You might also like

- Casing ProblemsDocument40 pagesCasing Problemssura srikanthNo ratings yet

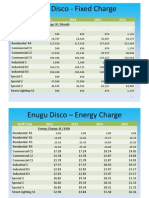

- Enugu Disco - Fixed Charge: Tariff Code 2012 2013 2014 2015Document2 pagesEnugu Disco - Fixed Charge: Tariff Code 2012 2013 2014 2015Tony AppsNo ratings yet

- Compensacion Angular Y Longitudinal: Ang. H. Ang.H G M S Decim. G M SDocument6 pagesCompensacion Angular Y Longitudinal: Ang. H. Ang.H G M S Decim. G M SEdwinNo ratings yet

- X-Park Calculation EarthworkDocument4 pagesX-Park Calculation EarthworknurNo ratings yet

- Fault Level 33kvDocument2 pagesFault Level 33kvAllama HasanNo ratings yet

- 33kV Fault Level: T1 T2 Substation Voltage (KV) Zs MVA %Z Zact MVA %ZDocument2 pages33kV Fault Level: T1 T2 Substation Voltage (KV) Zs MVA %Z Zact MVA %ZAllama HasanNo ratings yet

- Datos de Estacion "X" 1° Paso Precipitacion Max en 24hDocument23 pagesDatos de Estacion "X" 1° Paso Precipitacion Max en 24hPonce CristianNo ratings yet

- DATA DCP 1 KP LamprganDocument379 pagesDATA DCP 1 KP LamprganNadiah KhairunnisaNo ratings yet

- Estimacion de La Radiacion SolarDocument2 pagesEstimacion de La Radiacion SolarClinthon Chaca AyuqueNo ratings yet

- Calculation of Setting Pressure For:-Model Jvy-800T (K81) & Yzy801T Hydraulic Pile Jacking MachineDocument1 pageCalculation of Setting Pressure For:-Model Jvy-800T (K81) & Yzy801T Hydraulic Pile Jacking MachineAdam LimNo ratings yet

- Calcula PattyDocument9 pagesCalcula Pattygabriela monica ancasi choqueNo ratings yet

- PBL SpfeDocument10 pagesPBL Spfeyash chavanNo ratings yet

- Louvered Grille Performance DataDocument7 pagesLouvered Grille Performance DataCarlos Valle TurciosNo ratings yet

- Pembangunan Jalan Tol Trans Sumatera: Dynamic Cone Penetrometer (DCP)Document2 pagesPembangunan Jalan Tol Trans Sumatera: Dynamic Cone Penetrometer (DCP)Yeti Nur HayatiNo ratings yet

- TX To RX ObstructedDocument5 pagesTX To RX ObstructedKamin AgyaoNo ratings yet

- Tugas Merancang (Bianca Prima 4414100014 - Nuril Millatu 4414100025)Document28 pagesTugas Merancang (Bianca Prima 4414100014 - Nuril Millatu 4414100025)biancaprimaNo ratings yet

- Calculo APP SantanaDocument13 pagesCalculo APP SantanaCarlos Enrique Diaz ReyesNo ratings yet

- Lab 3Document10 pagesLab 3Joseph CarlsonNo ratings yet

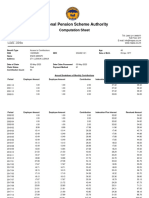

- Claim Computation SheetDocument5 pagesClaim Computation SheetRon ChunoNo ratings yet

- Data and GraphsDocument22 pagesData and GraphsManish KumarNo ratings yet

- Exercise 5.1 (Mod 5)Document6 pagesExercise 5.1 (Mod 5)Camille AmanteNo ratings yet

