You might also like

- CVP Question 6Document1 pageCVP Question 6Humphrey OsaigbeNo ratings yet

- Ch13 Exercise+9Document1 pageCh13 Exercise+9Ashley WilkeyNo ratings yet

- The Room Fellowship Video Transcript - Google Docs - 1157497090Document6 pagesThe Room Fellowship Video Transcript - Google Docs - 1157497090biggykhairNo ratings yet

- Astm D2467-2013Document8 pagesAstm D2467-2013Renato CorrêaNo ratings yet

- IMT 58 Management Accounting M3Document23 pagesIMT 58 Management Accounting M3solvedcareNo ratings yet

- CH 12Document3 pagesCH 12ghsoub777No ratings yet

- Classwork:: 1) Solved Following Question and Also Discussed Concept of Opening Trial BalanceDocument1 pageClasswork:: 1) Solved Following Question and Also Discussed Concept of Opening Trial BalanceAhmad HasnainNo ratings yet

- Redesigning Cost Systems: Is Standard Costing Obsolete?Document10 pagesRedesigning Cost Systems: Is Standard Costing Obsolete?SillyBee1205No ratings yet

- 2014 Bep Analysis ExercisesDocument5 pages2014 Bep Analysis ExercisesaimeeNo ratings yet

- Report On American and Efird, Inc (A&E) - BangladeshDocument31 pagesReport On American and Efird, Inc (A&E) - Bangladeshsalman.ja021No ratings yet

- Javier Danna Assignment 2.3 &3.5Document4 pagesJavier Danna Assignment 2.3 &3.5Danna ClaireNo ratings yet

- Job Costing CADocument13 pagesJob Costing CAmiranti dNo ratings yet

- Chapter Two Materials ManagementDocument40 pagesChapter Two Materials ManagementYeabsira WorkagegnehuNo ratings yet

- Mañanita Songs Mañanita SongsDocument2 pagesMañanita Songs Mañanita SongsSanchez Bayan100% (1)

- Practice Quiz M1 (Ungraded) - MergedDocument22 pagesPractice Quiz M1 (Ungraded) - MergedAbdullah Abdullah100% (1)

- CH 19 Inventory TheoryDocument15 pagesCH 19 Inventory TheoryRitesh SharmaNo ratings yet

- Question Bank Paper: Cost Accounting McqsDocument8 pagesQuestion Bank Paper: Cost Accounting McqsNikhilNo ratings yet

- Chapter 11 - Network ModelsDocument22 pagesChapter 11 - Network ModelsAbo Fawaz100% (1)

- BEP N CVP AnalysisDocument49 pagesBEP N CVP AnalysisJamaeca Ann MalsiNo ratings yet

- Quantity Discount Model (Example)Document13 pagesQuantity Discount Model (Example)shirleyna saraNo ratings yet

- Waiting Line ModelsDocument30 pagesWaiting Line ModelsPinky GuptaNo ratings yet

- Understand Support Department Cost Allocation MethodsDocument27 pagesUnderstand Support Department Cost Allocation Methodsluckystar251095No ratings yet

- Module 2 - Capacity Planning Practice ProblemsDocument3 pagesModule 2 - Capacity Planning Practice ProblemsIsabel CalderonNo ratings yet

- Should XYZ Company Make or Buy WidgetsDocument8 pagesShould XYZ Company Make or Buy WidgetsPui YanNo ratings yet

- LKAS 19 2021 UploadDocument31 pagesLKAS 19 2021 Uploadpriyantha dasanayake100% (1)

- Variance Analysis AND Standard CostingDocument37 pagesVariance Analysis AND Standard CostingWaniey HassanNo ratings yet

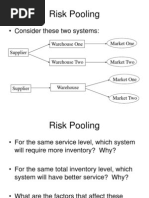

- Risk PoolingDocument11 pagesRisk PoolingAshok100% (1)

- Cost II Chapter ThreeDocument11 pagesCost II Chapter ThreeSemira100% (1)

- 17 SolutionsDocument7 pages17 Solutionsbrynner16No ratings yet

- Solutions ExosDocument11 pagesSolutions ExosazratNo ratings yet

- MBA 504 Ch3 SolutionsDocument22 pagesMBA 504 Ch3 SolutionsMohit Kumar GuptaNo ratings yet

