You might also like

- Ultimate Credit Repair GuideDocument38 pagesUltimate Credit Repair Guidewlingle11756% (9)

- Checkingstatement - 02 10 2023Document4 pagesCheckingstatement - 02 10 2023Super broly Jiren x gogetaNo ratings yet

- Mba Corporate FinanceDocument61 pagesMba Corporate Finance821sarwar100% (1)

- Chapter 1 - An Overview of Financial Managemen: ReviewerDocument3 pagesChapter 1 - An Overview of Financial Managemen: ReviewerChristian Mozo Oliva67% (3)

- Financial Market ReviewerDocument9 pagesFinancial Market ReviewerBryan NograNo ratings yet

- PaySlip PDFDocument1 pagePaySlip PDFLALA TomarNo ratings yet

- Business Finance ReviewerDocument4 pagesBusiness Finance ReviewerJanna rae BionganNo ratings yet

- Segregated Funds and Annuities Study ChecklistDocument2 pagesSegregated Funds and Annuities Study ChecklistYuhui Shi0% (1)

- Business Finance ModuleDocument41 pagesBusiness Finance ModulerhyzeNo ratings yet

- Lecture - Introduction To Banking and Financial InstitutionsDocument3 pagesLecture - Introduction To Banking and Financial InstitutionsJessalyn Cabael100% (1)

- CompleteFreedom 0066 22oct2022Document5 pagesCompleteFreedom 0066 22oct2022bigman walthoNo ratings yet

- 85Document58 pages85damnrod23100% (1)

- Mutual Funds - The Mutual Fund Retirement Plan For Long - Term Wealth BuildingFrom EverandMutual Funds - The Mutual Fund Retirement Plan For Long - Term Wealth BuildingNo ratings yet

- HHHJJDocument6 pagesHHHJJNiks MonzantoNo ratings yet

- FinmanDocument1 pageFinmansweet ecstacyNo ratings yet

- Finance ReviewerDocument6 pagesFinance Reviewerlun3l1ght18No ratings yet

- Xfinmar - PrelimsDocument22 pagesXfinmar - PrelimsAndrea CuiNo ratings yet

- Chapter 5 and 6 Financial SystemDocument7 pagesChapter 5 and 6 Financial SystemRemar22No ratings yet

- MBM 507 - Financial Management ReviewerDocument10 pagesMBM 507 - Financial Management ReviewerEdson FenequitoNo ratings yet

- Finmar Final Handouts 1 PDFDocument3 pagesFinmar Final Handouts 1 PDFAcissejNo ratings yet

- FINMAR - Introduction To Financial Management and Financial MarketsDocument8 pagesFINMAR - Introduction To Financial Management and Financial MarketsLagcao Claire Ann M.No ratings yet

- Business-Finance ReviewerDocument7 pagesBusiness-Finance ReviewerRed TigerNo ratings yet

- Credit and CollectionDocument2 pagesCredit and CollectionesparragokailaNo ratings yet

- Business Finance Chapter 1 Hand-OutDocument4 pagesBusiness Finance Chapter 1 Hand-OutAliza UrtalNo ratings yet

- GROUP 1: Developing Corporate Entrepreneurship GROUP 2: Entrepreneurial Finance SourceDocument3 pagesGROUP 1: Developing Corporate Entrepreneurship GROUP 2: Entrepreneurial Finance SourceLegendXNo ratings yet

- Capital Market ManagementDocument28 pagesCapital Market ManagementJenina Rose SalvadorNo ratings yet

- 1st Semester (Digital Notebook - Business Finance)Document9 pages1st Semester (Digital Notebook - Business Finance)Raven RubiNo ratings yet

- Investm Ent Bank Comme Rcial Bank: Principles of FinanceDocument4 pagesInvestm Ent Bank Comme Rcial Bank: Principles of FinanceJustine PascualNo ratings yet

- Business Finance ReviewerDocument17 pagesBusiness Finance ReviewerkassyvsNo ratings yet

- Introduction To Financial Management NotesDocument4 pagesIntroduction To Financial Management NotesDana Gabrielle Sta Maria OconNo ratings yet

- 4.1 Sources of Funds For Business Operations FundsDocument1 page4.1 Sources of Funds For Business Operations FundsChzNo ratings yet

- Finance Notes (M1 M6 John) MinDocument10 pagesFinance Notes (M1 M6 John) Minlalla.lilli026No ratings yet

