You might also like

- Ikea (G)Document3 pagesIkea (G)Afaq ZaimNo ratings yet

- This Study Resource Was Shared Via: Unit 1: Global Tapestry (1200-1450) Review "Brain Dump"Document4 pagesThis Study Resource Was Shared Via: Unit 1: Global Tapestry (1200-1450) Review "Brain Dump"AndreaNo ratings yet

- HER Traffic Forecast Study - Final Report - en - v3Document117 pagesHER Traffic Forecast Study - Final Report - en - v3sbiliristhodNo ratings yet

- Coronavirus Initial Impact AssessmentDocument14 pagesCoronavirus Initial Impact AssessmentJoni SutedjaNo ratings yet

- 2 - IATA-Economic Impact Global OverviewDocument14 pages2 - IATA-Economic Impact Global Overviewمحمود عليمىNo ratings yet

- تقرير اياتاDocument11 pagesتقرير اياتاMohamed MabroukNo ratings yet

- COVID-19: Cost of Air Travel Once Restrictions Start To LiftDocument13 pagesCOVID-19: Cost of Air Travel Once Restrictions Start To LiftSneha BasuNo ratings yet

- MRO OutlookDocument40 pagesMRO OutlookhudaNo ratings yet

- Glo DGF Ocean Market Update May 2023Document18 pagesGlo DGF Ocean Market Update May 2023Cléber MartinezNo ratings yet

- Glo DGF Ocean Market UpdateDocument18 pagesGlo DGF Ocean Market UpdateeifersuchtNo ratings yet

- ICAO Coronavirus Econ Impact PDFDocument110 pagesICAO Coronavirus Econ Impact PDFGreat WishNo ratings yet

- DescargaDocument4 pagesDescargaJorge Ignacio Ramos OlguinNo ratings yet

- Glo DGF Ocean Market UpdateDocument19 pagesGlo DGF Ocean Market UpdateRaja Churchill DassNo ratings yet

- Iata PDFDocument9 pagesIata PDFRaul Hernan Villacorta GarciaNo ratings yet

- ICAO Coronavirus Econ ImpactDocument110 pagesICAO Coronavirus Econ ImpactNikitaNo ratings yet

- ICAO - Coronavirus - Econ - Impact 20210120Document125 pagesICAO - Coronavirus - Econ - Impact 20210120Paola Cemin da SilvaNo ratings yet

- A New Way ForwardDocument21 pagesA New Way Forwardortez.gude8751No ratings yet

- Assignment 1Document8 pagesAssignment 1Krish TyagiNo ratings yet

- Glo DGF Ocean Market UpdateDocument21 pagesGlo DGF Ocean Market UpdateAishabi ShaikhNo ratings yet

- Air Passenger Monthly Analysis - Mar 2020Document4 pagesAir Passenger Monthly Analysis - Mar 2020Satrio AditomoNo ratings yet

- Glo DGF Ocean Market Update EneroDocument19 pagesGlo DGF Ocean Market Update EneroeifersuchtNo ratings yet

- Копия 2021-03-11 - - Q4 - and - 12M - 2020 - IFRS - Results - vF - website1Document47 pagesКопия 2021-03-11 - - Q4 - and - 12M - 2020 - IFRS - Results - vF - website1Irakli TolordavaNo ratings yet

- Infographic ACI World Airport Traffic Forecasts 2017-2040Document1 pageInfographic ACI World Airport Traffic Forecasts 2017-2040Robith Basyarul AlamNo ratings yet

- Covid-19 - The Route To A Planned and Predictable Aviation Industry RecoveryDocument22 pagesCovid-19 - The Route To A Planned and Predictable Aviation Industry RecoverySusheel Kumar SiramNo ratings yet

- Aviation Connects and Unites Us!: Airbus Global Market Forecast 2021 - 2040Document23 pagesAviation Connects and Unites Us!: Airbus Global Market Forecast 2021 - 2040Samy P.GNo ratings yet

