You might also like

- Financial Derivative and Energy Market Valuation: Theory and Implementation in MATLABFrom EverandFinancial Derivative and Energy Market Valuation: Theory and Implementation in MATLABRating: 3.5 out of 5 stars3.5/5 (1)

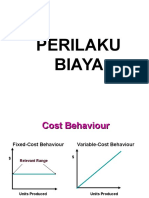

- Lecture 6 - Cost BehaviourDocument27 pagesLecture 6 - Cost BehaviourOphelia MensahNo ratings yet

- Accounting and Finance Formulas: A Simple IntroductionFrom EverandAccounting and Finance Formulas: A Simple IntroductionRating: 4 out of 5 stars4/5 (8)

- Understanding Cost Behavior and Analysis TechniquesDocument65 pagesUnderstanding Cost Behavior and Analysis TechniquesGabai AsaiNo ratings yet

- 2 Cost Concept and Cost Behavior1Document31 pages2 Cost Concept and Cost Behavior1Divine MungcalNo ratings yet

- Lecture 3 - Cost Behavior (Analysis and Uses)Document17 pagesLecture 3 - Cost Behavior (Analysis and Uses)RODOLFO AUSTRIA JR.No ratings yet

- 3.1 Definition and Application of Cost Behaviour ConceptDocument6 pages3.1 Definition and Application of Cost Behaviour ConceptPrince PierreNo ratings yet

- Costs: Costs Are Different From ExpensesDocument26 pagesCosts: Costs Are Different From Expensesnuwany2kNo ratings yet

- Chapter 10 CostDocument17 pagesChapter 10 Costالمنتج عمرNo ratings yet

- Statistical Techniques PDFDocument24 pagesStatistical Techniques PDFMatlokotsi SenekaneNo ratings yet

- Assumptions About Cost Behaviour: Prepared By: Talha Majeed Khan (M.Phil) Lecturer UCP, Faculty of Management StudiesDocument8 pagesAssumptions About Cost Behaviour: Prepared By: Talha Majeed Khan (M.Phil) Lecturer UCP, Faculty of Management StudieszubairNo ratings yet

- 2 CMA CostSystemsDocument28 pages2 CMA CostSystemsBushra FatimaNo ratings yet

- Cost Behavior AnalysisDocument30 pagesCost Behavior AnalysisMaha IqrarNo ratings yet

- Classification of CostDocument51 pagesClassification of CostSuman Samal MagarNo ratings yet

- CMA Part 2 Financial Decision Making: CVP Analysis and Marginal AnalysisDocument85 pagesCMA Part 2 Financial Decision Making: CVP Analysis and Marginal AnalysisNEERAJ GUPTANo ratings yet

- MPA 602: Analyze Cost Behavior and Estimation TechniquesDocument33 pagesMPA 602: Analyze Cost Behavior and Estimation TechniquesMd. ZakariaNo ratings yet

- Cost Behaviour and Cost-Volume-Profit (CVP) AnalysisDocument21 pagesCost Behaviour and Cost-Volume-Profit (CVP) AnalysisEugene TeoNo ratings yet

- Cost Behavior AnalysisDocument4 pagesCost Behavior AnalysisHafsah Amod DisomangcopNo ratings yet

- Classification of CostDocument50 pagesClassification of CostSuman Samal MagarNo ratings yet

- Acct403 Cost Behaviour and EstimationDocument62 pagesAcct403 Cost Behaviour and EstimationLEDORNU LEGBARANo ratings yet

- 2 - Cost Concepts and BehaviorsDocument4 pages2 - Cost Concepts and BehaviorsKaryl FailmaNo ratings yet

- Fundamentals of Management Accounting: Cima Ba2Document133 pagesFundamentals of Management Accounting: Cima Ba2Arsalan Ali100% (1)

- Cost-Volume-Profit Analysis: RevenuesDocument39 pagesCost-Volume-Profit Analysis: RevenuesDiane PascualNo ratings yet

- Biaya Perilaku dan Model Biaya AktivitasDocument24 pagesBiaya Perilaku dan Model Biaya AktivitasAchmadFahrizalNo ratings yet

- Mixed CostDocument4 pagesMixed CostPeter WagdyNo ratings yet

- MAS-01 Cost Behavior AnalysisDocument6 pagesMAS-01 Cost Behavior AnalysisPaupauNo ratings yet

- Cost Volume Profit AnalysisDocument25 pagesCost Volume Profit AnalysisAmit DeyNo ratings yet

