You might also like

- Kaba Simplex Catalog and Price ListDocument72 pagesKaba Simplex Catalog and Price ListSecurity Lock DistributorsNo ratings yet

- Boericke Bell DefDocument9 pagesBoericke Bell DefSUJEET A VAGHANINo ratings yet

- Administration of Company LawDocument9 pagesAdministration of Company LawHunsikaa JainNo ratings yet

- EM Lab DiagramsDocument11 pagesEM Lab DiagramsAnkit IngaleNo ratings yet

- Mayans 121Document11 pagesMayans 121OnenessNo ratings yet

- Adobe Scan 06 May 2023Document10 pagesAdobe Scan 06 May 2023vasu dha5058No ratings yet

- 12.7.23 Mid UlsterDocument1 page12.7.23 Mid UlsterdreneavalentinstefanNo ratings yet

- Mayans 122Document11 pagesMayans 122OnenessNo ratings yet

- Open Elective Basic StatisticsDocument13 pagesOpen Elective Basic StatisticsHappy PalNo ratings yet

- Dancing in The Rain NotesDocument7 pagesDancing in The Rain NotesHABEEB ANSARI ANSARINo ratings yet

- Without YouDocument2 pagesWithout YouIce PanganibanNo ratings yet

- Estimation & Costing by Jaspal Sir PDFDocument74 pagesEstimation & Costing by Jaspal Sir PDFTata Apprentice 2021No ratings yet

- gr11 Chem Record First HalfDocument16 pagesgr11 Chem Record First HalfNIGHNA BHARWANI 9266No ratings yet

- (' ' ..... ,....., R F O D Cl/IC 2, S/C 2Document12 pages(' ' ..... ,....., R F O D Cl/IC 2, S/C 2Alan Jules WebermanNo ratings yet

- Plasma CIA AssignmentDocument18 pagesPlasma CIA AssignmentmessiNo ratings yet

- P'1Jljra: FytenoulDocument26 pagesP'1Jljra: FytenoulAnita GajbhiyeNo ratings yet

- Planning and Production Budget ForecastDocument7 pagesPlanning and Production Budget ForecastDevid MiracleNo ratings yet

- Follows:: Origins. D T NatDocument16 pagesFollows:: Origins. D T NatBarani Kumar NNo ratings yet

- Scan 12 May 2021Document3 pagesScan 12 May 2021CHINUKURI AKHILANo ratings yet

- Biology Notes Grade 10 (Vietnamese)Document11 pagesBiology Notes Grade 10 (Vietnamese)Lưu QuangHưngNo ratings yet

- Adobe Scan 04 May 2023Document21 pagesAdobe Scan 04 May 2023Ishi MadanNo ratings yet

- Cihnir/ 9'' To R3a "': Fune-RonsDocument2 pagesCihnir/ 9'' To R3a "': Fune-Ronssasi bhaskarNo ratings yet

- Mayans 134Document7 pagesMayans 134OnenessNo ratings yet

- CH 2 EcoDocument13 pagesCH 2 EcoKhushi BothraNo ratings yet

- Adobe Scan Nov 15, 2023Document22 pagesAdobe Scan Nov 15, 2023anshuak5660No ratings yet

- Unit 1 Flip Flop IntroductionDocument8 pagesUnit 1 Flip Flop Introductionevaragland16No ratings yet

- LL.M. Syllabus 2021-22Document14 pagesLL.M. Syllabus 2021-22Arzoo khanNo ratings yet

- CD Unit-4Document15 pagesCD Unit-4Ganesh DegalaNo ratings yet

- p.RJU: NJCJ/CDocument23 pagesp.RJU: NJCJ/CNamita SahooNo ratings yet

- CaricatureDocument3 pagesCaricatureJarred Abiel BionaNo ratings yet

- Ienal: TND UniversityDocument15 pagesIenal: TND UniversityAnany SharmaNo ratings yet

- VMD Iso ScanDocument11 pagesVMD Iso ScanVishal DeshpandeNo ratings yet

- Take Note 11Document11 pagesTake Note 11Lưu QuangHưngNo ratings yet

- Heat LabDocument61 pagesHeat LabMinhazul Abedin RiadNo ratings yet

- Enterprise Credit Evaluation CertificateDocument1 pageEnterprise Credit Evaluation CertificateAaron Marius JuliusNo ratings yet

- Project File On Haloalkane and HaloarenesDocument28 pagesProject File On Haloalkane and HaloarenesTMG VANSH100% (6)

- Adobe Scan 25 May 2023Document4 pagesAdobe Scan 25 May 2023ENTERTAINMENTNo ratings yet

- Consumer Protection ActDocument25 pagesConsumer Protection ActVenisa TellisNo ratings yet