- Impact of Covid-19: Fleet & Mro Forecast: WebinarDocument27 pagesImpact of Covid-19: Fleet & Mro Forecast: WebinarJOSE LUIS QUIROSNo ratings yet

- ICAO Coronavirus Econ ImpactDocument125 pagesICAO Coronavirus Econ ImpactPhạm PhátNo ratings yet

- Cruise Line Industry - Statista Dossier 2019Document51 pagesCruise Line Industry - Statista Dossier 2019Raluca UrseNo ratings yet

- COVID 19 Outlook For Airlines' Cash BurnDocument12 pagesCOVID 19 Outlook For Airlines' Cash BurnTatiana RokouNo ratings yet

- Large Turboprop ReportDocument38 pagesLarge Turboprop ReportAndres MoraNo ratings yet

- Investor Presentation - Jan 2024Document46 pagesInvestor Presentation - Jan 2024minhnghia070203No ratings yet

- ICAO Coronavirus Econ ImpactDocument116 pagesICAO Coronavirus Econ ImpactzarifNo ratings yet

- Boeing Current Market Outlook 2013Document37 pagesBoeing Current Market Outlook 2013VaibhavNo ratings yet

- Air Passenger Forecasts Potential Paths For Recovery Into Medium and Long RunDocument23 pagesAir Passenger Forecasts Potential Paths For Recovery Into Medium and Long RunMouhamadou DansokhoNo ratings yet

- 2020 Year in Review 0Document19 pages2020 Year in Review 0Dany QasasNo ratings yet

- DHL Ocean Freight Market Update Sept2017Document18 pagesDHL Ocean Freight Market Update Sept2017soumyarm942No ratings yet

- ICAO Coronavirus Econ ImpactDocument125 pagesICAO Coronavirus Econ ImpactIkram SakoutiNo ratings yet

- DHL ReportDocument21 pagesDHL Reporttarun606No ratings yet

- 0920 MYTDYEi Pax FRTDocument32 pages0920 MYTDYEi Pax FRTMarius BuysNo ratings yet

- Boeing Current Market Outlook 2009 To 2028Document30 pagesBoeing Current Market Outlook 2009 To 2028Jijoo Jacob VargheseNo ratings yet

- Business Challenge For Maverick: Case Study: Gas Turbine Market Analysis For ABC FiltersDocument10 pagesBusiness Challenge For Maverick: Case Study: Gas Turbine Market Analysis For ABC FiltersMai DangNo ratings yet

- Air Care in Brazil DatagraphicsDocument4 pagesAir Care in Brazil DatagraphicsbabiNo ratings yet

- ICAO Coronavirus Econ ImpactDocument125 pagesICAO Coronavirus Econ ImpactRAMADHIAN EKAPUTRANo ratings yet

- Impact Assessment of The COVID-19 Outbreak On International TourismDocument16 pagesImpact Assessment of The COVID-19 Outbreak On International TourismPetrosRochaNo ratings yet

- q2 2019 Earnings Website PresentationDocument16 pagesq2 2019 Earnings Website PresentationTitoNo ratings yet

- Global Hotel IndustryDocument11 pagesGlobal Hotel IndustryJulieNo ratings yet

- 16 December 2020 ReportDocument40 pages16 December 2020 ReportCheah Chee MunNo ratings yet

- Boeing Current Market Outlook 2014Document43 pagesBoeing Current Market Outlook 2014VaibhavNo ratings yet

- DSP The Report Card 1h23Document30 pagesDSP The Report Card 1h23NikhilKapoor29No ratings yet

- ICAO CoronavirusDocument125 pagesICAO CoronavirusUmarul FarooqueNo ratings yet

- Pax Forecast Infographic 2020 FinalDocument1 pagePax Forecast Infographic 2020 Finallibardo silvaNo ratings yet

- Merchandising 17 Trends in Airline AncillariesDocument28 pagesMerchandising 17 Trends in Airline AncillariesYudi NurahmatNo ratings yet