- CementosDocument2 pagesCementosRudyard Torrico CarbajalNo ratings yet

- Costos 2021Document25 pagesCostos 2021stephanie caján poloNo ratings yet

- Carter Tracy GeneralDocument17 pagesCarter Tracy GeneraljalassalNo ratings yet

- Program Pascasarjana Universitas Negeri Medan State University of MedanDocument3 pagesProgram Pascasarjana Universitas Negeri Medan State University of MedanhilanNo ratings yet

- Fellenius ExercícioDocument3 pagesFellenius ExercícioCarlos PerunaNo ratings yet

- List of Transformers & Transmission Lines of BSPTCLDocument4 pagesList of Transformers & Transmission Lines of BSPTCLChief Engineer TransOMNo ratings yet

- Date: Sr. No. Trimmu Barrage (U/S) Qadirabad (D/S) Rasul (D/S) Time (HRS)Document7 pagesDate: Sr. No. Trimmu Barrage (U/S) Qadirabad (D/S) Rasul (D/S) Time (HRS)zeeshansheikh7No ratings yet

- Calculos Sistema AporticadoDocument105 pagesCalculos Sistema AporticadoyoelNo ratings yet

- Assignment 4 - 2Document4 pagesAssignment 4 - 2divyaNo ratings yet

- Tugas Michael Richie Aprilano (18021101057)Document12 pagesTugas Michael Richie Aprilano (18021101057)rivopolitonNo ratings yet

- Cuadre de Facturas Cerveceria Polar 1Document6 pagesCuadre de Facturas Cerveceria Polar 1jolyNo ratings yet

- Report Gls 200Document9 pagesReport Gls 200Muhammad AimanNo ratings yet

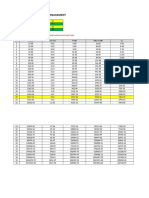

- Trade Bank Money Management: P/s - Sila Letakkan Value Pada Kotak Yang Berwarna Kuning & HijauDocument9 pagesTrade Bank Money Management: P/s - Sila Letakkan Value Pada Kotak Yang Berwarna Kuning & HijauCandra YudaNo ratings yet

- Ejercicio Unidad 3 Estabilidad de TaludesDocument10 pagesEjercicio Unidad 3 Estabilidad de TaludesFERMIN CONDORI QUISPENo ratings yet

- Fund Performance 23 Aug 2021 2052Document6 pagesFund Performance 23 Aug 2021 2052Khushi DaveNo ratings yet

- Sllecllishc@unasam - Edu.pe: Llecllish Carrasco, SchubertDocument48 pagesSllecllishc@unasam - Edu.pe: Llecllish Carrasco, SchubertBenjamin Chumbe RomanNo ratings yet

- Hasil Survei 049 - 11 - K (Jln. D.I. Panjaitan Ketapang)Document18 pagesHasil Survei 049 - 11 - K (Jln. D.I. Panjaitan Ketapang)Tantra WibisonoNo ratings yet

- Time Zone: East - "+", West - "-": ETA CalculationDocument5 pagesTime Zone: East - "+", West - "-": ETA CalculationPavel ViktorNo ratings yet

- Calculate The Standard Deviation by The Deviation Method: Worksheet # 17Document2 pagesCalculate The Standard Deviation by The Deviation Method: Worksheet # 17April CaringalNo ratings yet

- Greenstream Control Rooms' Informations: Mellitah Local Gas Market Gela Offshore PipelineDocument1 pageGreenstream Control Rooms' Informations: Mellitah Local Gas Market Gela Offshore PipelineEhab EzanbouziNo ratings yet

- Pile Capacity Calculation: From The DesignDocument1 pagePile Capacity Calculation: From The DesignthazinNo ratings yet

- Nama: I Made Dana Mulayasa NIM: 202061122015: Kolom 2 X Hujan EfektifDocument6 pagesNama: I Made Dana Mulayasa NIM: 202061122015: Kolom 2 X Hujan EfektifRyan Fernando ExstradapmNo ratings yet

