You might also like

- Industrial Automation and Robotics: Instructio N To CandidatesDocument2 pagesIndustrial Automation and Robotics: Instructio N To CandidatesManoj KumarNo ratings yet

- Production and Operations Management: Instruction To CandidatesDocument2 pagesProduction and Operations Management: Instruction To CandidatesTobalynti TiewsohNo ratings yet

- DWM (5th) May2016Document2 pagesDWM (5th) May2016beebemundeyNo ratings yet

- Digital Signal Processing: Instructions To CandidatesDocument3 pagesDigital Signal Processing: Instructions To CandidatesDr-Mrinal Kanti SarkarNo ratings yet

- Weight and Balance Guide Rev1Document12 pagesWeight and Balance Guide Rev1AndresLopezMllanNo ratings yet

- SCM ASSIGNMENT (Group 6)Document22 pagesSCM ASSIGNMENT (Group 6)ANUSHKANo ratings yet

- MC 1458Document8 pagesMC 1458كردن سيدي محمدNo ratings yet

- Software Engineering: Instruction To CandidatesDocument2 pagesSoftware Engineering: Instruction To CandidatesJibran BashirNo ratings yet

- Victor Brochure VturnII-16 - 20 - 23 - 26 (20091230)Document16 pagesVictor Brochure VturnII-16 - 20 - 23 - 26 (20091230)atif jabbarNo ratings yet

- TDB7910 TDA7910: Medium Power Single Bipolar Operational AmplifierDocument5 pagesTDB7910 TDA7910: Medium Power Single Bipolar Operational AmplifiertommyhghNo ratings yet

- S.No Thirupathi Works Remarks 5 Hamsafer PowercarDocument4 pagesS.No Thirupathi Works Remarks 5 Hamsafer PowercarSowmya DNo ratings yet

- SPM Telemetry CompatibilityDocument1 pageSPM Telemetry CompatibilityAeroinformadoNo ratings yet

- 8130 MLG Main Side Strut Assy PN 2309-3500-503 SN 052Document8 pages8130 MLG Main Side Strut Assy PN 2309-3500-503 SN 052TAR AEROLINEASNo ratings yet

- Ie10 - Schema Tablou Electric Etaj 2.1 Intrare Principala - 15.06.2022Document1 pageIe10 - Schema Tablou Electric Etaj 2.1 Intrare Principala - 15.06.2022Tudor AdremNo ratings yet

- Week 9 - Timing ConstraintsDocument18 pagesWeek 9 - Timing Constraints서종현No ratings yet

- UV Lamp Brochure AHU2Document5 pagesUV Lamp Brochure AHU2Technoserve IndustrialNo ratings yet

- Help Engineering Calculator RacknpinionDocument3 pagesHelp Engineering Calculator RacknpinionMohamed ElshenawyNo ratings yet

- Irrigation Engg.-Ii: Instruction To CandidatesDocument2 pagesIrrigation Engg.-Ii: Instruction To CandidatesHarsh WaliaNo ratings yet

- Rig Com StationDocument4 pagesRig Com StationCristof Naek Halomoan TobingNo ratings yet

- FST-27 (07-01-20247) (E+H) SolutionDocument30 pagesFST-27 (07-01-20247) (E+H) SolutionShreyash AmbarishNo ratings yet

- Quick Guide USB ProgrammerDocument1 pageQuick Guide USB Programmerbala8350No ratings yet

- Aline Alana - ApresentaçãoDocument25 pagesAline Alana - ApresentaçãoALINE ALANA OLIVEIRA SILVANo ratings yet

- Aalborg - EM20230327 - Rotameter - Selection - With ValveDocument3 pagesAalborg - EM20230327 - Rotameter - Selection - With ValveMashi JungNo ratings yet

- RG 0614 RGTGSC HVAC Refrigerant QuantityDocument2 pagesRG 0614 RGTGSC HVAC Refrigerant QuantitySamuel MerticariuNo ratings yet

- Experiment: Design of Synchronous and Asynchronous Counters Design of Mod-5 Synchronous CounterDocument3 pagesExperiment: Design of Synchronous and Asynchronous Counters Design of Mod-5 Synchronous CounterVrushali patilNo ratings yet

- Keiilf: Training ManualDocument53 pagesKeiilf: Training ManualGary GouveiaNo ratings yet

- Aline Alana ApresentaçãoDocument25 pagesAline Alana ApresentaçãoALINE ALANA OLIVEIRA SILVANo ratings yet

- YB SB 00018 2tocounterelectrolyticproblemsDocument4 pagesYB SB 00018 2tocounterelectrolyticproblemssakNo ratings yet

