You might also like

- Solution NIngDocument3 pagesSolution NIngfahim tusarNo ratings yet

- Less: Cost of Goods Sold: Capital ExpenditureDocument3 pagesLess: Cost of Goods Sold: Capital Expenditurefahim tusarNo ratings yet

- Financial Reporting, Statement and Analysis Assignment For 2 Semester Name: Dishant Tibrewal SUBMISSION DATE - 16/07/21Document3 pagesFinancial Reporting, Statement and Analysis Assignment For 2 Semester Name: Dishant Tibrewal SUBMISSION DATE - 16/07/21Dishant TibrewalNo ratings yet

- UntitledDocument13 pagesUntitledTejasree SaiNo ratings yet

- Prefinal Exam - SolutionDocument7 pagesPrefinal Exam - SolutionKarlo PalerNo ratings yet

- Tutorial 1 27 April 2022Document6 pagesTutorial 1 27 April 2022Swee Yi LeeNo ratings yet

- Ultimate Book of Accountancy: Brilliant ProblemsDocument9 pagesUltimate Book of Accountancy: Brilliant ProblemsPramod VasudevNo ratings yet

- Close LTDDocument5 pagesClose LTDXianFa WongNo ratings yet

- Cashflow ActivityDocument2 pagesCashflow ActivityHannie CaratNo ratings yet

- Consolidation/Group Accounts: Example 18: Disposal of SubsidiaryDocument4 pagesConsolidation/Group Accounts: Example 18: Disposal of SubsidiaryMuhammad Sarfraz AsmatNo ratings yet

- Acc Chapter 5Document11 pagesAcc Chapter 5NURUL HAZWANIE HIDNI BINTI MUHAMAD SABRI MoeNo ratings yet

- Apple Inc Com Economatica in Dollar US in Thousands: Profit Loss From Operating ActivitiesDocument3 pagesApple Inc Com Economatica in Dollar US in Thousands: Profit Loss From Operating ActivitiesJaime Alexander PENA VILLABONANo ratings yet

- Answer Exercise 1Document2 pagesAnswer Exercise 1Puteri Noor SyahiraNo ratings yet

- Cash Flow Statement and Financial Ratio AssignDocument4 pagesCash Flow Statement and Financial Ratio AssignChristian TanNo ratings yet

- BADVAC1XDocument8 pagesBADVAC1Xfaye pantiNo ratings yet

- ACC106 Assignment AccountDocument5 pagesACC106 Assignment AccountsyafiqahNo ratings yet

- Advanced Taxation - Solutions To Pilot Questions Suggested Solution To Question 1Document23 pagesAdvanced Taxation - Solutions To Pilot Questions Suggested Solution To Question 1Oyebisi OpeyemiNo ratings yet

- 8447809Document11 pages8447809blackghostNo ratings yet

- Assignment E & L Env 4 BusiDocument9 pagesAssignment E & L Env 4 BusiSyed Hamza RasheedNo ratings yet

- Solution Comp Acc Soalan 1Document4 pagesSolution Comp Acc Soalan 1maiNo ratings yet

- Ong Motors CorporationDocument4 pagesOng Motors CorporationJudy Ann Acruz100% (1)

- Suggested Answers Certified Finance and Accounting Professional Examination - Summer 2018Document7 pagesSuggested Answers Certified Finance and Accounting Professional Examination - Summer 2018Muhammad Usama SheikhNo ratings yet

- HW5.FT222004.Archit KumarDocument7 pagesHW5.FT222004.Archit KumarARCHIT KUMARNo ratings yet

- Bharat Chemicals Ltd. CPHi46l2eHDocument2 pagesBharat Chemicals Ltd. CPHi46l2eHChickooNo ratings yet

- Chapter-21 (Solved Past Papers of CA Mod CDocument67 pagesChapter-21 (Solved Past Papers of CA Mod CJer Rama100% (4)

- AssignmentDocument39 pagesAssignmentralph yapNo ratings yet

- IAS 12 Solutions PDFDocument74 pagesIAS 12 Solutions PDFrafid aliNo ratings yet

- Ratio Excercise 2Document1 pageRatio Excercise 2Marwan AqrabNo ratings yet

- Cost Accounting: Rs. Rs. Rs. Rs. Rs. RsDocument8 pagesCost Accounting: Rs. Rs. Rs. Rs. Rs. RsShehrozSTNo ratings yet

- SS Mid-Term Test Tax517 July 2022 Student VersionDocument6 pagesSS Mid-Term Test Tax517 July 2022 Student VersionFeahRafeah KikiNo ratings yet

- CSEC Accounting Formats and TemplatesDocument15 pagesCSEC Accounting Formats and TemplatesRealGenius (Carl)No ratings yet

