You might also like

- AFAR - Revenue Recognition 2019Document4 pagesAFAR - Revenue Recognition 2019Joanna Rose DeciarNo ratings yet

- Sharpened AMA12v2.0 PDFDocument6 pagesSharpened AMA12v2.0 PDFbelle100% (1)

- Section 68 (2020)Document10 pagesSection 68 (2020)ungku bahiyahNo ratings yet

- Long Term Construction Contracts Special Revenue Recognition JLM Illustrative Problems Problem 1 PDF FreeDocument5 pagesLong Term Construction Contracts Special Revenue Recognition JLM Illustrative Problems Problem 1 PDF FreeMichael Brian TorresNo ratings yet

- 13 Long Term Construction ContractsDocument2 pages13 Long Term Construction ContractsJem ValmonteNo ratings yet

- P2 Construction Contract - GuerreroDocument22 pagesP2 Construction Contract - GuerreroCelen OchocoNo ratings yet

- Long-Term Construction Contracts (Special Revenue Recognition) JLM Illustrative Problems Problem 1Document5 pagesLong-Term Construction Contracts (Special Revenue Recognition) JLM Illustrative Problems Problem 1Divine Cuasay100% (1)

- BQ PUSPEN SERI ISKANDAR - KontraktorDocument8 pagesBQ PUSPEN SERI ISKANDAR - KontraktorRYB ResourcesNo ratings yet

- Quiz 3 QuestionsDocument7 pagesQuiz 3 QuestionsVernnNo ratings yet

- 9006 - LTCC SolutionsDocument9 pages9006 - LTCC SolutionsFrancis Vonn Tapang100% (1)

- Accounting For LTCCDocument5 pagesAccounting For LTCCRoland CatubigNo ratings yet

- ACC110 P2 Q2 Answer - Docx 2Document13 pagesACC110 P2 Q2 Answer - Docx 2Sherwin SarzueloNo ratings yet

- ACCTG 7 - Final Exam V2Document10 pagesACCTG 7 - Final Exam V2Sarah Balisacan0% (2)

- LTCCDocument7 pagesLTCCGenesis Dizon67% (6)

- Quiz 3 Construction ContractsDocument7 pagesQuiz 3 Construction ContractsMarinel Mae Chica100% (2)

- 2 Contract-CostingDocument25 pages2 Contract-CostingBhavika GuptaNo ratings yet

- Final Examination Final ExaminationDocument14 pagesFinal Examination Final ExaminationTricia Mae FernandezNo ratings yet

- Merger and Acquisition StrategiesDocument45 pagesMerger and Acquisition Strategies--bolabolaNo ratings yet

- AFAR Self Test - 9002Document7 pagesAFAR Self Test - 9002Jennifer RueloNo ratings yet

- Construction Contracts Seatwork PDFDocument13 pagesConstruction Contracts Seatwork PDFaccounting prob100% (1)

- Solution Manual Contemporary Issues in Accounting 1st Edition by Michaela Rankin slw1027 PDF FreeDocument46 pagesSolution Manual Contemporary Issues in Accounting 1st Edition by Michaela Rankin slw1027 PDF Free--bolabola100% (1)

- Topic 13 Strategic EntrepreneurshipDocument43 pagesTopic 13 Strategic Entrepreneurship--bolabolaNo ratings yet

- Toaz - Info Acc110 p2 Quiz 2 Answers Construction Contracts 1 PRDocument10 pagesToaz - Info Acc110 p2 Quiz 2 Answers Construction Contracts 1 PRKimberly Claire AtienzaNo ratings yet

- Long-Term Construction QuizDocument4 pagesLong-Term Construction QuizCattleyaNo ratings yet

- Chapter 6 - Risk ManagementDocument76 pagesChapter 6 - Risk Management--bolabolaNo ratings yet

- Bill Statement: Previous Charges Amount (RM) Current Charges Amount (RM)Document7 pagesBill Statement: Previous Charges Amount (RM) Current Charges Amount (RM)WM Iskandar100% (1)

- Managing Successful Projects with PRINCE2 2009 EditionFrom EverandManaging Successful Projects with PRINCE2 2009 EditionRating: 4 out of 5 stars4/5 (3)

- Topic 9 Cooperative StrategyDocument46 pagesTopic 9 Cooperative Strategy--bolabolaNo ratings yet

- Percentage of Completion 33.33%Document6 pagesPercentage of Completion 33.33%AlexNo ratings yet