- Rem 55Document1 pageRem 55Marlo Caluya ManuelNo ratings yet

- U4 AcnDocument24 pagesU4 Acn20kd1a05c1No ratings yet

- LTC Surity FormDocument2 pagesLTC Surity FormjyothiprakashNo ratings yet

- Adobe Scan 01 Dic. 2021Document3 pagesAdobe Scan 01 Dic. 2021Erika PupialesNo ratings yet

- CNS CIA1 MaterialDocument32 pagesCNS CIA1 Materialsamirjoshi605No ratings yet

- Assignment - 2 (EC502)Document15 pagesAssignment - 2 (EC502)Ritesh GhoshNo ratings yet

- DS - Practical - 3Document16 pagesDS - Practical - 3Soha KULKARNINo ratings yet

- Adobe Scan 20 Dec 2020Document31 pagesAdobe Scan 20 Dec 2020abhibadgujjar2525No ratings yet

- Unit 2 ContouringDocument15 pagesUnit 2 ContouringgomatesgNo ratings yet

- FASCIKEL 3 - OO Ovira - Informacija o Nakupu Jadrnic Podjetja Hillbroock Ter PrilogeDocument8 pagesFASCIKEL 3 - OO Ovira - Informacija o Nakupu Jadrnic Podjetja Hillbroock Ter PrilogeResnicaoorozjuNo ratings yet

- Quality ManagementDocument72 pagesQuality Managementajitesh pradhanNo ratings yet

- Solid State Viva QuestionsDocument7 pagesSolid State Viva QuestionsAnanya SNo ratings yet

- Assignment - III (Interval Estimation)Document5 pagesAssignment - III (Interval Estimation)aggarwalansh61No ratings yet

- Plant Physio File 1Document24 pagesPlant Physio File 1Anjali OjhaNo ratings yet

- Adobe ScanDocument26 pagesAdobe Scanharshsingh14oct2006No ratings yet

- Adobe Scan Nov 29 2021 2Document1 pageAdobe Scan Nov 29 2021 2api-578310216No ratings yet

- Chapter 3Document47 pagesChapter 3Parth GargNo ratings yet

- Chapter 1 AccountancyDocument18 pagesChapter 1 AccountancyJackie chan JNo ratings yet

- Adobe Scan 05 Apr 2022 16 Dec 20212022Document6 pagesAdobe Scan 05 Apr 2022 16 Dec 20212022MohibNo ratings yet

- Solution and exponential decay of minority carrier concentration in semiconductorDocument6 pagesSolution and exponential decay of minority carrier concentration in semiconductorSekh AsifNo ratings yet

- How Online Coupons Attract Subscribers and Benefit BusinessesDocument16 pagesHow Online Coupons Attract Subscribers and Benefit BusinessesDiego SerranoNo ratings yet

- IronDocument15 pagesIronI m legend kcNo ratings yet

- 917 - B.A. MusicDocument20 pages917 - B.A. MusicmgmtNo ratings yet

- UOK B.A. History Exam Scheme 2023Document19 pagesUOK B.A. History Exam Scheme 2023mgmtNo ratings yet

- Creating Safe Workplace For WomenDocument5 pagesCreating Safe Workplace For WomenmgmtNo ratings yet

- Boosting India's Low Tax BaseDocument7 pagesBoosting India's Low Tax BasemgmtNo ratings yet

- Rise of Agri-Tech in IndiaDocument7 pagesRise of Agri-Tech in IndiamgmtNo ratings yet

- Shaping The Data Governance RegimeDocument8 pagesShaping The Data Governance RegimemgmtNo ratings yet

- Women's Underrepresentation in PoliticsDocument7 pagesWomen's Underrepresentation in PoliticsmgmtNo ratings yet

- Transforming India's LogisticsDocument7 pagesTransforming India's LogisticsmgmtNo ratings yet

- Transforming The Ailing Cotton SectorDocument6 pagesTransforming The Ailing Cotton SectormgmtNo ratings yet

- Sales data by region, rep, item and unitsDocument1 pageSales data by region, rep, item and unitsmgmtNo ratings yet

- UPSC 2024 Daily Planner With NOTESDocument192 pagesUPSC 2024 Daily Planner With NOTESmgmtNo ratings yet

- Safeguarding The Rights of ConsumersDocument6 pagesSafeguarding The Rights of ConsumersmgmtNo ratings yet

- E Ship Unit 1, 2Document6 pagesE Ship Unit 1, 2mgmtNo ratings yet

- UG Professional PT. I, II & III Time-Table-2023Document12 pagesUG Professional PT. I, II & III Time-Table-2023mgmtNo ratings yet

- Economics Unit 4 Market and Trade CycleDocument23 pagesEconomics Unit 4 Market and Trade CyclemgmtNo ratings yet

- GGSIPU CET BBA Last Round Cutoff 2019 - HtFuoxvDocument4 pagesGGSIPU CET BBA Last Round Cutoff 2019 - HtFuoxvPrashant SemwalNo ratings yet

