You might also like

- Management Accounting Strategy Study Resource for CIMA Students: CIMA Study ResourcesFrom EverandManagement Accounting Strategy Study Resource for CIMA Students: CIMA Study ResourcesNo ratings yet

- Cost Accounting Fundamentals ExplainedDocument24 pagesCost Accounting Fundamentals Explainedshanu rockNo ratings yet

- COST ACCOUNTING FUNDAMENTALSDocument27 pagesCOST ACCOUNTING FUNDAMENTALSParmeet KaurNo ratings yet

- Objectives:: Semester Cost and Management AccountingDocument87 pagesObjectives:: Semester Cost and Management AccountingJon MemeNo ratings yet

- Management Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageFrom EverandManagement Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageRating: 5 out of 5 stars5/5 (1)

- Assignment DataDocument284 pagesAssignment DataDerickMwansaNo ratings yet

- Introduction to Cost Accounting ChapterDocument134 pagesIntroduction to Cost Accounting ChapterRyan Brown100% (1)

- CH 1 IntroductionDocument20 pagesCH 1 IntroductionKashish BhutadaNo ratings yet

- 2 Overview of Cost AccountingDocument18 pages2 Overview of Cost AccountingHarsh KhatriNo ratings yet

- Unit 1 IntroductionDocument14 pagesUnit 1 IntroductionIrfan KhanNo ratings yet

- Unit 1 IntroductionDocument14 pagesUnit 1 IntroductionIrfan KhanNo ratings yet

- Cost Accounting and ControlDocument19 pagesCost Accounting and ControlLenyBarrogaNo ratings yet

- Welding Economics and Management WFC 212-1Document59 pagesWelding Economics and Management WFC 212-1ibrahim mustaphaNo ratings yet

- Introduction To Cost AccountingDocument9 pagesIntroduction To Cost AccountingShohidul Islam SaykatNo ratings yet

- Meaning of CostDocument9 pagesMeaning of Costsanket8989100% (1)

- Cost Accounting LecturesDocument1 pageCost Accounting LecturesMich PelagioNo ratings yet

- Basic Concepts - Cost AccountingDocument28 pagesBasic Concepts - Cost AccountingSunil Vadhva100% (1)

- Absorption CostingDocument2 pagesAbsorption Costingvanessa claire abadNo ratings yet

- Cost Accounting AssignmentDocument15 pagesCost Accounting AssignmentDirector Telecom DoTNo ratings yet

- Meaningof Cost AccountingDocument13 pagesMeaningof Cost AccountingEthereal DNo ratings yet

- UNIT-1: Introduction of Cost AccountingDocument36 pagesUNIT-1: Introduction of Cost AccountingKaran SharmaNo ratings yet

- Cost AccountingDocument30 pagesCost Accountingmohammed33nNo ratings yet

- Cost AccountingDocument77 pagesCost Accountinggokulamaromal2001No ratings yet

- CA Inter Costing Theory Notes by CA Namit Arora SirDocument78 pagesCA Inter Costing Theory Notes by CA Namit Arora SirINTER SMARTIANSNo ratings yet

- New Management Accounting-1Document264 pagesNew Management Accounting-1leaky100% (1)

- 11th Sem - Cost ACT 1st NoteDocument5 pages11th Sem - Cost ACT 1st NoteRobin420420No ratings yet

- Financial Unit 2 Cost AccountingDocument29 pagesFinancial Unit 2 Cost AccountingJulls ApouakoneNo ratings yet

- MODULE - 6B Elementary Cost Accounting NotesDocument7 pagesMODULE - 6B Elementary Cost Accounting Noteskatojunior1No ratings yet

- Chapter-1: A Study On Cost Elements and Its Effects On Cost of ProductionDocument84 pagesChapter-1: A Study On Cost Elements and Its Effects On Cost of ProductionPraveen HJNo ratings yet

- 1 Cost AccountingDocument29 pages1 Cost AccountingChristine Mae TilledoNo ratings yet

- Characteristics of Marginal CostingDocument2 pagesCharacteristics of Marginal CostingLJBernardoNo ratings yet