- Weekly Asigment 1Document1 pageWeekly Asigment 1Inge setiawanNo ratings yet

- TAÑOTE Daisy AEC7 MEPIIDocument9 pagesTAÑOTE Daisy AEC7 MEPIIDaisy TañoteNo ratings yet

- The Statement of Cash Flows Problems 5-1. (Currency Company)Document7 pagesThe Statement of Cash Flows Problems 5-1. (Currency Company)Marcos DmitriNo ratings yet

- Worksheet-4 On CFSDocument6 pagesWorksheet-4 On CFSNavya KhemkaNo ratings yet

- Taxation Solution 2018 SeptemberDocument9 pagesTaxation Solution 2018 SeptemberIffah NasuhaaNo ratings yet

- Hasil Abnormal ReturnDocument1 pageHasil Abnormal ReturnSurya KeceNo ratings yet

- ACT320 Assignment ProjectDocument11 pagesACT320 Assignment ProjectMd. Shakil Ahmed 1620890630No ratings yet

- For The Year Ended December 31, 2020: Rcs Consultancy CorporationDocument11 pagesFor The Year Ended December 31, 2020: Rcs Consultancy CorporationYzzabel Denise L. TolentinoNo ratings yet

- Ma AssigmentDocument32 pagesMa AssigmentAashayNo ratings yet

- Accounting For Managers (Assignment One (E-Finance) ) Question OneDocument7 pagesAccounting For Managers (Assignment One (E-Finance) ) Question OnehananNo ratings yet

- Taxation Solution 2017 SeptemberDocument11 pagesTaxation Solution 2017 Septemberzezu zazaNo ratings yet

- FFS - Numericals 2Document3 pagesFFS - Numericals 2Funny ManNo ratings yet

- Intl Business Machines Corp Com Economatica in Dollar US in ThousandsDocument2 pagesIntl Business Machines Corp Com Economatica in Dollar US in Thousandsluisa Fernanda PeñaNo ratings yet

- CHAPTER 15 17 InvestmentsDocument38 pagesCHAPTER 15 17 InvestmentsJinkyNo ratings yet

- Solution Tax667 - Jun 2016-1Document8 pagesSolution Tax667 - Jun 2016-1Zahiratul QamarinaNo ratings yet

- CFAS 16 and 18Document2 pagesCFAS 16 and 18Cath OquialdaNo ratings yet

- Tax 9Document2 pagesTax 9Anusha SharmaNo ratings yet

- TP1-W2-S3-R0 Sri Annisa KatariDocument3 pagesTP1-W2-S3-R0 Sri Annisa Katarisri annisa katariNo ratings yet

- Assignment1 - Profit and Loss Exercise E FinanceDocument8 pagesAssignment1 - Profit and Loss Exercise E Financees.eldeebNo ratings yet

- The Hong Kong Polytechnic University Hong Kong Community CollegeDocument6 pagesThe Hong Kong Polytechnic University Hong Kong Community CollegeFung Yat Kit KeithNo ratings yet

- Examination Question and Answers, Set D (Problem Solving), Chapter 15 - Statement of Cash FlowDocument2 pagesExamination Question and Answers, Set D (Problem Solving), Chapter 15 - Statement of Cash Flowjohn carlos doringoNo ratings yet

- Economatica Actividad 6Document17 pagesEconomatica Actividad 6Jenny Zulay SUAREZ SOLANONo ratings yet

- Ultimate Book of Accountancy: Dr. Vinod Kumar Vishvas PublicationsDocument4 pagesUltimate Book of Accountancy: Dr. Vinod Kumar Vishvas PublicationsPramod VasudevNo ratings yet

- Pr. 4-146-Income StatementDocument13 pagesPr. 4-146-Income StatementElene SamnidzeNo ratings yet

- Exam 14 October 2012, Answers Exam 14 October 2012, AnswersDocument9 pagesExam 14 October 2012, Answers Exam 14 October 2012, AnswerscandiceNo ratings yet

- 1capital and Revenue TransactionsDocument11 pages1capital and Revenue Transactionsdilhani sheharaNo ratings yet

- Assignment 2Document6 pagesAssignment 2TAWHID ARMANNo ratings yet

- Problem 1 2 3Document4 pagesProblem 1 2 3Ma Theresa MaguadNo ratings yet

- Equity Valuation: Models from Leading Investment BanksFrom EverandEquity Valuation: Models from Leading Investment BanksJan ViebigNo ratings yet

- Test 5-ConsolidationDocument3 pagesTest 5-ConsolidationAli OptimisticNo ratings yet

- CH 6 - Activity Based Costing UpdatedDocument16 pagesCH 6 - Activity Based Costing UpdatedAli OptimisticNo ratings yet