- 1 9:45 OJR Office: Dps Sales & Services Attendence Date:26.10.19 (Satuarday) S.No Name Works RemarksDocument21 pages1 9:45 OJR Office: Dps Sales & Services Attendence Date:26.10.19 (Satuarday) S.No Name Works RemarksSowmya DNo ratings yet

- Engine Data 22 Jul 2020Document1 pageEngine Data 22 Jul 2020permonoNo ratings yet

- 2021.09 BBT ReviewDocument17 pages2021.09 BBT ReviewBBT ProjectNo ratings yet

- SR71 Spares List 01012015Document2 pagesSR71 Spares List 01012015smartechengineering.infoNo ratings yet

- SmartMoor Series II - Mar 2021Document8 pagesSmartMoor Series II - Mar 2021Lovre PerkovićNo ratings yet

- WPC Week 30 (22 - 26 July 2019)Document6 pagesWPC Week 30 (22 - 26 July 2019)Adi SofyanNo ratings yet

- دستور کار آزمایشگاه ترمودینامیکDocument82 pagesدستور کار آزمایشگاه ترمودینامیکghsalma950No ratings yet

- Condensate & CoolingDocument111 pagesCondensate & CoolingSantosh KumarNo ratings yet

- Air Handling Unit 3: Total Air Quantity 12800 CFM Duct Velocity 4000 FPM (Recommended)Document7 pagesAir Handling Unit 3: Total Air Quantity 12800 CFM Duct Velocity 4000 FPM (Recommended)Santos JustinNo ratings yet

- Bill AttachmentDocument8 pagesBill AttachmentAditya arya singhNo ratings yet

- Standard Work Chart: (NVA) (NVA) (NVA)Document2 pagesStandard Work Chart: (NVA) (NVA) (NVA)Carlos Manuel ParionaNo ratings yet

- Interconnecting Piping For Hook Up New Wells at Guebiba ClusterDocument1 pageInterconnecting Piping For Hook Up New Wells at Guebiba ClusterCss SfaxienNo ratings yet

- Pusheph RelayDocument2 pagesPusheph RelayGanesan SankarNo ratings yet

- DataDocument3 pagesDataiaplit2007No ratings yet

- D D D D D D D D D: Description/ordering InformationDocument32 pagesD D D D D D D D D: Description/ordering InformationJuan David Ramirez De Los RiosNo ratings yet

- 74HC190Document30 pages74HC190ikatsirisNo ratings yet

- 2009 City Multi Engineering Manual: Outdoor UnitsDocument82 pages2009 City Multi Engineering Manual: Outdoor Unitsmatt12manyNo ratings yet

- 31G7770191E1Document33 pages31G7770191E1Thomas BarreNo ratings yet

- VMO Draft TemplateDocument23 pagesVMO Draft TemplateJaswasi SahooNo ratings yet

- John Holland CRN TOC 17 Section Pages West v40bDocument33 pagesJohn Holland CRN TOC 17 Section Pages West v40bAaron HoreNo ratings yet

- Electronica2012 PDFDocument66 pagesElectronica2012 PDFOdaliz EspinozaNo ratings yet

- PR 9000 E - Inst Manual (E) (SG14 SE001B - Rev 20170608)Document50 pagesPR 9000 E - Inst Manual (E) (SG14 SE001B - Rev 20170608)Mooi Pang Ng100% (2)

- CM305Document17 pagesCM305api-3853441No ratings yet

- Fla Unit 4Document103 pagesFla Unit 4lard BaringNo ratings yet

- Fla Unit 4 and 5Document198 pagesFla Unit 4 and 5lard BaringNo ratings yet

- S43-19577-20 Contango Group 070120Document3 pagesS43-19577-20 Contango Group 070120contango O&GNo ratings yet

- SN75555FNDocument9 pagesSN75555FNzokiNo ratings yet

- D D D D D D: MC1458, MC1558 Dual General-Purpose Operational AmplifiersDocument5 pagesD D D D D D: MC1458, MC1558 Dual General-Purpose Operational AmplifiersBA BIaNo ratings yet

- 1St Step (Load) 2ND STEP (With Swiping) C.C.R: Date Crane Survey Crane Lighter Name Total RUN Total C.C.R Total CraneDocument1 page1St Step (Load) 2ND STEP (With Swiping) C.C.R: Date Crane Survey Crane Lighter Name Total RUN Total C.C.R Total CraneRubel KaziNo ratings yet

