You might also like

- A Comparative Analysis of Tax Administration in Asia and the Pacific: 2016 EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific: 2016 EditionNo ratings yet

- Economic and Business Forecasting: Analyzing and Interpreting Econometric ResultsFrom EverandEconomic and Business Forecasting: Analyzing and Interpreting Econometric ResultsNo ratings yet

- Business Plan SampleDocument12 pagesBusiness Plan Sampleyam yam100% (2)

- KPMBM - Bad Debts and Doubtful DebtsDocument51 pagesKPMBM - Bad Debts and Doubtful DebtsAhmad Hafiz50% (2)

- STUDENT Copy Chapter 1 Review of The Accounting CycleDocument28 pagesSTUDENT Copy Chapter 1 Review of The Accounting CycleKurt Latrell AlcantaraNo ratings yet

- O'Level Accounting-Syllabus PDFDocument23 pagesO'Level Accounting-Syllabus PDFSumaia MariamNo ratings yet

- Remedial QuizDocument12 pagesRemedial QuizNadine VilloserNo ratings yet

- FFM Updated AnswersDocument79 pagesFFM Updated AnswersSrikrishnan SNo ratings yet

- Bep ProblemsDocument5 pagesBep ProblemsvamsibuNo ratings yet

- Marginal Costing ProblemsDocument12 pagesMarginal Costing ProblemsPratik ShitoleNo ratings yet

- Economic Insights from Input–Output Tables for Asia and the PacificFrom EverandEconomic Insights from Input–Output Tables for Asia and the PacificNo ratings yet

- Module 3 ACCTG 1 A & B Partnership & CorporationDocument32 pagesModule 3 ACCTG 1 A & B Partnership & CorporationMary Lynn Dela PeñaNo ratings yet

- MA-II Assignment V - Short Run Decision AnalysisDocument4 pagesMA-II Assignment V - Short Run Decision Analysisshriya2413No ratings yet

- Cost Volume Profit Analysis (Decision Making) - TaskDocument9 pagesCost Volume Profit Analysis (Decision Making) - TaskAshwin KarthikNo ratings yet

- 06 BasicAccTP1 SantosDocument3 pages06 BasicAccTP1 SantosJohn Santos100% (1)

- AssignmentDocument11 pagesAssignmentKBA AMIRNo ratings yet

- Problems On Marginal CostingDocument7 pagesProblems On Marginal Costingrathanreddy2002No ratings yet

- MARGINAL COSTIN1 Auto SavedDocument6 pagesMARGINAL COSTIN1 Auto SavedVedant RaneNo ratings yet

- Central College of Business Management: Mid Term Examination: February 2020Document2 pagesCentral College of Business Management: Mid Term Examination: February 2020UNik ROnz OFFICIALNo ratings yet

- MC1Document3 pagesMC1deepalish88No ratings yet

- Co 1815Document4 pagesCo 1815Josh JosephNo ratings yet

- Unit IVDocument14 pagesUnit IVkuselvNo ratings yet

- Model Question For Account409792809472943360Document8 pagesModel Question For Account409792809472943360yugeshNo ratings yet

- Bep QuestionsDocument14 pagesBep QuestionsAvneet OberoiNo ratings yet

- Business Budget - Assignment ProblemsDocument3 pagesBusiness Budget - Assignment ProblemsSHARATH JNo ratings yet

- Cost-Volume-Profit Analysis: Part-A QuestionsDocument10 pagesCost-Volume-Profit Analysis: Part-A QuestionsAtiq RehmanNo ratings yet

- Finan Decision Making II Probs On Decision AnalysisDocument10 pagesFinan Decision Making II Probs On Decision Analysisrathanreddy2002No ratings yet

- MA End TermDocument11 pagesMA End TermShashank AgarwalaNo ratings yet

- Problem of Pricing MethodDocument4 pagesProblem of Pricing MethodKhelin ShahNo ratings yet

- ALl Questions According To TopicsDocument11 pagesALl Questions According To TopicsHassan KhanNo ratings yet

- KL Business Finance May Jun 2017Document2 pagesKL Business Finance May Jun 2017Tanvir PrantoNo ratings yet

- Cost Accounting - 2 2020Document5 pagesCost Accounting - 2 2020Shone Philips ThomasNo ratings yet

- CVP ProblemsDocument6 pagesCVP ProblemsKronisa ChowdharyNo ratings yet

- Symbiosis Center For Management & HRDDocument3 pagesSymbiosis Center For Management & HRDKUMAR ABHISHEKNo ratings yet

- Cost Sheet Questions FastrackDocument8 pagesCost Sheet Questions Fastrackdegikoh540No ratings yet

