You might also like

- Billionaires Black Book by Robert BaileyDocument256 pagesBillionaires Black Book by Robert Baileyrbailey922695% (19)

- Founding Stage Capitalization Table SummaryDocument6 pagesFounding Stage Capitalization Table SummarysonkarmanishNo ratings yet

- Basics of Share Market OperationsDocument8 pagesBasics of Share Market Operationslelesachin100% (2)

- Vault-Finance Interview QuestionsDocument22 pagesVault-Finance Interview QuestionsSandeep Chowdhury100% (1)

- Best fund managers 2019Document26 pagesBest fund managers 2019Manohar BNo ratings yet

- Using Behavioral Investor TypesDocument8 pagesUsing Behavioral Investor TypesVidushi Bonomaully100% (1)

- Care Rating Sterling - Addlife - India - Private - LimitedDocument6 pagesCare Rating Sterling - Addlife - India - Private - Limitedrahul.tibrewalNo ratings yet

- Piramal Pharma Credit Rating - 13 March 2023Document8 pagesPiramal Pharma Credit Rating - 13 March 2023Ikp IkpNo ratings yet

- T V Sundram Iyengar - R-25022019 PDFDocument7 pagesT V Sundram Iyengar - R-25022019 PDFSankar KumarNo ratings yet

- Sandfits Foundries Private LimitedDocument7 pagesSandfits Foundries Private Limitedvignesh seenirajNo ratings yet

- Press Release RACL Geartech LTDDocument4 pagesPress Release RACL Geartech LTDSourav DuttaNo ratings yet

- Press Release Om Logistics Limited: Details of Instruments/facilities in Annexure-1Document6 pagesPress Release Om Logistics Limited: Details of Instruments/facilities in Annexure-1Sinius InfracomNo ratings yet

- Incred Financial Services Limited Press+ReleaseDocument7 pagesIncred Financial Services Limited Press+ReleaseGautam MehtaNo ratings yet

- Maithan Alloys LimitedDocument6 pagesMaithan Alloys Limiteddrkashish1989No ratings yet

- Press Release Adani Agri Logistics (Harda) Limited: Details of Facilities in Annexure-1Document3 pagesPress Release Adani Agri Logistics (Harda) Limited: Details of Facilities in Annexure-1surprise MFNo ratings yet

- Subros LimitedDocument8 pagesSubros LimitedrajpersonalNo ratings yet

- Rating Definitions - 19 July 2018Document4 pagesRating Definitions - 19 July 2018SushantNo ratings yet

- Filatex India Limited press release ratings reaffirmedDocument6 pagesFilatex India Limited press release ratings reaffirmedfatNo ratings yet

- CARE_Sunflag_4.01.2024Document9 pagesCARE_Sunflag_4.01.2024Swapnil SomkuwarNo ratings yet

- Ajanta Soya 13may2021Document7 pagesAjanta Soya 13may2021praveen kumarNo ratings yet

- R. K. Marble Private Limited-12!30!2020Document6 pagesR. K. Marble Private Limited-12!30!2020Brajpal JhalaNo ratings yet

- Press Release Adani Agri Logistics (Harda) Limited: Rating Sensitivities: Positive Factors: Negative FactorsDocument4 pagesPress Release Adani Agri Logistics (Harda) Limited: Rating Sensitivities: Positive Factors: Negative Factorssurprise MFNo ratings yet

- Vijay Sales (India) Private LimitedDocument5 pagesVijay Sales (India) Private LimitedAakanksha RaiNo ratings yet

- 13186Document3 pages13186amitagar42No ratings yet

- 10102022062806_Myra_Hygiene_Products_Private_LimitedDocument7 pages10102022062806_Myra_Hygiene_Products_Private_Limitedanuj7729No ratings yet

- T V Sundram Iyengar-R-16022018Document7 pagesT V Sundram Iyengar-R-16022018AGN YaNo ratings yet

- Fund-Based Working Capital Facility of The Company.: Press ReleaseDocument2 pagesFund-Based Working Capital Facility of The Company.: Press ReleaseVikrant MishraNo ratings yet