- WCM QuestionsDocument13 pagesWCM QuestionsjeevikaNo ratings yet

- Standard (I Unit Produced) ParticularsDocument11 pagesStandard (I Unit Produced) ParticularsForam Raval100% (1)

- Inventory Management (2021)Document8 pagesInventory Management (2021)JustyNo ratings yet

- Practical BEP QuestionsDocument16 pagesPractical BEP QuestionsSanyam GoelNo ratings yet

- Paper 2 Quantitative Techniques PDFDocument12 pagesPaper 2 Quantitative Techniques PDFTuryamureeba JuliusNo ratings yet

- Capacity Planning: Mcgraw-Hill/IrwinDocument15 pagesCapacity Planning: Mcgraw-Hill/IrwinKader KARAAĞAÇNo ratings yet

- Chapter 10 Plant Assets, Natural Resources, and Intangible Assets (13 E)Document18 pagesChapter 10 Plant Assets, Natural Resources, and Intangible Assets (13 E)Raa100% (1)

- ValuationDocument23 pagesValuationishaNo ratings yet

- Chi-Square Test Examples for Business ResearchDocument5 pagesChi-Square Test Examples for Business ResearchSahil Bansal100% (1)

- Lista SiemensDocument65 pagesLista SiemensAlexandraNo ratings yet

- Standard CostingDocument18 pagesStandard Costingpakistan 123No ratings yet

- Select the most profitable capital investment alternativeDocument24 pagesSelect the most profitable capital investment alternativeDave DespabiladerasNo ratings yet

- I. Product Costs and Service Costs: Absorption CostingDocument12 pagesI. Product Costs and Service Costs: Absorption CostingLinyVatNo ratings yet

- Chapter 20Document93 pagesChapter 20Irina AlexandraNo ratings yet

- InventoryDocument46 pagesInventoryAnkit SharmaNo ratings yet

- A Numerical Example of Target and Lifecycle CostingDocument2 pagesA Numerical Example of Target and Lifecycle CostingAtulSinghNo ratings yet

- TYBCOM - Sem 6 - Cost AccountingDocument40 pagesTYBCOM - Sem 6 - Cost AccountingKhushi PrajapatiNo ratings yet

- Past Papers For Single Entry and Incomplete RecordsDocument2 pagesPast Papers For Single Entry and Incomplete RecordsMahreena IlyasNo ratings yet

- CA Ipcc Costing Suggested Answers For Nov 20161Document12 pagesCA Ipcc Costing Suggested Answers For Nov 20161Sai Kumar SandralaNo ratings yet

- Capital Budgeting Decisions ChapterDocument24 pagesCapital Budgeting Decisions Chapterpheeyona100% (1)

- MPR Lot Sizing Rules (L4L)Document30 pagesMPR Lot Sizing Rules (L4L)ajeng.saraswatiNo ratings yet

- TP ExampleDocument3 pagesTP ExampleWasik Abdullah MomitNo ratings yet

- 05 AC212 Lecture 5-Marginal Costing and Absorption Costing PDFDocument22 pages05 AC212 Lecture 5-Marginal Costing and Absorption Costing PDFsengpisalNo ratings yet

- Lesson 2Document6 pagesLesson 2Carlos Jan P. PenasNo ratings yet

- Job and Batch CostingDocument7 pagesJob and Batch CostingDeepak R GoradNo ratings yet

- Cost 2021-MayDocument8 pagesCost 2021-MayDAVID I MUSHINo ratings yet

- Assignment 8 AnswersDocument6 pagesAssignment 8 AnswersMyaNo ratings yet

- Valuing Bonds Yield Maturity CurrentDocument12 pagesValuing Bonds Yield Maturity CurrentLaraNo ratings yet

- Process CostingDocument37 pagesProcess CostingFrank ChinguwoNo ratings yet

- Exercise Process CostingDocument5 pagesExercise Process Costingshahadat hossainNo ratings yet

- Process Costing Bac 2 2023Document16 pagesProcess Costing Bac 2 2023Alice Emily0% (1)

- Just-In-Time and Backflush AccountingDocument3 pagesJust-In-Time and Backflush AccountingElla Mae VergaraNo ratings yet

