You might also like

- Executive's Guide to Fair Value: Profiting from the New Valuation RulesFrom EverandExecutive's Guide to Fair Value: Profiting from the New Valuation RulesNo ratings yet

- Optimize profits with managerial economicsDocument9 pagesOptimize profits with managerial economicsKang ChulNo ratings yet

- Cash Return on Capital Invested: Ten Years of Investment Analysis with the CROCI Economic Profit ModelFrom EverandCash Return on Capital Invested: Ten Years of Investment Analysis with the CROCI Economic Profit ModelRating: 5 out of 5 stars5/5 (3)

- Chap 001Document28 pagesChap 001Kyren GreiggNo ratings yet

- Sesi01 Dasar Ekonomi ManajerialDocument26 pagesSesi01 Dasar Ekonomi ManajerialjuwelismailNo ratings yet

- Fundamentals of Managerial EconomicsDocument14 pagesFundamentals of Managerial EconomicsLyka RamosNo ratings yet

- Roles of An Effective ManagerDocument15 pagesRoles of An Effective ManagerMarin, Nicole DondoyanoNo ratings yet

- Managerial Economics An Analysis of Business IssuesDocument25 pagesManagerial Economics An Analysis of Business Issueslinda zyongweNo ratings yet

- ACF2 2024Document30 pagesACF2 2024rodrigo.felix17012002No ratings yet

- Introduction To Enterprise Valuation Inkedup-1Document59 pagesIntroduction To Enterprise Valuation Inkedup-1FrancisDrakeNo ratings yet

- UntitledDocument24 pagesUntitledAnkit YadavNo ratings yet

- 2.the Theory of The FirmDocument9 pages2.the Theory of The FirmRazvan Dima100% (1)

- Financing Your GrowthDocument81 pagesFinancing Your Growthtidiane.syNo ratings yet

- Financial Market AnalysisDocument21 pagesFinancial Market Analysishareesh008No ratings yet

- C2 Revision of Concepts v1Document11 pagesC2 Revision of Concepts v1Umer FarooqNo ratings yet

- Concepts of Value and Return - Chapter 2Document26 pagesConcepts of Value and Return - Chapter 2RabinNo ratings yet

- Capital Budgeting-Investment Decision CriteriaDocument57 pagesCapital Budgeting-Investment Decision CriteriaSheila ArjonaNo ratings yet

- Present Value Analysis of Flu Vaccine StrategiesDocument35 pagesPresent Value Analysis of Flu Vaccine StrategiesTarekegnBelayNo ratings yet

- Managerial Economics: An Analysis of Business IssuesDocument25 pagesManagerial Economics: An Analysis of Business IssuesMamta GanatwarNo ratings yet

- CH - 02 Concept of Value and ReturnDocument25 pagesCH - 02 Concept of Value and ReturnMrhunt394 YTNo ratings yet

- Fundamental Economic Concepts ExplainedDocument34 pagesFundamental Economic Concepts ExplainedWilliam DC RiveraNo ratings yet

- Chapter 1 Fundamentals of Managerial Economics PDFDocument25 pagesChapter 1 Fundamentals of Managerial Economics PDFNeni BangunNo ratings yet

- Start Working On Chapter One Homework: Numbers 10, 12 and 17Document14 pagesStart Working On Chapter One Homework: Numbers 10, 12 and 17maxinejoyjuareNo ratings yet

- Chapter3 EFA2 NPVDocument29 pagesChapter3 EFA2 NPVDương DươngNo ratings yet

- Damodaran On ValuationDocument102 pagesDamodaran On Valuationgioro_mi100% (4)

- Topic 2. Discounting: Future ValueDocument13 pagesTopic 2. Discounting: Future ValueАндрей ДымовNo ratings yet

- Managerial EconomicsDocument28 pagesManagerial EconomicsPrakhar SahayNo ratings yet

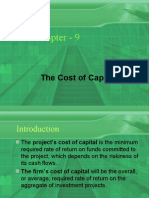

- Cost of Capital Calculation and AnalysisDocument36 pagesCost of Capital Calculation and AnalysisPrashant Kapoor0% (1)

