You might also like

- Week 6 Exercise SolutionsDocument6 pagesWeek 6 Exercise SolutionsrahmawNo ratings yet

- Eyedropper Clinic: Accounting Equation: Current Assets Non Current AssetsDocument5 pagesEyedropper Clinic: Accounting Equation: Current Assets Non Current AssetsSofía MargaritaNo ratings yet

- Cash FlowDocument6 pagesCash Flowsilvia indahsariNo ratings yet

- Explanation: 1. No, Production and Sale of The Racing Bikes Should Not Be Discontinued 2Document1 pageExplanation: 1. No, Production and Sale of The Racing Bikes Should Not Be Discontinued 2Eevan SalazarNo ratings yet

- MAS Final Preboard Solutions B93Document5 pagesMAS Final Preboard Solutions B93813 cafeNo ratings yet

- Sesi 11 & 12 SharedDocument28 pagesSesi 11 & 12 SharedDian Permata SariNo ratings yet

- DocxDocument5 pagesDocxainun nisaNo ratings yet

- Tugas Kelompok 11 November - Cicilia Cindy (20-026) - Siska Muliatri (20-066)Document22 pagesTugas Kelompok 11 November - Cicilia Cindy (20-026) - Siska Muliatri (20-066)Cicilia Cindy100% (1)

- Tugas Kelompok 3 Intermediate Accounting IDocument9 pagesTugas Kelompok 3 Intermediate Accounting IEvelyn Purnama SariNo ratings yet

- FaldoDocument10 pagesFaldodinda ardiyaniNo ratings yet

- Model Ans - Sas - I April 2018Document68 pagesModel Ans - Sas - I April 2018প্রীতম সেনNo ratings yet

- Book Solution To 3.6Document5 pagesBook Solution To 3.6Tanmay SharmaNo ratings yet

- Final Exam - FA PDFDocument7 pagesFinal Exam - FA PDFNga NguyễnNo ratings yet

- Ch9 ExercisesDocument15 pagesCh9 ExercisesMarshanda BerliantiNo ratings yet

- Sol. Man. - Chapter 8 - Inventory Estimation - Ia Part 1aDocument5 pagesSol. Man. - Chapter 8 - Inventory Estimation - Ia Part 1aYamateNo ratings yet

- Intacc Cash Flow SolutionDocument3 pagesIntacc Cash Flow SolutionMila MercadoNo ratings yet

- Sol. Man. - Chapter 8 - Inventory Estimation - Ia Part 1aDocument6 pagesSol. Man. - Chapter 8 - Inventory Estimation - Ia Part 1aRezzan Joy Camara MejiaNo ratings yet

- ForumDocument5 pagesForumMariana Hb0% (1)

- Exchange of MachineDocument2 pagesExchange of MachineShoebNo ratings yet

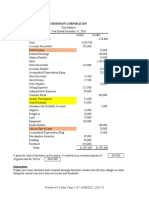

- Thompson Corporation: InstructionsDocument7 pagesThompson Corporation: InstructionsrahmawNo ratings yet

- Quiz #2 - Set C - Solutions To PSDocument2 pagesQuiz #2 - Set C - Solutions To PSPia DigaNo ratings yet

- 2E Intermediate (Sat - 16-3-2024) - Final Ch.2 (A)Document20 pages2E Intermediate (Sat - 16-3-2024) - Final Ch.2 (A)ahmedNo ratings yet

- PPE SolutionDocument6 pagesPPE SolutionHuỳnh Thị Thu BaNo ratings yet

- CA TM 2nd Edition Chapter 22 EngDocument38 pagesCA TM 2nd Edition Chapter 22 EngIp NicoleNo ratings yet

- Cost of Goods Available For SaleDocument4 pagesCost of Goods Available For SaleColeen RamosNo ratings yet

- Chapter 15 Akun Keuangan TugasDocument3 pagesChapter 15 Akun Keuangan Tugassegeri kecNo ratings yet

- P12-1 Dan P 12-5 - Ak KeuanganDocument2 pagesP12-1 Dan P 12-5 - Ak KeuanganNenna SadukNo ratings yet

- Bsa Midterm Non Graded Exercises Worksheet and Financial Statements Preparation Answer KeyDocument7 pagesBsa Midterm Non Graded Exercises Worksheet and Financial Statements Preparation Answer KeyGarp BarrocaNo ratings yet

- Chapter 1 - Question 1Document4 pagesChapter 1 - Question 1Sophie ChopraNo ratings yet

- Absorption and Marginal Costing TemplateDocument13 pagesAbsorption and Marginal Costing TemplateGeorge PNo ratings yet

- BAFACR16 04 Answer Key To Post TestsDocument5 pagesBAFACR16 04 Answer Key To Post TestsThats BellaNo ratings yet