- Mahindra & Mahindra LimitedDocument6 pagesMahindra & Mahindra Limitedjerin jNo ratings yet

- SMFG India Credit Company LimitedDocument9 pagesSMFG India Credit Company Limitedvatsal sinhaNo ratings yet

- Credit Rating LetterDocument10 pagesCredit Rating LetterMAHI LADNo ratings yet

- Nelcast Limited: Long-Term Rating Re-Affirmed and Outlook Revised To Negative Short-Term Rating Downgraded To (ICRA) A1 Summary of Rating ActionDocument7 pagesNelcast Limited: Long-Term Rating Re-Affirmed and Outlook Revised To Negative Short-Term Rating Downgraded To (ICRA) A1 Summary of Rating ActionPuneet367No ratings yet

- La Opala RG LimitedDocument5 pagesLa Opala RG LimitedAshwani KesharwaniNo ratings yet

- Udaipur Cement Works receives rating reaffirmationDocument6 pagesUdaipur Cement Works receives rating reaffirmationflying400No ratings yet

- Agrocel Industries Private LimitedDocument7 pagesAgrocel Industries Private LimitedNitin KumarNo ratings yet

- VRL Logistics LimitedDocument8 pagesVRL Logistics LimitedChatgptguyNo ratings yet

- Credit Rating Post March 2023Document26 pagesCredit Rating Post March 2023Sumiran BansalNo ratings yet

- AVT Natural Products LimitedDocument7 pagesAVT Natural Products LimitedHarpreet SinghNo ratings yet

- RACL Geartech ratings reaffirmedDocument4 pagesRACL Geartech ratings reaffirmedSourav DuttaNo ratings yet

- V-Mart Retail R 02032020Document8 pagesV-Mart Retail R 02032020Yusuf MalikNo ratings yet

- Haldiram Products Private LimitedDocument7 pagesHaldiram Products Private LimitedAman GuptaNo ratings yet

- SGS Tekniks Manufacturing Pvt LtdDocument7 pagesSGS Tekniks Manufacturing Pvt Ltdgcgary87No ratings yet

- Press Release Deccan Industries: Positive FactorsDocument4 pagesPress Release Deccan Industries: Positive FactorsHARI HARANNo ratings yet

- 04102022073602_Divis_Laboratories_LimitedDocument7 pages04102022073602_Divis_Laboratories_Limiteddivygupta198No ratings yet

- AA- Rating Reflects ACME Laboratories' Strengths but Concerns RemainDocument13 pagesAA- Rating Reflects ACME Laboratories' Strengths but Concerns RemainnasirNo ratings yet

- Press Release Adani Agri Logistics (Harda) LimitedDocument5 pagesPress Release Adani Agri Logistics (Harda) Limitedsurprise MFNo ratings yet

- Mamta Transformers-R-19102020Document7 pagesMamta Transformers-R-19102020DarshanNo ratings yet

- Fine Organic Industries - R - 17012020Document8 pagesFine Organic Industries - R - 17012020Sameer NaikNo ratings yet

- Shilchar_Technologies_LimitedDocument5 pagesShilchar_Technologies_Limitedjaikumar608jainNo ratings yet

- AVT McCormick-R-26032018Document7 pagesAVT McCormick-R-26032018Siddharth DamaniNo ratings yet

- Reliance Industries LimitedDocument13 pagesReliance Industries Limitedsattyak.sharma.2022No ratings yet

- Saraf Chemicals Private LimitedDocument6 pagesSaraf Chemicals Private LimitedCedric KerkettaNo ratings yet

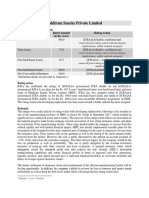

- Haldiram Snacks Private Limited: Summary of Rated Instruments Instrument Rated Amount (In Rs. Crore) Rating ActionDocument7 pagesHaldiram Snacks Private Limited: Summary of Rated Instruments Instrument Rated Amount (In Rs. Crore) Rating ActionJaleel ChennaiNo ratings yet

- Vardhman Pharma Distributors Private Limited-10-01-2020Document6 pagesVardhman Pharma Distributors Private Limited-10-01-2020Saifuddin LalaNo ratings yet

