You might also like

- USDA Forecasts Record World Coffee Production in 2020/21Document1 pageUSDA Forecasts Record World Coffee Production in 2020/21Red DensonerNo ratings yet

- Coffee PDFDocument9 pagesCoffee PDFesulawyer2001No ratings yet

- Coffee: World Markets and Trade: Ethiopia: World's Third Largest Arabica Coffee ProducerDocument10 pagesCoffee: World Markets and Trade: Ethiopia: World's Third Largest Arabica Coffee ProducermulerstarNo ratings yet

- Coffee: World Markets and Trade: 2018/19 Forecast OverviewDocument8 pagesCoffee: World Markets and Trade: 2018/19 Forecast OverviewzmahfudzNo ratings yet

- 2022 - USDA - Coffee World Markets and TradeDocument9 pages2022 - USDA - Coffee World Markets and TradeJUAN EDUARDO SOTO MORANo ratings yet

- CoffeeDocument9 pagesCoffeemt7908609No ratings yet

- Sugar Quarterly Q1 2020Document18 pagesSugar Quarterly Q1 2020Ahmed OuhniniNo ratings yet

- Chile: The Macroeconomic Scenario: Rodrigo VergaraDocument30 pagesChile: The Macroeconomic Scenario: Rodrigo Vergaraharshnvicky123No ratings yet

- Cotton Outlook: United States Department of AgricultureDocument18 pagesCotton Outlook: United States Department of AgricultureNitin GuptaNo ratings yet

- India's rice production, exports and global market outlookDocument10 pagesIndia's rice production, exports and global market outlooksatyanarayana markandeyaNo ratings yet

- Balrampur Chini: Moving To Next OrbitDocument9 pagesBalrampur Chini: Moving To Next OrbitDebjit AdakNo ratings yet

- Coffee: World Markets and Trade: 2020/21 Forecast OverviewDocument9 pagesCoffee: World Markets and Trade: 2020/21 Forecast OverviewJauhar ArtNo ratings yet

- 09.EK September 2022Document6 pages09.EK September 2022kleber VergaraNo ratings yet

- Sugar Annual: Report NameDocument9 pagesSugar Annual: Report Namenusrat jehanNo ratings yet

- Vodafone Group PLC: DisclaimerDocument17 pagesVodafone Group PLC: DisclaimerTawfiq4444No ratings yet

- 101022-Ecowrap 20221010 PDFDocument6 pages101022-Ecowrap 20221010 PDFVindhuja VijayanNo ratings yet

- Oilseeds and Products Annual Canberra Australia 04-01-2020Document18 pagesOilseeds and Products Annual Canberra Australia 04-01-2020coriolisresearchNo ratings yet

- Thapar Institute of Engineering & Technology, Patiala: (Deemed To Be University)Document12 pagesThapar Institute of Engineering & Technology, Patiala: (Deemed To Be University)Haltz t00nNo ratings yet

- Program Review Chart TemplatesDocument9 pagesProgram Review Chart TemplatesAktar PTDI STTDNo ratings yet

- GoI Slashes SBM-G Budget by 31Document10 pagesGoI Slashes SBM-G Budget by 31Sonmani ChoudharyNo ratings yet

- Director's Report Highlights Record Wheat Production in IndiaDocument80 pagesDirector's Report Highlights Record Wheat Production in Indiakamlesh tiwariNo ratings yet

- Bangladesh's Growing EconomyDocument10 pagesBangladesh's Growing EconomyMizanur RahmanNo ratings yet

- Freshmen Enrollment, Total Enrollment and Graduates of Medical DisciplinesDocument4 pagesFreshmen Enrollment, Total Enrollment and Graduates of Medical DisciplinesIan PalmaNo ratings yet

- 13 Transport and CommunicationDocument26 pages13 Transport and CommunicationHammad ShahzadNo ratings yet

- Interational Energy Outlook EIA 2017-49-64Document16 pagesInterational Energy Outlook EIA 2017-49-64JLeonidas UmaTNo ratings yet

- Club Fundraising AnalysisDocument131 pagesClub Fundraising AnalysisRjendra LamsalNo ratings yet

- 00 AgCommodities202312 v1.0.0Document78 pages00 AgCommodities202312 v1.0.0vive0017No ratings yet

- Sugar Outlook For 2029Document12 pagesSugar Outlook For 2029ٍSahar AboudNo ratings yet

- MCE 8 Instn Building of FPO2Document17 pagesMCE 8 Instn Building of FPO2AMIT KUMAR NAYAKNo ratings yet

