You might also like

- Assessment Task 1Document7 pagesAssessment Task 1purva02No ratings yet

- BSBPEF502 Project Portfolio - RevisedDocument17 pagesBSBPEF502 Project Portfolio - RevisedQasim YousafNo ratings yet

- Bounce FitnessDocument4 pagesBounce FitnessCarolina DuqueNo ratings yet

- Financial Management Planning and Budgeting ReportDocument12 pagesFinancial Management Planning and Budgeting Reportarshia_fareedNo ratings yet

- BSBMKG606 Assessment Task 1Document7 pagesBSBMKG606 Assessment Task 1sammyNo ratings yet

- Academia BSBINN601 - Lead - and - Manage - Organisational Fast Track PDFDocument6 pagesAcademia BSBINN601 - Lead - and - Manage - Organisational Fast Track PDFMaria TahreemNo ratings yet

- BSBCMM401Document17 pagesBSBCMM401Jaskarn Singh Dhonkal100% (2)

- BSBCMM401 Assessment 1 Template PowerPointDocument7 pagesBSBCMM401 Assessment 1 Template PowerPointQN.FlamingNo ratings yet

- BSBMGT617 Develop Strategic HR PlanDocument10 pagesBSBMGT617 Develop Strategic HR PlanDaphne MahinayNo ratings yet

- BSBCUS403 Task 2Document5 pagesBSBCUS403 Task 2Suu PromchantuekNo ratings yet

- Part 3 - Written Questionnaire: 494460245.docxversion 2.0 Nov 2019 1 of 2Document2 pagesPart 3 - Written Questionnaire: 494460245.docxversion 2.0 Nov 2019 1 of 2Stacy ParkerNo ratings yet

- BSBLDR511 Task 2Document4 pagesBSBLDR511 Task 2fernan fernandezNo ratings yet

- Draft Marketing BudgetDocument2 pagesDraft Marketing Budgetanisha neupaneNo ratings yet

- Identifying change needs at Fast Track CouriersDocument7 pagesIdentifying change needs at Fast Track CouriersNidhi GuptaNo ratings yet

- BSBMKG624 Simulation PackDocument7 pagesBSBMKG624 Simulation PackJing Yao ONo ratings yet

- Mayur (Stubborn) - BSBHRM513 - Assessment 3 (7!08!2020)Document7 pagesMayur (Stubborn) - BSBHRM513 - Assessment 3 (7!08!2020)chakshu jainNo ratings yet

- Assesment 2Document8 pagesAssesment 2star trendz0% (1)

- Indirect CostsDocument2 pagesIndirect CostsAngie Fer.No ratings yet

- Plan a presentationDocument9 pagesPlan a presentationalexNo ratings yet

- Task 1 Finance ManagementDocument17 pagesTask 1 Finance Managementraj ramukNo ratings yet

- BSBFIM601 Manage Finances Task 1Document16 pagesBSBFIM601 Manage Finances Task 1Kathleen RamientoNo ratings yet

- Describe One Thing You Could Do To Maximise Participation in and Support For Organisational Development in Each of The Following AreasDocument3 pagesDescribe One Thing You Could Do To Maximise Participation in and Support For Organisational Development in Each of The Following AreasSushan PradhanNo ratings yet

- Assessment 2 Vandana DeviDocument15 pagesAssessment 2 Vandana DeviHaseeb AshrafNo ratings yet

- BSBINN801 Assessment Instruction v1.0 Mar 2020Document29 pagesBSBINN801 Assessment Instruction v1.0 Mar 2020Asad Mumtaz GhalluNo ratings yet

- Task 10326Document3 pagesTask 10326EricKang0% (4)

- BSBMGT605 Assessment 3Document6 pagesBSBMGT605 Assessment 3KOKOWARA VIANo ratings yet

- Assessment Task 3 InstructionsDocument2 pagesAssessment Task 3 InstructionsVanessa May Sandoval0% (2)

- Develop Customer Service PlanDocument7 pagesDevelop Customer Service PlanPhung KimNo ratings yet

- 2 - Bsbadm506 - SlidesDocument79 pages2 - Bsbadm506 - SlidesVatsal PatelNo ratings yet

- BSBINN801 Student Assessment Tasks 21-05-19Document31 pagesBSBINN801 Student Assessment Tasks 21-05-19harryNo ratings yet

- Sha Yee YongDocument17 pagesSha Yee YongJenny YipNo ratings yet

- BSBOPS503 Student GuideDocument30 pagesBSBOPS503 Student GuideBui AnNo ratings yet

- BSBFIM601 - Part B - Budget - NovoDocument18 pagesBSBFIM601 - Part B - Budget - NovoGabi Assis0% (2)

- BSBHRM405 AssessmentDocument52 pagesBSBHRM405 AssessmentAli Raza Mashhadi100% (1)