- Course Title: Cost & Management Accounting Course Code:ACC 205Document37 pagesCourse Title: Cost & Management Accounting Course Code:ACC 205Ishita GuptaNo ratings yet

- Cost AccountingDocument59 pagesCost AccountingDitto SabuNo ratings yet

- 1meaning and Origin of Cost Accounting 1Document3 pages1meaning and Origin of Cost Accounting 1Jyoti GuptaNo ratings yet

- 4 Sem Bcom - Cost AccountingDocument54 pages4 Sem Bcom - Cost Accountingraja chatterjeeNo ratings yet

- Cost AccountingDocument30 pagesCost AccountingSunlight SirSundeepNo ratings yet

- Accounting For Business II PM Xii Chapter1Document27 pagesAccounting For Business II PM Xii Chapter1Anusga RamasamyNo ratings yet

- Cost AccountingDocument29 pagesCost Accountinghusman hussinNo ratings yet

- Cost Accounting BasicsDocument22 pagesCost Accounting BasicsSiddharth KakaniNo ratings yet

- Unit 1 Cost AccountingDocument20 pagesUnit 1 Cost AccountingCollins NyendwaNo ratings yet

- RFG 196 0113Document16 pagesRFG 196 0113Lets fight CancerNo ratings yet

- COST Accounting AND EstimationDocument38 pagesCOST Accounting AND EstimationMollaNo ratings yet

- Introduction To Costing: Page 1 of 2Document2 pagesIntroduction To Costing: Page 1 of 2Srayee BanikNo ratings yet

- Managerial Accounting DefinitionsDocument15 pagesManagerial Accounting Definitionskamal sahabNo ratings yet

- BBA V Sem Cost and Management Accounting IntroductionDocument19 pagesBBA V Sem Cost and Management Accounting IntroductionPridhvi Raj ReddyNo ratings yet

- Nature and Scope of Cost & Management Accounting: Unit 1Document24 pagesNature and Scope of Cost & Management Accounting: Unit 1umang8808No ratings yet

- Topic One Introduction TopicDocument37 pagesTopic One Introduction Topicramadhanamos620No ratings yet

- Cost and Management AccountingDocument52 pagesCost and Management Accountings.lakshmi narasimhamNo ratings yet

- COST ACCOUNTING MODULE 1 2 MARK QUESTIONSDocument24 pagesCOST ACCOUNTING MODULE 1 2 MARK QUESTIONSjoe josephNo ratings yet

- Meaning and Scope of Cost AccountingDocument1 pageMeaning and Scope of Cost AccountingSabyasachi RoyNo ratings yet

- Techniques of CostingDocument1 pageTechniques of CostingAlamin MohammadNo ratings yet

- Cost Accounting FundamentalsDocument192 pagesCost Accounting FundamentalsVijayaraj JeyabalanNo ratings yet

- Accounting For Business II PM Xii Chapter1Document27 pagesAccounting For Business II PM Xii Chapter1Senthil S. VelNo ratings yet

- Atp 106 LPM Accounting - Topic 6 - Costing and BudgetingDocument17 pagesAtp 106 LPM Accounting - Topic 6 - Costing and BudgetingTwain JonesNo ratings yet

- Cost AccountingDocument9 pagesCost Accountingyaqoob008No ratings yet

- Cost Accounting-2Document114 pagesCost Accounting-2Saurabh BansalNo ratings yet

- Cost and Management AccountingDocument181 pagesCost and Management AccountingFaithful nongerai100% (1)

- Tools and Techniques of Cost ReductionDocument27 pagesTools and Techniques of Cost Reductionপ্রিয়াঙ্কুর ধর100% (2)

- Solutions To MidtermsDocument61 pagesSolutions To MidtermsEthereal DNo ratings yet

- !!download Your DataDocument1 page!!download Your DataKertis GundersonNo ratings yet

- Soriano ReviewerDocument142 pagesSoriano ReviewerKay100% (2)

- Data Privacy ActDocument11 pagesData Privacy ActEthereal DNo ratings yet

- Philippine Competition Law Defines Prohibited ActsDocument24 pagesPhilippine Competition Law Defines Prohibited ActsEthereal DNo ratings yet