- Xiaomi Corp financial analysis 2020Document6 pagesXiaomi Corp financial analysis 2020Chaermalyn Bao-idangNo ratings yet

- KFH Annual Report 2018 - English PDFDocument162 pagesKFH Annual Report 2018 - English PDFFardheen BanuNo ratings yet

- District FundDocument131 pagesDistrict FundRjendra LamsalNo ratings yet

- Wheat Outlook: U.S. 2020/21 Wheat Crop Shrinks On Reduced Outlook For Winter and Other Spring WheatDocument11 pagesWheat Outlook: U.S. 2020/21 Wheat Crop Shrinks On Reduced Outlook For Winter and Other Spring WheatBrittany EtheridgeNo ratings yet

- 07 - Central Visayas Cebu Medical and AlliedDocument4 pages07 - Central Visayas Cebu Medical and AlliedIan PalmaNo ratings yet

- Sujata: %age Turnover of ABCDocument7 pagesSujata: %age Turnover of ABCKunikaNo ratings yet

- Cupid Analyst Report May 2017Document5 pagesCupid Analyst Report May 2017Santosh KadamNo ratings yet

- Meat Market Review Fao 2020Document15 pagesMeat Market Review Fao 2020Robinson Alexander Timana ArevaloNo ratings yet

- Statistics - PSDADocument5 pagesStatistics - PSDADivisha AgarwalNo ratings yet

- ECDocument3 pagesECDinesh YadavNo ratings yet

- Harrison 2022-08-22Document1 pageHarrison 2022-08-22Cherbiti Mohammed AmineNo ratings yet

- Relaxo Footwears: Resilient Performance Amid Challenging ScenarioDocument6 pagesRelaxo Footwears: Resilient Performance Amid Challenging ScenarioGuarachandar ChandNo ratings yet

- Introduction To Hyve December 2021Document36 pagesIntroduction To Hyve December 2021Jose María MateuNo ratings yet

- Coffee Report and Outlook December 2023 ICODocument43 pagesCoffee Report and Outlook December 2023 ICOqiweijhihNo ratings yet

- Connecting Farmers To Markets FPO Update - March 2020Document13 pagesConnecting Farmers To Markets FPO Update - March 2020nirajmyeduNo ratings yet

- Two Wheeler Landscape ChangesDocument37 pagesTwo Wheeler Landscape ChangesGrim ReaperNo ratings yet

- Saregama India: Near Term Challenges PersistDocument5 pagesSaregama India: Near Term Challenges Persistnikhil gayamNo ratings yet

- Awp Department Wise - Kpi 22-23 - LogisticsDocument5 pagesAwp Department Wise - Kpi 22-23 - LogisticsqmsNo ratings yet

- TVS MOTORS by AmbitDocument15 pagesTVS MOTORS by Ambitrs reddy100% (1)

- Annual Report 2015 16 PDFDocument90 pagesAnnual Report 2015 16 PDFanup dasNo ratings yet

- Chemical Enhanced Oil Recovery (EOR)Document7 pagesChemical Enhanced Oil Recovery (EOR)NIRAJ DUBEYNo ratings yet

- Rn1a 2018-2019 en A.fahrerDocument2 pagesRn1a 2018-2019 en A.fahrerBretzel CorporationNo ratings yet

- P#5 - Indian Pulse Production and Market Situation (Dr. Bharat Kulkarni)Document9 pagesP#5 - Indian Pulse Production and Market Situation (Dr. Bharat Kulkarni)RASNo ratings yet

- IDirect UnitedBreweries Q4FY20Document6 pagesIDirect UnitedBreweries Q4FY20dnwekfnkfnknf skkjdbNo ratings yet

- Investment Thesis by Prateek LalDocument2 pagesInvestment Thesis by Prateek LalPrateek LalNo ratings yet

- AY Charlotte Office Report Q4 2022Document11 pagesAY Charlotte Office Report Q4 2022Anonymous gDTyrCzoNo ratings yet

- Soyabean: Supply Demand AnalysisDocument12 pagesSoyabean: Supply Demand AnalysisMudit ChauhanNo ratings yet

- Malaysia Trade Profile 2020Document2 pagesMalaysia Trade Profile 2020Rizal KhalidNo ratings yet

- Kaveri Seeds - June 2021Document10 pagesKaveri Seeds - June 2021gaurav guptaNo ratings yet

