You might also like

- Milady 9781439059302 ch22Document22 pagesMilady 9781439059302 ch22Mais Omer100% (2)

- DC-Machines-Problems & SolutionsDocument23 pagesDC-Machines-Problems & SolutionsMais Omer83% (12)

- UCD81 Mark McGradyDocument4 pagesUCD81 Mark McGradymark mcgradyNo ratings yet

- Benefit Cost Analysis HandoutDocument16 pagesBenefit Cost Analysis HandoutGemma P. TabadaNo ratings yet

- Environmental Economics - Field & FieldDocument21 pagesEnvironmental Economics - Field & FieldMateo PradaNo ratings yet

- Environmental Law ProjectDocument11 pagesEnvironmental Law ProjectFaraz SiddiquiNo ratings yet

- Public Private PartnershipDocument14 pagesPublic Private PartnershipNeenu Rajput100% (1)

- Public Private Partnership-: Lessons from Gujarat for Uttar PradeshFrom EverandPublic Private Partnership-: Lessons from Gujarat for Uttar PradeshNo ratings yet

- Weimer & Vining (2011) Chapter 4Document17 pagesWeimer & Vining (2011) Chapter 4DiegoNo ratings yet

- Inventory of Barangay Facilities and Barangay Based Workers2022Document1 pageInventory of Barangay Facilities and Barangay Based Workers2022Robert Dela Cruz LamelaNo ratings yet

- Welfare EconomicsDocument6 pagesWelfare EconomicsBernardokpeNo ratings yet

- Motivation Letter - GermanyDocument2 pagesMotivation Letter - GermanyMais Omer100% (1)

- Welfare EconomicsDocument77 pagesWelfare Economicsgazal1987No ratings yet

- Chap 3. HET II Class NotesDocument14 pagesChap 3. HET II Class NotesFetsum LakewNo ratings yet

- Pigovian Welfare Economics 1Document8 pagesPigovian Welfare Economics 1vikram inamdarNo ratings yet

- Finteo (2) (Vseborec cz-f33sx)Document25 pagesFinteo (2) (Vseborec cz-f33sx)Matej HaraslínNo ratings yet

- Weitamann - BienestarDocument23 pagesWeitamann - Bienestaralvaropiogomez1No ratings yet

- Haveman and Weisbrod 1975 Defining BenefitsDocument29 pagesHaveman and Weisbrod 1975 Defining Benefitsgonutswithsquirrels0No ratings yet

- Assignment No. 1 Q.1 Explain Pareto Optimality in DetailDocument18 pagesAssignment No. 1 Q.1 Explain Pareto Optimality in Detailgulzar ahmadNo ratings yet

- Public-Private Partnerships: A Public Economics Perspective: Efraim SadkaDocument29 pagesPublic-Private Partnerships: A Public Economics Perspective: Efraim SadkaspratiwiaNo ratings yet

- 10 Chapter 2Document48 pages10 Chapter 2zizu1234No ratings yet

- Welfare Aspects of Benefit-Cost Analysis (Krutilla, JPE 1961)Document11 pagesWelfare Aspects of Benefit-Cost Analysis (Krutilla, JPE 1961)Muhammad AbubakrNo ratings yet

- PigouDocument3 pagesPigouvikram inamdarNo ratings yet

- Cost Benefit AnalysisDocument20 pagesCost Benefit Analysisdavid56565No ratings yet

- Chapter 1 Dan 2Document18 pagesChapter 1 Dan 2Keijo HandaNo ratings yet

- A Man Kept Searching For His Wallet Under The Street Lamp Because, He Said, It Was Too Dark in The Back Alley Where He Had Lost It.Document32 pagesA Man Kept Searching For His Wallet Under The Street Lamp Because, He Said, It Was Too Dark in The Back Alley Where He Had Lost It.giaythuytinh_424No ratings yet

- Concept and Measurement of Productivity: BY Gboyega A. OyerantiDocument24 pagesConcept and Measurement of Productivity: BY Gboyega A. Oyerantikrystale_1ttt11No ratings yet