- Acc110p2quiz 2answers Construction Contracts 1 PDF FreeDocument10 pagesAcc110p2quiz 2answers Construction Contracts 1 PDF FreeMichael Brian TorresNo ratings yet

- Cebu Institute of Technology - University: Use The Following Information For The Next Two QuestionsDocument13 pagesCebu Institute of Technology - University: Use The Following Information For The Next Two QuestionsPrima Facie50% (2)

- Afar Construction Contracts PDFDocument10 pagesAfar Construction Contracts PDFArah Opalec0% (1)

- tUT3 MFRS15Document4 pagestUT3 MFRS15--bolabolaNo ratings yet

- LTCCDocument7 pagesLTCCgenevieve sicatNo ratings yet

- Construction ContractDocument17 pagesConstruction ContractYvonne Gam-oyNo ratings yet

- LTCCDocument16 pagesLTCCandzie09876No ratings yet

- Tutorial 3 MFRS111 Construction ContractDocument9 pagesTutorial 3 MFRS111 Construction Contractnatasha thaiNo ratings yet

- Tutorial Answer On Mfrs111 Construction ContractsDocument7 pagesTutorial Answer On Mfrs111 Construction ContractsJeyaletchumy Nava Ratinam67% (3)

- Contarct CostingDocument13 pagesContarct CostingBuddhadev NathNo ratings yet

- Construction FranchiseDocument7 pagesConstruction FranchisetheresaazuresNo ratings yet

- Accounting For EngineersDocument31 pagesAccounting For EngineerssuniljayaNo ratings yet

- Construction ContractttttDocument6 pagesConstruction ContractttttMARTINEZ, EmilynNo ratings yet

- ICDS - 3 Construction ContractsDocument13 pagesICDS - 3 Construction Contractskavita.m.yadavNo ratings yet

- Long-Term Construction Contracts & FranchiseDocument6 pagesLong-Term Construction Contracts & FranchiseBryan ReyesNo ratings yet

- 4 Material 4 LTCC For Students 2Document3 pages4 Material 4 LTCC For Students 2Joyce Anne GarduqueNo ratings yet

- Contract Costing 1 Day Revision NotesDocument12 pagesContract Costing 1 Day Revision NotesSanskar VarshneyNo ratings yet

- 06 Long Term Construction ContractsDocument4 pages06 Long Term Construction ContractsAllegria AlamoNo ratings yet

- Quiz ConstructionDocument1 pageQuiz ConstructionErjohn PapaNo ratings yet

- CHP 2. Contract Costing SumsDocument59 pagesCHP 2. Contract Costing SumsUchit MehtaNo ratings yet

- Long Term Construction ContractsDocument4 pagesLong Term Construction ContractsAnalynNo ratings yet

- MASB7 Construction Contract6Document2 pagesMASB7 Construction Contract6hyraldNo ratings yet

- LTCCDocument2 pagesLTCCAivan De LeonNo ratings yet

- Quiz On Construction Contracts 11.19.2022Document7 pagesQuiz On Construction Contracts 11.19.2022Julian CheezeNo ratings yet

- Afar 6Document5 pagesAfar 6Roxell CaibogNo ratings yet

- This Paper Is Not To Be Removed From The Examination HallsDocument56 pagesThis Paper Is Not To Be Removed From The Examination HallsDương DươngNo ratings yet

- LTCC Work BookDocument49 pagesLTCC Work BookHannah NolongNo ratings yet

- Identify The Choice That Best Completes The Statement or Answers The QuestionDocument10 pagesIdentify The Choice That Best Completes The Statement or Answers The QuestionErwin Labayog MedinaNo ratings yet

- CONTRACT COSTING - Chapter 6Document21 pagesCONTRACT COSTING - Chapter 6abhilekh91No ratings yet

- IFRS 15 Questions 02042024 122821pmDocument4 pagesIFRS 15 Questions 02042024 122821pmAbdullah ButtNo ratings yet

- Reviconstruct 012Document1 pageReviconstruct 012blink blinkNo ratings yet

- Special Revenue Recognition Special Revenue RecognitionDocument4 pagesSpecial Revenue Recognition Special Revenue RecognitionCee Gee BeeNo ratings yet

- Contract CostingDocument17 pagesContract CostingHarshit DaveNo ratings yet

- Long Term Construction Quiz PDF FreeDocument4 pagesLong Term Construction Quiz PDF FreeMichael Brian TorresNo ratings yet

- AS 7 - Construction ContractDocument13 pagesAS 7 - Construction Contractsourabhgoyal3075No ratings yet