- Lmad 3.2 Bsbdiv601Document26 pagesLmad 3.2 Bsbdiv601Kuya Rimson VlogsNo ratings yet

- Before You Begin VII Topic 1: Review Programs, Systems and Processes 1Document20 pagesBefore You Begin VII Topic 1: Review Programs, Systems and Processes 1Vaishali AroraNo ratings yet

- Student Assessment Information GuideDocument8 pagesStudent Assessment Information GuideManpreetNo ratings yet

- Bsbmkg502 BBQ Fun Task 1&2Document13 pagesBsbmkg502 BBQ Fun Task 1&2prasannareddy9989No ratings yet

- Task 3: Boutique Build Australia Part A 1. Write A Short (One-Page) Report On Potential Work-Life Balance StrategiesDocument10 pagesTask 3: Boutique Build Australia Part A 1. Write A Short (One-Page) Report On Potential Work-Life Balance StrategiesKelvin AnthonyNo ratings yet

- BSB502 EffectDocument14 pagesBSB502 EffectNan Wonghan50% (8)

- BSBINM601 - Assessment Workbook-Task-2Document23 pagesBSBINM601 - Assessment Workbook-Task-2Nazakat AliNo ratings yet

- Mayur (Stubborn) - BSBHRM513 - Assessment 5 (7!08!2020)Document8 pagesMayur (Stubborn) - BSBHRM513 - Assessment 5 (7!08!2020)chakshu jainNo ratings yet

- DIPLMBPB15 Assessment 2 Brief 20171101Document6 pagesDIPLMBPB15 Assessment 2 Brief 20171101Denmark WilsonNo ratings yet

- BSBMGT517 Bbqfun NewDocument24 pagesBSBMGT517 Bbqfun NewSukhdeep ChohanNo ratings yet

- BSBPMG624 - T1 - Michael Johan Cruz VerdugoDocument12 pagesBSBPMG624 - T1 - Michael Johan Cruz VerdugoLaura VargasNo ratings yet

- BSBCMM401 - Make A Presentation Written QuestionsDocument1 pageBSBCMM401 - Make A Presentation Written QuestionsJenny ParashakisNo ratings yet

- Thanyaporn Lohitya BSBINN601 Task 1Document2 pagesThanyaporn Lohitya BSBINN601 Task 1Tang LohityaNo ratings yet

- 18.11.26 Diploma BSBCRT401 Articulate Present and Debate Ideas Assessments LEGENDSDocument34 pages18.11.26 Diploma BSBCRT401 Articulate Present and Debate Ideas Assessments LEGENDSMichelle SukamtoNo ratings yet

- BSBADM502 Student Assessment Tasks V1.0 09-20Document31 pagesBSBADM502 Student Assessment Tasks V1.0 09-20tanvir019No ratings yet

- BSBMKG603 Marketing Mix and Product OpportunitiesDocument1 pageBSBMKG603 Marketing Mix and Product OpportunitiesnattyNo ratings yet

- Lead personal transformation and strategic skillsDocument5 pagesLead personal transformation and strategic skillsJoanne Navarro AlmeriaNo ratings yet

- Task 2 - Bsbcus501Document10 pagesTask 2 - Bsbcus501Phung KimNo ratings yet

- Bsbinn601 Ppslides v1.3Document86 pagesBsbinn601 Ppslides v1.3hossain alviNo ratings yet

- Student Assessment Tasks: BSBCRT401 Articulate, Present and Debate IdeasDocument9 pagesStudent Assessment Tasks: BSBCRT401 Articulate, Present and Debate IdeasSuhaib AhmedNo ratings yet

- Task 1 Develop An Operational PlanDocument16 pagesTask 1 Develop An Operational PlanPanduka Bandara50% (2)

- BSBFIA401 1 BSBFIA401 Prepare Financial Reports Practice Task Answer BookletDocument3 pagesBSBFIA401 1 BSBFIA401 Prepare Financial Reports Practice Task Answer Bookletnatty100% (1)

- BSBMGT608 Manage Innovation and Continuous Improvement: Assessment Task 2 Team Project: Product InnovationDocument19 pagesBSBMGT608 Manage Innovation and Continuous Improvement: Assessment Task 2 Team Project: Product InnovationKOKOWARA VIANo ratings yet

- Lecture Assessment 1 Case Study and Projects-Group ActivitiesDocument25 pagesLecture Assessment 1 Case Study and Projects-Group ActivitiesHimanshuNo ratings yet

- Master Budget Components and UsesDocument10 pagesMaster Budget Components and UsesNur Athirah Binti MahdirNo ratings yet