- Process Costing Tutorial SheetDocument3 pagesProcess Costing Tutorial Sheets_camika7534No ratings yet

- MBAU601 L1d, Money Laundering & ISA 250Document36 pagesMBAU601 L1d, Money Laundering & ISA 250biggykhairNo ratings yet

- MBA A&F Elective Class Groupings MBAU608 Advance Audit 2023Document22 pagesMBA A&F Elective Class Groupings MBAU608 Advance Audit 2023biggykhairNo ratings yet

- UPSA SOGS MBA timetables 2022/2023Document9 pagesUPSA SOGS MBA timetables 2022/2023biggykhairNo ratings yet

- Opening of Bursary Portal - GRASAG UPSA-1Document1 pageOpening of Bursary Portal - GRASAG UPSA-1biggykhairNo ratings yet

- Corporate Reporting Strategy-MBA 2023 - Vertical GroupsDocument58 pagesCorporate Reporting Strategy-MBA 2023 - Vertical GroupsbiggykhairNo ratings yet

- University project workshop outlines groups programs facilitators datesDocument2 pagesUniversity project workshop outlines groups programs facilitators datesbiggykhairNo ratings yet

- IAS 12 Income Tax AccountingDocument29 pagesIAS 12 Income Tax AccountingbiggykhairNo ratings yet

- Topic 4 PefaDocument36 pagesTopic 4 PefabiggykhairNo ratings yet

- Registration Procedure for Continuing Graduate StudentsDocument3 pagesRegistration Procedure for Continuing Graduate StudentsbiggykhairNo ratings yet

- Standards On ConsoDocument33 pagesStandards On ConsobiggykhairNo ratings yet

- NOTICE-REOPNING OF UNDERGRADUATE STUDENTS-1ST SEM-2022-2023-RevisedDocument1 pageNOTICE-REOPNING OF UNDERGRADUATE STUDENTS-1ST SEM-2022-2023-RevisedbiggykhairNo ratings yet

- FR Outline - Graduate School Upsa 2020Document10 pagesFR Outline - Graduate School Upsa 2020biggykhairNo ratings yet

- University calendar 2022/23Document2 pagesUniversity calendar 2022/23biggykhairNo ratings yet

- Job Opportunities - Banking SectorDocument1 pageJob Opportunities - Banking SectorbiggykhairNo ratings yet

- Financial Management Course OutlineDocument9 pagesFinancial Management Course OutlinebiggykhairNo ratings yet

- Topic 4 - Competitve Dynamics (Autosaved)Document42 pagesTopic 4 - Competitve Dynamics (Autosaved)biggykhairNo ratings yet

- Transcript Dweck - 1960649121Document3 pagesTranscript Dweck - 1960649121biggykhairNo ratings yet

- UPSA MBA Sample Marketing Plan Georcynn (MPP) MBA 2021-22Document33 pagesUPSA MBA Sample Marketing Plan Georcynn (MPP) MBA 2021-22biggykhairNo ratings yet

- Top Talent Fellowship Accelerates CareersDocument23 pagesTop Talent Fellowship Accelerates CareersbiggykhairNo ratings yet

- Vmup7t - Stephen Kwadwo Agyakwa Dxb-AccDocument2 pagesVmup7t - Stephen Kwadwo Agyakwa Dxb-AccbiggykhairNo ratings yet

- MCPC 614 COST & MANAGEMENT ACC Course Outline 2021Document10 pagesMCPC 614 COST & MANAGEMENT ACC Course Outline 2021biggykhairNo ratings yet

- Financial Management AssignmentDocument1 pageFinancial Management AssignmentbiggykhairNo ratings yet

- Marketing AssignmentDocument5 pagesMarketing AssignmentbiggykhairNo ratings yet

- DR Amakye's Ia Sol-1Document5 pagesDR Amakye's Ia Sol-1biggykhairNo ratings yet

- The Marketing Journal RevisedDocument4 pagesThe Marketing Journal RevisedbiggykhairNo ratings yet

- Mini Case 1 - Time Value of MoneyDocument1 pageMini Case 1 - Time Value of MoneybiggykhairNo ratings yet