- Design For Duct-1: Straight Duct Friction Loss (How To Decide " Mmaq/M", "Pa/M")Document3 pagesDesign For Duct-1: Straight Duct Friction Loss (How To Decide " Mmaq/M", "Pa/M")Azrinshah Abu BakarNo ratings yet

- Hasil Survey 040 (Temajuk - Merbau) AcDocument343 pagesHasil Survey 040 (Temajuk - Merbau) AcTantra WibisonoNo ratings yet

- Abaqus 3 TutorialDocument2 pagesAbaqus 3 Tutorialmssaber77No ratings yet

- Dinamika Clau PitchingDocument11 pagesDinamika Clau Pitchingclaudia egidiyani1998No ratings yet

- Hybrid Retaining Wall and RE Wall Design and AnalysisDocument22 pagesHybrid Retaining Wall and RE Wall Design and Analysisharshit.rNo ratings yet

- Cost Gang RipDocument5 pagesCost Gang Ripdanny1995No ratings yet

- MACASPAC MARISH QUALITY SYSTEM Activity 4Document25 pagesMACASPAC MARISH QUALITY SYSTEM Activity 4Dranreb Jazzver BautistaNo ratings yet

- Year Month Day Hours Minutes SecondsDocument6 pagesYear Month Day Hours Minutes SecondsMartinNo ratings yet

- Elastic Modulas of Gravel Mix Sand PDFDocument1 pageElastic Modulas of Gravel Mix Sand PDFPrakash Singh RawalNo ratings yet

- Tabel Perhitungan Data Pengukuran Dengan Mistar Ingsut Skala Nonius Hasil Pengukuran A B N X - X (X - X) X - XDocument10 pagesTabel Perhitungan Data Pengukuran Dengan Mistar Ingsut Skala Nonius Hasil Pengukuran A B N X - X (X - X) X - Xaqil murtadhoNo ratings yet

- Stone Column CapacityDocument10 pagesStone Column CapacitySandeep Kumar DangdaNo ratings yet

- Stone Column CapacityDocument10 pagesStone Column CapacityMonal Raj100% (1)

- Yo-Yo IR L1 Test - Time TableDocument1 pageYo-Yo IR L1 Test - Time TableMihai DomsaNo ratings yet

- Ahsp 2022 - 074528Document102 pagesAhsp 2022 - 074528Oni KurniawanNo ratings yet

- Standard I BeamsDocument1 pageStandard I BeamsAlden CayagaNo ratings yet

- Template MpsDocument128 pagesTemplate MpsYan De GuzmanNo ratings yet

- Jesus according to Scripture: Restoring the Portrait from the GospelsFrom EverandJesus according to Scripture: Restoring the Portrait from the GospelsRating: 5 out of 5 stars5/5 (2)

- Yale Night LatchDocument2 pagesYale Night LatchIan FranklinNo ratings yet

- 08 - How To Calculate Breaker Wire Size & WattageDocument1 page08 - How To Calculate Breaker Wire Size & Wattageoadipphone7031No ratings yet

- Cable Table Web PDFDocument1 pageCable Table Web PDFeplan drawingsNo ratings yet

- 2018 WageDocument45 pages2018 WageIan FranklinNo ratings yet

- RMP For Drug Establishments - 26 August 2015 PDFDocument88 pagesRMP For Drug Establishments - 26 August 2015 PDFIan FranklinNo ratings yet

- 08 - How To Calculate Breaker Wire Size & WattageDocument1 page08 - How To Calculate Breaker Wire Size & Wattageoadipphone7031No ratings yet

- Literature Review HRMDocument10 pagesLiterature Review HRMnicksneelNo ratings yet

- Migration Study Report OF Gaisilat Block of Bargarh District of OdishaDocument19 pagesMigration Study Report OF Gaisilat Block of Bargarh District of OdishaDillip naikNo ratings yet

- Supply-Side Determinants of Child LaborDocument11 pagesSupply-Side Determinants of Child LaborAllen AlfredNo ratings yet