- Financier AsDocument14 pagesFinancier AsImaneNo ratings yet

- Financial Accounting - Tugas 2 - 28 Agustus 2019Document3 pagesFinancial Accounting - Tugas 2 - 28 Agustus 2019AlfiyanNo ratings yet

- Deirdre BarlowDocument4 pagesDeirdre BarlowlornaNo ratings yet

- Correct Amount of Inventory 677,500Document8 pagesCorrect Amount of Inventory 677,500Maria Kathreena Andrea AdevaNo ratings yet

- Acinac Problem 5Document5 pagesAcinac Problem 5Angelo Gian CoNo ratings yet

- ACCT - Break Even Buy or Sell Budgeting Operation AnalysisDocument19 pagesACCT - Break Even Buy or Sell Budgeting Operation AnalysisTavakoli MehranNo ratings yet

- Practical Questions (Sandeep Garg 2018-19)Document10 pagesPractical Questions (Sandeep Garg 2018-19)Kanishk SinglaNo ratings yet

- FDNACCT - Mock Exam - Answer Key - 3 - Fill in The Blank Problems PDFDocument5 pagesFDNACCT - Mock Exam - Answer Key - 3 - Fill in The Blank Problems PDFJames de LeonNo ratings yet

- ECO Depreciation ChargesDocument2 pagesECO Depreciation ChargesOliver SlovenskoNo ratings yet

- Acccob3 HW9Document33 pagesAcccob3 HW9Reshawn Kimi SantosNo ratings yet

- Vertical and Horizontal Analysis For Balance Sheet - 12-1Document8 pagesVertical and Horizontal Analysis For Balance Sheet - 12-1Krissya Masis MoraNo ratings yet

- IA3 Chapter 14 Problem 31Document3 pagesIA3 Chapter 14 Problem 31Bea TumulakNo ratings yet

- Mas (Solutions)Document6 pagesMas (Solutions)Mark Anthony Casupang100% (1)

- Akuntansi - Week 3Document9 pagesAkuntansi - Week 3joddy lintar002No ratings yet

- Comprehensive IncomeDocument2 pagesComprehensive IncomeLeomar CabandayNo ratings yet

- Total Comprehensive Income For The Year 139,400.00Document2 pagesTotal Comprehensive Income For The Year 139,400.00Siti rahmahNo ratings yet

- Chapter 9 Exercises: Exercise 9 1Document8 pagesChapter 9 Exercises: Exercise 9 1karenmae intangNo ratings yet

- Solution Case 1Document2 pagesSolution Case 1Ario LintangNo ratings yet

- Financial ManagementDocument9 pagesFinancial ManagementAtif SiddiquiNo ratings yet

- Financial Accounting - Tugas 4 - 23 Oktober 2019Document3 pagesFinancial Accounting - Tugas 4 - 23 Oktober 2019AlfiyanNo ratings yet

- Installment Sales Consignment Sales Construction ContractsDocument4 pagesInstallment Sales Consignment Sales Construction ContractsShaene GalloraNo ratings yet

- ACCT-312: Class Exercises (Chapter 2) : AnnualDocument35 pagesACCT-312: Class Exercises (Chapter 2) : AnnualAmir ContrerasNo ratings yet

- Hardhat Case - Rajesh Kumar NayakDocument12 pagesHardhat Case - Rajesh Kumar NayakSandeep RawatNo ratings yet

- ExercisesDocument3 pagesExercisesMaitaNo ratings yet

- MTP 12 16 Answers 1696782053Document14 pagesMTP 12 16 Answers 1696782053harshallahotNo ratings yet

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- Contoh Soal AkuntansiDocument4 pagesContoh Soal AkuntansiRicky ChenNo ratings yet

- Accounting NoteDocument8 pagesAccounting NoteRicky ChenNo ratings yet

- AssignmentDocument3 pagesAssignmentRicky ChenNo ratings yet

- Managerial AccountingDocument2 pagesManagerial AccountingRicky ChenNo ratings yet

- Introduction To Database Mid-Term Answer SheetDocument10 pagesIntroduction To Database Mid-Term Answer SheetRicky ChenNo ratings yet

- Assignment 1 - Central Tendency and Standard DeviationDocument5 pagesAssignment 1 - Central Tendency and Standard DeviationRicky ChenNo ratings yet

- Ricky Chen LA 16 - Accounting and Information SystemDocument2 pagesRicky Chen LA 16 - Accounting and Information SystemRicky ChenNo ratings yet

- HRD - 1.1.0.0 RND - 1.2.0.0 Production - 1.3.0.0 Marketing - 1.4.0.0 Purchasing-1.5.0.0 Accounting - 1.6.0.0Document1 pageHRD - 1.1.0.0 RND - 1.2.0.0 Production - 1.3.0.0 Marketing - 1.4.0.0 Purchasing-1.5.0.0 Accounting - 1.6.0.0Ricky ChenNo ratings yet

