You might also like

- The Basics of Public Budgeting and Financial Management: A Handbook for Academics and PractitionersFrom EverandThe Basics of Public Budgeting and Financial Management: A Handbook for Academics and PractitionersNo ratings yet

- Economies and Consumers Quarterly Data - Historical - Non-Seasonally AdjustedDocument5 pagesEconomies and Consumers Quarterly Data - Historical - Non-Seasonally AdjustedJoseph MateoNo ratings yet

- Business StatisticsDocument5 pagesBusiness StatisticsShubham100% (1)

- An Empirical Study On Factors Affecting Customer Retention in Logistics Service Providers - A Case Study On Abc Logistics (PVT) LimitedDocument24 pagesAn Empirical Study On Factors Affecting Customer Retention in Logistics Service Providers - A Case Study On Abc Logistics (PVT) LimitedAza SamsudeenNo ratings yet

- Brigade Enterprises LimitedDocument36 pagesBrigade Enterprises LimitedAnkur MittalNo ratings yet

- OOIL 2017 Annual Results Presentation PDFDocument29 pagesOOIL 2017 Annual Results Presentation PDFmdorneanuNo ratings yet

- Startup Finance ModelDocument88 pagesStartup Finance ModelAbhishek AggarwalNo ratings yet

- KFH Annual Report 2018 - English PDFDocument162 pagesKFH Annual Report 2018 - English PDFFardheen BanuNo ratings yet

- UShine Implementation PlanDocument4 pagesUShine Implementation PlanwongchingkiNo ratings yet

- Annual Report FY 2018-19Document146 pagesAnnual Report FY 2018-19Javeed GurramkondaNo ratings yet

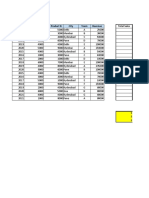

- Excel - Assignment - 1 (1Document16 pagesExcel - Assignment - 1 (1Ashish ChangediyaNo ratings yet

- Market Capitalisation of Capital Market SegmentsDocument3 pagesMarket Capitalisation of Capital Market Segmentsanjali shilpa kajalNo ratings yet

- PT Hilti - Company Profile - Approval Chemical AnchorDocument18 pagesPT Hilti - Company Profile - Approval Chemical Anchorfalahaskar0% (1)

- HongKong - Industrial - MarketView - Q1 2021Document5 pagesHongKong - Industrial - MarketView - Q1 2021Tu LiangNo ratings yet

- Insead Tech Logistics in SEA 2019Document33 pagesInsead Tech Logistics in SEA 2019Mukul RaghavNo ratings yet

- BCC Sindh Forms 2018-19Document29 pagesBCC Sindh Forms 2018-19Sarmad SamejoNo ratings yet

- Q1 2021 E Commerce ReportDocument6 pagesQ1 2021 E Commerce ReportEstefania HernandezNo ratings yet

- Pacifica Bay Future Resource Analysis: 2014 2015 2016 2017 2018 TotalDocument1 pagePacifica Bay Future Resource Analysis: 2014 2015 2016 2017 2018 TotalNishiki NishioNo ratings yet

- Introduction To Time Series ModelsDocument20 pagesIntroduction To Time Series ModelsManuel Alejandro Sanabria AmayaNo ratings yet

- Indigo Stock Pitch: Nse: Buy at 1046Document21 pagesIndigo Stock Pitch: Nse: Buy at 1046Sourabh ChiprikarNo ratings yet

- Telematics DataDocument19 pagesTelematics DataRenauld SNo ratings yet

- Why Service Robots Boom Worldwide: IFR Press Conference, 11 October 2017 BrusselsDocument25 pagesWhy Service Robots Boom Worldwide: IFR Press Conference, 11 October 2017 BrusselsRishabhNo ratings yet

- Financial AnalysisDocument18 pagesFinancial Analysismaizatul rosniNo ratings yet