- Gov - Acc AppendicesDocument48 pagesGov - Acc AppendicesEthereal DNo ratings yet

- Intellectual Property Rights LawDocument26 pagesIntellectual Property Rights LawEthereal DNo ratings yet

- Government Procurement Law (RA 9184) PDFDocument35 pagesGovernment Procurement Law (RA 9184) PDFEthereal DNo ratings yet

- Leadership and Management SkillsDocument5 pagesLeadership and Management SkillsEthereal DNo ratings yet

- Gov - Acc Chapter5Document67 pagesGov - Acc Chapter5Ethereal DNo ratings yet

- Health Dec New 1Document1 pageHealth Dec New 1Mary Rose RagasaNo ratings yet

- Acctg 101 Module 4Document4 pagesAcctg 101 Module 4Ethereal DNo ratings yet

- Cost - Pa2Document2 pagesCost - Pa2Ethereal DNo ratings yet

- Solicitation LetterDocument1 pageSolicitation LetterEthereal DNo ratings yet

- DKDocument1 pageDKEthereal DNo ratings yet

- Pre-Assessment Activity 1 - CostDocument1 pagePre-Assessment Activity 1 - CostEthereal DNo ratings yet

- History of Dance and its BenefitsDocument12 pagesHistory of Dance and its BenefitsEthereal DNo ratings yet

- Meaningof Cost AccountingDocument13 pagesMeaningof Cost AccountingEthereal DNo ratings yet

- Chapter 1 Economics and It's NatureDocument31 pagesChapter 1 Economics and It's NatureAlthea Faye RabanalNo ratings yet

- Relations and Functions - UpdatedDocument37 pagesRelations and Functions - UpdatedEthereal DNo ratings yet

- OWWA Welfare Assistance for Earthquake VictimsDocument1 pageOWWA Welfare Assistance for Earthquake VictimsEthereal D100% (1)

- AOM No. 2022-001 (21-22) - Audit of Accounts and Transactions Brgy. San Leonardo, BambangDocument27 pagesAOM No. 2022-001 (21-22) - Audit of Accounts and Transactions Brgy. San Leonardo, BambangGilbert D. AfallaNo ratings yet

- Statistics For Engineers and Scientists 4th Edition William Navidi Solutions ManualDocument26 pagesStatistics For Engineers and Scientists 4th Edition William Navidi Solutions ManualMarioAbbottojqd98% (46)

- Causes For Safety ObservationsDocument1 pageCauses For Safety ObservationsAlberto CastilloNo ratings yet

- Key Tips & Takeaways For GDPR Implementation Using COBIT 5Document2 pagesKey Tips & Takeaways For GDPR Implementation Using COBIT 5Atila TiniNo ratings yet

- Compensation Term Test 1 Cheat SheetDocument1 pageCompensation Term Test 1 Cheat SheetSydneyNo ratings yet

- Trade Mrak CertifDocument3 pagesTrade Mrak Certifmemes knowledgeNo ratings yet

- ISO 13485 Certification in Philippines - Factocert Provides Top ServicesDocument12 pagesISO 13485 Certification in Philippines - Factocert Provides Top ServicesJulius C. VillalvaNo ratings yet

- Mcclelland'S Theory of Needs: AchievementDocument3 pagesMcclelland'S Theory of Needs: AchievementAniket BiswasNo ratings yet

- Invoice 92013866 9100011081 MapalDocument2 pagesInvoice 92013866 9100011081 MapalSaulo TrejoNo ratings yet

- Module 2 Introduction To Cost Terms and ConceptsDocument52 pagesModule 2 Introduction To Cost Terms and ConceptsChesca AlonNo ratings yet

- Inventory Sap b1Document8 pagesInventory Sap b1Queen ValleNo ratings yet

- Afar2 Construction QuizDocument2 pagesAfar2 Construction QuizJoyce Anne MananquilNo ratings yet