- Press Release Irb Invit Fund: Complete Definition of The Ratings Assigned Are Available at and Other Care PublicationsDocument5 pagesPress Release Irb Invit Fund: Complete Definition of The Ratings Assigned Are Available at and Other Care PublicationsANUBHAVCFANo ratings yet

- Adani Power Limited: Project FinanceDocument11 pagesAdani Power Limited: Project FinanceRajarshiRoyChoudhuryNo ratings yet

- CP Bangladesh Company Limited Rating Report 2012 CheckedDocument3 pagesCP Bangladesh Company Limited Rating Report 2012 CheckedMuannis MahmoodNo ratings yet

- Ocean Pearl Hotels Private LimitedDocument7 pagesOcean Pearl Hotels Private LimitedAaaaNo ratings yet

- AcmeDocument2 pagesAcmePavel ZephyrusNo ratings yet

- Epyllion LTD Rating Report 2011Document4 pagesEpyllion LTD Rating Report 2011Boni AminNo ratings yet

- Rockman Industries Limited: Summary of Rated Instruments Instrument Rated Amount (Rs. Crore) Rating ActionDocument7 pagesRockman Industries Limited: Summary of Rated Instruments Instrument Rated Amount (Rs. Crore) Rating ActionVirender RawatNo ratings yet

- Khadim India Limited - ICRA Feb 2020 PDFDocument7 pagesKhadim India Limited - ICRA Feb 2020 PDFPuneet367No ratings yet

- Care RatingDocument4 pagesCare RatingChandrasekar KrishnamurthyNo ratings yet

- Sakthi Finance Limited R 20022020Document9 pagesSakthi Finance Limited R 20022020Elan ChelianNo ratings yet

- Rating Rationale - Hero Steel Oct 2019Document4 pagesRating Rationale - Hero Steel Oct 2019Puneet367No ratings yet

- Padget Electronics Pvt. LTDDocument9 pagesPadget Electronics Pvt. LTDvenkyniyerNo ratings yet

- ASEAN Corporate Governance Scorecard Country Reports and Assessments 2015: Joint Initiative of the ASEAN Capital Markets Forum and the Asian Development BankFrom EverandASEAN Corporate Governance Scorecard Country Reports and Assessments 2015: Joint Initiative of the ASEAN Capital Markets Forum and the Asian Development BankNo ratings yet

- Shahid Umar Khan (19MBAR0266)Document17 pagesShahid Umar Khan (19MBAR0266)Anjum SamiraNo ratings yet

- Scanned With CamscannerDocument17 pagesScanned With CamscannerAnjum SamiraNo ratings yet

- CSR 2nd Assignment (ANJUM SAMIRA)Document18 pagesCSR 2nd Assignment (ANJUM SAMIRA)Anjum SamiraNo ratings yet

- Empire Restaurant Operations Management FunctionsDocument19 pagesEmpire Restaurant Operations Management FunctionsAnjum SamiraNo ratings yet

- Managerial Economics Mini ProjectDocument17 pagesManagerial Economics Mini ProjectAnjum SamiraNo ratings yet

- Banking - Module-Revison Class SentDocument163 pagesBanking - Module-Revison Class SentAnjum SamiraNo ratings yet

- CF 3rd AssignmentDocument6 pagesCF 3rd AssignmentAnjum SamiraNo ratings yet

- Dolphin Offshore's History as India's First Underwater Engineering CompanyDocument12 pagesDolphin Offshore's History as India's First Underwater Engineering CompanyAnjum SamiraNo ratings yet

- Impact of public company acquisition on private limited companyDocument2 pagesImpact of public company acquisition on private limited companyAnjum SamiraNo ratings yet

- Excel FunctionsDocument7 pagesExcel FunctionsAnjum SamiraNo ratings yet

- A Discussion of Rational and Psychological Decision-Making Theories and Models - The Search For A Cultural-Ethical Decision-Making ModelDocument6 pagesA Discussion of Rational and Psychological Decision-Making Theories and Models - The Search For A Cultural-Ethical Decision-Making ModelAnjum SamiraNo ratings yet