- UI-UX Forum AssignmentDocument2 pagesUI-UX Forum AssignmentRicky ChenNo ratings yet

- Pi 4400000700Document1 pagePi 4400000700KrishnaNo ratings yet

- Chapter 1 QuizDocument9 pagesChapter 1 QuizRyan SalipsipNo ratings yet

- Piddig District - Piddig, Ilocos Norte - Employee No. 4117269Document2 pagesPiddig District - Piddig, Ilocos Norte - Employee No. 4117269DanielLarryAquinoNo ratings yet

- E3-5 Hwang Ltd. Has The Following Balances in Selected Accounts On December 31, 2017.accounts Receivable NT$ - 0Document3 pagesE3-5 Hwang Ltd. Has The Following Balances in Selected Accounts On December 31, 2017.accounts Receivable NT$ - 0arjun ladoNo ratings yet

- Wiltw - 2020 - 04 - 02 - E02 - Is - Deflation - Coming - or - Is - MMT - and - Hyperinflation - Coming - Are - y 2Document18 pagesWiltw - 2020 - 04 - 02 - E02 - Is - Deflation - Coming - or - Is - MMT - and - Hyperinflation - Coming - Are - y 2Jonathan NgNo ratings yet

- Road Maintenance in Nepal - Most Neglected Aspect - The Himalayan TimesDocument3 pagesRoad Maintenance in Nepal - Most Neglected Aspect - The Himalayan TimesShambhu SahNo ratings yet

- TYO To CAI, 711 - 718Document1 pageTYO To CAI, 711 - 718Faye OlaezNo ratings yet

- UntitledDocument12 pagesUntitledSHER LYN LOWNo ratings yet

- Banking and Insurance Law NotesDocument164 pagesBanking and Insurance Law NotesFaisal KhanNo ratings yet

- Online 645Document2 pagesOnline 645Aishwarya SenthilNo ratings yet

- Vault Fund Venture Studio Structure AnalysisDocument6 pagesVault Fund Venture Studio Structure AnalysisKleber Bastos Gomes JuniorNo ratings yet

- Almi-Lkt 2008Document48 pagesAlmi-Lkt 2008rizqinstNo ratings yet

- Construction PricesDocument5 pagesConstruction PricesGueanne ConsolacionNo ratings yet

- Urban and Regional Planning Unit 1: Why Does One Need To Study It ?Document29 pagesUrban and Regional Planning Unit 1: Why Does One Need To Study It ?Pranav PadmavasanNo ratings yet

- Class 10th Development BoardPrep SolutionDocument10 pagesClass 10th Development BoardPrep SolutionABISHUA HANOK LALNo ratings yet

- Insights Mind Maps: Golden Quadrilateral ProjectDocument2 pagesInsights Mind Maps: Golden Quadrilateral Projectashish kumarNo ratings yet

- A PDFDocument105 pagesA PDFDandolph TanNo ratings yet

- 1..loading Unloading and Erection of Steel StructuresDocument2 pages1..loading Unloading and Erection of Steel StructuresFrancis VinojNo ratings yet

- W01 - Managers, Profits, and Markets-FJODocument36 pagesW01 - Managers, Profits, and Markets-FJOALPAMA SALSABILANo ratings yet

- Participants AqabaConf 2019Document16 pagesParticipants AqabaConf 2019Mohammad AbdullahNo ratings yet

- Business PlanDocument5 pagesBusiness Planetio basseyNo ratings yet

- Geopolitics Chapter 2Document25 pagesGeopolitics Chapter 2Yassmine DNo ratings yet

- Auto Rexel Manual-Rexel-Smartech-300x-2103250eusDocument22 pagesAuto Rexel Manual-Rexel-Smartech-300x-2103250euscarmenNo ratings yet

- Goods Receipt Valuation For Purchase Orders When Involving Foreign CurrenciesDocument9 pagesGoods Receipt Valuation For Purchase Orders When Involving Foreign CurrenciesBalanathan VirupasanNo ratings yet

- SunTrust StatDocument1 pageSunTrust StatIrakli IrakliNo ratings yet

- Module 1 Topic 1Document17 pagesModule 1 Topic 1Shreenidhi JoshiNo ratings yet

- 06 Rupel, Dimitrij - Slovenia in Post Modern EuropeDocument10 pages06 Rupel, Dimitrij - Slovenia in Post Modern EuropecetinjeNo ratings yet

- MoneysupplyDocument27 pagesMoneysupplySufian HimelNo ratings yet

- Global Capital Confidence Barometer: Colombian Executives Press Pause On M&A Amid UncertaintyDocument2 pagesGlobal Capital Confidence Barometer: Colombian Executives Press Pause On M&A Amid UncertaintyMaritza CardenasNo ratings yet

- Accounts TR 10 MDTDocument4 pagesAccounts TR 10 MDTOluwatobi AkindeNo ratings yet