- Chapter 11Document25 pagesChapter 11aleema anjumNo ratings yet

- Cost of CapitalDocument11 pagesCost of CapitalMANSI JOSHINo ratings yet

- ING - Equity ValDocument42 pagesING - Equity ValoladipupotijaniNo ratings yet

- Manage corporate finance objectives and maximize firm valueDocument15 pagesManage corporate finance objectives and maximize firm valueAjay AjayNo ratings yet

- Money Time RelationshipsDocument6 pagesMoney Time RelationshipsKevin KoNo ratings yet

- Cash Flow Estimation and Risk AnalysisDocument51 pagesCash Flow Estimation and Risk AnalysisANo ratings yet

- Chapter-4Document7 pagesChapter-4Hal kNo ratings yet

- Capital Budgeting Methods and CalculationsDocument80 pagesCapital Budgeting Methods and Calculationssharon torrefielNo ratings yet

- Capital Budgeting Methods and CalculationsDocument80 pagesCapital Budgeting Methods and CalculationsVillena Divina Victoria100% (1)

- Unit 3Document71 pagesUnit 3martaNo ratings yet

- Calculate CPI, inflation rates, and exchange ratesDocument8 pagesCalculate CPI, inflation rates, and exchange ratesNguyễn Long VũNo ratings yet

- Tools For Project Evaluation l3prj - Eval - Fina2Document41 pagesTools For Project Evaluation l3prj - Eval - Fina2api-27145250No ratings yet

- CH 09 RevisedDocument36 pagesCH 09 RevisedNiharikaChouhanNo ratings yet

- Financial Management:: Investment Decision CriteriaDocument96 pagesFinancial Management:: Investment Decision CriteriaBen OusoNo ratings yet

- Time Value of MoneyDocument43 pagesTime Value of Moneym.gerryNo ratings yet

- Valuing Distressed Firms & Assets Under 40 CharactersDocument67 pagesValuing Distressed Firms & Assets Under 40 CharactersSaputra SanjayaNo ratings yet

- Smart Summary Equity Valuation Concepts and Basic Tools CFADocument4 pagesSmart Summary Equity Valuation Concepts and Basic Tools CFABhuvnesh KotharNo ratings yet

- ch1 Notes CfaDocument18 pagesch1 Notes Cfaashutosh JhaNo ratings yet

- Financial Management: Jia, Ning (贾宁) School of Economics and Management Tsinghua UniversityDocument53 pagesFinancial Management: Jia, Ning (贾宁) School of Economics and Management Tsinghua University王振權No ratings yet

- Outline: Investment AnalysisDocument15 pagesOutline: Investment AnalysisYe TunNo ratings yet

- Net Present Value: For New Project ManagersDocument70 pagesNet Present Value: For New Project ManagersMa8 Au8No ratings yet

- Net Present Value: For New Project ManagersDocument69 pagesNet Present Value: For New Project ManagersErlet Shaqe100% (1)

- Corporate Finance Lecture 2 - Capital Budgeting PDFDocument39 pagesCorporate Finance Lecture 2 - Capital Budgeting PDFSamuel HenriqueNo ratings yet

- MBA Finance and Financial Management: Bond, Equity and Firm ValuationsDocument52 pagesMBA Finance and Financial Management: Bond, Equity and Firm Valuationsconstruction omanNo ratings yet

- Present Value and Future Value: Finance: Time Value of MoneyDocument11 pagesPresent Value and Future Value: Finance: Time Value of MoneyTes DudteNo ratings yet

- Valuation FundamentalsDocument54 pagesValuation FundamentalsMaxNo ratings yet

- Valuation of Long Term Securities SolutionsDocument82 pagesValuation of Long Term Securities SolutionsRashed Hussain RatulNo ratings yet

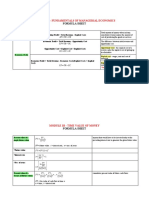

- CA5102 Q1 FORMULA SHEETDocument12 pagesCA5102 Q1 FORMULA SHEETDyra Mae OmegaNo ratings yet

- Entrepreneurial FinanceDocument112 pagesEntrepreneurial FinanceJohnny BravoNo ratings yet

- Sesion 11 Chapter 10 Dan 11Document60 pagesSesion 11 Chapter 10 Dan 11Gilang Akbar RizkyanNo ratings yet

- Wharton On Coursera: Introduction To Corporate Finance: DiscountingDocument7 pagesWharton On Coursera: Introduction To Corporate Finance: Discountingjhon doeNo ratings yet