- Paint IndustryDocument28 pagesPaint IndustryRAJNI SHRIVASTAVANo ratings yet

- Tata CommunicationsDocument6 pagesTata CommunicationspriyaNo ratings yet

- 2019 q2 Cbre Vietnam Forum - en - HCMDocument78 pages2019 q2 Cbre Vietnam Forum - en - HCMNguyen Quang MinhNo ratings yet

- Choice IntroductionDocument22 pagesChoice IntroductionMonu SinghNo ratings yet

- Book 1Document2 pagesBook 1Blend BerishaNo ratings yet

- ITIDA - Egypt Destination of Choice 2018Document28 pagesITIDA - Egypt Destination of Choice 2018AKNo ratings yet

- Graphical Representation of Nalco Working Capital RatioDocument15 pagesGraphical Representation of Nalco Working Capital RatioAbhijitNo ratings yet

- Analysis NewDocument12 pagesAnalysis NewFairooz AliNo ratings yet

- 19 Investment Economic Cycles and GrowthDocument4 pages19 Investment Economic Cycles and Growthsaywhat133No ratings yet

- Summer Internship Project: On "Working Capital Management of Rastriya Ispat Nigam Limited-Vsp"Document27 pagesSummer Internship Project: On "Working Capital Management of Rastriya Ispat Nigam Limited-Vsp"Avinash GoguNo ratings yet

- Feasibility StudyDocument18 pagesFeasibility StudyJessa BallonNo ratings yet

- Year-End Presentation 2014Document29 pagesYear-End Presentation 2014stefany IINo ratings yet

- #BOLD STOP Marketing PlanDocument50 pages#BOLD STOP Marketing PlanAhmed Alaa100% (1)

- 2017 Budget-Country Presentation FormatDocument59 pages2017 Budget-Country Presentation FormatYhane Hermann BackNo ratings yet

- 2 Charts Show How Much The World Depends On Taiwan For: Revenue RecognitionDocument5 pages2 Charts Show How Much The World Depends On Taiwan For: Revenue RecognitionDuong Trinh MinhNo ratings yet

- AFSA ProjectDocument9 pagesAFSA Projectsunit dasNo ratings yet

- Calzado en España StatistaDocument65 pagesCalzado en España StatistaPaula Calvo ZaragozanoNo ratings yet

- pp16Document30 pagespp16Mark GrahamNo ratings yet

- Client: Taiwan Semiconductor Manufacturing Co., Ltd. (NYSE: TSM / TSE: 2330) Auditor: Deloitte (1) Understanding of The ClientDocument8 pagesClient: Taiwan Semiconductor Manufacturing Co., Ltd. (NYSE: TSM / TSE: 2330) Auditor: Deloitte (1) Understanding of The ClientDuong Trinh MinhNo ratings yet

- Appraisal of Dividend Policy of Navana CNG Limited: Presented by Easmin Ara Eity ID: 2018-2-10-048Document11 pagesAppraisal of Dividend Policy of Navana CNG Limited: Presented by Easmin Ara Eity ID: 2018-2-10-048Movie SenderNo ratings yet

- Sokkelaret 2017 Engelsk PresentasjonDocument25 pagesSokkelaret 2017 Engelsk PresentasjonHải Thân NgọcNo ratings yet

- Eadr Project On Infosys CompanyDocument5 pagesEadr Project On Infosys CompanyDivyavadan MateNo ratings yet

- Investment Thesis by Prateek LalDocument2 pagesInvestment Thesis by Prateek LalPrateek LalNo ratings yet

- Creating Bar Charts With Single Series of Data: Period SalesDocument8 pagesCreating Bar Charts With Single Series of Data: Period Saleslakshmi PurushothmanNo ratings yet

- EasyJet vs. RyanairDocument22 pagesEasyJet vs. RyanairDiana CostaNo ratings yet

- 2017 Annual Report EN PDFDocument160 pages2017 Annual Report EN PDFYuk SimNo ratings yet