- Impacts of Adverse Macro Environment On AuditDocument7 pagesImpacts of Adverse Macro Environment On AuditAli OptimisticNo ratings yet

- 5.consolidated SOCI - AAFRDocument11 pages5.consolidated SOCI - AAFRAli OptimisticNo ratings yet

- Final FAR-2 Mock Q. PaperDocument6 pagesFinal FAR-2 Mock Q. PaperAli OptimisticNo ratings yet

- 1-Final Account Disclosures Rev (110822)Document20 pages1-Final Account Disclosures Rev (110822)Ali OptimisticNo ratings yet

- IAS-12 Lecture NotesDocument11 pagesIAS-12 Lecture NotesAli OptimisticNo ratings yet

- CAF-07 Assessment-1 Solution: Answer-1 A) Date Particular Dr. Cr. 2015Document5 pagesCAF-07 Assessment-1 Solution: Answer-1 A) Date Particular Dr. Cr. 2015Ali OptimisticNo ratings yet

- Introduction To Computing Lab # 2: C++ Tool LearningDocument1 pageIntroduction To Computing Lab # 2: C++ Tool LearningAli OptimisticNo ratings yet

- Substantive Procedures (1-Page Summary)Document2 pagesSubstantive Procedures (1-Page Summary)Ali OptimisticNo ratings yet

- Institute of Chartered Accountants of PakistanDocument6 pagesInstitute of Chartered Accountants of PakistanAli OptimisticNo ratings yet

- Institute of Chartered Accountants of PakistanDocument7 pagesInstitute of Chartered Accountants of PakistanAli OptimisticNo ratings yet

- IFRS 16 - by Zubair SaleemDocument34 pagesIFRS 16 - by Zubair SaleemAli OptimisticNo ratings yet

- Assessment IDocument2 pagesAssessment IAli OptimisticNo ratings yet

- Institute of Chartered Accountants of PakistanDocument5 pagesInstitute of Chartered Accountants of PakistanAli OptimisticNo ratings yet

- Blaw Mock Spring 19Document5 pagesBlaw Mock Spring 19Ali OptimisticNo ratings yet

- 2013 Paper F8 Mnemonics and Charts Sample Download v1Document71 pages2013 Paper F8 Mnemonics and Charts Sample Download v1Ali OptimisticNo ratings yet

- Lab 4 - Graded TasksDocument1 pageLab 4 - Graded TasksAli OptimisticNo ratings yet

- Answers of Modal Paper AFC-3 (Quantitative Techniques) Prepared by DAWOOD SHAHIDDocument1 pageAnswers of Modal Paper AFC-3 (Quantitative Techniques) Prepared by DAWOOD SHAHIDAli OptimisticNo ratings yet

- Assignment 3 Part 2: Input Case 1: Input Case 2Document2 pagesAssignment 3 Part 2: Input Case 1: Input Case 2Ali OptimisticNo ratings yet

- Introduction To Computing:: Dead Line For Assignment Submission: 2 November 2018 11:55pmDocument2 pagesIntroduction To Computing:: Dead Line For Assignment Submission: 2 November 2018 11:55pmAli OptimisticNo ratings yet

- 03 Afc QM MP 2013Document9 pages03 Afc QM MP 2013Ali OptimisticNo ratings yet

- Dryrun Practice QuestionsDocument6 pagesDryrun Practice QuestionsAli Optimistic0% (1)

- ENG - 1 Course Outline - Fall 2018Document8 pagesENG - 1 Course Outline - Fall 2018Ali OptimisticNo ratings yet

- Adverb QuizDocument9 pagesAdverb QuizAli OptimisticNo ratings yet

- Introduction To Computing Lab # 2: C++ Tool LearningDocument1 pageIntroduction To Computing Lab # 2: C++ Tool LearningAli OptimisticNo ratings yet

- Assignment 3 Part 1Document2 pagesAssignment 3 Part 1Ali OptimisticNo ratings yet

- LAB - 04 Bscs Fall 2018: Introduction To ComputingDocument5 pagesLAB - 04 Bscs Fall 2018: Introduction To ComputingAli OptimisticNo ratings yet

- University of Central Punjab Basic ElectronicsDocument2 pagesUniversity of Central Punjab Basic ElectronicsAli OptimisticNo ratings yet

- Test 4Document2 pagesTest 4Ali OptimisticNo ratings yet

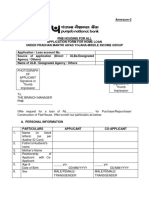

- Application Form For PMAY MIG Loan PDFDocument8 pagesApplication Form For PMAY MIG Loan PDFakibNo ratings yet

- What Is Revenue Recognition?Document9 pagesWhat Is Revenue Recognition?MishuNo ratings yet