- Lesson 5 - Investment FunctionDocument37 pagesLesson 5 - Investment FunctionJulie Ann Marie BernadezNo ratings yet

- Obtain FinancingDocument2 pagesObtain FinancingKang ChulNo ratings yet

- Linear Algebra and Machine LearningDocument3 pagesLinear Algebra and Machine LearningKang ChulNo ratings yet

- Intro to Linear Algebra for MLDocument3 pagesIntro to Linear Algebra for MLKang ChulNo ratings yet

- Linear RegressionDocument2 pagesLinear RegressionKang ChulNo ratings yet

- Learn Matrix FactorizationDocument3 pagesLearn Matrix FactorizationKang ChulNo ratings yet

- Num PyDocument3 pagesNum PyKang ChulNo ratings yet

- Principal Component AnalysisDocument3 pagesPrincipal Component AnalysisKang ChulNo ratings yet

- Numerical Linear AlgebraDocument3 pagesNumerical Linear AlgebraKang ChulNo ratings yet

- Financial Reporting ConventionsDocument2 pagesFinancial Reporting ConventionsKang ChulNo ratings yet

- Applications of Linear AlgebraDocument3 pagesApplications of Linear AlgebraKang ChulNo ratings yet

- Functions To Create ArraysDocument3 pagesFunctions To Create ArraysKang ChulNo ratings yet

- PURC 111 Midterm Reviewer GuideDocument2 pagesPURC 111 Midterm Reviewer GuideKang ChulNo ratings yet

- Examples of Linear Algebra in Machine LearningDocument3 pagesExamples of Linear Algebra in Machine LearningKang ChulNo ratings yet

- Before An Emergency: 1. Be PreparedDocument2 pagesBefore An Emergency: 1. Be PreparedKang ChulNo ratings yet

- Week 7 11 Reviewer CRWTDocument21 pagesWeek 7 11 Reviewer CRWTKang Chul100% (1)

- Merchandising SummaryDocument15 pagesMerchandising SummaryKang ChulNo ratings yet

- Midterm Lesson 1 4 StasDocument9 pagesMidterm Lesson 1 4 StasKang ChulNo ratings yet

- Life and Works of Jose Rizal: Prelim MidtermDocument23 pagesLife and Works of Jose Rizal: Prelim MidtermKang ChulNo ratings yet

- PC Chapter 4 6 ReviewerDocument19 pagesPC Chapter 4 6 ReviewerKang ChulNo ratings yet

- Week 7 11 Reviewer CRWTDocument21 pagesWeek 7 11 Reviewer CRWTKang Chul100% (1)

- MULTIPLE CHOICE. Choose The One Alternative That Best Completes The Statement or Answers The QuestionDocument19 pagesMULTIPLE CHOICE. Choose The One Alternative That Best Completes The Statement or Answers The QuestionKang ChulNo ratings yet

- Rizal Life and Works: Critical Analysis of The Rizal LawDocument7 pagesRizal Life and Works: Critical Analysis of The Rizal LawKang ChulNo ratings yet

- Quiz 1 & 2 and Prelim ReviewDocument15 pagesQuiz 1 & 2 and Prelim ReviewKang ChulNo ratings yet

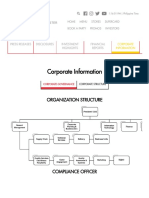

- Corporate Information: Organization StructureDocument11 pagesCorporate Information: Organization StructureKang ChulNo ratings yet

- Exam Prelim RizalDocument4 pagesExam Prelim RizalAnonymous yiqdcRgYdJ100% (3)

- Exam Prelim RizalDocument4 pagesExam Prelim RizalAnonymous yiqdcRgYdJ100% (3)

- The Contemporary WorldDocument175 pagesThe Contemporary WorldKang Chul100% (6)

- Chapter 1Document79 pagesChapter 1shafirann0% (1)

- Basic Concepts of Stocks and Bonds Part 1Document5 pagesBasic Concepts of Stocks and Bonds Part 1Rica Mae LopezNo ratings yet

- Difference Between Primary and Secondary Cost ElementDocument2 pagesDifference Between Primary and Secondary Cost Elementatsc68100% (1)

- Green Charcoal Manufactures (GCM) 03Document18 pagesGreen Charcoal Manufactures (GCM) 03Shubhangi GuptaNo ratings yet