- University Accra Calendar 2022Document2 pagesUniversity Accra Calendar 2022biggykhairNo ratings yet

- MBA MARKETING COURSE REGISTRATION-newDocument2 pagesMBA MARKETING COURSE REGISTRATION-newbiggykhairNo ratings yet

- Overview of Financial Management... MBADocument32 pagesOverview of Financial Management... MBAbiggykhairNo ratings yet

- Sponge BobDocument4 pagesSponge BobchabriesNo ratings yet

- Sampling and Field Testing at Wastewater Treatment FacilitiesDocument11 pagesSampling and Field Testing at Wastewater Treatment FacilitiesSundarapandiyan SundaramoorthyNo ratings yet

- Circuits Review P2Document44 pagesCircuits Review P2José CastilloNo ratings yet

- Rules For The CertificationDocument84 pagesRules For The CertificationhdelriovNo ratings yet

- Demonstration POSTNATAL EXAMINATION Easy WayDocument9 pagesDemonstration POSTNATAL EXAMINATION Easy Wayjyoti singhNo ratings yet

- Flacs CFD ManualDocument658 pagesFlacs CFD ManualCyanNo ratings yet

- Brochure - 2018 - Hitfact Mkii 2Document2 pagesBrochure - 2018 - Hitfact Mkii 2diaa ahmedNo ratings yet

- Popular CultureDocument25 pagesPopular CultureVibhuti KachhapNo ratings yet

- NOISE ANALYSISDocument16 pagesNOISE ANALYSISDiana Rose TapelNo ratings yet

- Shock Classification and PathophysiologyDocument40 pagesShock Classification and PathophysiologyErick Anca100% (2)

- Genética, Modificaciones y MutacionesDocument12 pagesGenética, Modificaciones y MutacionespokemaniacoplancheNo ratings yet

- Mass DisasterDocument70 pagesMass DisasterJoseph RadovanNo ratings yet

- Saej401v002 PDFDocument6 pagesSaej401v002 PDFLuis LujanoNo ratings yet

- OrlDocument186 pagesOrlMuli MaroshiNo ratings yet

- Top 21 Largest EMS Companies in WorldDocument22 pagesTop 21 Largest EMS Companies in WorldjackNo ratings yet

- Air release plug and lifting lug details for 15 MVA 66/11.55 kV transformer radiatorDocument1 pageAir release plug and lifting lug details for 15 MVA 66/11.55 kV transformer radiatorshravan Kumar SinghNo ratings yet

- Plasma ChemistryDocument6 pagesPlasma ChemistryArief RomadhonNo ratings yet

- 5020-Article Text-10917-1-10-20220808Document9 pages5020-Article Text-10917-1-10-20220808indah rumah4No ratings yet

- Radiological Investigations: UltrasonographyDocument42 pagesRadiological Investigations: UltrasonographyDeeptanu GhoshNo ratings yet

- Fair Directory 02-2016Document44 pagesFair Directory 02-2016Ravichandran SNo ratings yet

- EniSpA - The Corporate Strategy of An International Energy Major PDFDocument24 pagesEniSpA - The Corporate Strategy of An International Energy Major PDFAnonymous 9ZMbuR75% (4)

- Do Not Open This Booklet Until Told To Do So: Question Booklet Series: - Question Booklet No.Document7 pagesDo Not Open This Booklet Until Told To Do So: Question Booklet Series: - Question Booklet No.Rakesh KumawatNo ratings yet

- Bread and Pastry Production NCII June 10, 2019 - July 03, 2019 ReviewerDocument14 pagesBread and Pastry Production NCII June 10, 2019 - July 03, 2019 ReviewerJames BaculaNo ratings yet

- Lista Arancelaria EUADocument547 pagesLista Arancelaria EUAvilisbeth18No ratings yet

- EE 102 Cabric Final Spring08 o Id15Document10 pagesEE 102 Cabric Final Spring08 o Id15Anonymous TbHpFLKNo ratings yet

- Managed Pressure Drilling MPD BrochureDocument5 pagesManaged Pressure Drilling MPD Brochureswaala4realNo ratings yet

- Computations on a waiters bill pad and conversations in the mistDocument3 pagesComputations on a waiters bill pad and conversations in the mistRavishu NagarwalNo ratings yet