- Const PDF FreeDocument15 pagesConst PDF FreeMichael Brian TorresNo ratings yet

- As GR 1 Ipcc Compiler 2015-18Document24 pagesAs GR 1 Ipcc Compiler 2015-18KRISHNA MANDLOINo ratings yet

- Construction ContractsDocument4 pagesConstruction ContractsAnjelica MarcoNo ratings yet

- Cma-I Semester-Ii Contract Costing (C.U Sums For Revision) : Compute The Amount Profit ThatDocument13 pagesCma-I Semester-Ii Contract Costing (C.U Sums For Revision) : Compute The Amount Profit Thatvivek kumarNo ratings yet

- Engineering Service Revenues World Summary: Market Values & Financials by CountryFrom EverandEngineering Service Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- Tutorial 2 Lululemon Case 1Document2 pagesTutorial 2 Lululemon Case 1--bolabolaNo ratings yet

- Topic 12 Strategic LeadershipDocument54 pagesTopic 12 Strategic Leadership--bolabolaNo ratings yet

- Topic 10 Corporate GovernanceDocument53 pagesTopic 10 Corporate Governance--bolabolaNo ratings yet

- Organizational Structure and ControlsDocument66 pagesOrganizational Structure and Controls--bolabolaNo ratings yet

- Topic 8 International StrategyDocument54 pagesTopic 8 International Strategy--bolabolaNo ratings yet

- Solutions To Questions - Chapter 6 Mortgages: Additional Concepts, Analysis, and Applications Question 6-1Document16 pagesSolutions To Questions - Chapter 6 Mortgages: Additional Concepts, Analysis, and Applications Question 6-1--bolabolaNo ratings yet

- Tutorial 1 Revision Q Jan2021-AnswersDocument8 pagesTutorial 1 Revision Q Jan2021-Answers--bolabolaNo ratings yet

- TUTORIAL 2 - Related Party (Questions) : UKAF4034 Advanced Corporate ReportingDocument6 pagesTUTORIAL 2 - Related Party (Questions) : UKAF4034 Advanced Corporate Reporting--bolabolaNo ratings yet

- Tutorial 3 Answer SegmentalDocument6 pagesTutorial 3 Answer Segmental--bolabolaNo ratings yet

- (Answer) : Tutorial 2 (MFRS 124 - Related Party Disclosures)Document11 pages(Answer) : Tutorial 2 (MFRS 124 - Related Party Disclosures)--bolabolaNo ratings yet

- Solutions To Questions - Chapter 20 The Secondary Mortgage Market: Cmos and Derivative Securities Question 20-1Document17 pagesSolutions To Questions - Chapter 20 The Secondary Mortgage Market: Cmos and Derivative Securities Question 20-1--bolabolaNo ratings yet

- Capital Statement: Tax InvestigationDocument23 pagesCapital Statement: Tax Investigation--bolabolaNo ratings yet

- P2mys 2008 Jun ADocument12 pagesP2mys 2008 Jun A--bolabolaNo ratings yet

- Real Property Gains Tax: Taxation of RPC SharesDocument30 pagesReal Property Gains Tax: Taxation of RPC Shares--bolabolaNo ratings yet

- Historical Development of Accounting PDF FreeDocument25 pagesHistorical Development of Accounting PDF Free--bolabolaNo ratings yet

- Tutorial 1 (Answer) - Tax Evasion and AvoidanceDocument5 pagesTutorial 1 (Answer) - Tax Evasion and Avoidance--bolabolaNo ratings yet

- Revision ExcerciseDocument2 pagesRevision Excercise--bolabolaNo ratings yet

- Real Property Gains Tax: (Cukai Keuntungan Harta Tanah)Document61 pagesReal Property Gains Tax: (Cukai Keuntungan Harta Tanah)--bolabolaNo ratings yet

- Chapter 7 - INTERNAL CONTROLSDocument74 pagesChapter 7 - INTERNAL CONTROLS--bolabola100% (1)

- L1 - Tax Evasion and AvoidanceDocument64 pagesL1 - Tax Evasion and Avoidance--bolabolaNo ratings yet

- Minutes 49 Agm Summary03Document7 pagesMinutes 49 Agm Summary03--bolabolaNo ratings yet

- Chapter 8 - INTERNAL AUDIT AND FRAUD RISK AutosavedDocument80 pagesChapter 8 - INTERNAL AUDIT AND FRAUD RISK Autosaved--bolabolaNo ratings yet