- Managerial Accounting Managerial AccountingDocument30 pagesManagerial Accounting Managerial Accountingpvsk17072005No ratings yet

- Be AnalysisDocument32 pagesBe AnalysisMuskan GoyalNo ratings yet

- Module - 3 Theory of CostDocument47 pagesModule - 3 Theory of Costlakshmi dileepNo ratings yet

- Cost Classification As To Behavior - Variable - Fixed - Mixed (Semi-Variable/semi-Fixed)Document2 pagesCost Classification As To Behavior - Variable - Fixed - Mixed (Semi-Variable/semi-Fixed)Aaron CantonesNo ratings yet

- MasterbudgetDocument154 pagesMasterbudgetrochielanciolaNo ratings yet

- MALec Batch 2Document105 pagesMALec Batch 2duong duongNo ratings yet

- Unit 6 MANAGEMENT ACCOUNTINGDocument46 pagesUnit 6 MANAGEMENT ACCOUNTINGSANDFORD MALULUNo ratings yet

- CostDocument9 pagesCostTanya AroraNo ratings yet

- 1-Cost Classfication and Behaviours PDFDocument2 pages1-Cost Classfication and Behaviours PDFMuhammad Usman FareedNo ratings yet

- Module-2-UE-F2F-Cost-Behavior-Answer 2Document31 pagesModule-2-UE-F2F-Cost-Behavior-Answer 2Sophia DayaoNo ratings yet

- Chap2b FacilitieslayoutamaterialshandlingDocument28 pagesChap2b Facilitieslayoutamaterialshandlingdhinesh kumarNo ratings yet

- Understand Cost-Volume-Profit (CVP) AnalysisDocument39 pagesUnderstand Cost-Volume-Profit (CVP) AnalysisVandana SharmaNo ratings yet

- Cost-Volume-Profit Analysis and ABC ChapterDocument63 pagesCost-Volume-Profit Analysis and ABC ChapterGizachewNo ratings yet

- CVP AnalysisDocument21 pagesCVP AnalysisDaksh AnejaNo ratings yet

- Cost Behaviour-1Document20 pagesCost Behaviour-1MatinChris KisomboNo ratings yet

- M10 CVP RelationshipDocument72 pagesM10 CVP Relationship3ID04Viviani RaraNo ratings yet

- 4.basics of Marginal Costing-SN FoundationDocument22 pages4.basics of Marginal Costing-SN FoundationHasim SaiyedNo ratings yet

- Ammar ch2Document14 pagesAmmar ch2Dania Al-ȜbadiNo ratings yet

- Block 5 MCO 5 Unit 5Document27 pagesBlock 5 MCO 5 Unit 5Tushar SharmaNo ratings yet

- Edited Farm ManagmentDocument27 pagesEdited Farm Managmentjohn pierreNo ratings yet

- CMA Part 1 Sec CDocument131 pagesCMA Part 1 Sec CMusthaqMohammedMadathilNo ratings yet

- Cost-Volume-Profit RelationshipsDocument72 pagesCost-Volume-Profit RelationshipsFantahun kebedeNo ratings yet

- 1 Cost in Management AccountingDocument15 pages1 Cost in Management AccountingAphol Joyce MortelNo ratings yet

- Cost Analysis BreakdownDocument13 pagesCost Analysis BreakdownNouman BaigNo ratings yet

- Mixed CostsDocument28 pagesMixed CostsBrix ArriolaNo ratings yet

- Ch-13 The Cost of ProductDocument46 pagesCh-13 The Cost of ProductDarshan VadherNo ratings yet

- Cost Classification Based On Cost BehaviorDocument38 pagesCost Classification Based On Cost Behaviorshriya2413No ratings yet

- Costs and Cost Concepts: Different Costs For Different PurposesDocument11 pagesCosts and Cost Concepts: Different Costs For Different PurposesAudie Anthony Palpal-latocNo ratings yet

- CVP analysis: Cost-volume-profit analysis guideDocument21 pagesCVP analysis: Cost-volume-profit analysis guiderangoli maheshwariNo ratings yet

- Weygandt, Kieso, & Kimmel: Managerial AccountingDocument74 pagesWeygandt, Kieso, & Kimmel: Managerial Accountingخـــتــام عبد زيدNo ratings yet

- Management Accounting Systems ComparisonDocument39 pagesManagement Accounting Systems ComparisonPintér BarnabásNo ratings yet