- Adobe Scan 29-Sep-2020Document11 pagesAdobe Scan 29-Sep-2020mgmtNo ratings yet

- FMNotesDocument98 pagesFMNotesmgmtNo ratings yet

- CAT 2023 Composite Score & Calls PredictorDocument72 pagesCAT 2023 Composite Score & Calls PredictormgmtNo ratings yet

- Adobe Scan 11-Oct-2020Document21 pagesAdobe Scan 11-Oct-2020mgmtNo ratings yet

- Business Env. Unit 1Document7 pagesBusiness Env. Unit 1mgmtNo ratings yet

- Assignment 1Document3 pagesAssignment 1Zhi Jin LouNo ratings yet

- Lxe10e A36 ADocument62 pagesLxe10e A36 AСергей ПетровNo ratings yet

- Hydraulic Quick Couplings: Double Shut-Off and Straight-Thru Couplings Rated PressureDocument66 pagesHydraulic Quick Couplings: Double Shut-Off and Straight-Thru Couplings Rated PressureRJ MechNo ratings yet

- What Do TIPS Say About Real Interest Rates and Required ReturnsDocument25 pagesWhat Do TIPS Say About Real Interest Rates and Required ReturnsKamel RamtanNo ratings yet

- Sipoc CompletionDocument3 pagesSipoc CompletionVishvas SutharNo ratings yet

- Punjab Small Industries Corporation Lahore (PSIC)Document42 pagesPunjab Small Industries Corporation Lahore (PSIC)Mueenhasan100% (1)

- Cost Accounting Midterm Examdocx PDF FreeDocument5 pagesCost Accounting Midterm Examdocx PDF FreeHannah Denise BatallangNo ratings yet

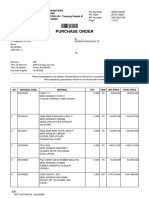

- Po NPN 5053104337 KrisbowDocument2 pagesPo NPN 5053104337 Krisbowryan vernando manikNo ratings yet

- CHAPTER-14 Cost10Document1 pageCHAPTER-14 Cost10Louiza Kyla AridaNo ratings yet

- EFS 40&50 Installation ManualDocument1,701 pagesEFS 40&50 Installation ManualHouvenaghelNo ratings yet

- Journal Entries For JulyDocument5 pagesJournal Entries For JulyGwendolyn PansoyNo ratings yet

- INTL ECON CHAPTER 1Document20 pagesINTL ECON CHAPTER 1Jubayer 3DNo ratings yet

- Barium NitrateDocument19 pagesBarium NitrateAli RafiqueNo ratings yet

- Choosing The Right Home Furniture For Your Own Home Some Advicedcvsx PDFDocument2 pagesChoosing The Right Home Furniture For Your Own Home Some Advicedcvsx PDFVinsonLaw13No ratings yet

- Pecp3003 - April 2022 PSKDocument855 pagesPecp3003 - April 2022 PSKAlberto100% (3)

- Toll Collection Since Inception PDFDocument9 pagesToll Collection Since Inception PDFsubhk2No ratings yet

- Unn - 2021 2022 Primary Admission List 1Document175 pagesUnn - 2021 2022 Primary Admission List 1LinzartxNo ratings yet

- AFM Practice Apply Guidance - Step 1Document1 pageAFM Practice Apply Guidance - Step 1Martin CannonNo ratings yet

- Pengaruh Kualitas Sumber Daya Manusia Ukuran UsahaDocument10 pagesPengaruh Kualitas Sumber Daya Manusia Ukuran Usahafebriantirismaa2No ratings yet

- MCQ From All Chapters of Economics Ca FoundationDocument48 pagesMCQ From All Chapters of Economics Ca FoundationShruti Raj70% (10)

- Slick LineDocument7 pagesSlick LineHosamMohamedNo ratings yet

- Group 4 members financial recordsDocument7 pagesGroup 4 members financial recordsvomawew647No ratings yet

- Pooja SinghDocument10 pagesPooja SinghPooja SinghNo ratings yet

- Polynomial RegressionDocument3 pagesPolynomial RegressionDennis ANo ratings yet

- Resentettlement PlanDocument185 pagesResentettlement PlanPranoy BaruaNo ratings yet

- University of ZimbabweDocument4 pagesUniversity of ZimbabwefaraiNo ratings yet

- Mohite Suzuki Kolhapur and Star Local Mart Kolhapur Travling Sheet 16-11-2023 To 21-11-2023Document3 pagesMohite Suzuki Kolhapur and Star Local Mart Kolhapur Travling Sheet 16-11-2023 To 21-11-2023phamberkarNo ratings yet

- Principles of Managerial Finance: Risk and ReturnDocument57 pagesPrinciples of Managerial Finance: Risk and ReturnJoshNo ratings yet