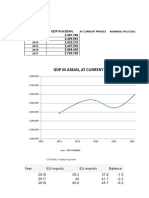

- GDP in Asean, at Current Prrices (Nominal) in Us DollarsDocument3 pagesGDP in Asean, at Current Prrices (Nominal) in Us DollarsMehul AgarwallaNo ratings yet

- Annual Report 2018Document519 pagesAnnual Report 2018MR RockyNo ratings yet

- Demand PlanningDocument31 pagesDemand PlanningRahulRahuNo ratings yet

- Trend of Netflix's Streaming Subscribers Worldwide in Nine Years From 2011-2020Document7 pagesTrend of Netflix's Streaming Subscribers Worldwide in Nine Years From 2011-2020Minh Thu NguyenNo ratings yet

- SaaS Financial Model 3.0 ExcelDocument367 pagesSaaS Financial Model 3.0 Excelმექანიკური ფორთოხალიNo ratings yet

- Business As UsualDocument24 pagesBusiness As UsualRenold DarmasyahNo ratings yet

- AssignmentDocument3 pagesAssignmentLEON JOAQUIN VALDEZNo ratings yet

- Introduction:-: Headquartered - Chennai ValueDocument4 pagesIntroduction:-: Headquartered - Chennai ValueArijit sahaNo ratings yet

- Assets: Director's Letter & Auditor's Notes Flag Major Points Attributed To RiskDocument7 pagesAssets: Director's Letter & Auditor's Notes Flag Major Points Attributed To RiskCH NAIRNo ratings yet

- Chiang Mai Hotel Market Update 2017 03Document4 pagesChiang Mai Hotel Market Update 2017 03Oon KooNo ratings yet

- CEE Budapest City Report Q3 2020Document10 pagesCEE Budapest City Report Q3 2020Iringo NovakNo ratings yet

- Generating FunctionDocument14 pagesGenerating FunctionSrishti UpadhyayNo ratings yet

- Resulticks Credentials Deck 2019 1Document16 pagesResulticks Credentials Deck 2019 1leminhbkNo ratings yet

- Comparative Research On Market Size of Cigarette Brand of ITDocument105 pagesComparative Research On Market Size of Cigarette Brand of ITAbhi SriNo ratings yet

- The Best SharePoint Online Training by Real Time ExpertsDocument15 pagesThe Best SharePoint Online Training by Real Time ExpertsestherNo ratings yet

- Wyndham Worldwide 2011 Competency DictionaryDocument38 pagesWyndham Worldwide 2011 Competency DictionaryNerissa ArvianaNo ratings yet

- Workers Participation in ManagementDocument4 pagesWorkers Participation in Managementbhagathnagar100% (1)

- PP - Master Data-Sap PPDocument16 pagesPP - Master Data-Sap PPratnesh_xpNo ratings yet

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Document1 pageTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Ganesh PrabuNo ratings yet

- CBSE Class 12 Economics Sample Paper (For 2014)Document19 pagesCBSE Class 12 Economics Sample Paper (For 2014)cbsesamplepaperNo ratings yet

- 09.stock - Statement - 31.12.2023 GAJANANDDocument4 pages09.stock - Statement - 31.12.2023 GAJANANDSEENU PATELNo ratings yet

- CH 05Document41 pagesCH 05pravyramNo ratings yet

- Infor Ming - Le Install 11 1 AD r18Document114 pagesInfor Ming - Le Install 11 1 AD r18rhutudeva2463No ratings yet

- Export Promotion Capital Goods Scheme PresentationDocument32 pagesExport Promotion Capital Goods Scheme PresentationDakshata SawantNo ratings yet

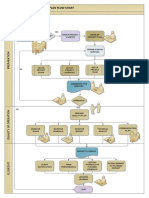

- Project Management Flowchart 2Document1 pageProject Management Flowchart 2LightNo ratings yet

- Global Marketing UNIQLODocument11 pagesGlobal Marketing UNIQLOM.Maulana Iskandar ZulkarnainNo ratings yet