- TestsDocument6 pagesTestsAmirNo ratings yet

- Datasheet PDFDocument10 pagesDatasheet PDFMohammed AliNo ratings yet

- Game Theory 1Document27 pagesGame Theory 1Sunit SomuNo ratings yet

- QA 04 AveragesDocument34 pagesQA 04 AveragesSunit SomuNo ratings yet

- QA 05 Ratio-1Document39 pagesQA 05 Ratio-1Sunit SomuNo ratings yet

- Budget Final PDFDocument1 pageBudget Final PDFSunit SomuNo ratings yet

- Catking SP Jain: Wat Pi WorkbookDocument40 pagesCatking SP Jain: Wat Pi WorkbookSunit SomuNo ratings yet

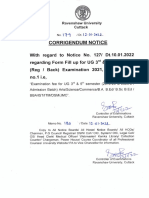

- Corrigendum Notice of Ug 3RD & 5TH Sem Sem Exam, 2021Document1 pageCorrigendum Notice of Ug 3RD & 5TH Sem Sem Exam, 2021Sunit SomuNo ratings yet

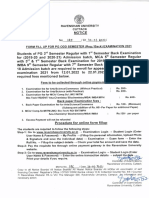

- Form Fill Up Notice For Odd Sem Exam, 2021Document2 pagesForm Fill Up Notice For Odd Sem Exam, 2021Sunit SomuNo ratings yet

- SM1001905 Chapter-1 LinearArrangementDocument7 pagesSM1001905 Chapter-1 LinearArrangementCharlie GoyalNo ratings yet

- Qa 10 TSD-3Document31 pagesQa 10 TSD-3Sunit SomuNo ratings yet

- Qa 08 TSD-1Document38 pagesQa 08 TSD-1Sunit SomuNo ratings yet

- QA 12 Numbers-2Document22 pagesQA 12 Numbers-2Sunit SomuNo ratings yet

- Qa 08 TSD-1Document38 pagesQa 08 TSD-1Sunit SomuNo ratings yet

- QA 06 Ratio-2Document34 pagesQA 06 Ratio-2Sunit SomuNo ratings yet

- Budget Final PDFDocument1 pageBudget Final PDFSunit SomuNo ratings yet

- QA 04 AveragesDocument34 pagesQA 04 AveragesSunit SomuNo ratings yet

- DP IDocument12 pagesDP ISunit SomuNo ratings yet

- LR Chapter 8 - CubesDocument4 pagesLR Chapter 8 - CubesSunit SomuNo ratings yet

- LR Chapter 4 - SelectionsDocument7 pagesLR Chapter 4 - SelectionsSunit SomuNo ratings yet

- 2 Recession Response Asset Assessment WorkSheetDocument1 page2 Recession Response Asset Assessment WorkSheetSunit SomuNo ratings yet

- Budget Final PDFDocument1 pageBudget Final PDFSunit SomuNo ratings yet

- QA 03 Percentage-3Document34 pagesQA 03 Percentage-3Sunit SomuNo ratings yet

- QA 04 AveragesDocument34 pagesQA 04 AveragesSunit SomuNo ratings yet

- LR Chapter 3 - DistributionDocument8 pagesLR Chapter 3 - DistributionVaibhav KumarNo ratings yet

- 01 - Week 1 FAQDocument6 pages01 - Week 1 FAQSunit SomuNo ratings yet

- CA (3rd) May2018Document2 pagesCA (3rd) May2018Sunit SomuNo ratings yet

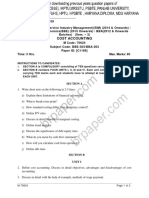

- 4th Sem Costing 2018Document4 pages4th Sem Costing 2018Sunit SomuNo ratings yet

- 3.developing Your Business PlanDocument8 pages3.developing Your Business PlanSunit SomuNo ratings yet

- LR Chapter 1 - Linear ArrangementsDocument7 pagesLR Chapter 1 - Linear ArrangementsSunit SomuNo ratings yet

- CA (3rd) Dec2016Document3 pagesCA (3rd) Dec2016Sunit SomuNo ratings yet

- Data Moneycontrol - Com - Company Info - Print FinancialsDocument2 pagesData Moneycontrol - Com - Company Info - Print FinancialsshreyasNo ratings yet

- COSMY - Perfume & Cosmetic TemplateDocument43 pagesCOSMY - Perfume & Cosmetic Templaterosylia tchitemboNo ratings yet

- Profitability Turnover RatiosDocument32 pagesProfitability Turnover RatiosAnushka JindalNo ratings yet

- Alaska Journal - ConocoPhillipsDocument1 pageAlaska Journal - ConocoPhillipsREandoNo ratings yet

