You might also like

- Continuous Improvement Policy and ProcedureDocument3 pagesContinuous Improvement Policy and ProcedureCandiceNo ratings yet

- Farm HouseDocument14 pagesFarm HousePavan Kumar RanguduNo ratings yet

- Product Recall SOPDocument3 pagesProduct Recall SOPvioletaflora81% (16)

- Article On External and Internal IssuesDocument4 pagesArticle On External and Internal IssuesVIGNESH PNo ratings yet

- Change Management at Dell CorporationDocument21 pagesChange Management at Dell CorporationimuffysNo ratings yet

- PAS 10 Events After The Reporting PeriodDocument2 pagesPAS 10 Events After The Reporting PeriodJennicaBailonNo ratings yet

- Activity 1 - Income and Business Tax (Finals)Document4 pagesActivity 1 - Income and Business Tax (Finals)Jam SurdivillaNo ratings yet

- Conduct ProcurementDocument11 pagesConduct ProcurementRey Dominique VillarNo ratings yet

- BSA Company December journal entries and financial statementsDocument33 pagesBSA Company December journal entries and financial statementsJasmine ActaNo ratings yet

- MODULE 4 - Completing The Accounting Cycle - MerchandisingDocument27 pagesMODULE 4 - Completing The Accounting Cycle - MerchandisingFRANCES JEANALLEN DE JESUSNo ratings yet

- Journal Entries Module 1Document7 pagesJournal Entries Module 1Jervin Maon Velasco100% (1)

- Students Satisfaction On Byju'S Learning App: Project Report Submitted ToDocument75 pagesStudents Satisfaction On Byju'S Learning App: Project Report Submitted ToHemant Deshmukh100% (1)

- Adjusting Entries and Reversing Entries: Arden Trading DECEMBER 31, 2015Document10 pagesAdjusting Entries and Reversing Entries: Arden Trading DECEMBER 31, 2015John Carlo LorenzoNo ratings yet

- 1a Millan Solution Manual 2021 1Document259 pages1a Millan Solution Manual 2021 1avilastephjaneNo ratings yet

- Case Study Analysis - Performance Management at Vitality Health Enterprises Inc - Syndicate 5Document15 pagesCase Study Analysis - Performance Management at Vitality Health Enterprises Inc - Syndicate 5Yocky Tegar HerdiansyahNo ratings yet

- Pamantasan NG Lungsod NG Valenzuela: College of AccountancyDocument2 pagesPamantasan NG Lungsod NG Valenzuela: College of AccountancyPatricia Camille AustriaNo ratings yet

- Chapters 1,2&3Document33 pagesChapters 1,2&3Erika BuenaNo ratings yet

- Activity 25 - Journal Entry To Post-ClosingDocument23 pagesActivity 25 - Journal Entry To Post-ClosingAdam Cuenca100% (1)

- Management Science - HomeworkDocument15 pagesManagement Science - HomeworkVinaNo ratings yet

- Obligation and ContractDocument12 pagesObligation and ContractJae SyNo ratings yet

- Praktiswan Complete WorksheetDocument12 pagesPraktiswan Complete WorksheetMiranda, Aliana Jasmine M.No ratings yet

- 01 - Accounting For Trades and Other ReceivablesDocument5 pages01 - Accounting For Trades and Other ReceivablesCatherine CaleroNo ratings yet

- Valve Market Report ESADocument53 pagesValve Market Report ESAAshwin KumarNo ratings yet

- CFAS MODULE and AssDocument87 pagesCFAS MODULE and AsshellokittysaranghaeNo ratings yet

- Cause and Effect. ManonggalDocument15 pagesCause and Effect. ManonggalMarc Arnyl QuibolNo ratings yet

- Merchandise Inventory For A Personal Computer Would IncludeDocument1 pageMerchandise Inventory For A Personal Computer Would Includejahnhannalei marticioNo ratings yet