- Balance Growth - FinalDocument8 pagesBalance Growth - FinalMahendra ChhetriNo ratings yet

- Acme Co.: Key Partners Key Activities Value Proposition Customer Relationship Customer SegmentsDocument5 pagesAcme Co.: Key Partners Key Activities Value Proposition Customer Relationship Customer SegmentsGladys NolascoNo ratings yet

- CMA-Stages of Development in OmanDocument17 pagesCMA-Stages of Development in OmanYenthizhai SellyNo ratings yet

- Risk Management in Banks DDocument63 pagesRisk Management in Banks DAryan KumarNo ratings yet

- Form PDF 166390820121221Document38 pagesForm PDF 166390820121221SethuramanNo ratings yet

- Investor RelationsDocument5 pagesInvestor RelationsDanielNo ratings yet

- Prime Brokerage: J.P. Morgan MarketsDocument2 pagesPrime Brokerage: J.P. Morgan MarketsMarco PoloNo ratings yet

- Derivagem - Version 1.52: "Options, Futures and Other Derivatives" 7/E "Fundamentals of Futures and Options Markets" 6/EDocument61 pagesDerivagem - Version 1.52: "Options, Futures and Other Derivatives" 7/E "Fundamentals of Futures and Options Markets" 6/Eمحمد احمد جیلانیNo ratings yet

- Retail Layout Management at TescoDocument9 pagesRetail Layout Management at TescoRowanAtkinson88% (8)

- APS L2M2 Extra Revision QUESTIONSDocument5 pagesAPS L2M2 Extra Revision QUESTIONSHayley DobsonNo ratings yet

- Pointers in Evaluating A Project StudyDocument23 pagesPointers in Evaluating A Project StudyMarjun_Cagalin_4856No ratings yet

- Mastering The Covered Call FinalDocument65 pagesMastering The Covered Call Finaljenna100% (1)

- Ib SMB202 4Document108 pagesIb SMB202 4RanjitNo ratings yet

- Pure Play Method of Divisional Beta (CA 2002)Document4 pagesPure Play Method of Divisional Beta (CA 2002)So LokNo ratings yet

- Kotler Keller Summary CompressDocument69 pagesKotler Keller Summary CompressApple DCLozanoNo ratings yet

- Digital Marketing Strategy in Automotive SectorDocument99 pagesDigital Marketing Strategy in Automotive SectorTrumpet MediaNo ratings yet

- Final MarketingDocument47 pagesFinal MarketingRalp ManglicmotNo ratings yet

- NMIMS Solved Dec 2021 Assignment Call 9025810064Document52 pagesNMIMS Solved Dec 2021 Assignment Call 9025810064Annmalai MBA Assignment Guidance0% (1)

- Case Study:Demand Forecasting of Rekha SoapDocument13 pagesCase Study:Demand Forecasting of Rekha Soapcadalal71% (7)

- Marketing Engineering of Durr StudyDocument3 pagesMarketing Engineering of Durr StudykumarNo ratings yet

- Chapter 6 Business Markets and Business Buyer Behavior: Principles of Marketing, 17e (Kotler/Armstrong)Document52 pagesChapter 6 Business Markets and Business Buyer Behavior: Principles of Marketing, 17e (Kotler/Armstrong)Tram Anh HoNo ratings yet

- DOMS Industries LTD - RHPDocument506 pagesDOMS Industries LTD - RHPGovernment ExamsNo ratings yet

- D-MART Analysis: REM Assignment 1 Group 09Document6 pagesD-MART Analysis: REM Assignment 1 Group 09Juhi SharmaBD21018No ratings yet

- Microeconomics: Mr. Nithin Kumar S Department of EconomicsDocument36 pagesMicroeconomics: Mr. Nithin Kumar S Department of EconomicsJellane SeletariaNo ratings yet

- Tutorial 9 & 10-Qs-2Document2 pagesTutorial 9 & 10-Qs-2YunesshwaaryNo ratings yet

- The Strategic Management Process True/False QuestionsDocument15 pagesThe Strategic Management Process True/False Questionsureka6arnicaNo ratings yet

- Tutorial 3 QuestionsDocument3 pagesTutorial 3 Questionsguan junyanNo ratings yet