- Q1 2021 E Commerce ReportDocument6 pagesQ1 2021 E Commerce ReportEstefania HernandezNo ratings yet

- Food Outlook: Biannual Report on Global Food Markets July 2018From EverandFood Outlook: Biannual Report on Global Food Markets July 2018No ratings yet

- FSM With DCFDocument31 pagesFSM With DCFjustinbui85No ratings yet

- DocsumoDocument2 pagesDocsumojustinbui85No ratings yet

- Tỉ Giá VNDUSD Hằng Tháng (2019 - 2023)Document1 pageTỉ Giá VNDUSD Hằng Tháng (2019 - 2023)justinbui85No ratings yet

- Sperandeo, Victor - Trader Vic - Methods of A Wall Street MasterDocument147 pagesSperandeo, Victor - Trader Vic - Methods of A Wall Street Mastervinengch93% (28)

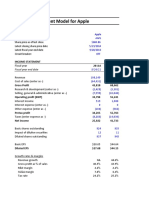

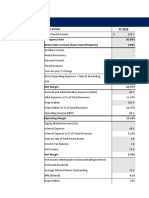

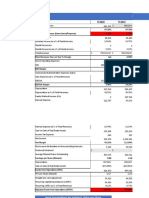

- Financial Statement Model For Apple: $ MM Except Per ShareDocument7 pagesFinancial Statement Model For Apple: $ MM Except Per Sharejustinbui85No ratings yet

- Vanguard DiscussionDocument2 pagesVanguard Discussionjustinbui85No ratings yet

- Step Name Appendix # Uc 1 Uc 2 Uc 3 Uc 4 Uc 5 Uc 6 Uc 7 Uc 8 BPM Use CaseDocument2 pagesStep Name Appendix # Uc 1 Uc 2 Uc 3 Uc 4 Uc 5 Uc 6 Uc 7 Uc 8 BPM Use Casejustinbui85No ratings yet

- Financial Statement Model For Apple: $ MM Except Per ShareDocument7 pagesFinancial Statement Model For Apple: $ MM Except Per Sharejustinbui85No ratings yet

- Ultimate Resume Template College v8 by Andrew Lacivita PDFDocument4 pagesUltimate Resume Template College v8 by Andrew Lacivita PDFOndraSedláčekNo ratings yet

- DCF ConeDocument37 pagesDCF Conejustinbui85No ratings yet

- Equity ValuationDocument20 pagesEquity Valuationjustinbui85No ratings yet

- Team1020walt20disney20case20 13409390077202 Phpapp02 120628220558 Phpapp02Document20 pagesTeam1020walt20disney20case20 13409390077202 Phpapp02 120628220558 Phpapp02justinbui85No ratings yet

- L'Atelier Sungha Jung Tabs PDFDocument8 pagesL'Atelier Sungha Jung Tabs PDFjustinbui85No ratings yet

- Vietnam Coffee Annual Report Forecasts Lower Production, ExportsDocument10 pagesVietnam Coffee Annual Report Forecasts Lower Production, Exportsjustinbui85No ratings yet

- Roku Inc (ROKU US) - AdjustedDocument9 pagesRoku Inc (ROKU US) - Adjustedjustinbui85No ratings yet

- 472 MidtermDocument11 pages472 Midtermjustinbui85No ratings yet

- Project ProposalDocument1 pageProject Proposaljustinbui85No ratings yet

- Disney CaseDocument25 pagesDisney Casejustinbui85No ratings yet

- BPM Analysis TechniquesDocument6 pagesBPM Analysis Techniquesjustinbui85No ratings yet

- BPM Analysis TechniquesDocument6 pagesBPM Analysis Techniquesjustinbui85No ratings yet

- A Smarter Way - To Learn JavaScriptDocument288 pagesA Smarter Way - To Learn JavaScriptImtiaz Ahmed96% (54)

- Manufacturing - LP TemplateDocument1 pageManufacturing - LP Templatejustinbui85No ratings yet

- Chipotle negotiates with suppliersDocument9 pagesChipotle negotiates with suppliersjustinbui85No ratings yet

- Study Id15822 Industry Report Banking and FinanceDocument62 pagesStudy Id15822 Industry Report Banking and Financejustinbui85No ratings yet

- Thesis On Cooperative Banks in IndiaDocument6 pagesThesis On Cooperative Banks in Indiadenisemillerdesmoines100% (2)

- Business A Level Revision Notes Series A PDFDocument30 pagesBusiness A Level Revision Notes Series A PDFruvimbo shoniwaNo ratings yet