- Acct 202 Ch5Document39 pagesAcct 202 Ch5Hải Anh LươngNo ratings yet

- Lecture Note On - COST-VOLUME-PROFIT RELATIONSHIPS 22.10.2018Document47 pagesLecture Note On - COST-VOLUME-PROFIT RELATIONSHIPS 22.10.2018Tejaswi BandlamudiNo ratings yet

- Fin286 Week 3Document4 pagesFin286 Week 3Claudette ClementeNo ratings yet

- FIN286 Notes 8Document3 pagesFIN286 Notes 8Claudette ClementeNo ratings yet

- FIN286 Presentation 7Document2 pagesFIN286 Presentation 7Claudette ClementeNo ratings yet

- FIN286 Summary 8Document4 pagesFIN286 Summary 8Claudette ClementeNo ratings yet

- FIN286 Problems 4Document7 pagesFIN286 Problems 4Claudette ClementeNo ratings yet

- FIN286 Exam 5Document5 pagesFIN286 Exam 5Claudette ClementeNo ratings yet

- FIN286 Answers 3Document5 pagesFIN286 Answers 3Claudette ClementeNo ratings yet

- Week 1Document3 pagesWeek 1Claudette ClementeNo ratings yet

- Cfed Week 1-5Document11 pagesCfed Week 1-5Claudette ClementeNo ratings yet

- University of Saint Louis: National Service Training Program Short Term A.Y. 2020-2021Document15 pagesUniversity of Saint Louis: National Service Training Program Short Term A.Y. 2020-2021Claudette ClementeNo ratings yet

- Groningen Growth and Development Centre, Faculty of Economics, University of GroningenDocument32 pagesGroningen Growth and Development Centre, Faculty of Economics, University of GroningenClaudette ClementeNo ratings yet

- Correspondence Learning Module NSTP 1023 (National Service Training Program 2) Module 1: Introduction To Community Engagament and Development TopicsDocument26 pagesCorrespondence Learning Module NSTP 1023 (National Service Training Program 2) Module 1: Introduction To Community Engagament and Development TopicsClaudette ClementeNo ratings yet

- Important Elements in Strong ArgumentsDocument3 pagesImportant Elements in Strong ArgumentsClaudette ClementeNo ratings yet

- Fin286 Pre Lab 5Document5 pagesFin286 Pre Lab 5Claudette ClementeNo ratings yet

- This Study Resource WasDocument2 pagesThis Study Resource WasClaudette ClementeNo ratings yet

- Partnership Accounting: - Partner Capital AccountsDocument22 pagesPartnership Accounting: - Partner Capital AccountsPhilip K BugaNo ratings yet

- Week 2Document5 pagesWeek 2Claudette ClementeNo ratings yet

- Special Journals (Purchase) : Exercise 5.7Document12 pagesSpecial Journals (Purchase) : Exercise 5.7Claudette ClementeNo ratings yet

- Answer Keys AIS FINAL EXAMDocument10 pagesAnswer Keys AIS FINAL EXAMClaudette ClementeNo ratings yet

- Response Paper SampleDocument3 pagesResponse Paper SampleClaudette ClementeNo ratings yet

- Trial Balance: ABC EnterprisesDocument6 pagesTrial Balance: ABC EnterprisesClaudette ClementeNo ratings yet

- Quiz LaterDocument2 pagesQuiz LaterClaudette ClementeNo ratings yet

- Ais Final QuizDocument5 pagesAis Final QuizClaudette ClementeNo ratings yet

- This Study Resource Was: Use The Following Information For The Next Two QuestionsDocument2 pagesThis Study Resource Was: Use The Following Information For The Next Two QuestionsClaudette Clemente100% (1)

- Hence Amount of Current Liability 20,00,000+50,00,000 70,00,000Document1 pageHence Amount of Current Liability 20,00,000+50,00,000 70,00,000Claudette ClementeNo ratings yet

- ICT - 1 - Inventory ManagementDocument4 pagesICT - 1 - Inventory ManagementClaudette ClementeNo ratings yet

- Trial Balance: ABC EnterprisesDocument6 pagesTrial Balance: ABC EnterprisesClaudette ClementeNo ratings yet

- Current Liabilities ProblemsDocument6 pagesCurrent Liabilities ProblemsClaudette ClementeNo ratings yet

- Just-in-Time and Backflushing Costing TechniquesDocument6 pagesJust-in-Time and Backflushing Costing TechniquesClaudette ClementeNo ratings yet

- The Church's Link to Jesus Obligates MissionDocument7 pagesThe Church's Link to Jesus Obligates MissionClaudette ClementeNo ratings yet

