You might also like

- Management Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageFrom EverandManagement Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageRating: 5 out of 5 stars5/5 (1)

- Transfer PricingDocument20 pagesTransfer Pricingabhi2244inNo ratings yet

- Transfer Pricing: Mcgraw-Hill/IrwinDocument17 pagesTransfer Pricing: Mcgraw-Hill/Irwinmkkaran90No ratings yet

- Unit5 Finance Student Presantation 2324Document57 pagesUnit5 Finance Student Presantation 2324BebeNo ratings yet

- Study Unit 5.1Document26 pagesStudy Unit 5.1Valerie Verity MarondedzeNo ratings yet

- Ch12 Transfer Pricing P12-15, P12-17, P12-24, P12-32, P12-35Document8 pagesCh12 Transfer Pricing P12-15, P12-17, P12-24, P12-32, P12-35kidflash1234No ratings yet

- Gross Profit Variance AnalysisDocument3 pagesGross Profit Variance AnalysisI am JacobNo ratings yet

- PRICINGDocument25 pagesPRICINGJulianne Lopez EusebioNo ratings yet

- Marginal Costing&backward CostingDocument7 pagesMarginal Costing&backward CostingSauumye ChauhanNo ratings yet

- Pricing Decision and Trasfer (Week 7)Document36 pagesPricing Decision and Trasfer (Week 7)Winston 葉永隆 DiepNo ratings yet

- Contribution Analysis and Marginal CostingDocument15 pagesContribution Analysis and Marginal CostingADITI BISWASNo ratings yet

- Overhead and Other Variances PDFDocument26 pagesOverhead and Other Variances PDFAnuruddha RajasuriyaNo ratings yet

- Accounting & Control: Cost ManagementDocument38 pagesAccounting & Control: Cost ManagementMosha MochaNo ratings yet

- 3 - BREAK EVEN ANALYSIS - UploadDocument5 pages3 - BREAK EVEN ANALYSIS - Uploadniaz kilamNo ratings yet

- CVP Analysis Notes 1Document4 pagesCVP Analysis Notes 1Potie RhymeszNo ratings yet

- Contribution Price. This Contribution Approach To Pricing Is Most Appropriate When: (1) There Is ADocument7 pagesContribution Price. This Contribution Approach To Pricing Is Most Appropriate When: (1) There Is AEVELYN ROSE MOGAONo ratings yet

- Transfer PricingDocument41 pagesTransfer PricingJudy Ann AcruzNo ratings yet

- Cost and Management Accounting VaaniDocument13 pagesCost and Management Accounting Vaanidhawalbaria7No ratings yet

- CVP Analysis: PG D M2 0 21-23 RelevantreadingsDocument21 pagesCVP Analysis: PG D M2 0 21-23 RelevantreadingsAthi SivaNo ratings yet

- Ch19 Guan Hansen MowenDocument38 pagesCh19 Guan Hansen MowenratuhsNo ratings yet

- COSTMAN - MidtermDocument23 pagesCOSTMAN - MidtermHoney MuliNo ratings yet

- CH 17 Rel Cost PotpourriDocument4 pagesCH 17 Rel Cost PotpourrialiNo ratings yet

- Presented By: Lutfi Ms Ananthakrishnan Malavika Sreekumar Manilal Kasera Mitesh KumarDocument14 pagesPresented By: Lutfi Ms Ananthakrishnan Malavika Sreekumar Manilal Kasera Mitesh KumarManilal kaseraNo ratings yet

- Contribution Margin Definition - InvestopediaDocument6 pagesContribution Margin Definition - InvestopediaBob KaneNo ratings yet

- Chapter 2 CVP AnalysisDocument56 pagesChapter 2 CVP AnalysisnathalieroseNo ratings yet

- Udah Bener'Document4 pagesUdah Bener'Shafa AzahraNo ratings yet

- Transfer Pricing - Ch7 - SDocument44 pagesTransfer Pricing - Ch7 - SLok Fung KanNo ratings yet

- Ch19 - Guan CM - AISEDocument38 pagesCh19 - Guan CM - AISELydia WulandariNo ratings yet

- ACCT3104 - Lecture 5 - Lecture Exercise 2 & Solution RFDocument7 pagesACCT3104 - Lecture 5 - Lecture Exercise 2 & Solution RFnikkiNo ratings yet