- Accounting 1Document3 pagesAccounting 1Carmina Dongcayan100% (1)

- Participation in The Market: A Portion ofDocument5 pagesParticipation in The Market: A Portion ofRonah Abigail BejocNo ratings yet

- MCM Tutorial 2Document3 pagesMCM Tutorial 2SHU WAN TEHNo ratings yet

- Bus. Finance Lecture Ch. 12Document16 pagesBus. Finance Lecture Ch. 12Camille BigataNo ratings yet

- Introduction To FinanceDocument32 pagesIntroduction To FinancezhengcunzhangNo ratings yet

- FinmanDocument3 pagesFinmanDiana Rose BassigNo ratings yet

- FNDC ModulesDocument2 pagesFNDC ModulesJessa LanuzaNo ratings yet

- CHP 1 NTRO ADVANCED FINANCIAL MANAGEMENTDocument4 pagesCHP 1 NTRO ADVANCED FINANCIAL MANAGEMENTcuteserese roseNo ratings yet

- Philippine Stock Exchange (PSE) :: FinanceDocument3 pagesPhilippine Stock Exchange (PSE) :: FinanceAdrienne Erika MANAIGNo ratings yet

- Value of StocksDocument3 pagesValue of StocksYummyNo ratings yet

- Bsac 274 Finmrkts Class Seatwork May 20 2022-Student Copy - RoldanDocument5 pagesBsac 274 Finmrkts Class Seatwork May 20 2022-Student Copy - RoldanJheraldinemae RoldanNo ratings yet

- Financial Institutions Market and InstrumentsDocument36 pagesFinancial Institutions Market and InstrumentsJean FlordelizNo ratings yet

- Micro Mid Terms Revision (EC1101E)Document6 pagesMicro Mid Terms Revision (EC1101E)ongnigel88No ratings yet

- Business Finance Notes Finals TermDocument3 pagesBusiness Finance Notes Finals TermMary Antonette VeronaNo ratings yet

- BF BinderDocument7 pagesBF BinderShane VeiraNo ratings yet

- Investment & Portfolio Management Chapter 1: Investing Is An Important Activity Worldwide InvestmentDocument6 pagesInvestment & Portfolio Management Chapter 1: Investing Is An Important Activity Worldwide InvestmentMuhammad Adil HusnainNo ratings yet

- Financial Institution Institutions and MarketsDocument13 pagesFinancial Institution Institutions and Marketstarekegn gezahegnNo ratings yet

- RES455 TUTORIAL 3 MONETARY & BANKING - WilDocument6 pagesRES455 TUTORIAL 3 MONETARY & BANKING - WilwilmaNo ratings yet

- Banks of QuestionsDocument28 pagesBanks of QuestionsViệt Hưng ĐặngNo ratings yet

- REVIEWERDocument10 pagesREVIEWERVeemaeNo ratings yet

- Asummary For Sources of FinanceDocument11 pagesAsummary For Sources of FinanceMostafa SakrNo ratings yet

- Lesson 1: Introduction To Financial AccountingDocument3 pagesLesson 1: Introduction To Financial AccountingRomae DomagasNo ratings yet

- Banking and Financial Institution 1ST Term MT ReviewerDocument16 pagesBanking and Financial Institution 1ST Term MT ReviewerAly JoNo ratings yet

- Finance BasicsDocument6 pagesFinance BasicsBushra HaqueNo ratings yet

- Annual Coupon Payments Paid by The Issuer Relative To The Bond's Face or Par ValueDocument4 pagesAnnual Coupon Payments Paid by The Issuer Relative To The Bond's Face or Par ValueRonah Abigail BejocNo ratings yet

- BUSINESS FINANCE Reviewer PrelimsDocument3 pagesBUSINESS FINANCE Reviewer Prelimssushi nakiriNo ratings yet

- W1f FINS3650 Essential Readings SummaryDocument6 pagesW1f FINS3650 Essential Readings SummaryShruti IyengarNo ratings yet

- Course II "International Financial Markets and Institutions"Document22 pagesCourse II "International Financial Markets and Institutions"Valentina OlteanuNo ratings yet

- REVIEWER TuesdayDocument5 pagesREVIEWER TuesdayVeemaeNo ratings yet

- Financial MGMT (Mod 1)Document4 pagesFinancial MGMT (Mod 1)Mikaella LamadoraNo ratings yet

