 pagesIslanded Distribution Network Control with DGs and ESSMohamed SaeedNo ratings yet

- Review of Related Studies (Solar Panel) : Charger - BODY FULL PDFDocument2 pagesReview of Related Studies (Solar Panel) : Charger - BODY FULL PDFMatti NoNo ratings yet

- TA 4665 PAK Power Transmission Enhancement Project - PakistanDocument45 pagesTA 4665 PAK Power Transmission Enhancement Project - PakistanJaved RashidNo ratings yet

- Energy StorageDocument146 pagesEnergy StorageGuillermo Lopez-FloresNo ratings yet

- Design and Development of Hybrid Wind and Solar Energy System For Power GenerationDocument8 pagesDesign and Development of Hybrid Wind and Solar Energy System For Power GenerationBayu pradanaNo ratings yet

- Regulation 2008 Eee SyllabusDocument78 pagesRegulation 2008 Eee SyllabusAlen PinkNo ratings yet

- Power Plant Types PhilippinesDocument25 pagesPower Plant Types PhilippinesJo Sofia Delos SantosNo ratings yet

- Energy Powering Ontarios Growth Report en 2023-07-07Document86 pagesEnergy Powering Ontarios Growth Report en 2023-07-07Randolph SeccafienNo ratings yet

- Pittsburgh Coal ConferenceDocument68 pagesPittsburgh Coal ConferenceNileshNo ratings yet

- 100 KWp Solar Power Plant Proposal for Nazareth Foods Pvt LtdDocument24 pages100 KWp Solar Power Plant Proposal for Nazareth Foods Pvt LtdRabindra SinghNo ratings yet

- SiemensDocument46 pagesSiemensrituNo ratings yet

- APSEBEA Power Trends Booklet-1-2016Document32 pagesAPSEBEA Power Trends Booklet-1-2016msreddy86No ratings yet

- Solar Water Pump Mini Project 2Document13 pagesSolar Water Pump Mini Project 2Houssem Sendelzereg MadridNo ratings yet

- Environment Management Guwahati UniversityDocument17 pagesEnvironment Management Guwahati UniversityRahul DekaNo ratings yet