- Fringe Benefit Tax Dealings in PropertiesDocument13 pagesFringe Benefit Tax Dealings in PropertiesBea Marie BernardoNo ratings yet

- Indian Income Tax Return Acknowledgement 2022-23: Assessment YearDocument1 pageIndian Income Tax Return Acknowledgement 2022-23: Assessment YearRahul Kumar PatelNo ratings yet

- Percentage Tax Return: BIR Form NoDocument2 pagesPercentage Tax Return: BIR Form NoRichard Rhamil Carganillo Garcia Jr.No ratings yet

- Receipt of House RentDocument2 pagesReceipt of House Rentsunny sagarNo ratings yet

- Employee Details Payment & Leave Details: Arrears Current AmountDocument1 pageEmployee Details Payment & Leave Details: Arrears Current AmountSuresh ChandraNo ratings yet

- RMO No.49-2018Document2 pagesRMO No.49-2018FloisNo ratings yet

- Capital Gains Taxation-3Document37 pagesCapital Gains Taxation-3Cory RitaNo ratings yet

- E-Return Acknowledgment Receipt: Personal Information and Return Filing DetailsDocument1 pageE-Return Acknowledgment Receipt: Personal Information and Return Filing DetailsFaith OndiekiNo ratings yet

- About & Tax Regime: Frequently Asked Questions (FAQ)Document6 pagesAbout & Tax Regime: Frequently Asked Questions (FAQ)umasankarNo ratings yet

- Lovely Professional University Academic Task-1 Mittal School of BusinessDocument9 pagesLovely Professional University Academic Task-1 Mittal School of BusinessPankaj MahantaNo ratings yet

- AnswersDocument7 pagesAnswersQueen ValleNo ratings yet

- CIR v. PrietoDocument2 pagesCIR v. PrietoFSCBNo ratings yet

- This Study Resource Was: Saint Paul School of Business and LawDocument4 pagesThis Study Resource Was: Saint Paul School of Business and LawKim FloresNo ratings yet

- DR Reddy Lab 5 Year DataDocument4 pagesDR Reddy Lab 5 Year Datashishir5087No ratings yet

- Engagement Letter For Business Bookkeeping and Tax PrepartionDocument2 pagesEngagement Letter For Business Bookkeeping and Tax PrepartionPinky Daisies100% (1)

- Problem Exercises - TaxationDocument2 pagesProblem Exercises - TaxationDanny LabordoNo ratings yet

- Green Clean SpreadsheetDocument3 pagesGreen Clean SpreadsheetRalph MorganNo ratings yet

- Sarda Electrical Servicing Began Operations Two Years Ago Its AdjustedDocument1 pageSarda Electrical Servicing Began Operations Two Years Ago Its AdjustedTaimur TechnologistNo ratings yet

- ITAT-No Income Tax On Adjustment of Excess Salary RecoverdDocument3 pagesITAT-No Income Tax On Adjustment of Excess Salary RecoverdManok KumarNo ratings yet

- Use Detailed Income Tax Calculator With More Features and Functions For All IndividualsDocument3 pagesUse Detailed Income Tax Calculator With More Features and Functions For All IndividualsVishwaNo ratings yet

- Encana Corporation: The Cost of Capital: Ivey Case No. 907N02 A) Cost of Equity Dividend Growth ModelDocument5 pagesEncana Corporation: The Cost of Capital: Ivey Case No. 907N02 A) Cost of Equity Dividend Growth ModelAninda DuttaNo ratings yet

- TDS For Overseas Agents When There Is No PE in IndiaDocument9 pagesTDS For Overseas Agents When There Is No PE in Indiasanket.tatedNo ratings yet

- ITR's and AssessmentDocument11 pagesITR's and Assessmentashutosh4iipmNo ratings yet

- Total Earnings Total Deductions: Net Pay (RS.) 41,000.00Document1 pageTotal Earnings Total Deductions: Net Pay (RS.) 41,000.00Diwakar ChaturvediNo ratings yet

- Taxation Atty. Macmod, Cpa Partnership, Estates & Trusts: ST NDDocument1 pageTaxation Atty. Macmod, Cpa Partnership, Estates & Trusts: ST NDFaye Cecil Posadas CuramingNo ratings yet

- 1601eq 1q Ebc-LarDocument1 page1601eq 1q Ebc-LarDIANNE ROCONo ratings yet

- Accounting For Sole Proprietorship Problem1-5Document8 pagesAccounting For Sole Proprietorship Problem1-5Rocel Domingo100% (1)

- Theoretical Problems: Chapter Deductions Out Gross Total (Including of Income Tax)Document25 pagesTheoretical Problems: Chapter Deductions Out Gross Total (Including of Income Tax)chandrani4029No ratings yet