- Final CH 5Document5 pagesFinal CH 5worknehNo ratings yet

- 03-04-2012Document62 pages03-04-2012Adeel AliNo ratings yet

- Financial Aspects of Marketing ManagementDocument10 pagesFinancial Aspects of Marketing Managementraza73735No ratings yet

- Incremental AnalysisDocument82 pagesIncremental AnalysisMicha Silvestre100% (1)

- General Pricing Approaches Final (By Bilal)Document19 pagesGeneral Pricing Approaches Final (By Bilal)Bilal100% (10)

- Lesson 2: Relevant Costs For Decision MakingDocument41 pagesLesson 2: Relevant Costs For Decision MakingChuah Chong AnnNo ratings yet

- Decision MakingDocument33 pagesDecision Makingali100% (1)

- Transfer Pricing PDFDocument10 pagesTransfer Pricing PDFFabrienne Kate Eugenio LiberatoNo ratings yet

- Unit Four: Measuring Mix and Yield VariancesDocument6 pagesUnit Four: Measuring Mix and Yield VariancesTammy 27100% (1)

- Chapter 12 TRF PricingDocument30 pagesChapter 12 TRF Pricingleeroybradley44No ratings yet

- A Management Control System Is A Means of Gathering and Using InformationDocument41 pagesA Management Control System Is A Means of Gathering and Using InformationVipul JainNo ratings yet

- Variance Analysis: Study Questions and Answers Are On Page 4 and Pages 5-11Document21 pagesVariance Analysis: Study Questions and Answers Are On Page 4 and Pages 5-11Andy OcegueraNo ratings yet

- Chapter 4 ACCA F2Document7 pagesChapter 4 ACCA F2siksha100% (1)

- Chapter 3Document60 pagesChapter 3Adam AbdullahiNo ratings yet

- Espinosa&Gabijan - Export Pricing CostingDocument17 pagesEspinosa&Gabijan - Export Pricing CostingDulce Amor Margallo ValdescoNo ratings yet

- Breakeven AnalysisDocument19 pagesBreakeven AnalysisJitenderKumarNo ratings yet

- Activity Based CostingDocument28 pagesActivity Based CostingApril TorresNo ratings yet

- Tutorial Chapter 12 Cost Behaviour and Measurement of CostsDocument54 pagesTutorial Chapter 12 Cost Behaviour and Measurement of CostsNaKib Nahri0% (1)

- Decision Making 36 Practice Questions SolutionsDocument33 pagesDecision Making 36 Practice Questions SolutionsVias TikaNo ratings yet

- Absorption and Variable CostingDocument12 pagesAbsorption and Variable CostingMatrika ThapaNo ratings yet

- Test Bank For Managerial Accounting 17th Edition Ray Garrison Eric Noreen Peter BrewerDocument36 pagesTest Bank For Managerial Accounting 17th Edition Ray Garrison Eric Noreen Peter Brewerstarread.effablelkwfv2100% (46)

- Summary 2Document9 pagesSummary 2Eman El-kholyNo ratings yet

- Relevant Costing: ExampleDocument7 pagesRelevant Costing: Examplebakhtawar soniaNo ratings yet

- Transfer PricingDocument27 pagesTransfer PricingAnshuNo ratings yet

- Cost Managementt AccountingDocument7 pagesCost Managementt AccountingMohan KottuNo ratings yet

- Cost Analysis PPT Bec Bagalkot MbaDocument8 pagesCost Analysis PPT Bec Bagalkot MbaBabasab Patil (Karrisatte)100% (1)

- CVP New + LastDocument19 pagesCVP New + LastDawit AmahaNo ratings yet

- Chap 011 ADocument24 pagesChap 011 AHawatiNo ratings yet

- Decentralization and PricingDocument38 pagesDecentralization and PricingFidelina CastroNo ratings yet

- RWD 08 Transfer PriceDocument28 pagesRWD 08 Transfer Pricehamba allahNo ratings yet

- 16 Ais 072Document7 pages16 Ais 072MD Hafizul Islam HafizNo ratings yet

- DeeganFAT3e PPT Ch02-EdDocument33 pagesDeeganFAT3e PPT Ch02-EdElok HendionoNo ratings yet