- Fiscal Management WF Dr. Emerita R. Alias Edgar Roy M. Curammeng Financial Forecasting, Corporate Planning and BudgetingDocument10 pagesFiscal Management WF Dr. Emerita R. Alias Edgar Roy M. Curammeng Financial Forecasting, Corporate Planning and BudgetingJeannelyn CondeNo ratings yet

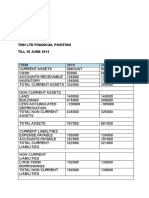

- Manage Finances: TMH LTD Financial Position TILL 30 JUNE 2015Document4 pagesManage Finances: TMH LTD Financial Position TILL 30 JUNE 2015raj ramukNo ratings yet

- Develop and Implement Marketing Strategies2Document10 pagesDevelop and Implement Marketing Strategies2raj ramukNo ratings yet

- Develop and Implement Marketing StrategiesDocument8 pagesDevelop and Implement Marketing Strategiesraj ramukNo ratings yet

- Establish and Maintain Whs Safety System1Document46 pagesEstablish and Maintain Whs Safety System1raj ramukNo ratings yet

- Revenue, Expenditure and Capital Investment Proposal/Plan: Manage FinancesDocument25 pagesRevenue, Expenditure and Capital Investment Proposal/Plan: Manage Financesraj ramukNo ratings yet

- Develop and Implement Marketing Strategies2Document10 pagesDevelop and Implement Marketing Strategies2raj ramukNo ratings yet

- Develop and Implement A Business Plan1Document2 pagesDevelop and Implement A Business Plan1raj ramukNo ratings yet

- Recruit Induct and Select Staff1Document8 pagesRecruit Induct and Select Staff1raj ramukNo ratings yet

- Develop and Implement Marketing StrategiesDocument8 pagesDevelop and Implement Marketing Strategiesraj ramukNo ratings yet

- Develop and Implement Marketing StrategiesDocument8 pagesDevelop and Implement Marketing Strategiesraj ramukNo ratings yet

- Revenue, Expenditure and Capital Investment Proposal/Plan: Manage FinancesDocument25 pagesRevenue, Expenditure and Capital Investment Proposal/Plan: Manage Financesraj ramukNo ratings yet

- Develop and Implement Marketing Strategies2Document10 pagesDevelop and Implement Marketing Strategies2raj ramukNo ratings yet

- Develop and Implement Marketing Strategies2Document10 pagesDevelop and Implement Marketing Strategies2raj ramukNo ratings yet

- Recruit Select Induct Staff 2Document3 pagesRecruit Select Induct Staff 2raj ramukNo ratings yet

- Manage Finances: TMH LTD Financial Position TILL 30 JUNE 2015Document4 pagesManage Finances: TMH LTD Financial Position TILL 30 JUNE 2015raj ramukNo ratings yet

- Develop and Implement A Business Plan2Document14 pagesDevelop and Implement A Business Plan2raj ramukNo ratings yet

- Develop and Implement Marketing Strategies2Document10 pagesDevelop and Implement Marketing Strategies2raj ramukNo ratings yet

- Develop and Implement A Business Plan1Document2 pagesDevelop and Implement A Business Plan1raj ramukNo ratings yet

- Produce and Serve Food For BuffetsDocument14 pagesProduce and Serve Food For Buffetsraj ramukNo ratings yet

- Develop and Implement A Business Plan2Document14 pagesDevelop and Implement A Business Plan2raj ramukNo ratings yet

- Revenue, Expenditure and Capital Investment Proposal/Plan: Manage FinancesDocument25 pagesRevenue, Expenditure and Capital Investment Proposal/Plan: Manage Financesraj ramukNo ratings yet

- Prepare Seafood DishesDocument21 pagesPrepare Seafood Dishesraj ramuk100% (1)

- Prepare Poultry DishesDocument17 pagesPrepare Poultry Dishesraj ramukNo ratings yet

- PREPARE SANDWICHESDocument19 pagesPREPARE SANDWICHESraj ramukNo ratings yet

- c3 Assignment UnknownDocument5 pagesc3 Assignment Unknownraj ramukNo ratings yet

- Prepare Meat DishesDocument20 pagesPrepare Meat Dishesraj ramukNo ratings yet

- Prepare Vegetables, Fruit, Eggs and Farinaceous DishesDocument30 pagesPrepare Vegetables, Fruit, Eggs and Farinaceous Dishesraj ramuk75% (4)

- Asisgnment No 2 PREPARE MEAT DISHESDocument6 pagesAsisgnment No 2 PREPARE MEAT DISHESraj ramuk100% (1)

- 20 April Final PREPARE MEAT DISHESDocument17 pages20 April Final PREPARE MEAT DISHESraj ramukNo ratings yet

- 20 April Produce Cakes and Pasteries and BreadsDocument16 pages20 April Produce Cakes and Pasteries and Breadsraj ramuk50% (2)