- Sales TrainingDocument146 pagesSales TrainingdsunteNo ratings yet

- 10 Info SheetDocument6 pages10 Info Sheetdungnv151No ratings yet

- Monetizing VoLTE, RCS and Video IMS MRF and Conferencing SolutionsDocument13 pagesMonetizing VoLTE, RCS and Video IMS MRF and Conferencing SolutionslcardonagNo ratings yet

- SP1 PDFDocument12 pagesSP1 PDFyumyumpuieNo ratings yet

- SNOWTEXDocument29 pagesSNOWTEXMD NayeemNo ratings yet

- Full Download Solution Manual For Horngrens Financial Managerial Accounting 6th Edition PDF Full ChapterDocument36 pagesFull Download Solution Manual For Horngrens Financial Managerial Accounting 6th Edition PDF Full Chaptercrantspremieramxpiz100% (16)

- Case Study Alibaba Versus Tencent APADocument4 pagesCase Study Alibaba Versus Tencent APALeonardo Ferreira da Silva50% (4)

- Ringing A BellDocument31 pagesRinging A Bellnfpsynergy100% (1)

- Dettol - A Complete Product Description and Its ReviewDocument13 pagesDettol - A Complete Product Description and Its ReviewRitesh SrivastavaNo ratings yet

- Supply and Demand ExamplesDocument2 pagesSupply and Demand ExamplesJay R ChivaNo ratings yet

- Name: Jinal M. MistryDocument10 pagesName: Jinal M. MistryjinnymistNo ratings yet

- AA Accounts Course DetailsDocument3 pagesAA Accounts Course DetailsBalaNo ratings yet

- 2Q14 Atlanta Industrial Market ReportDocument4 pages2Q14 Atlanta Industrial Market ReportBea LorinczNo ratings yet

- A Study On Management of Non Performing Assets in District Central Cooperative Bank PDFDocument5 pagesA Study On Management of Non Performing Assets in District Central Cooperative Bank PDFDevikaNo ratings yet

- GW4 - Quantity and InventoryDocument1 pageGW4 - Quantity and InventoryPhương TrầnNo ratings yet

- Waiter Rant: Thanks for the Tip—Confessions of a Cynical WaiterFrom EverandWaiter Rant: Thanks for the Tip—Confessions of a Cynical WaiterRating: 3.5 out of 5 stars3.5/5 (487)

- Dealers of Lightning: Xerox PARC and the Dawn of the Computer AgeFrom EverandDealers of Lightning: Xerox PARC and the Dawn of the Computer AgeRating: 4 out of 5 stars4/5 (88)

- The Intel Trinity: How Robert Noyce, Gordon Moore, and Andy Grove Built the World's Most Important CompanyFrom EverandThe Intel Trinity: How Robert Noyce, Gordon Moore, and Andy Grove Built the World's Most Important CompanyNo ratings yet

- AI Superpowers: China, Silicon Valley, and the New World OrderFrom EverandAI Superpowers: China, Silicon Valley, and the New World OrderRating: 4.5 out of 5 stars4.5/5 (399)

- The United States of Beer: A Freewheeling History of the All-American DrinkFrom EverandThe United States of Beer: A Freewheeling History of the All-American DrinkRating: 4 out of 5 stars4/5 (7)

- Getting Started in Consulting: The Unbeatable Comprehensive Guidebook for First-Time ConsultantsFrom EverandGetting Started in Consulting: The Unbeatable Comprehensive Guidebook for First-Time ConsultantsRating: 4.5 out of 5 stars4.5/5 (10)

- To Pixar and Beyond: My Unlikely Journey with Steve Jobs to Make Entertainment HistoryFrom EverandTo Pixar and Beyond: My Unlikely Journey with Steve Jobs to Make Entertainment HistoryRating: 4.5 out of 5 stars4.5/5 (260)

- Summary: Unreasonable Hospitality: The Remarkable Power of Giving People More than They Expect by Will Guidara: Key Takeaways, Summary & Analysis IncludedFrom EverandSummary: Unreasonable Hospitality: The Remarkable Power of Giving People More than They Expect by Will Guidara: Key Takeaways, Summary & Analysis IncludedRating: 2.5 out of 5 stars2.5/5 (5)