- Pareto OptimalityDocument14 pagesPareto OptimalityGoso GosoNo ratings yet

- Approaches: Welfare Economics Is A Branch of Economics That UsesDocument3 pagesApproaches: Welfare Economics Is A Branch of Economics That UsesDhaval AsharNo ratings yet

- Block 5Document45 pagesBlock 5Erika DoregoNo ratings yet

- Pearse and Turner Public NotesDocument9 pagesPearse and Turner Public NotesAbhinav MishraNo ratings yet

- MacroeconomicsDocument23 pagesMacroeconomicssanjeet_kaur_10No ratings yet

- Kaldor IS-LMDocument12 pagesKaldor IS-LMeddieNo ratings yet

- Keynes ProfPigouMoney 1937Document12 pagesKeynes ProfPigouMoney 1937Jorge “Pollux” MedranoNo ratings yet

- Ricardo Pigou ThesisDocument4 pagesRicardo Pigou ThesisKathryn Patel100% (2)

- Economic ExternalitiesDocument14 pagesEconomic ExternalitiesHaniyaAngelNo ratings yet

- Lecture 2 - Economics As Applied ScienceDocument9 pagesLecture 2 - Economics As Applied ScienceLuna LedezmaNo ratings yet

- Sustainability 13 04581 v2Document21 pagesSustainability 13 04581 v2ihp4romaniaNo ratings yet

- Ecological Economics-Principles and Applications-4Document50 pagesEcological Economics-Principles and Applications-4Edwin JoyoNo ratings yet

- Privatization, Information Incentives: David E - M - Sappington Joseph E - StiglitzDocument19 pagesPrivatization, Information Incentives: David E - M - Sappington Joseph E - StiglitzEdward KarimNo ratings yet

- The MIT Press The Review of Economics and StatisticsDocument4 pagesThe MIT Press The Review of Economics and StatisticsVitor VasconcelosNo ratings yet

- Part 1: Foundational Concepts For Media Economics: OutlineDocument17 pagesPart 1: Foundational Concepts For Media Economics: Outlinendh611No ratings yet

- Global Agricultural Value Systems and The South: Some Critical Issues at The Current JunctureDocument16 pagesGlobal Agricultural Value Systems and The South: Some Critical Issues at The Current JunctureMaria Eduarda Borges BarbosaNo ratings yet

- The Concept of "Efficiency" in Economics: WWS-597 ReinhardtDocument27 pagesThe Concept of "Efficiency" in Economics: WWS-597 ReinhardtPRATIK ROYNo ratings yet

- Chief Statisticion, United Kinrdorn Cer Trol Sfatistical: OflccDocument22 pagesChief Statisticion, United Kinrdorn Cer Trol Sfatistical: Oflccdwipchandnani6No ratings yet

- EEA Unit III 2023Document57 pagesEEA Unit III 2023Dr Gampala PrabhakarNo ratings yet

- SodapdfDocument50 pagesSodapdfzed zedlavNo ratings yet

- Environmental Law (Rajat)Document16 pagesEnvironmental Law (Rajat)Rajat KaushikNo ratings yet

- Externalities Research PaperDocument9 pagesExternalities Research PaperAdityaNo ratings yet

- 2.0. Overview of Welfare EconomicsDocument15 pages2.0. Overview of Welfare EconomicsDemasko TadesseNo ratings yet

- El Capitalismo Nacional y La Integracion Regional - 2012-2Document106 pagesEl Capitalismo Nacional y La Integracion Regional - 2012-2Dakotah LillyNo ratings yet

- Externalities and Market FailureDocument15 pagesExternalities and Market FailureRussell KuehNo ratings yet

- ACF Report Supply Chain Exp and Inv. Opportunities 20171124 FinalDocument43 pagesACF Report Supply Chain Exp and Inv. Opportunities 20171124 FinalFeyisa KebebeNo ratings yet

- Cardinal Utility AnalysisDocument17 pagesCardinal Utility AnalysisJayant SinglaNo ratings yet

- Social Responsibility and Business ExcellenceDocument7 pagesSocial Responsibility and Business ExcellenceIJAERS JOURNALNo ratings yet

- The Efficiency of The Green Taxes As InsDocument8 pagesThe Efficiency of The Green Taxes As InsvladNo ratings yet