- Geography Grade 11 ANotes and Worksheet On Topography Associated With Horozontally Layered RocksDocument13 pagesGeography Grade 11 ANotes and Worksheet On Topography Associated With Horozontally Layered RocksTheo MolotoNo ratings yet

- Stigmatization of Feminism: Gender Studies As "Gender Ideology" in Right-Wing Populist Political Discourse in HungaryDocument55 pagesStigmatization of Feminism: Gender Studies As "Gender Ideology" in Right-Wing Populist Political Discourse in HungaryAnubhav SinghNo ratings yet

- MMA2019 SDocument2 pagesMMA2019 SToni IbrahimNo ratings yet

- Kyle Capodice Ecet Candidate ResumeDocument1 pageKyle Capodice Ecet Candidate Resumeapi-394690479No ratings yet

- Birla Institute of Technology and Science, Pilani: Pilani Campus AUGS/ AGSR DivisionDocument5 pagesBirla Institute of Technology and Science, Pilani: Pilani Campus AUGS/ AGSR DivisionDeep PandyaNo ratings yet

- THE HOUSE ON ZAPOTE STREET - Lyka PalerDocument11 pagesTHE HOUSE ON ZAPOTE STREET - Lyka PalerDivine Lyka Ordiz PalerNo ratings yet

- UntitledDocument421 pagesUntitledtunggal KecerNo ratings yet

- Railways MedicalDocument73 pagesRailways MedicalGaurav KapoorNo ratings yet

- 2022-02-03 Adidas Global Supplier ListDocument179 pages2022-02-03 Adidas Global Supplier ListTrần Đức Dũng100% (1)

- WWII 2nd Army HistoryDocument192 pagesWWII 2nd Army HistoryCAP History Library100% (1)

- Mathematics Engagement in An Australian Lower Secondary SchoolDocument23 pagesMathematics Engagement in An Australian Lower Secondary SchoolDane SinclairNo ratings yet

- Corporate Level Strategies ExplainedDocument30 pagesCorporate Level Strategies ExplainedNazir AnsariNo ratings yet

- Digital Mining Technology CAS-GPS Light Vehicle System Technical SpecificationDocument5 pagesDigital Mining Technology CAS-GPS Light Vehicle System Technical SpecificationAbhinandan PadhaNo ratings yet

- Change Management HRDocument2 pagesChange Management HRahmedaliNo ratings yet

- Bitonio V CoaDocument24 pagesBitonio V Coamarjorie requirmeNo ratings yet

- Popular Telugu Novel "Prema DeepikaDocument2 pagesPopular Telugu Novel "Prema Deepikasindhu60% (5)

- MSDS TriacetinDocument4 pagesMSDS TriacetinshishirchemNo ratings yet

- Nilai Murni PKN XII Mipa 3Document8 pagesNilai Murni PKN XII Mipa 3ilmi hamdinNo ratings yet

- Step 5 - PragmaticsDocument7 pagesStep 5 - PragmaticsRomario García UrbinaNo ratings yet

- Pricelist PT SCB Maret 2023Document11 pagesPricelist PT SCB Maret 2023PT RUKUN CAHAYA ABADINo ratings yet

- Forming Plurals of NounsDocument5 pagesForming Plurals of NounsCathy GalNo ratings yet

- (1902) The Centennial of The United States Military Academy at West Point New YorkDocument454 pages(1902) The Centennial of The United States Military Academy at West Point New YorkHerbert Hillary Booker 2nd100% (1)

- Group No 5 - Ultratech - Jaypee 20th Sep-1Document23 pagesGroup No 5 - Ultratech - Jaypee 20th Sep-1Snehal100% (1)

- Tower Scientific CompanyDocument3 pagesTower Scientific Companymaloy0% (1)

- Sri Sathya Sai Bhagavatam Part IDocument300 pagesSri Sathya Sai Bhagavatam Part ITumuluru Krishna Murty67% (6)

- Heliopolis Language Modern School Academic Year (2015-2016) Model Exam (9) 1st Prep (Unit 3) Aim High (A-Level)Document2 pagesHeliopolis Language Modern School Academic Year (2015-2016) Model Exam (9) 1st Prep (Unit 3) Aim High (A-Level)Yasser MohamedNo ratings yet

- Analyzing Potential Audit Client LakesideDocument22 pagesAnalyzing Potential Audit Client LakesideLet it be100% (1)

- Kisan Seva Android Application: ISSN 2395-1621Document4 pagesKisan Seva Android Application: ISSN 2395-1621Survive YouNo ratings yet

- EN Sample Paper 19 UnsolvedDocument12 pagesEN Sample Paper 19 UnsolvedRashvandhNo ratings yet

- Stone Fox BookletDocument19 pagesStone Fox Bookletapi-220567377100% (3)