You might also like

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (589)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (842)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5806)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Safety Perception Survey Based HRA at RefineryDocument5 pagesSafety Perception Survey Based HRA at RefineryK3L UP3 SERPONGNo ratings yet

- 5 M's of ManagementDocument3 pages5 M's of ManagementrajtulyaNo ratings yet

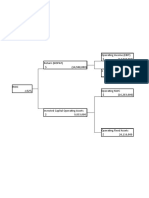

- OIDD6360 - Peapod ROICTreeDocument6 pagesOIDD6360 - Peapod ROICTreeA JNo ratings yet

- Dokumen - Tips Sap Co PC Product Costing WorkshopDocument150 pagesDokumen - Tips Sap Co PC Product Costing WorkshopBalanathan VirupasanNo ratings yet

- QUALITY CONTROL PROCEDURE FOR INSTALLATION & TESTING OF FIRE FIGHTING PIPING SYSTEM AND ACCESSORIES - The Engineer's BlogDocument12 pagesQUALITY CONTROL PROCEDURE FOR INSTALLATION & TESTING OF FIRE FIGHTING PIPING SYSTEM AND ACCESSORIES - The Engineer's BlogNESTOR YUMULNo ratings yet

- Chapter 6 OverheadsDocument3 pagesChapter 6 OverheadsDevender SinghNo ratings yet

- Chapter 5 ReconciliationDocument7 pagesChapter 5 ReconciliationDevender SinghNo ratings yet

- Chapter 4 Cost SheetDocument9 pagesChapter 4 Cost SheetDevender SinghNo ratings yet

- Chapter 3 ProcessDocument8 pagesChapter 3 ProcessDevender SinghNo ratings yet

- Chapter 1 MaterialDocument15 pagesChapter 1 MaterialDevender SinghNo ratings yet

- Consulting BD: Multi-Directional Support For EnterpriseDocument6 pagesConsulting BD: Multi-Directional Support For EnterpriseRajib Ul HaqueNo ratings yet

- The Stakeholders Group 3 SRGGDocument15 pagesThe Stakeholders Group 3 SRGGFuyumi HikotoNo ratings yet

- SERVICE MANAGEMENT Unit 3Document10 pagesSERVICE MANAGEMENT Unit 3Parth KumarNo ratings yet

- Cost & MGT Accounting - Lecture Note - Ch. 3 & 4Document28 pagesCost & MGT Accounting - Lecture Note - Ch. 3 & 4Ashe BalchaNo ratings yet

- Philip Niraj Joseph - 80206200005 - Analytics For ManagersDocument4 pagesPhilip Niraj Joseph - 80206200005 - Analytics For ManagersPhilip NjNo ratings yet

- Entrepreneurship PPT 2 2Document16 pagesEntrepreneurship PPT 2 2Amabelle AbapoNo ratings yet

- Internal Verification of Assessment Decisions - BTEC (RQF) : Higher NationalsDocument44 pagesInternal Verification of Assessment Decisions - BTEC (RQF) : Higher NationalsJASRA FAZEERNo ratings yet

- Business Profile - IKRAM QADocument9 pagesBusiness Profile - IKRAM QAamwin bizNo ratings yet

- 22 27351 002 Matter 1 1 Device Library SpecificationDocument95 pages22 27351 002 Matter 1 1 Device Library Specificationcagona5339No ratings yet

- Quality Management For The Medical Laboratory: Michael Noble MD FRCPCDocument26 pagesQuality Management For The Medical Laboratory: Michael Noble MD FRCPCRobinson KetarenNo ratings yet

- Lecture 11 - Standards On Auditing (SA 540 and 550)Document7 pagesLecture 11 - Standards On Auditing (SA 540 and 550)Harshit JainNo ratings yet

- Asian Paints Internship ReportDocument39 pagesAsian Paints Internship Reportrakibulislammbstu01100% (1)

- Managing Human Resources Canadian 8th Edition Belcourt Solutions ManualDocument25 pagesManaging Human Resources Canadian 8th Edition Belcourt Solutions ManualJohnPinedacfbd100% (56)

- 08 Project Performance DomainsDocument9 pages08 Project Performance DomainsShivansh TulsyanNo ratings yet

- PA3 Quispe1 Puclla2 Gutirrez3 Serrano4 Zacarias5Document10 pagesPA3 Quispe1 Puclla2 Gutirrez3 Serrano4 Zacarias5Paola MendezNo ratings yet

- Chapter 12 PresentationDocument31 pagesChapter 12 PresentationWa Qās RajpoøtNo ratings yet

- Project Management A Managerial Approach 10th Edition Meredith Test BankDocument36 pagesProject Management A Managerial Approach 10th Edition Meredith Test Bankincubousbrocard.u8eo02100% (12)

- Harshita Mishra CV 2023Document7 pagesHarshita Mishra CV 2023Satish SrivastavaNo ratings yet

- Inc42's 100 Unicorn Report 2022Document253 pagesInc42's 100 Unicorn Report 2022imrahulpasiNo ratings yet

- Discussion Questions (Participation)Document4 pagesDiscussion Questions (Participation)Sam SamNo ratings yet

- SCM Chapter 5Document4 pagesSCM Chapter 5mini moniNo ratings yet

- Sample Report-BBADocument24 pagesSample Report-BBASabbir Hossan ChowdhuryNo ratings yet

- Executive Assistant JDDocument3 pagesExecutive Assistant JDMadhura DhoreNo ratings yet

- Retrofitting Strengthening of Permanent Bridges - Magus BridgeDocument3 pagesRetrofitting Strengthening of Permanent Bridges - Magus BridgeJohn Rheynor MayoNo ratings yet

- BBC International LTD 1t 24may2020 UbsDocument19 pagesBBC International LTD 1t 24may2020 Ubspezhmanbayat924No ratings yet