- Presentation On Meera Herbal Powder: Gowrishankar.V Vinothkumar.G Vinraj.T Neelamani.M.KDocument24 pagesPresentation On Meera Herbal Powder: Gowrishankar.V Vinothkumar.G Vinraj.T Neelamani.M.KGowri ShankarNo ratings yet

- IC Quality Assurance Audit Checklist 11546 - WORDDocument2 pagesIC Quality Assurance Audit Checklist 11546 - WORDnafis2uNo ratings yet

- Synergy Consultants Group 2020 CampusDocument13 pagesSynergy Consultants Group 2020 Campusnishant guptaNo ratings yet

- The Principles of Project Management Cap. 2 ResumenDocument7 pagesThe Principles of Project Management Cap. 2 ResumenlauraNo ratings yet

- Permit To Work Training HSE PresentationDocument24 pagesPermit To Work Training HSE PresentationAhtesham AlamNo ratings yet

- SAMPLE MCQ's For STRATEGIC MANAGEMENTDocument9 pagesSAMPLE MCQ's For STRATEGIC MANAGEMENTWwe MomentsNo ratings yet

- Entrepreneurship Education KNEC Notes - Diploma - PDF Education - 1637647537581Document18 pagesEntrepreneurship Education KNEC Notes - Diploma - PDF Education - 1637647537581MosesNo ratings yet

- 11e AR ConfirmationsDocument12 pages11e AR ConfirmationsJL Huang0% (1)

- NEW Kontoor Manufacturing Routing Guide 2021.22 Version 2.1.FINALDocument29 pagesNEW Kontoor Manufacturing Routing Guide 2021.22 Version 2.1.FINALVeronica BrenisNo ratings yet

- Auditing and Assurance - HonoursDocument2 pagesAuditing and Assurance - HonoursVardaan JaiswalNo ratings yet

- Kaertech Electronics PO for Splice Clips and TapesDocument2 pagesKaertech Electronics PO for Splice Clips and TapesElena MosnitNo ratings yet

- Co Module Entrep q1 ST 1 Qad For Cnhs Shs OnlyDocument4 pagesCo Module Entrep q1 ST 1 Qad For Cnhs Shs Onlymycah hagadNo ratings yet

- Supplier Assessment Report-Zhejiang Hengdong Stainless Steel Co., Ltd.Document25 pagesSupplier Assessment Report-Zhejiang Hengdong Stainless Steel Co., Ltd.Joel VillafuerteNo ratings yet

- Labor Relations Case Digest CompilationDocument2 pagesLabor Relations Case Digest CompilationPraisah Marjorey PicotNo ratings yet

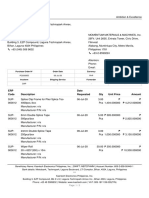

- Bradley Caldwell Inc. 200 Kiwanis Blvd. Hazleton, PA 18202 Tel: (570) 455-7511 Fax: (570) 455-0385Document3 pagesBradley Caldwell Inc. 200 Kiwanis Blvd. Hazleton, PA 18202 Tel: (570) 455-7511 Fax: (570) 455-0385Martin StrahilovskiNo ratings yet

- Bank of Baroda Leadership ChallengesDocument8 pagesBank of Baroda Leadership ChallengesShubham PriyamNo ratings yet

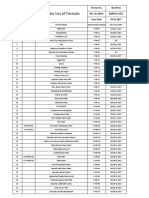

- Master List of Formats: SR No. Format No. Format Name New Format Number Rev. No./DateDocument14 pagesMaster List of Formats: SR No. Format No. Format Name New Format Number Rev. No./DateAbhishek DahiyaNo ratings yet

- Project Risk ManagementDocument16 pagesProject Risk ManagementRishabhGuptaNo ratings yet

- How to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)From EverandHow to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)Rating: 4.5 out of 5 stars4.5/5 (5)

- The Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindFrom EverandThe Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindRating: 5 out of 5 stars5/5 (231)

- I Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)From EverandI Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)Rating: 4.5 out of 5 stars4.5/5 (13)

- Love Your Life Not Theirs: 7 Money Habits for Living the Life You WantFrom EverandLove Your Life Not Theirs: 7 Money Habits for Living the Life You WantRating: 4.5 out of 5 stars4.5/5 (146)