- Polluter-Pays-Principle: The Cardinal Instrument For Addressing Climate ChangeDocument16 pagesPolluter-Pays-Principle: The Cardinal Instrument For Addressing Climate ChangeIvan GonzalesNo ratings yet

- Test HsdfhfhhfshsasfyDocument32 pagesTest Hsdfhfhhfshsasfyade118No ratings yet

- Zhuang (2007) - Asian Development Bank: II. Theoretical Foundations For The Choice of A Social Discount Rate SRTPDocument8 pagesZhuang (2007) - Asian Development Bank: II. Theoretical Foundations For The Choice of A Social Discount Rate SRTPSimone PalladinoNo ratings yet

- Word Bank Impact PPPDocument23 pagesWord Bank Impact PPPdewangga04radenNo ratings yet

- Harnessing PPPDocument60 pagesHarnessing PPPasdf789456123No ratings yet

- 022 Article A014 enDocument4 pages022 Article A014 enmarijaandonova1992No ratings yet

- Lecture Notes On General Equilibrium Analysis and Resource AllocationDocument13 pagesLecture Notes On General Equilibrium Analysis and Resource AllocationYolanda TshakaNo ratings yet

- ManagementofpublicfundsDocument9 pagesManagementofpublicfundsNabeelNo ratings yet

- Public Private Partnerships: Principles for Sustainable ContractsFrom EverandPublic Private Partnerships: Principles for Sustainable ContractsNo ratings yet

- Trad Data Brazil To All CountryDocument42 pagesTrad Data Brazil To All CountryMais OmerNo ratings yet

- DocxDocument13 pagesDocxMais OmerNo ratings yet

- ERP ProjectDocument8 pagesERP ProjectMais OmerNo ratings yet

- Tarrif Brazil Export To All CountryDocument23 pagesTarrif Brazil Export To All CountryMais OmerNo ratings yet

- FulltextDocument31 pagesFulltextMais OmerNo ratings yet

- Course CurriculumDocument4 pagesCourse CurriculumMais OmerNo ratings yet

- Unit 24Document28 pagesUnit 24Mais OmerNo ratings yet

- Unit 16Document22 pagesUnit 16Mais OmerNo ratings yet

- Unit 21Document20 pagesUnit 21Mais OmerNo ratings yet

- Unit 19Document24 pagesUnit 19Mais OmerNo ratings yet

- Application of Fresco Art in Modern Interior Design: Hua QinDocument4 pagesApplication of Fresco Art in Modern Interior Design: Hua QinMais OmerNo ratings yet

- Several Sub-Questions Rise From The Main Question, Which Is As FollowsDocument6 pagesSeveral Sub-Questions Rise From The Main Question, Which Is As FollowsMais OmerNo ratings yet

- Unit 18Document22 pagesUnit 18Mais OmerNo ratings yet

- Unit 11Document16 pagesUnit 11Mais OmerNo ratings yet

- Unit 17Document18 pagesUnit 17Mais OmerNo ratings yet

- AI Reloaded: Objectives, Potentials, and Challenges of The Novel Field of Brain-Like Artificial IntelligenceDocument32 pagesAI Reloaded: Objectives, Potentials, and Challenges of The Novel Field of Brain-Like Artificial IntelligenceMais OmerNo ratings yet

- Remotesensing 13 03587Document22 pagesRemotesensing 13 03587Mais OmerNo ratings yet

- Unit 15Document16 pagesUnit 15Mais OmerNo ratings yet

- DefiningtheBlueEconomy 1Document9 pagesDefiningtheBlueEconomy 1Mais OmerNo ratings yet

- This Study Resource Was: About MobilyDocument6 pagesThis Study Resource Was: About MobilyMais OmerNo ratings yet

- The Modern Touch Interior Design and ModernisationDocument40 pagesThe Modern Touch Interior Design and ModernisationMais OmerNo ratings yet

- Or Admission To The English Degree Programs of Corvinus University of BudapestDocument2 pagesOr Admission To The English Degree Programs of Corvinus University of BudapestMais OmerNo ratings yet

- International Economy and Business Master'S ProgramDocument13 pagesInternational Economy and Business Master'S ProgramMais OmerNo ratings yet