- Mle02 Far 1 Answer KeyDocument9 pagesMle02 Far 1 Answer KeyCarNo ratings yet

- May 1 110 P100,000 310: W. Kayayan Accounting Firm General JournalDocument14 pagesMay 1 110 P100,000 310: W. Kayayan Accounting Firm General JournalShania ReighnNo ratings yet

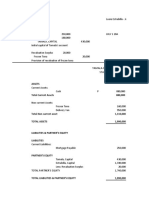

- Tamala and Estrabilla Tuna Fish Business Financial StatementDocument2 pagesTamala and Estrabilla Tuna Fish Business Financial StatementAdam CuencaNo ratings yet

- Chapter 9 Rizal in France and GemanyDocument2 pagesChapter 9 Rizal in France and GemanykennypennyNo ratings yet

- CFAS - Chapter 3: True or FalseDocument1 pageCFAS - Chapter 3: True or Falseagm25No ratings yet

- Accounting Cycle ProblemDocument2 pagesAccounting Cycle ProblemAyeshaNo ratings yet

- Practice Set 1 (Basic Accounting)Document3 pagesPractice Set 1 (Basic Accounting)Maica LagareNo ratings yet

- The AccountDocument12 pagesThe AccountRose PinedaNo ratings yet

- Bank ReconciliationDocument6 pagesBank Reconciliationclarisse jaramillaNo ratings yet

- Intermediate Accounting I - Cash and Cash EquivalentsDocument2 pagesIntermediate Accounting I - Cash and Cash EquivalentsJoovs Joovho0% (1)

- Manunggul-Cave EditedDocument14 pagesManunggul-Cave EditedCoco MartinNo ratings yet

- Trucking and StorageDocument2 pagesTrucking and StorageMichael San Luis100% (1)

- S. Roces (Closing)Document11 pagesS. Roces (Closing)Jesseric RomeroNo ratings yet

- ULTRA TRADINGDocument16 pagesULTRA TRADINGRonNo ratings yet

- Short Case ActivitiesDocument2 pagesShort Case ActivitiesRaff LesiaaNo ratings yet

- Stevenson 14e Ch01writingDocument2 pagesStevenson 14e Ch01writingelvis oheneba manuNo ratings yet

- Analyze The Political Economic Cultural and Social Factors Underlying The Global Movements of PeoDocument1 pageAnalyze The Political Economic Cultural and Social Factors Underlying The Global Movements of PeoKarylle SabaldanNo ratings yet

- Cavite MutinyDocument9 pagesCavite MutinyRuby Ann Rubio100% (1)

- Problem 5-1 PDFDocument1 pageProblem 5-1 PDFJaira AsuncionNo ratings yet

- Understand Bank Reconciliation with 20 Multiple Choice and True or False QuestionsDocument3 pagesUnderstand Bank Reconciliation with 20 Multiple Choice and True or False QuestionsRejie AndoNo ratings yet

- Reconciling bank and book cash balancesDocument4 pagesReconciling bank and book cash balancesRon MagnoNo ratings yet

- Lim Tong Lim v. Phil Fishing Gear IndustriesDocument10 pagesLim Tong Lim v. Phil Fishing Gear IndustriesPatrick Jorge SibayanNo ratings yet

- Acct 1abDocument73 pagesAcct 1abXivaughn SebastianNo ratings yet

- Intermediate Accounting 1 Departmental Exam MidtermsDocument6 pagesIntermediate Accounting 1 Departmental Exam MidtermsCharles AtimNo ratings yet

- Reflection Paper Enm 211: Organization and Management: Nueva Ecija University of Science and TechnologyDocument3 pagesReflection Paper Enm 211: Organization and Management: Nueva Ecija University of Science and TechnologyIdaniel Ilai DavidNo ratings yet

- My Company Unadjusted Trial Balance December 31, 2018 Debit CreditDocument9 pagesMy Company Unadjusted Trial Balance December 31, 2018 Debit CreditRey Joyce AbuelNo ratings yet

- ACPS 1 Complete SolutionsDocument2 pagesACPS 1 Complete SolutionsArnel Olsim0% (1)

