You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- SOAP PLANT Project Report CompleteDocument8 pagesSOAP PLANT Project Report CompleteER. INDERAMAR SINGH52% (25)

- Spare Parts Manual M1T - 298 File-IsharatDocument97 pagesSpare Parts Manual M1T - 298 File-IsharatSharat ChutiaNo ratings yet

- Enrichment Learning Activity: Name: Date: Year and Section: Instructor: Module #: TopicDocument3 pagesEnrichment Learning Activity: Name: Date: Year and Section: Instructor: Module #: TopicImthe OneNo ratings yet

- 04 Homework (Ramirez)Document4 pages04 Homework (Ramirez)Imthe OneNo ratings yet

- Enrichment Learning Activity: Name: Date: Year and Section: Instructor: Module #: TopicDocument6 pagesEnrichment Learning Activity: Name: Date: Year and Section: Instructor: Module #: TopicImthe OneNo ratings yet

- Condominium Subcontractor CDC Holdings Corporation Ramirez CondominiumDocument3 pagesCondominium Subcontractor CDC Holdings Corporation Ramirez CondominiumImthe OneNo ratings yet

- Enrichment Learning Activity: Name: Date: Year and Section: Instructor: Module #: TopicDocument2 pagesEnrichment Learning Activity: Name: Date: Year and Section: Instructor: Module #: TopicImthe OneNo ratings yet

- Enrichment Learning Activity: Name: Date: Year and Section: Instructor: Module #: TopicDocument3 pagesEnrichment Learning Activity: Name: Date: Year and Section: Instructor: Module #: TopicImthe OneNo ratings yet

- Enrichment Learning Activity: Name: Date: Year and Section: Instructor: Module #: TopicDocument5 pagesEnrichment Learning Activity: Name: Date: Year and Section: Instructor: Module #: TopicImthe OneNo ratings yet

- Navotas Polytechnic College Bs HRM ACTIVITY 1.6 (20pts)Document2 pagesNavotas Polytechnic College Bs HRM ACTIVITY 1.6 (20pts)Imthe OneNo ratings yet

- Enrichment Learning Activity: Name: Date: Year and Section: Instructor: Module #: TopicDocument2 pagesEnrichment Learning Activity: Name: Date: Year and Section: Instructor: Module #: TopicImthe OneNo ratings yet

- Enrichment Learning Activity: Name: Date: Year and Section: Instructor: Module #: TopicDocument3 pagesEnrichment Learning Activity: Name: Date: Year and Section: Instructor: Module #: TopicImthe OneNo ratings yet

- John Carlo C. Tolentino March 3, 2022 Bsma-3A Mr. Jefferson Cruz 3Document5 pagesJohn Carlo C. Tolentino March 3, 2022 Bsma-3A Mr. Jefferson Cruz 3Imthe OneNo ratings yet

- A Contract of Sale May Be Absolute or ConditionalDocument5 pagesA Contract of Sale May Be Absolute or ConditionalImthe OneNo ratings yet

- Starbuck Corporate GovernanceDocument26 pagesStarbuck Corporate GovernanceImthe One100% (1)

- Quiz 1Document3 pagesQuiz 1Imthe OneNo ratings yet

- Chapter 2 Notes PayableDocument13 pagesChapter 2 Notes PayableImthe OneNo ratings yet

- Competitive Analysis: Porter's Five-Forces Model: Rivalry Among Competing FirmsDocument3 pagesCompetitive Analysis: Porter's Five-Forces Model: Rivalry Among Competing FirmsImthe OneNo ratings yet

- Guerta Term Paper - Ethical Issues and Problem of Our EconomyDocument2 pagesGuerta Term Paper - Ethical Issues and Problem of Our EconomyImthe OneNo ratings yet

- The Impact of Corporate Governance On Financial RiDocument9 pagesThe Impact of Corporate Governance On Financial RiImthe OneNo ratings yet

- Delay Sanction RulesDocument2 pagesDelay Sanction RulesImthe OneNo ratings yet

- Group 7 Activity BMWs Competitive AnalysisDocument2 pagesGroup 7 Activity BMWs Competitive AnalysisImthe OneNo ratings yet

- Internal Control BasicsDocument29 pagesInternal Control BasicsImthe OneNo ratings yet

- Two Sample T-Test StatologyDocument5 pagesTwo Sample T-Test StatologyMahek RawatNo ratings yet

- Although The Sale of Rhinoceros Horns Is Illegal WorldwideDocument1 pageAlthough The Sale of Rhinoceros Horns Is Illegal Worldwidezulfiqarali nagriNo ratings yet

- and His Name Shall Be Called WonderfulDocument3 pagesand His Name Shall Be Called WonderfulAlfirson BakarbessyNo ratings yet