- MGB Accomplishment Report Without FinanceDocument34 pagesMGB Accomplishment Report Without Financeralph vasquezNo ratings yet

- 2021-Downstream Market Cost ProjectionsDocument10 pages2021-Downstream Market Cost ProjectionsAswin Lorenso Gultom NamoralotungNo ratings yet

- Damage Prevention BlaneyDocument28 pagesDamage Prevention BlaneyJHONDURANNo ratings yet

- CR-Hotels-Q3-1-September 2020Document83 pagesCR-Hotels-Q3-1-September 2020Sandhya1No ratings yet

- APATS 2018 Managing Aviation Training IntelligenceDocument27 pagesAPATS 2018 Managing Aviation Training IntelligenceToto Subagyo100% (1)

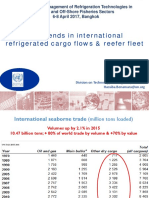

- Key Trends in International Refrigerated Cargo Flows & Reefer FleetDocument21 pagesKey Trends in International Refrigerated Cargo Flows & Reefer FleetMiguel Rodríguez SoutoNo ratings yet

- Iata PDFDocument6 pagesIata PDFTatiana RokouNo ratings yet

- Airline Sector - Monthly Snapshot Oct 09Document2 pagesAirline Sector - Monthly Snapshot Oct 09indianaviationNo ratings yet

- GDP C+I + G + (X-M) : GDP Growth GDP GrowthDocument7 pagesGDP C+I + G + (X-M) : GDP Growth GDP Growthpranjal92pandeyNo ratings yet

- Bangladesh Climate and Disaster Risk Atlas: Hazards—Volume IFrom EverandBangladesh Climate and Disaster Risk Atlas: Hazards—Volume INo ratings yet

- The Greater Mekong Subregion 2030 and Beyond: Integration, Upgrading, Cities, and ConnectivityFrom EverandThe Greater Mekong Subregion 2030 and Beyond: Integration, Upgrading, Cities, and ConnectivityNo ratings yet

- The Paris Cdg2 Hub A Strategic Asset For Airfrance 01Document62 pagesThe Paris Cdg2 Hub A Strategic Asset For Airfrance 01sbiliristhodNo ratings yet

- ΣΤΑΤΙΣΤΙΚΗ ΑΕΡΟΠΟΡΙΚΗΣ ΚΙΝΗΣΗΣ 2017Document169 pagesΣΤΑΤΙΣΤΙΚΗ ΑΕΡΟΠΟΡΙΚΗΣ ΚΙΝΗΣΗΣ 2017sbiliristhodNo ratings yet

- Check-In PartiesDocument1 pageCheck-In PartiessbiliristhodNo ratings yet

- Gekterna Fs Notes 31-12-2018 en PDFDocument232 pagesGekterna Fs Notes 31-12-2018 en PDFsbiliristhodNo ratings yet

- Oregen Wasted Heat Recovery CycleDocument6 pagesOregen Wasted Heat Recovery CyclesbiliristhodNo ratings yet

- Ti 166Document1 pageTi 166MAI_QualityNo ratings yet

- Athens International Airport: Developing Airport Business: The Key Role of Pavements in Airfield InvestmentsDocument47 pagesAthens International Airport: Developing Airport Business: The Key Role of Pavements in Airfield InvestmentssbiliristhodNo ratings yet

- KKS Guidelines - 1AHA062168 - Rev. B PDFDocument26 pagesKKS Guidelines - 1AHA062168 - Rev. B PDFsbiliristhodNo ratings yet

- Power Plants Programme 2014Document138 pagesPower Plants Programme 2014sbiliristhodNo ratings yet

- 1 s2.0 S0141029615004265 MainDocument11 pages1 s2.0 S0141029615004265 Mainmeher chaituNo ratings yet

- ISM3 Conference ProgrammeDocument6 pagesISM3 Conference Programmeno-w-hereNo ratings yet

- Text Museum 02Document4 pagesText Museum 02Aklil YasmineNo ratings yet

- Types of Kung Fu StylesDocument2 pagesTypes of Kung Fu Stylesshaolinkungfu100% (1)