- Why Burundi Remains One of the Poorest CountriesDocument2 pagesWhy Burundi Remains One of the Poorest CountriesThird MontefalcoNo ratings yet

- Bam 040 ReviewerDocument7 pagesBam 040 ReviewerAndrea Vila VelascoNo ratings yet

- Receivable FinancingDocument15 pagesReceivable FinancingshaneNo ratings yet

- Zayat - Elaborate (Ghist 1752)Document2 pagesZayat - Elaborate (Ghist 1752)Joaquin ZayatNo ratings yet

- The Year 1872 There Are 2 Historical EventsDocument2 pagesThe Year 1872 There Are 2 Historical EventsMonina AmanoNo ratings yet

- Ethics vs Morals: Understanding the Key DifferencesDocument8 pagesEthics vs Morals: Understanding the Key DifferencesChristopher PantojaNo ratings yet

- Hbo Chapter 17Document2 pagesHbo Chapter 17Diosdado IV GALVEZNo ratings yet

- Mira's School Supplies Store Financial AnalysisDocument1 pageMira's School Supplies Store Financial AnalysisMiguel Lulab100% (1)

- Activities 1-5 - BoncalesDocument12 pagesActivities 1-5 - BoncalesBraille Boncales100% (1)

- Answer Problem 1Document9 pagesAnswer Problem 1MARY JUSTINE PAQUIBOTNo ratings yet

- Ias 1 Presentation of Financial StatementsDocument30 pagesIas 1 Presentation of Financial Statementsesulawyer2001No ratings yet

- 1 Cfas - Chapter 4 - Exercise 1Document8 pages1 Cfas - Chapter 4 - Exercise 1Danica CatalanNo ratings yet

- Final Theories ReviewerDocument16 pagesFinal Theories Reviewermary jane facerondaNo ratings yet

- CFAS DiscussionDocument5 pagesCFAS DiscussionXiunah MinynneNo ratings yet

- Pas 1 Presentation of Financial StatementsDocument16 pagesPas 1 Presentation of Financial StatementsJustine VeralloNo ratings yet

- Chapter 14 Financial StatementsDocument82 pagesChapter 14 Financial StatementsKate CuencaNo ratings yet

- Google Drive: (CITATION Bet13 /L 1033) (CITATION Sot12 /L 1033)Document2 pagesGoogle Drive: (CITATION Bet13 /L 1033) (CITATION Sot12 /L 1033)PATRICIA SANTOSNo ratings yet

- Santos 1a11Document2 pagesSantos 1a11PATRICIA SANTOSNo ratings yet

- A. Plan and RationaleDocument8 pagesA. Plan and RationalePATRICIA SANTOSNo ratings yet

- (CITATION Cod16 /L 1033) (CITATION H3V19 /L 1033)Document4 pages(CITATION Cod16 /L 1033) (CITATION H3V19 /L 1033)PATRICIA SANTOSNo ratings yet

- DIVING MUSCLESDocument2 pagesDIVING MUSCLESPATRICIA SANTOSNo ratings yet

- Conceptual Framework and Accounting StandardsDocument8 pagesConceptual Framework and Accounting StandardsPATRICIA SANTOSNo ratings yet

- Answers To True or False, Relating To SFP, With ExplanationsDocument3 pagesAnswers To True or False, Relating To SFP, With ExplanationsPATRICIA SANTOS100% (1)

- Answers To True or False, Relating To SFP, With ExplanationsDocument3 pagesAnswers To True or False, Relating To SFP, With ExplanationsPATRICIA SANTOS100% (1)

- Cfas AnswersDocument5 pagesCfas AnswersPATRICIA SANTOSNo ratings yet

- Ca5106: Conceptual Framework and Accounting StandardsDocument1 pageCa5106: Conceptual Framework and Accounting StandardsPATRICIA SANTOSNo ratings yet