- Certificate of EligibilityDocument2 pagesCertificate of EligibilityReina montes100% (1)

- Basic Elements of Rural DevelopmentDocument7 pagesBasic Elements of Rural DevelopmentShivam KumarNo ratings yet

- In Gov edisha-CTCER-031411901009091Document1 pageIn Gov edisha-CTCER-031411901009091Sumit Kumar(1995) 12ANo ratings yet

- Guilford County Division of Social Services Ordered To Make Corrective Action PlanDocument4 pagesGuilford County Division of Social Services Ordered To Make Corrective Action PlanFOX8No ratings yet

- CS-FORM-LEAVE DepedDocument9 pagesCS-FORM-LEAVE DepedAlyssa LoisNo ratings yet

- Letter For CSRDocument2 pagesLetter For CSRalmarah FoundationNo ratings yet

- Social Welfare Administrartion McqsDocument2 pagesSocial Welfare Administrartion McqsAbd ur Rehman Vlogs & VideosNo ratings yet

- PENILAIAN TENGAH SEMESTER (GEOGRAFI) (Respons)Document25 pagesPENILAIAN TENGAH SEMESTER (GEOGRAFI) (Respons)Giva Gelviandini SuhermanNo ratings yet

- Anh 10-Unit 4-Phonetics - Vocab-HSDocument2 pagesAnh 10-Unit 4-Phonetics - Vocab-HSÁnh PhạmNo ratings yet

- Tax Law IIDocument14 pagesTax Law IIshreya ahujaNo ratings yet

- Letter To Line Departments For Convergence Operaton Smile - VIDocument1 pageLetter To Line Departments For Convergence Operaton Smile - VIDistrict Child Protection Officer VikarabadNo ratings yet

- Certificate of Commendation: Christine Queen G. UngabDocument14 pagesCertificate of Commendation: Christine Queen G. UngabGianne Azel Gorne Torrejos-SaludoNo ratings yet

- Animal Rights Conference 2013Document20 pagesAnimal Rights Conference 2013Vegan FutureNo ratings yet

- Orphanages in Jaipur and UdaipurDocument20 pagesOrphanages in Jaipur and Udaipurships0401No ratings yet

- Diagnostic Test G9 2023Document4 pagesDiagnostic Test G9 2023Sweetzell IsaguirreNo ratings yet

- May 2021 MarDocument13 pagesMay 2021 MarHamid Ampatuan TatakNo ratings yet

- ArgumentativeessayfinalDocument11 pagesArgumentativeessayfinalapi-323064191No ratings yet

- Nandigama: SachivalayamDocument4 pagesNandigama: Sachivalayamkunkalaguntagp2No ratings yet

- Child Information SheetDocument3 pagesChild Information SheetHaidi MeanaNo ratings yet

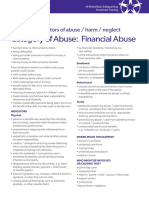

- Financial Abuse Handout Activity 5Document1 pageFinancial Abuse Handout Activity 5LEONARD ALMAZANNo ratings yet

- Project Proposal in Community ImmersionDocument3 pagesProject Proposal in Community Immersionmdelosreyes.uccbpanorthNo ratings yet

- Efficiency and Equity - Chap#7Document19 pagesEfficiency and Equity - Chap#7afzalkhancss3311No ratings yet

- Affidavit - Noel DomingoDocument2 pagesAffidavit - Noel DomingoHannahQuilangNo ratings yet

- Rebar Detail (Draft) - Model - PDF 1 1Document1 pageRebar Detail (Draft) - Model - PDF 1 1Jopheth RelucioNo ratings yet

- 6th NOVICE MOOT COURT COMPETITIONDocument17 pages6th NOVICE MOOT COURT COMPETITIONSAI CHAITANYA YEPURINo ratings yet

- Letter of ComplaintDocument7 pagesLetter of ComplaintHouston ChronicleNo ratings yet

- E Anudan RegistrationDocument2 pagesE Anudan RegistrationNgo PartnerNo ratings yet

- Groupwork Casestudy To Be RevisedDocument20 pagesGroupwork Casestudy To Be RevisedRovern Keith Oro CuencaNo ratings yet