- 460-13-3 Midterm Study QuestionsDocument12 pages460-13-3 Midterm Study QuestionsHarry ZhanNo ratings yet

- Literature Review On Consumer AttitudeDocument8 pagesLiterature Review On Consumer Attitudeaflspyogf100% (1)

- Course Name: Master of Business Administration: Computation of Weighted Average Cost of CapitalDocument8 pagesCourse Name: Master of Business Administration: Computation of Weighted Average Cost of CapitalshriyaNo ratings yet

- 31 - Enano-Bote v. AlvarezDocument4 pages31 - Enano-Bote v. AlvarezWilfredo Guerrero IIINo ratings yet

- Workshop 2 - Customer Service Karen OrtizDocument8 pagesWorkshop 2 - Customer Service Karen OrtizOlga Lucia Escobar SernaNo ratings yet

- Applied Economics Exam 2Document2 pagesApplied Economics Exam 2Rupelma Salazar PatnugotNo ratings yet

- A Study On Financial Planning For Salaried Employee and For Tax Saving at Smik Systems, Coimbatore CityDocument5 pagesA Study On Financial Planning For Salaried Employee and For Tax Saving at Smik Systems, Coimbatore CityAniket MoreNo ratings yet

- PHD Monthly Connect - January'24Document27 pagesPHD Monthly Connect - January'24varun.ramakrishnaNo ratings yet

- Master List of Registered Cooperatives in The PhilippinesDocument1,324 pagesMaster List of Registered Cooperatives in The PhilippinesJahanna MartorillasNo ratings yet

- Projected Profit Rates Feb 2023Document14 pagesProjected Profit Rates Feb 2023adeelNo ratings yet

- Nefas Silk Poly Technic College: Learning GuideDocument39 pagesNefas Silk Poly Technic College: Learning GuideNigussie BerhanuNo ratings yet

- QHSE002 QHSE Manual Rev 0.0 PDFDocument41 pagesQHSE002 QHSE Manual Rev 0.0 PDFRafeeq rahman100% (1)

- Strategic Management Process - A Case Study - BoschDocument10 pagesStrategic Management Process - A Case Study - BoschBhagat Kamra (RA1911011010044)100% (1)

- Working: Lunch Dinner Sales Units 7800 20280 Sales Price 12 25 93600 507000Document8 pagesWorking: Lunch Dinner Sales Units 7800 20280 Sales Price 12 25 93600 507000kudkhanNo ratings yet

- Introduction To Management AccountingDocument37 pagesIntroduction To Management AccountingVin me.No ratings yet

- Sample Stratma of Farmacia DienteDocument33 pagesSample Stratma of Farmacia DienteAILYN GRACE PARENONo ratings yet

- Cau Hoi Unit1Document3 pagesCau Hoi Unit1Hiền HiềnNo ratings yet

- Fall Term 2021: Academic CalendarDocument2 pagesFall Term 2021: Academic CalendarZeeshan AhmadNo ratings yet

- Quiz 2 - Integrated Review AFARDocument9 pagesQuiz 2 - Integrated Review AFAROjims Christjohn C CadungganNo ratings yet

- Management CH 1 Part 1 - Ahmed Yehia - ' Cairo University FCES (Cairo & Zayed) MKTBT NouR - Studocu 2Document1 pageManagement CH 1 Part 1 - Ahmed Yehia - ' Cairo University FCES (Cairo & Zayed) MKTBT NouR - Studocu 2Ahmed FawzyNo ratings yet

- A Study of Recruitment and Selection at Deeesha Fin TechDocument10 pagesA Study of Recruitment and Selection at Deeesha Fin TechAtrangi StoodiyoNo ratings yet

- MARK2007 - Spring 2021 Course SupplementDocument3 pagesMARK2007 - Spring 2021 Course SupplementRaquel Stroher ManoNo ratings yet

- Nissan Intelligent Ownership BrochureDocument4 pagesNissan Intelligent Ownership BrochureJjhdental OpdNo ratings yet

- 419-Article Text-1018-1-10-20191118Document12 pages419-Article Text-1018-1-10-20191118Rejjal As-SaqqāfNo ratings yet

- Chapter 17 Consolidated Fs Part 1 Afar Part 2Document23 pagesChapter 17 Consolidated Fs Part 1 Afar Part 2Kathrina RoxasNo ratings yet

- Transactions That Affect Revenue, Expenses, and Withdrawals: What You'll LearnDocument28 pagesTransactions That Affect Revenue, Expenses, and Withdrawals: What You'll LearnKaden Kelly100% (1)