- Jaya College of Arts and Science Department of ManagDocument4 pagesJaya College of Arts and Science Department of ManagMythili KarthikeyanNo ratings yet

- Question PapeeDocument5 pagesQuestion Papeepurumehta26No ratings yet

- Acm 701 2017-18-1-1-2Document13 pagesAcm 701 2017-18-1-1-2Utkarsh Kumar SrivastavNo ratings yet

- Marginal Costing TutorialDocument5 pagesMarginal Costing TutorialRajyaLakshmiNo ratings yet

- Costing & FM J 2021Document147 pagesCosting & FM J 2021Priya RajNo ratings yet

- Loyola College (Autonomous), Chennai - 600 034: APRIL 2016 Co 6608 - Financial ManagementDocument3 pagesLoyola College (Autonomous), Chennai - 600 034: APRIL 2016 Co 6608 - Financial ManagementvivekNo ratings yet

- Marginal Costing NumericalDocument6 pagesMarginal Costing Numericalswarnim chauhanNo ratings yet

- Tutorial 1Document5 pagesTutorial 1FEI FEINo ratings yet

- Marginal Costing and Break-Even AnalysisDocument6 pagesMarginal Costing and Break-Even AnalysisPrasanna SharmaNo ratings yet

- Practice Set 2 (Cost Segregation and CVP)Document2 pagesPractice Set 2 (Cost Segregation and CVP)Jessica Aningat0% (1)

- Loyola College (Autonomous), Chennai - 600 034: APRIL 2016 Co 6608 - Financial ManagementDocument34 pagesLoyola College (Autonomous), Chennai - 600 034: APRIL 2016 Co 6608 - Financial ManagementSimon JosephNo ratings yet

- Marginal CostingDocument4 pagesMarginal CostingRohan MehtaNo ratings yet

- MC&bepproblemsDocument6 pagesMC&bepproblemsNishanth PrabhakarNo ratings yet

- Variable and Absorption M 02Document6 pagesVariable and Absorption M 02sm munNo ratings yet

- Prob. On CVP & BEP AnalysisDocument4 pagesProb. On CVP & BEP AnalysisMoihekNo ratings yet

- Answer ALL The Questions (10 2 20) Answer ALL The Questions (10 2 20) Answer ALL The Questions (10 2 20)Document4 pagesAnswer ALL The Questions (10 2 20) Answer ALL The Questions (10 2 20) Answer ALL The Questions (10 2 20)Harish KapoorNo ratings yet

- Marginal CostingDocument9 pagesMarginal CostingSharika EpNo ratings yet

- 10 Marginal CostingDocument10 pages10 Marginal CostingVishal Kumar 5504No ratings yet

- Marginal CostingDocument4 pagesMarginal CostingFareha Riaz100% (3)

- Abacus India Ltd.Document3 pagesAbacus India Ltd.Minto MathewNo ratings yet

- 8104 MbaexDocument3 pages8104 Mbaexgaurav jainNo ratings yet

- Cost and Management Accounting Pass 2019Document3 pagesCost and Management Accounting Pass 2019AditNo ratings yet

- Symbiosis International (Deemed University)Document3 pagesSymbiosis International (Deemed University)waqar.baig2025No ratings yet

- 9 Budgets - Budgetary ControlDocument10 pages9 Budgets - Budgetary ControlLakshay SharmaNo ratings yet

- Metrillo - Comprehensive ProbDocument12 pagesMetrillo - Comprehensive ProbLordCelene C MagyayaNo ratings yet

- BBS - 1st - Financial Accounting and AnalysisDocument46 pagesBBS - 1st - Financial Accounting and AnalysisJALDIMAINo ratings yet

- Adobe Scan 01 Jul 2023Document5 pagesAdobe Scan 01 Jul 2023Faisal NawazNo ratings yet

- MCS Question BankDocument4 pagesMCS Question BankVrushali P.No ratings yet

- 2017 International Comparison Program for Asia and the Pacific: Purchasing Power Parities and Real Expenditures—Results and MethodologyFrom Everand2017 International Comparison Program for Asia and the Pacific: Purchasing Power Parities and Real Expenditures—Results and MethodologyNo ratings yet

- 2017 International Comparison Program in Asia and the Pacific: Purchasing Power Parities and Real Expenditures—A Summary ReportFrom Everand2017 International Comparison Program in Asia and the Pacific: Purchasing Power Parities and Real Expenditures—A Summary ReportNo ratings yet

- One Year of Living with COVID-19: An Assessment of How ADB Members Fought the Pandemic in 2020From EverandOne Year of Living with COVID-19: An Assessment of How ADB Members Fought the Pandemic in 2020No ratings yet