- University of Berkshire Hathaway: 30 Years of Lessons Learned from Warren Buffett & Charlie Munger at the Annual Shareholders MeetingFrom EverandUniversity of Berkshire Hathaway: 30 Years of Lessons Learned from Warren Buffett & Charlie Munger at the Annual Shareholders MeetingRating: 4.5 out of 5 stars4.5/5 (97)

- The War Below: Lithium, Copper, and the Global Battle to Power Our LivesFrom EverandThe War Below: Lithium, Copper, and the Global Battle to Power Our LivesRating: 4.5 out of 5 stars4.5/5 (8)

- Narrative Economics: How Stories Go Viral and Drive Major Economic EventsFrom EverandNarrative Economics: How Stories Go Viral and Drive Major Economic EventsRating: 4.5 out of 5 stars4.5/5 (94)

- A History of the United States in Five Crashes: Stock Market Meltdowns That Defined a NationFrom EverandA History of the United States in Five Crashes: Stock Market Meltdowns That Defined a NationRating: 4 out of 5 stars4/5 (11)

- The Trillion-Dollar Conspiracy: How the New World Order, Man-Made Diseases, and Zombie Banks Are Destroying AmericaFrom EverandThe Trillion-Dollar Conspiracy: How the New World Order, Man-Made Diseases, and Zombie Banks Are Destroying AmericaNo ratings yet

- The New Elite: Inside the Minds of the Truly WealthyFrom EverandThe New Elite: Inside the Minds of the Truly WealthyRating: 4 out of 5 stars4/5 (10)

- The Infinite Machine: How an Army of Crypto-Hackers Is Building the Next Internet with EthereumFrom EverandThe Infinite Machine: How an Army of Crypto-Hackers Is Building the Next Internet with EthereumRating: 3 out of 5 stars3/5 (12)

- The Technology Trap: Capital, Labor, and Power in the Age of AutomationFrom EverandThe Technology Trap: Capital, Labor, and Power in the Age of AutomationRating: 4.5 out of 5 stars4.5/5 (46)

- Vulture Capitalism: Corporate Crimes, Backdoor Bailouts, and the Death of FreedomFrom EverandVulture Capitalism: Corporate Crimes, Backdoor Bailouts, and the Death of FreedomNo ratings yet

- Chip War: The Quest to Dominate the World's Most Critical TechnologyFrom EverandChip War: The Quest to Dominate the World's Most Critical TechnologyRating: 4.5 out of 5 stars4.5/5 (227)

- Second Class: How the Elites Betrayed America's Working Men and WomenFrom EverandSecond Class: How the Elites Betrayed America's Working Men and WomenNo ratings yet

- Doughnut Economics: Seven Ways to Think Like a 21st-Century EconomistFrom EverandDoughnut Economics: Seven Ways to Think Like a 21st-Century EconomistRating: 4.5 out of 5 stars4.5/5 (37)

- Principles for Dealing with the Changing World Order: Why Nations Succeed or FailFrom EverandPrinciples for Dealing with the Changing World Order: Why Nations Succeed or FailRating: 4.5 out of 5 stars4.5/5 (237)

- The Genius of Israel: The Surprising Resilience of a Divided Nation in a Turbulent WorldFrom EverandThe Genius of Israel: The Surprising Resilience of a Divided Nation in a Turbulent WorldRating: 4 out of 5 stars4/5 (17)

- The Myth of the Rational Market: A History of Risk, Reward, and Delusion on Wall StreetFrom EverandThe Myth of the Rational Market: A History of Risk, Reward, and Delusion on Wall StreetNo ratings yet

- Poor Economics: A Radical Rethinking of the Way to Fight Global PovertyFrom EverandPoor Economics: A Radical Rethinking of the Way to Fight Global PovertyRating: 4.5 out of 5 stars4.5/5 (263)

- Look Again: The Power of Noticing What Was Always ThereFrom EverandLook Again: The Power of Noticing What Was Always ThereRating: 5 out of 5 stars5/5 (3)

- Nudge: The Final Edition: Improving Decisions About Money, Health, And The EnvironmentFrom EverandNudge: The Final Edition: Improving Decisions About Money, Health, And The EnvironmentRating: 4.5 out of 5 stars4.5/5 (92)

- The Finance Curse: How Global Finance Is Making Us All PoorerFrom EverandThe Finance Curse: How Global Finance Is Making Us All PoorerRating: 4.5 out of 5 stars4.5/5 (18)