- The Search For Entrepreneurial CapitalDocument5 pagesThe Search For Entrepreneurial CapitalAngelie Anillo100% (1)

- AE 18 Financial Market Prelim ExamDocument3 pagesAE 18 Financial Market Prelim ExamWenjunNo ratings yet

- Fin 2Document5 pagesFin 2ENCARNACION, Chatrisia J.No ratings yet

- Business FinanceDocument16 pagesBusiness FinanceFat AjummaNo ratings yet

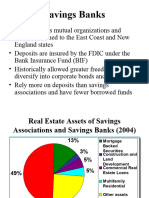

- Savings BanksDocument7 pagesSavings BanksLara KhanNo ratings yet

- Understanding Your Bank Statement Oct 17 3Document3 pagesUnderstanding Your Bank Statement Oct 17 3mohammad moradiNo ratings yet

- Best High-Yield Savings Account Rates For August 2023-Up To 5.25%Document11 pagesBest High-Yield Savings Account Rates For August 2023-Up To 5.25%Benjamin YokeshNo ratings yet

- Fortnightly Tax Table 2016 17Document10 pagesFortnightly Tax Table 2016 17nirpatel2No ratings yet

- Canara Delite Current Account Product Features A CO Vijayawada Marketing InitiativeDocument7 pagesCanara Delite Current Account Product Features A CO Vijayawada Marketing InitiativeRammurthy JVNo ratings yet

- Authority Letter & NOC (Faizan Pharmacy) SamundriDocument2 pagesAuthority Letter & NOC (Faizan Pharmacy) Samundrifaizanhafeez786No ratings yet

- Apollo Global Asset Backed Finance White PaperDocument16 pagesApollo Global Asset Backed Finance White PaperstieberinspirujNo ratings yet

- Momin 1408101063900Document12 pagesMomin 1408101063900mominalibaigNo ratings yet

- IDFCFIRSTBankstatement 10051177724 170334404Document2 pagesIDFCFIRSTBankstatement 10051177724 170334404Samson PereiraNo ratings yet

- Enhancement in Gratuity Limit Under Payment of Gratuity ActDocument4 pagesEnhancement in Gratuity Limit Under Payment of Gratuity ActPaymaster ServicesNo ratings yet

- Chapter-12: Tender No PLM/PHDPL-AUG Technical Specifications - Combined Station WorksDocument8 pagesChapter-12: Tender No PLM/PHDPL-AUG Technical Specifications - Combined Station WorksAjay HawaldarNo ratings yet

- Assignment On Mobile BankingDocument7 pagesAssignment On Mobile BankingArpon SAUNo ratings yet

- Allama Iqbal Open University, Islamabad WarningDocument2 pagesAllama Iqbal Open University, Islamabad WarningAbdullah ShahNo ratings yet

- Standing Instruction Format: Mortgages/DVRA/Ver5.0/July2013Document5 pagesStanding Instruction Format: Mortgages/DVRA/Ver5.0/July2013Yudhi OctoraNo ratings yet

- The Fidelity Self-Employed 401 (K) Contribution W Worksheet For Unincorporated BusinessesDocument2 pagesThe Fidelity Self-Employed 401 (K) Contribution W Worksheet For Unincorporated BusinessesokumurakozoNo ratings yet

- MEcDocument12 pagesMEcBinduMishraNo ratings yet

- Gen Math 11Document5 pagesGen Math 11Lee GorgonioNo ratings yet

- Adjusting 12Document32 pagesAdjusting 12Prince Dkalm PolishedNo ratings yet

- Account ProjectDocument31 pagesAccount ProjectAayush ShNo ratings yet

- Iifk 3 T Rua IZUb EyyDocument3 pagesIifk 3 T Rua IZUb Eyyashutoshbbk786No ratings yet

- Management of Non Performing Assets Public Sector BankDocument76 pagesManagement of Non Performing Assets Public Sector BankShubham MuktiNo ratings yet

- Credit Bureau Report SampleDocument5 pagesCredit Bureau Report SampleIndra ChanNo ratings yet

- Advantages of Housing LoansDocument2 pagesAdvantages of Housing LoansVANYA DIXITNo ratings yet

- Saqib Ahmad MirDocument18 pagesSaqib Ahmad Mirsaqib mirNo ratings yet