- IAPMDocument16 pagesIAPMAnjum SamiraNo ratings yet

- CFA Project CGDocument66 pagesCFA Project CGAnjum SamiraNo ratings yet

- CFA Project CG PDFDocument66 pagesCFA Project CG PDFAnjum SamiraNo ratings yet

- Excel FunctionsDocument7 pagesExcel FunctionsAnjum SamiraNo ratings yet

- Hedgebay Index - July 2010Document2 pagesHedgebay Index - July 2010economicburnNo ratings yet

- Quiz Results Learning FPDocument45 pagesQuiz Results Learning FPthebhas1954No ratings yet

- Pepsico Final Communication Plan Presentation 1Document21 pagesPepsico Final Communication Plan Presentation 1api-545909907No ratings yet

- IFRS 13-Eng PDFDocument71 pagesIFRS 13-Eng PDFNhhư QuỳnhhNo ratings yet

- What Is A Bear Trap?: Key TakeawaysDocument1 pageWhat Is A Bear Trap?: Key TakeawaysAli Abdelfatah MahmoudNo ratings yet

- Governance Risk Ethics Notes ExplainedDocument17 pagesGovernance Risk Ethics Notes ExplainedhoyokeweiNo ratings yet

- A S I P O T N S E O I: Tudy of Nitial Ublic Fferings On HE Ational Tock Xchange F NdiaDocument33 pagesA S I P O T N S E O I: Tudy of Nitial Ublic Fferings On HE Ational Tock Xchange F NdiarhtmhrNo ratings yet

- SLF: Sun Life Financial To Acquire U.S. Employee Benefits Business of AssurantDocument5 pagesSLF: Sun Life Financial To Acquire U.S. Employee Benefits Business of AssurantBusinessWorldNo ratings yet

- The Problematic of Financing Small and Medium Sized Enterprise in MoroccoDocument13 pagesThe Problematic of Financing Small and Medium Sized Enterprise in MoroccoHAMED JamalNo ratings yet

- Chapter AnswersDocument6 pagesChapter AnswersMiguelito AlcazarNo ratings yet

- Understanding The Right Ecosystem For StartupsDocument5 pagesUnderstanding The Right Ecosystem For StartupsRaza AliNo ratings yet

- Study on Client Acquisition and Retention Process in Event Ticketing IndustryDocument60 pagesStudy on Client Acquisition and Retention Process in Event Ticketing IndustryBhavesh GuptaNo ratings yet

- CH 2Document10 pagesCH 2Miftahudin Miftahudin100% (1)

- Dubai Realty Transactions To Touch Dh700b - TBW August 3 - UAE SpotlightDocument1 pageDubai Realty Transactions To Touch Dh700b - TBW August 3 - UAE Spotlightjiminabottle100% (5)

- A Study On Awareness About Investment in Derivatives Among Government Employees in Calicut District of KeralaDocument8 pagesA Study On Awareness About Investment in Derivatives Among Government Employees in Calicut District of KeralaHarish.PNo ratings yet

- Best Practices For Effectively Managing Non-Performing LoansDocument12 pagesBest Practices For Effectively Managing Non-Performing LoansSyed FoadNo ratings yet

- CUFF Should RecDocument5 pagesCUFF Should RecLlerry Darlene Abaco RacuyaNo ratings yet

- Chapter-7 Investment ManagementDocument7 pagesChapter-7 Investment Managementhasan alNo ratings yet

- FM II Chapter 1Document23 pagesFM II Chapter 1Amanuel AbebawNo ratings yet

- Sebi GuidelinesDocument44 pagesSebi Guidelinesdivya57trueNo ratings yet

- Holotrck Vs PLFXDocument76 pagesHolotrck Vs PLFXtriguy_2010No ratings yet

- 2MBA Biz PlanDocument22 pages2MBA Biz PlanCarinna Saldaña - PierardNo ratings yet

- Wealth Management: Faculty: Mr. Aneesh DayDocument29 pagesWealth Management: Faculty: Mr. Aneesh DayHIMANSHU DUTTANo ratings yet

- Dossier December en CompressedDocument53 pagesDossier December en CompressedJuan David PalacinoNo ratings yet