- Chapter 4 - Engagement Planning Considerations, Objectives, Scope, Risk-Based Internal Audit EngagementDocument45 pagesChapter 4 - Engagement Planning Considerations, Objectives, Scope, Risk-Based Internal Audit Engagement--bolabolaNo ratings yet

- Internal Audit Tools & TechniquesDocument62 pagesInternal Audit Tools & Techniques--bolabolaNo ratings yet

- Topic 1 SM CompetitivenessDocument46 pagesTopic 1 SM Competitiveness--bolabolaNo ratings yet

- t1q Rca2 Ya2020 Intro & RDocument2 pagest1q Rca2 Ya2020 Intro & RHaananth SubramaniamNo ratings yet

- 5 Days 4 Nights Bali Beautiful PackageDocument8 pages5 Days 4 Nights Bali Beautiful PackageMuhd Ghazali Mat RejabNo ratings yet

- Academic Session 2022 MAY 2022 Semester: AssignmentDocument6 pagesAcademic Session 2022 MAY 2022 Semester: AssignmentChristopher KipsangNo ratings yet

- Kedah Land (Amendment) Rules 1993Document10 pagesKedah Land (Amendment) Rules 1993Kelly LimNo ratings yet

- Application of ArithmeticsDocument9 pagesApplication of ArithmeticsRoszelan MajidNo ratings yet

- MF Tutorial - Q - June2020Document19 pagesMF Tutorial - Q - June2020Marcia PattersonNo ratings yet

- New Zealand CurrencyDocument5 pagesNew Zealand CurrencyAmy LauNo ratings yet

- Welcome To AFFINMAXDocument2 pagesWelcome To AFFINMAXcmbbcorporNo ratings yet

- DSK Mathematics Year 1 DLP PDFDocument38 pagesDSK Mathematics Year 1 DLP PDFZai Sulaiman80% (25)

- U9it8e PDFDocument20 pagesU9it8e PDFWongNo ratings yet

- Asset Draft Plan Form (Airflow Meter)Document2 pagesAsset Draft Plan Form (Airflow Meter)Osh 0717No ratings yet

- D24174R104750Document11 pagesD24174R104750Nurul 'AinNo ratings yet

- Case 5Document4 pagesCase 5ad1gamer100% (1)

- Energy Asia Prospectus 8thjune2023Document11 pagesEnergy Asia Prospectus 8thjune2023Inspirasi HakimieNo ratings yet

- Press Release 2013: Imagine Musa Tabling A RM40 Billion 2014 Sabah Budget 13 Nov 2013Document2 pagesPress Release 2013: Imagine Musa Tabling A RM40 Billion 2014 Sabah Budget 13 Nov 2013Daniel John JambunNo ratings yet

- PLB Webinar FAQ - 18 Jan 2023Document15 pagesPLB Webinar FAQ - 18 Jan 2023TomNo ratings yet

- TFFE Math 2Document9 pagesTFFE Math 2Shamima AkterNo ratings yet

- Final Report Ent 300Document107 pagesFinal Report Ent 300fakhrulNo ratings yet

- Bill Statement: Previous Charges Amount (RM) Current Charges Amount (RM)Document6 pagesBill Statement: Previous Charges Amount (RM) Current Charges Amount (RM)Akram YasinNo ratings yet

- Acc AssingmentDocument13 pagesAcc Assingmentummi nursyifaNo ratings yet

- Y5 WorksheetDocument23 pagesY5 WorksheetVivian GraceNo ratings yet

- MyHALAL BASKET PITCH DECK PRESENTATIONDocument35 pagesMyHALAL BASKET PITCH DECK PRESENTATIONPrince Babansala RamzyNo ratings yet

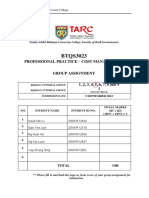

- BTQS3023 Neoh Wei Li RQS4G5 AssignmentDocument32 pagesBTQS3023 Neoh Wei Li RQS4G5 AssignmentWei Li NeohNo ratings yet

- Financing Details: Cik Syazwani Binti Aziz Financing Account 06028080069448 MYR MYR 85,000.00Document1 pageFinancing Details: Cik Syazwani Binti Aziz Financing Account 06028080069448 MYR MYR 85,000.00GINTAMAGINTOKINo ratings yet

- Mohd Azzarain Bin Abdul Aziz: Injection WithdrawalDocument2 pagesMohd Azzarain Bin Abdul Aziz: Injection WithdrawalAffeif AzzarainNo ratings yet