- All The Beauty in the World: The Metropolitan Museum of Art and MeFrom EverandAll The Beauty in the World: The Metropolitan Museum of Art and MeRating: 4.5 out of 5 stars4.5/5 (83)

- The War Below: Lithium, Copper, and the Global Battle to Power Our LivesFrom EverandThe War Below: Lithium, Copper, and the Global Battle to Power Our LivesRating: 4.5 out of 5 stars4.5/5 (9)

- The Toyota Way (Second Edition): 14 Management Principles from the World's Greatest ManufacturerFrom EverandThe Toyota Way (Second Edition): 14 Management Principles from the World's Greatest ManufacturerRating: 4 out of 5 stars4/5 (121)

- Vulture Capitalism: Corporate Crimes, Backdoor Bailouts, and the Death of FreedomFrom EverandVulture Capitalism: Corporate Crimes, Backdoor Bailouts, and the Death of FreedomNo ratings yet

- The Infinite Machine: How an Army of Crypto-Hackers Is Building the Next Internet with EthereumFrom EverandThe Infinite Machine: How an Army of Crypto-Hackers Is Building the Next Internet with EthereumRating: 3 out of 5 stars3/5 (12)

- All You Need to Know About the Music Business: Eleventh EditionFrom EverandAll You Need to Know About the Music Business: Eleventh EditionNo ratings yet

- How to Make Money Online with OnlyFans Earn More than $10,000 per Month From Zero With the 7 Secret Hacks To Start and Scale Your Digital BusinessFrom EverandHow to Make Money Online with OnlyFans Earn More than $10,000 per Month From Zero With the 7 Secret Hacks To Start and Scale Your Digital BusinessRating: 5 out of 5 stars5/5 (1)

- The Formula: How Rogues, Geniuses, and Speed Freaks Reengineered F1 into the World's Fastest Growing SportFrom EverandThe Formula: How Rogues, Geniuses, and Speed Freaks Reengineered F1 into the World's Fastest Growing SportRating: 4 out of 5 stars4/5 (1)

- Lean Six Sigma: The Ultimate Guide to Lean Six Sigma, Lean Enterprise, and Lean Manufacturing, with Tools Included for Increased Efficiency and Higher Customer SatisfactionFrom EverandLean Six Sigma: The Ultimate Guide to Lean Six Sigma, Lean Enterprise, and Lean Manufacturing, with Tools Included for Increased Efficiency and Higher Customer SatisfactionRating: 5 out of 5 stars5/5 (2)

- Rainmaker: Superagent Hughes Norton and the Money Grab Explosion of Golf from Tiger to LIV and BeyondFrom EverandRainmaker: Superagent Hughes Norton and the Money Grab Explosion of Golf from Tiger to LIV and BeyondRating: 4 out of 5 stars4/5 (1)

- 15 Lies Women Are Told at Work: …And the Truth We Need to SucceedFrom Everand15 Lies Women Are Told at Work: …And the Truth We Need to SucceedNo ratings yet

- INSPIRED: How to Create Tech Products Customers LoveFrom EverandINSPIRED: How to Create Tech Products Customers LoveRating: 5 out of 5 stars5/5 (9)

- Network of Lies: The Epic Saga of Fox News, Donald Trump, and the Battle for American DemocracyFrom EverandNetwork of Lies: The Epic Saga of Fox News, Donald Trump, and the Battle for American DemocracyRating: 4 out of 5 stars4/5 (16)

- How to Make a Killing: Blood, Death and Dollars in American MedicineFrom EverandHow to Make a Killing: Blood, Death and Dollars in American MedicineRating: 5 out of 5 stars5/5 (1)

- Excellence Wins: A No-Nonsense Guide to Becoming the Best in a World of CompromiseFrom EverandExcellence Wins: A No-Nonsense Guide to Becoming the Best in a World of CompromiseRating: 5 out of 5 stars5/5 (79)