- Profit First for Therapists: A Simple Framework for Financial FreedomFrom EverandProfit First for Therapists: A Simple Framework for Financial FreedomNo ratings yet

- Tax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesFrom EverandTax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesNo ratings yet

- Getting to Yes: How to Negotiate Agreement Without Giving InFrom EverandGetting to Yes: How to Negotiate Agreement Without Giving InRating: 4 out of 5 stars4/5 (652)

- The One-Page Financial Plan: A Simple Way to Be Smart About Your MoneyFrom EverandThe One-Page Financial Plan: A Simple Way to Be Smart About Your MoneyRating: 4.5 out of 5 stars4.5/5 (37)

- 7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelFrom Everand7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelNo ratings yet

- Financial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanFrom EverandFinancial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanRating: 4.5 out of 5 stars4.5/5 (79)

- Finance Basics (HBR 20-Minute Manager Series)From EverandFinance Basics (HBR 20-Minute Manager Series)Rating: 4.5 out of 5 stars4.5/5 (32)

- Bookkeeping: A Beginner’s Guide to Accounting and Bookkeeping for Small BusinessesFrom EverandBookkeeping: A Beginner’s Guide to Accounting and Bookkeeping for Small BusinessesRating: 5 out of 5 stars5/5 (4)

- Ledger Legends: A Bookkeeper's Handbook for Financial Success: Navigating the World of Business Finances with ConfidenceFrom EverandLedger Legends: A Bookkeeper's Handbook for Financial Success: Navigating the World of Business Finances with ConfidenceNo ratings yet

- Accounting Principles: Learn The Simple and Effective Methods of Basic Accounting And Bookkeeping Using This comprehensive Guide for Beginners(quick-books,made simple,easy,managerial,finance)From EverandAccounting Principles: Learn The Simple and Effective Methods of Basic Accounting And Bookkeeping Using This comprehensive Guide for Beginners(quick-books,made simple,easy,managerial,finance)Rating: 4.5 out of 5 stars4.5/5 (5)

- The Accounting Game: Learn the Basics of Financial Accounting - As Easy as Running a Lemonade Stand (Basics for Entrepreneurs and Small Business Owners)From EverandThe Accounting Game: Learn the Basics of Financial Accounting - As Easy as Running a Lemonade Stand (Basics for Entrepreneurs and Small Business Owners)Rating: 4 out of 5 stars4/5 (33)

- I'll Make You an Offer You Can't Refuse: Insider Business Tips from a Former Mob Boss (NelsonFree)From EverandI'll Make You an Offer You Can't Refuse: Insider Business Tips from a Former Mob Boss (NelsonFree)Rating: 4.5 out of 5 stars4.5/5 (24)

- Accounting 101: From Calculating Revenues and Profits to Determining Assets and Liabilities, an Essential Guide to Accounting BasicsFrom EverandAccounting 101: From Calculating Revenues and Profits to Determining Assets and Liabilities, an Essential Guide to Accounting BasicsRating: 4 out of 5 stars4/5 (7)

- Overcoming Underearning(TM): A Simple Guide to a Richer LifeFrom EverandOvercoming Underearning(TM): A Simple Guide to a Richer LifeRating: 4 out of 5 stars4/5 (21)

- Warren Buffett and the Interpretation of Financial Statements: The Search for the Company with a Durable Competitive AdvantageFrom EverandWarren Buffett and the Interpretation of Financial Statements: The Search for the Company with a Durable Competitive AdvantageRating: 4.5 out of 5 stars4.5/5 (109)

- Financial Accounting - Want to Become Financial Accountant in 30 Days?From EverandFinancial Accounting - Want to Become Financial Accountant in 30 Days?Rating: 5 out of 5 stars5/5 (1)

- LLC Beginner's Guide: The Most Updated Guide on How to Start, Grow, and Run your Single-Member Limited Liability CompanyFrom EverandLLC Beginner's Guide: The Most Updated Guide on How to Start, Grow, and Run your Single-Member Limited Liability CompanyRating: 5 out of 5 stars5/5 (1)