- International BusinessDocument3 pagesInternational Businesskarthi320No ratings yet

- Modern Beekeeping Adoption in EthiopiaDocument38 pagesModern Beekeeping Adoption in EthiopiaMehari Temesgen100% (1)

- Department of Economic and Statistical Affairs, HaryanaDocument197 pagesDepartment of Economic and Statistical Affairs, Haryanapchh231No ratings yet

- Persepsi Stakeholder Terhadap Kebutuhan Terminal Barang Di Kota Semarang Berdasarkan FungsinyaDocument5 pagesPersepsi Stakeholder Terhadap Kebutuhan Terminal Barang Di Kota Semarang Berdasarkan FungsinyaHazmi D AlfianNo ratings yet

- Dal Mill RollDocument18 pagesDal Mill Roll123harsh123No ratings yet

- Astm A 193-2020Document14 pagesAstm A 193-2020Mohammed Ali100% (1)

- Risks and Mitigation Strategies in Poultry FarmingDocument108 pagesRisks and Mitigation Strategies in Poultry FarmingTewfic SeidNo ratings yet

- Армения 17.07. Крупняк КомпанииDocument99 pagesАрмения 17.07. Крупняк КомпанииPolli. PNo ratings yet

- World B PDFDocument202 pagesWorld B PDFAnur WakhidNo ratings yet

- Organisational-Chart-Feb-2020 AMSADocument1 pageOrganisational-Chart-Feb-2020 AMSAVicente Brian Paumig Conde Jr.No ratings yet

- Budgetary Estimates - Commercial Urban FarmsDocument14 pagesBudgetary Estimates - Commercial Urban FarmssasideepNo ratings yet

- Proceso de Peletizado - ClarkDocument35 pagesProceso de Peletizado - ClarkHanz Kevin Boy MendozaNo ratings yet

- TNAU Price Forecast For Small Onion - EngDocument2 pagesTNAU Price Forecast For Small Onion - EngH SNo ratings yet

- Junior R&D Technical: Job OpportunityDocument1 pageJunior R&D Technical: Job Opportunitycassilda_carvalho@hotmail.comNo ratings yet

- Complete Economic Revision Nots - 230309 - 104419Document23 pagesComplete Economic Revision Nots - 230309 - 104419Deepankar SinghNo ratings yet

- 25800-220-M6-0330-00002 (004) Celdas Rougher Fila 1Document2 pages25800-220-M6-0330-00002 (004) Celdas Rougher Fila 1Edwing William Salhuana MendozaNo ratings yet

- FM 202 QMS Issue 1-20 JanDocument4 pagesFM 202 QMS Issue 1-20 Jandaniel manafNo ratings yet

- Pepsi Basix Partnership Case Study AnalysisDocument4 pagesPepsi Basix Partnership Case Study AnalysisSayan Bhattacharya100% (1)

- India's Growing Service Sector and its Contribution to GDPDocument19 pagesIndia's Growing Service Sector and its Contribution to GDPfatema_murabbiNo ratings yet

- RFP DCA Annexures Kosi BridgeDocument293 pagesRFP DCA Annexures Kosi BridgePPPnewsNo ratings yet

- Farm Business Operations in Bongabon, Philippines Status and ChallengesDocument5 pagesFarm Business Operations in Bongabon, Philippines Status and ChallengesInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- Minutes of Meetings at Sialmal Coal Mines: SL N o Particulars Completion Date/action Action by RemarksDocument2 pagesMinutes of Meetings at Sialmal Coal Mines: SL N o Particulars Completion Date/action Action by RemarksRAJAT SAMANTANo ratings yet

- Participatory Coconut Planting ProjectDocument2 pagesParticipatory Coconut Planting ProjectCarmelaEspinoNo ratings yet

- Ork DCC Mas Id 001Document10 pagesOrk DCC Mas Id 001Phea RomNo ratings yet

- India's Five Year Plans Goals & Development Policies 1950-1990Document18 pagesIndia's Five Year Plans Goals & Development Policies 1950-1990Cara XNo ratings yet

- AA - Charter Party MeaningDocument4 pagesAA - Charter Party MeaningSeneca CabreraNo ratings yet

- Asdem Newslet56Document8 pagesAsdem Newslet56Jayakumar SankaranNo ratings yet

- 01 Firelock FittingsDocument2 pages01 Firelock FittingsELVIN RODRIGUEZNo ratings yet