- 16 Ais 050Document8 pages16 Ais 050MD Hafizul Islam HafizNo ratings yet

- Id 16 Ais 020Document10 pagesId 16 Ais 020MD Hafizul Islam HafizNo ratings yet

- Id 16 Ais 025Document13 pagesId 16 Ais 025MD Hafizul Islam HafizNo ratings yet

- 16 Ais 072Document7 pages16 Ais 072MD Hafizul Islam HafizNo ratings yet

- 1st MidtermDocument9 pages1st MidtermMD Hafizul Islam HafizNo ratings yet

- Exam 02Document1 pageExam 02MD Hafizul Islam HafizNo ratings yet

- 16 Ais 010Document13 pages16 Ais 010MD Hafizul Islam HafizNo ratings yet

- Ariful Islam Rasel Internship (1) (1) .EditedDocument58 pagesAriful Islam Rasel Internship (1) (1) .EditedMD Hafizul Islam HafizNo ratings yet

- Analysis Annual Report: Submitted byDocument18 pagesAnalysis Annual Report: Submitted byMD Hafizul Islam HafizNo ratings yet

- Risk and ReturnDocument11 pagesRisk and ReturnMD Hafizul Islam HafizNo ratings yet

- Group 01 Report UpdateDocument24 pagesGroup 01 Report UpdateMD Hafizul Islam HafizNo ratings yet

- 2nd MidtermDocument3 pages2nd MidtermMD Hafizul Islam HafizNo ratings yet

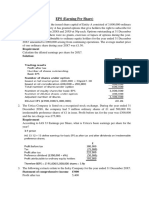

- EPS (Earning Per Share) : Requirement SolutionDocument4 pagesEPS (Earning Per Share) : Requirement SolutionMD Hafizul Islam HafizNo ratings yet

- CamScanner 03-03-2022 20.50Document7 pagesCamScanner 03-03-2022 20.50MD Hafizul Islam HafizNo ratings yet

- CamScanner 03-03-2022 20.55Document35 pagesCamScanner 03-03-2022 20.55MD Hafizul Islam HafizNo ratings yet

- Accounting Treatment (Ias - 21) Recognition and Initial MeasurementDocument8 pagesAccounting Treatment (Ias - 21) Recognition and Initial MeasurementMD Hafizul Islam HafizNo ratings yet

- Systems Development Life Cycle (SDLC) - A Five-Step Process Used To Design and Implement A New SystemDocument4 pagesSystems Development Life Cycle (SDLC) - A Five-Step Process Used To Design and Implement A New SystemMD Hafizul Islam HafizNo ratings yet

- Impact of Price Hike Over Lower Middle Class: A Case Study On Barishal Metropolitan Area. Literature Review AbstractDocument1 pageImpact of Price Hike Over Lower Middle Class: A Case Study On Barishal Metropolitan Area. Literature Review AbstractMD Hafizul Islam HafizNo ratings yet

- Ias 24Document2 pagesIas 24MD Hafizul Islam HafizNo ratings yet

- IAS 21: The Effects of Changes in Foreign Exchange RatesDocument5 pagesIAS 21: The Effects of Changes in Foreign Exchange RatesMD Hafizul Islam HafizNo ratings yet

- Cash Flow Statement IAS 7Document3 pagesCash Flow Statement IAS 7MD Hafizul Islam HafizNo ratings yet

- Memory Test On Article & CorrectionDocument2 pagesMemory Test On Article & CorrectionMD Hafizul Islam HafizNo ratings yet

- IFRS 8 Operating Segment & IFRS 1 PDFDocument4 pagesIFRS 8 Operating Segment & IFRS 1 PDFMD Hafizul Islam HafizNo ratings yet

- Theory PDFDocument7 pagesTheory PDFMD Hafizul Islam HafizNo ratings yet

- PROBIR MathDocument11 pagesPROBIR MathMD Hafizul Islam HafizNo ratings yet

- AIS 5103 Course OutlineDocument1 pageAIS 5103 Course OutlineMD Hafizul Islam HafizNo ratings yet

- All Math pdf2Document6 pagesAll Math pdf2MD Hafizul Islam HafizNo ratings yet

- Final InShaAllahDocument10 pagesFinal InShaAllahMD Hafizul Islam HafizNo ratings yet

