0% found this document useful (0 votes)

763 views13 pagesTax Compliance and Allowances in Malaysia

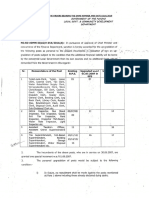

The four main criteria of plant and machinery for the purposes of claiming capital allowances are:

1. Used for the purposes of a business.

2. Used for the production of income from a source.

3. Used for the purposes of a business of a person other than an individual.

4. Not excluded items such as motor vehicles, buildings, structures, etc.

(a)(ii) Which of the expenditure incurred by I-Tiles Sdn Bhd qualify for capital allowances and which do not? Provide reasons.

Uploaded by

Choo LeeCopyright

© © All Rights Reserved

We take content rights seriously. If you suspect this is your content, claim it here.

0% found this document useful (0 votes)

763 views13 pagesTax Compliance and Allowances in Malaysia

The four main criteria of plant and machinery for the purposes of claiming capital allowances are:

1. Used for the purposes of a business.

2. Used for the production of income from a source.

3. Used for the purposes of a business of a person other than an individual.

4. Not excluded items such as motor vehicles, buildings, structures, etc.

(a)(ii) Which of the expenditure incurred by I-Tiles Sdn Bhd qualify for capital allowances and which do not? Provide reasons.

Uploaded by

Choo LeeCopyright

© © All Rights Reserved

We take content rights seriously. If you suspect this is your content, claim it here.