- 10-Correlation and Linear RegressionDocument25 pages10-Correlation and Linear RegressionKarazayNo ratings yet

- Multiple Regression EstimationDocument18 pagesMultiple Regression EstimationSakshi VashishthaNo ratings yet

- Chapter 3 - Planning Resources - FULLDocument56 pagesChapter 3 - Planning Resources - FULLAnh Lương QuỳnhNo ratings yet

- SLR NotesDocument96 pagesSLR NotesRafi DawarNo ratings yet

- Young Et Al 2016 Role of Trust in Resolution of Conservation ConflictsDocument7 pagesYoung Et Al 2016 Role of Trust in Resolution of Conservation ConflictsAcinom OjivalcNo ratings yet

- Levine Smume7 Bonus Ch13Document2 pagesLevine Smume7 Bonus Ch13Kiran SoniNo ratings yet

- Sorting Variables by Using Informative Vectors As A Strategy For Feature Selection in Multivariate RegressionDocument17 pagesSorting Variables by Using Informative Vectors As A Strategy For Feature Selection in Multivariate RegressionALDO JAVIER GUZMAN DUXTANNo ratings yet

- What's Up For Today's Session?: Regression EquationDocument12 pagesWhat's Up For Today's Session?: Regression EquationRochelle AlmeraNo ratings yet

- Pset 6 - Fall2019 - Solutions PDFDocument33 pagesPset 6 - Fall2019 - Solutions PDFjoshua arnett100% (3)

- Balancing of RotorsDocument20 pagesBalancing of RotorsChetan Mistry100% (1)

- FF654 Final-Syllabus SY Common - Sem 2 AY 2020-21Document40 pagesFF654 Final-Syllabus SY Common - Sem 2 AY 2020-21My NameNo ratings yet

- 102-Article Text-278-1-10-20210227Document7 pages102-Article Text-278-1-10-20210227andis p17No ratings yet

- Trend Analysis and ForecastingDocument24 pagesTrend Analysis and ForecastingMICHAEL MEDINA FLORESNo ratings yet

- Ordered Logit ModelDocument4 pagesOrdered Logit Modelmengistu jiloNo ratings yet

- Baum - An Introduction To Modern Econometrics Using StataDocument376 pagesBaum - An Introduction To Modern Econometrics Using StataVelichka Dimitrova100% (1)

- Paper Review by Daniel AwokeDocument11 pagesPaper Review by Daniel AwokeDani Azmi AwokeNo ratings yet

- Research On Automobile Exterior Color AnDocument9 pagesResearch On Automobile Exterior Color AnChandrasekar SekarNo ratings yet

- R basics: Intro, stats, data analysisDocument4 pagesR basics: Intro, stats, data analysishazel nuttNo ratings yet

- SRT 605 - Topic (10) SLRDocument39 pagesSRT 605 - Topic (10) SLRpugNo ratings yet

- Student Performance Analysis Based On IQ and EI Using MLDocument6 pagesStudent Performance Analysis Based On IQ and EI Using MLIJRASETPublicationsNo ratings yet

- Road Fatalities in KuwaitDocument5 pagesRoad Fatalities in Kuwaitleonardo.cotrufoNo ratings yet

- Siop Lesson PlanDocument7 pagesSiop Lesson Planapi-589124264No ratings yet

- Fuzzy Logic - Algorithms Techniques and ImplementationsDocument294 pagesFuzzy Logic - Algorithms Techniques and ImplementationsjesusortegavNo ratings yet

- Cma p1 Mock Exam 2 ADocument34 pagesCma p1 Mock Exam 2 ATalalTANo ratings yet

- Vonblanckenburg 2020Document7 pagesVonblanckenburg 2020Yutika JasvitaNo ratings yet

- Chapter 11Document22 pagesChapter 11anggiNo ratings yet

- R Programming Data Science & Machine Learning CourseDocument6 pagesR Programming Data Science & Machine Learning CourseVikram SinghNo ratings yet

- Effects of Employee Training On Employee Performance: A Case of The Judiciary of KenyaDocument9 pagesEffects of Employee Training On Employee Performance: A Case of The Judiciary of KenyaSalman Hussain KazimNo ratings yet

- Chapter 2 (Econometrics)Document36 pagesChapter 2 (Econometrics)Rajan NandolaNo ratings yet

- 14 Statistics and ProbabilityDocument37 pages14 Statistics and ProbabilityMuhammad AliNo ratings yet