- Assign HafizahDocument26 pagesAssign HafizahJAGATHESANNo ratings yet

- Ucrp 1976 Tier Summary Plan DescriptionDocument36 pagesUcrp 1976 Tier Summary Plan DescriptionKhatija Kam100% (1)

- Budgetary ControlDocument11 pagesBudgetary ControlrscjatNo ratings yet

- AddisonEdwards. Economics Notes 2013.2015Document204 pagesAddisonEdwards. Economics Notes 2013.2015KNAH TutoringNo ratings yet

- 02-Capitalizing On Case StudiesDocument4 pages02-Capitalizing On Case StudiesMohamad SidikNo ratings yet

- Very Good Morning To Ladies and Gentlemen Present HereDocument3 pagesVery Good Morning To Ladies and Gentlemen Present HeretusharNo ratings yet

- Instructions: Students May Work in Groups On The Problem Set. Each Student Must Turn in His/her OWNDocument16 pagesInstructions: Students May Work in Groups On The Problem Set. Each Student Must Turn in His/her OWNHamna AzeezNo ratings yet

- Soriano vs. Secretary of Finance G.R. No. 184450 January 24 2017Document1 pageSoriano vs. Secretary of Finance G.R. No. 184450 January 24 2017Anonymous MikI28PkJcNo ratings yet

- EWG Life Sumary of BenefitsDocument4 pagesEWG Life Sumary of BenefitsEnvironmental Working GroupNo ratings yet

- Convoy MKTG V AlbiaDocument16 pagesConvoy MKTG V Albiacarlo_tabangcura100% (1)

- Minimum Wages in Delhi: Revised Rates ofDocument3 pagesMinimum Wages in Delhi: Revised Rates ofkasim_khan07No ratings yet

- Case Study Sample Write UpDocument4 pagesCase Study Sample Write UpMark Roger Huberit IINo ratings yet

- STAFFINGDocument6 pagesSTAFFINGSaloni AgrawalNo ratings yet

- SANTUYO V REMERCO GARMENTS MANUFACTURINGDocument2 pagesSANTUYO V REMERCO GARMENTS MANUFACTURINGMCNo ratings yet

- Personnel Management (Jenny Rose P. Dalmacion)Document62 pagesPersonnel Management (Jenny Rose P. Dalmacion)Jenny Dalmacion100% (1)

- An Assignment On Rana Plaza Impact On Bangladesh Economy ConditionDocument19 pagesAn Assignment On Rana Plaza Impact On Bangladesh Economy ConditionRabiul NahidNo ratings yet

- Theory of ProductionDocument24 pagesTheory of ProductionKafonyi John100% (1)

- Labor Law in SenegalDocument5 pagesLabor Law in SenegalDaouda ThiamNo ratings yet

- Application Word FormatDocument1 pageApplication Word Formatsandeep kumarNo ratings yet

- Kasambahay Law and Maternity Leave LawDocument8 pagesKasambahay Law and Maternity Leave LawJeiel Jill TajanlangitNo ratings yet

- Theory of CostDocument42 pagesTheory of CostSharmaine CangoNo ratings yet

- Recruitment ProcessDocument23 pagesRecruitment ProcessLiyaqath Ali100% (4)

- Work Study IntroductionDocument36 pagesWork Study IntroductionHéctor F BonillaNo ratings yet

- Management Accounting Summer 20091Document18 pagesManagement Accounting Summer 20091MahmozNo ratings yet

- Chapter 6 (Performance Management Linked Reward Systems)Document15 pagesChapter 6 (Performance Management Linked Reward Systems)Soyed Mohammed Zaber HossainNo ratings yet

- Thesis About Del Monte Farm and WorkersDocument96 pagesThesis About Del Monte Farm and WorkersMarry Ellorig100% (1)

- DidiDocument4 pagesDidiSurya GoleyNo ratings yet