- Cfas AnswersDocument5 pagesCfas AnswersPATRICIA SANTOSNo ratings yet

- CA5106: Liability ClassificationDocument3 pagesCA5106: Liability ClassificationPATRICIA SANTOSNo ratings yet

- Abc 2020Document9 pagesAbc 2020PATRICIA SANTOSNo ratings yet

- Reviewer From Idk WhereDocument10 pagesReviewer From Idk WherePATRICIA SANTOSNo ratings yet

- The Accounting and Business Environment: After Reading This Chapter, The Learners Should Be Able ToDocument14 pagesThe Accounting and Business Environment: After Reading This Chapter, The Learners Should Be Able ToPATRICIA SANTOSNo ratings yet

- Chapter 2 EditedDocument10 pagesChapter 2 EditedJULIANNE CLARISSE JIMENEZNo ratings yet

- CA Final Mock Test Paper 2 SolutionsDocument19 pagesCA Final Mock Test Paper 2 SolutionsdikshaNo ratings yet

- Staples IncDocument4 pagesStaples IncNo nameNo ratings yet

- Tax InvoiceDocument1 pageTax InvoiceHsnsbsNo ratings yet

- CII Duff & Phelps Report On Using IP As Collateral 2019Document35 pagesCII Duff & Phelps Report On Using IP As Collateral 2019shoumikNo ratings yet

- Ch.1 - Introduction To AdvertisingDocument27 pagesCh.1 - Introduction To AdvertisingYousra Mohamed Fawzy Ali GabrNo ratings yet

- Digital-Banking-Presentation-Sept-2021 - Axis BankDocument91 pagesDigital-Banking-Presentation-Sept-2021 - Axis Bankv1997inNo ratings yet

- Business Organisation ProjectDocument8 pagesBusiness Organisation ProjectGAME SPOT TAMIZHANNo ratings yet

- Ermiyas TeshomeDocument129 pagesErmiyas Teshomeshambel asfawNo ratings yet

- Rushikesh Mane EDA Capstone Project On Hotel Booking AnalysisDocument22 pagesRushikesh Mane EDA Capstone Project On Hotel Booking AnalysisDevendra kushwahNo ratings yet

- ERP Project TimelineDocument4 pagesERP Project TimelineAdebola OgunleyeNo ratings yet

- Ril Pe Price DT.16.01.2019 PDFDocument86 pagesRil Pe Price DT.16.01.2019 PDFAkshat JainNo ratings yet

- Passenger Terminal Expansion Works Materials CatalogueDocument82 pagesPassenger Terminal Expansion Works Materials CatalogueMariam MousaNo ratings yet

- FAC11A1Document9 pagesFAC11A1sacey20.hbNo ratings yet

- 5 6079871711837160054Document566 pages5 6079871711837160054Mehak KaushikkNo ratings yet

- Personal Branding Persevering Towards Success Leza KlenkDocument13 pagesPersonal Branding Persevering Towards Success Leza KlenkPrabhuNo ratings yet

- Absolute Sale: Understanding the Key Legal DocumentDocument1 pageAbsolute Sale: Understanding the Key Legal DocumentcondorianoNo ratings yet

- NINER REVIEW CENTER: THE RISE OF THE FIRST IELTS REVIEW CENTER IN THE PHILIPPINESDocument8 pagesNINER REVIEW CENTER: THE RISE OF THE FIRST IELTS REVIEW CENTER IN THE PHILIPPINESPeter Andre GuintoNo ratings yet

- Strategies for Customer Relationship ManagementDocument26 pagesStrategies for Customer Relationship Managementprince100% (3)

- PIP - One Time CleansingDocument5 pagesPIP - One Time Cleansingcpscmain.supplyNo ratings yet

- Prequalification Checklist Form: ANNEX-D (Returnable Form) Infrastructure Services: ContractorsDocument2 pagesPrequalification Checklist Form: ANNEX-D (Returnable Form) Infrastructure Services: ContractorsJavier ContrerasNo ratings yet

- UCODocument9 pagesUCOjamy2goaNo ratings yet