- Solution:: Step: 1 of 7: Job Costing, Accounting For Manufacturing Overhead, Budgeted Rates. The PisanoDocument5 pagesSolution:: Step: 1 of 7: Job Costing, Accounting For Manufacturing Overhead, Budgeted Rates. The PisanoHerry SugiantoNo ratings yet

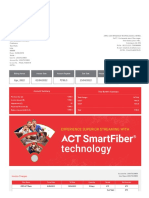

- Tax Invoice Gokulakrishnan .: Billing Period Invoice Date Amount Payable Due Date Amount After Due DateDocument2 pagesTax Invoice Gokulakrishnan .: Billing Period Invoice Date Amount Payable Due Date Amount After Due DateKumaresan SubramanianNo ratings yet

- Geeken New Price List - 2023Document91 pagesGeeken New Price List - 2023NirbhayNo ratings yet

- Period: Receipts Payments Net Receipts Export (F.o.b) Import (F.o.b) Trade BalanceDocument12 pagesPeriod: Receipts Payments Net Receipts Export (F.o.b) Import (F.o.b) Trade BalanceJannat TaqwaNo ratings yet

- Magma HDI General Insurance Company Limited: Magma House, 24 P S, K - 700016 Website: Http://magma-Hdi - Co.inDocument1 pageMagma HDI General Insurance Company Limited: Magma House, 24 P S, K - 700016 Website: Http://magma-Hdi - Co.inpratik ranaNo ratings yet

- Mathematical Analysis 2019 ASSIGNDocument9 pagesMathematical Analysis 2019 ASSIGNMario Rioux JnrNo ratings yet

- Monthly Stock Break Up (Nov.22)Document97 pagesMonthly Stock Break Up (Nov.22)CwsNo ratings yet

- 460d-Proposal Implementasi SAP B1 HANA-KAG-06 19Document94 pages460d-Proposal Implementasi SAP B1 HANA-KAG-06 19jusufjkNo ratings yet

- Tugas 2 Analyzing TransactionsDocument5 pagesTugas 2 Analyzing TransactionsNasrullahNo ratings yet

- Budgetary ControlDocument28 pagesBudgetary ControlDidie Diyanah0% (1)

- VII. Financial Plan: A. OverviewDocument9 pagesVII. Financial Plan: A. OverviewMark CafeNo ratings yet

- Chapter 8: Accounting For Receivables: Exercise 1Document45 pagesChapter 8: Accounting For Receivables: Exercise 1jokerightwegmail.com joke1233No ratings yet

- Office of Temporalities: Jerome TenebroDocument2 pagesOffice of Temporalities: Jerome TenebroJerome TenebroNo ratings yet

- Cash-And-Cash-Equivalent - Answers On HandoutDocument6 pagesCash-And-Cash-Equivalent - Answers On HandoutElaine AntonioNo ratings yet

- James S. Coleman - Free Riders and Zealots. The Role of Social NetworksDocument7 pagesJames S. Coleman - Free Riders and Zealots. The Role of Social NetworksJorgeA GNNo ratings yet

- Factors That Contributed To Euro Disneys Poor Performance Tourism EssayDocument12 pagesFactors That Contributed To Euro Disneys Poor Performance Tourism EssayOlusesan OpeyemiNo ratings yet

- Invoice: Your Companyname Your Companystreet 00 Postal Code and City 0044 (0) 000 000 000Document1 pageInvoice: Your Companyname Your Companystreet 00 Postal Code and City 0044 (0) 000 000 000Tagutswa Emmanuel MaingehamaNo ratings yet

- 1.all Drafting System. All Parts of DraftingDocument3 pages1.all Drafting System. All Parts of DraftingRatul Hasan0% (1)

- Indian Immunologicals Ltd.Document10 pagesIndian Immunologicals Ltd.Nani VolsNo ratings yet

- Lithos Design PietreLuminose Hamal TechnicalCardDocument4 pagesLithos Design PietreLuminose Hamal TechnicalCardermohamednaseemNo ratings yet

- 2147 Bill OmrDocument1 page2147 Bill Omrofficer lkoNo ratings yet

- Tutorial 6 Week 7 Short Answer SolutionDocument2 pagesTutorial 6 Week 7 Short Answer SolutionOmisha SinghNo ratings yet

- DPWH-INFR-45 ConMethDocument3 pagesDPWH-INFR-45 ConMethRayarch WuNo ratings yet

- Potensi Pasar Sekunder Spektrum Frekuensi Radio Di IndonesiaDocument16 pagesPotensi Pasar Sekunder Spektrum Frekuensi Radio Di IndonesiaLodewijk SitompulNo ratings yet

- Triveni Exp Third Ac (3A)Document2 pagesTriveni Exp Third Ac (3A)Anurag KumarNo ratings yet