- Group A Attempt All Questions. (2X10 20) : Questions (20) The New Training ProgramDocument6 pagesGroup A Attempt All Questions. (2X10 20) : Questions (20) The New Training ProgramUNik ROnz OFFICIALNo ratings yet

- Central College of Business Management Central College of Business ManagementDocument2 pagesCentral College of Business Management Central College of Business ManagementUNik ROnz OFFICIALNo ratings yet

- OM QuestionsDocument5 pagesOM QuestionsUNik ROnz OFFICIALNo ratings yet

- Central College of Business Management Central College of Business ManagementDocument2 pagesCentral College of Business Management Central College of Business ManagementUNik ROnz OFFICIALNo ratings yet

- SIC InterpretationsDocument42 pagesSIC InterpretationsJean Fajardo Badillo100% (1)

- Hire Purchases and Instalment Purchase System ExercisesDocument18 pagesHire Purchases and Instalment Purchase System ExercisesHarsha Baby100% (1)

- Review - Basic For StudentDocument13 pagesReview - Basic For StudentMai LinhNo ratings yet

- National Accounting Standard For Commercial Organisations 1 "Presentation of Financial Statements"Document15 pagesNational Accounting Standard For Commercial Organisations 1 "Presentation of Financial Statements"azimovazNo ratings yet

- Enseval-Putera-Megatrading Billingual 31 Des 2016 Released-SecuredDocument113 pagesEnseval-Putera-Megatrading Billingual 31 Des 2016 Released-SecuredAnto KristianNo ratings yet

- Debt F-GDocument261 pagesDebt F-GkenindiNo ratings yet

- Partnership FormationDocument6 pagesPartnership FormationXajimarie StylesNo ratings yet

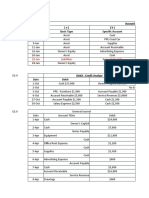

- Account Debited (A) (B) Date Basic Type Specific AccountDocument12 pagesAccount Debited (A) (B) Date Basic Type Specific AccountVALENCIA TORENTHANo ratings yet

- Teori Akuntansi Soal JawabDocument5 pagesTeori Akuntansi Soal JawabDarren LatifNo ratings yet

- Intermediate Financial Management 11th Edition Brigham Test BankDocument20 pagesIntermediate Financial Management 11th Edition Brigham Test Banknicholasyoungxqwsbcdogz100% (34)

- Inventories and Investment Theories v2Document10 pagesInventories and Investment Theories v2Joovs JoovhoNo ratings yet

- 01 PowerpointDocument64 pages01 PowerpointVave IsraelNo ratings yet

- Baniya Kirana Stores F.Y. 2074-75 TaxDocument17 pagesBaniya Kirana Stores F.Y. 2074-75 TaxasasasNo ratings yet

- ZDC Act 2014 - FinalDocument17 pagesZDC Act 2014 - FinalBILAL KHANNo ratings yet

- AEC 5211 Practical 1 Balance SheetDocument2 pagesAEC 5211 Practical 1 Balance SheetNIDHINo ratings yet

- Exam ReviewerDocument10 pagesExam Reviewerjoseph christopher vicenteNo ratings yet

- Financial AccountingDocument181 pagesFinancial AccountingMinhaz UddinNo ratings yet

- Accountancy (+2 2nd Year New Batch)Document3 pagesAccountancy (+2 2nd Year New Batch)sourabh sabatNo ratings yet

- Shipping Companies' Financial Performance Measurement Using Industry Key Performance Indicators Case Study: The Highly Volatile Period 2007 - 2010Document22 pagesShipping Companies' Financial Performance Measurement Using Industry Key Performance Indicators Case Study: The Highly Volatile Period 2007 - 2010Luis Enrique LavayenNo ratings yet

- Accounting Week 2Document3 pagesAccounting Week 2Erryn M. ParamythaNo ratings yet

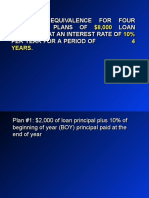

- Economic Equivalence For Four Repayment Plans of $8,000 Loan Borrowed at An Interest Rate of 10% Per Year For A Period of 4 YearsDocument21 pagesEconomic Equivalence For Four Repayment Plans of $8,000 Loan Borrowed at An Interest Rate of 10% Per Year For A Period of 4 YearsMuhammad atif latifNo ratings yet

- FM SethDocument30 pagesFM SethUtsav MehtaNo ratings yet

- PST CL 2015 2023Document88 pagesPST CL 2015 2023Benny MwaloziNo ratings yet