- ECON102 Specimen Exam PaperDocument11 pagesECON102 Specimen Exam PaperEduardoNo ratings yet

- SwiftPay FAQsDocument2 pagesSwiftPay FAQsKiran SheikhNo ratings yet

- All Alerts For 17 Jan - ChartinkDocument17 pagesAll Alerts For 17 Jan - Chartinkkashinath09No ratings yet

- IAD Uc1-AtsDocument5 pagesIAD Uc1-AtsEdna Alliones ValienteNo ratings yet

- Goods and Services Tax - GSTR-2BDocument48 pagesGoods and Services Tax - GSTR-2BR.Roshini RNo ratings yet

- Rte BXM4C Timetable 011011Document2 pagesRte BXM4C Timetable 011011Teresa ChongNo ratings yet

- Robert Giffen and The Irish Potato - 1984Document6 pagesRobert Giffen and The Irish Potato - 1984ahem ahemNo ratings yet

- Capacity and Constraint ManagementDocument30 pagesCapacity and Constraint ManagementtayerNo ratings yet

- Econs Notes AusmatDocument49 pagesEcons Notes Ausmatashleymae19No ratings yet

- Merchant Merchant Mobile S No Shop Name Shop Address City 83 Abhijeet Saha 99065620Document167 pagesMerchant Merchant Mobile S No Shop Name Shop Address City 83 Abhijeet Saha 99065620Delta PayNo ratings yet

- BKI MM Aug2022 ReportDocument25 pagesBKI MM Aug2022 ReportZerohedgeNo ratings yet

- International Business Enviornment: Case Study of MexicoDocument36 pagesInternational Business Enviornment: Case Study of MexicoKartikNo ratings yet

- Saving Money and BudgetingDocument6 pagesSaving Money and BudgetingretrolaNo ratings yet

- Topic 8 - Location DecisionDocument43 pagesTopic 8 - Location DecisionSiang ElsonNo ratings yet

- The Great Depression NotesDocument3 pagesThe Great Depression NotesAthena GuzmanNo ratings yet

- International Economics Problem SetDocument5 pagesInternational Economics Problem SetBucha GetachewNo ratings yet

- Pre Feasibility Report: Essar Steel India LimitedDocument54 pagesPre Feasibility Report: Essar Steel India LimitedSubrato GhoshNo ratings yet

- Nestlé Internationalization: Introduction To International and Global MarketingDocument9 pagesNestlé Internationalization: Introduction To International and Global MarketingQytyku BoranaNo ratings yet

- Risk Management in Future ContractsDocument4 pagesRisk Management in Future Contractsareesakhtar100% (1)

- En Custom Form 22Document1 pageEn Custom Form 22Tamil Arasu100% (1)

- Advantages and Disadvantages of Cardinal ApproachDocument2 pagesAdvantages and Disadvantages of Cardinal ApproachGift MoyoNo ratings yet

- Budget Brief 2020 Final - SomalilandDocument16 pagesBudget Brief 2020 Final - SomalilandMohamed AliNo ratings yet

- International Financial Management 9th Edition Jeff Madura Test BankDocument15 pagesInternational Financial Management 9th Edition Jeff Madura Test Bankclitusarielbeehax100% (30)

- MFR203 FAR-4 AssignmentDocument5 pagesMFR203 FAR-4 Assignmentgillian soonNo ratings yet

- Financial Inclusion - RBI - S InitiativesDocument12 pagesFinancial Inclusion - RBI - S Initiativessahil_saini298No ratings yet

- 01 Introduction To MacroeconomicsDocument8 pages01 Introduction To MacroeconomicsRaunak RayNo ratings yet

- Evo EcoDocument31 pagesEvo EcoolyNo ratings yet

- The Fiscal Impact and Policy Response To Covid 19 in VietnamDocument19 pagesThe Fiscal Impact and Policy Response To Covid 19 in VietnamNGHIÊM NGUYỄN MINHNo ratings yet

- The Case For Small and Medium Enterprises in Afghanistan PDFDocument34 pagesThe Case For Small and Medium Enterprises in Afghanistan PDFNomanNo ratings yet

- Cambridge International AS & A Level: HISTORY 9489/12Document8 pagesCambridge International AS & A Level: HISTORY 9489/12Eshaal Hamza MalikNo ratings yet