- 108 Chinese New Year Greeting Phrases and SentencesDocument12 pages108 Chinese New Year Greeting Phrases and SentencesVictor ChengNo ratings yet

- The Future of Japans Tourism Full ReportDocument48 pagesThe Future of Japans Tourism Full ReportSam DyerNo ratings yet

- Spring Semester Pae SetsDocument139 pagesSpring Semester Pae SetsgülfemNo ratings yet

- RizalDocument3 pagesRizalAthea Ella B. GanadoNo ratings yet

- Group 5 - Script Mandarin CornerDocument4 pagesGroup 5 - Script Mandarin CornerMUHAMMAD RAGIL SETIAWANNo ratings yet

- Ming-Yan Lai - Nativism and Modernity - Cultural Contestations in China and Taiwan Under Global Capitalism (S U N Y Series, Explorations in Postcolonial Studies) (2008) 2 PDFDocument244 pagesMing-Yan Lai - Nativism and Modernity - Cultural Contestations in China and Taiwan Under Global Capitalism (S U N Y Series, Explorations in Postcolonial Studies) (2008) 2 PDFJayNo ratings yet

- China and The USDocument3 pagesChina and The USjustinescu80No ratings yet

- The Paradigmatic Crisis in Chinese Studies: Paradoxes in Social and Economic HistoryDocument44 pagesThe Paradigmatic Crisis in Chinese Studies: Paradoxes in Social and Economic HistoryYadanarHninNo ratings yet

- Sun BuerDocument4 pagesSun BuerCentre Wudang Taichi-qigongNo ratings yet

- Detente Between China and IndiaDocument230 pagesDetente Between China and IndiaVenkat Naren Karlapalem100% (1)

- Cross-Cultural Leadership in Asia: Neighbors and StrangersDocument5 pagesCross-Cultural Leadership in Asia: Neighbors and StrangersHora Tjitra100% (1)

- Wal-Mart Vs CarrefourDocument7 pagesWal-Mart Vs Carrefourkirin19No ratings yet

- Plato's Main Principles and Ideas About An Ideal State.Document2 pagesPlato's Main Principles and Ideas About An Ideal State.Dan Cociu100% (1)

- Commencing The Dual System: The Yan Kingdom of Mu-Rong XianbeiDocument6 pagesCommencing The Dual System: The Yan Kingdom of Mu-Rong XianbeiIdo ShternNo ratings yet

- International Business - Case - Big Business Is Attractive, With Huge Profits For Some.Document4 pagesInternational Business - Case - Big Business Is Attractive, With Huge Profits For Some.Sailpoint CourseNo ratings yet

- Why Invest in RomaniaDocument21 pagesWhy Invest in RomaniaAlexandru Vlad CiocirlanNo ratings yet

- BASF in Greater China 2016Document32 pagesBASF in Greater China 2016aymanNo ratings yet

- Investment Quarterly: Savills ResearchDocument28 pagesInvestment Quarterly: Savills ResearchArchitecte UrbanisteNo ratings yet

- 024fb4158326e-CLAT Sample Paper 02 QuestionsDocument36 pages024fb4158326e-CLAT Sample Paper 02 QuestionsHackerman FirefreeNo ratings yet

- 300 Beautiful Sentences For TOEFL WritingDocument2 pages300 Beautiful Sentences For TOEFL WritingKathy Thanh PKNo ratings yet

- Shijing 1Document10 pagesShijing 1D CNo ratings yet

- Resrep 21343Document5 pagesResrep 21343Ayush PandeyNo ratings yet

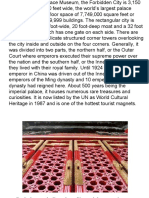

- Forbidden City - ChinaDocument17 pagesForbidden City - ChinaMuhammad Zubair HassanNo ratings yet

- Case Study XDocument12 pagesCase Study XMd. Tanvir HasanNo ratings yet