You might also like

- Math Practice Simplified: Decimals & Percents (Book H): Practicing the Concepts of Decimals and PercentagesFrom EverandMath Practice Simplified: Decimals & Percents (Book H): Practicing the Concepts of Decimals and PercentagesRating: 5 out of 5 stars5/5 (3)

- AirThreads Valuation SolutionDocument20 pagesAirThreads Valuation SolutionBill JoeNo ratings yet

- Marriott (2) ..Document13 pagesMarriott (2) ..veninsssssNo ratings yet

- Dupont Analysis ModelDocument278 pagesDupont Analysis ModelKartikay GoswamiNo ratings yet

- Broadcom Financial AnalysisDocument68 pagesBroadcom Financial AnalysisKipley_Pereles_5949No ratings yet

- MERCURY ATHLETIC FOOTWEAR COST OF CAPITAL ANALYSISDocument16 pagesMERCURY ATHLETIC FOOTWEAR COST OF CAPITAL ANALYSISBharat KoiralaNo ratings yet

- Assumptions: Comparable Companies:Market ValueDocument18 pagesAssumptions: Comparable Companies:Market ValueTanya YadavNo ratings yet

- AirThread CalcDocument15 pagesAirThread CalcSwati VermaNo ratings yet

- Air Thread ConnectionsDocument31 pagesAir Thread ConnectionsJasdeep SinghNo ratings yet

- Financial Projections and Analysis 2005-2011Document7 pagesFinancial Projections and Analysis 2005-2011akashNo ratings yet

- Airthreads Valuation Case Study Excel File PDF FreeDocument18 pagesAirthreads Valuation Case Study Excel File PDF Freegoyalmuskan412No ratings yet

- Rosetta Stone IPODocument5 pagesRosetta Stone IPOFatima Ansari d/o Muhammad AshrafNo ratings yet

- Case 1 MarriottDocument14 pagesCase 1 Marriotthimanshu sagar100% (1)

- Caso PolaroidDocument45 pagesCaso PolaroidByron AlarcònNo ratings yet

- CVR - Case - Excel FileDocument7 pagesCVR - Case - Excel FileVinay JajuNo ratings yet

- Main YearDocument3 pagesMain YearKe ShuNo ratings yet

- Altagas Green Exhibits With All InfoDocument4 pagesAltagas Green Exhibits With All InfoArjun NairNo ratings yet

- Industry Median 2018 2017 2016 2015 2014 2013 2012Document10 pagesIndustry Median 2018 2017 2016 2015 2014 2013 2012AnuragNo ratings yet

- Revenue, Costs, Profits, and Financial Analysis of Company from 1995-2011Document4 pagesRevenue, Costs, Profits, and Financial Analysis of Company from 1995-2011Anchal ChokhaniNo ratings yet

- Pe RatiosDocument6 pagesPe RatiosRakesh SharmaNo ratings yet

- DCF Modelling - WACC - Completed (1)Document6 pagesDCF Modelling - WACC - Completed (1)kukrejanikhil70No ratings yet

- NPV Function: Discount Rate Time Periods 2 3 4 Cash Flows NPV $35.9Document11 pagesNPV Function: Discount Rate Time Periods 2 3 4 Cash Flows NPV $35.9Ali Hussain Al SalmawiNo ratings yet

- Discounted Cash Flow (DCF) Valuation: This Model Is For Illustrative Purposes Only and Contains No FormulasDocument2 pagesDiscounted Cash Flow (DCF) Valuation: This Model Is For Illustrative Purposes Only and Contains No Formulasrito2005No ratings yet

- DCF Modelling - 12Document24 pagesDCF Modelling - 12sujal KumarNo ratings yet

- MFL 1 Cfin2Document17 pagesMFL 1 Cfin2Siddharth SureshNo ratings yet

- Ratio Analysis TemplateDocument3 pagesRatio Analysis TemplateTom CatNo ratings yet

- Financial Table Analysis of ZaraDocument9 pagesFinancial Table Analysis of ZaraCeren75% (4)

- Marico Financial Model (Final) (Final-1Document22 pagesMarico Financial Model (Final) (Final-1Jayant JainNo ratings yet

- P&L Statement Analysis of PI Industries LtdDocument45 pagesP&L Statement Analysis of PI Industries LtddixitBhavak DixitNo ratings yet

- 1996 Revenue Growth Rate Ebitda Margin Net Working Capital Percent of RevenueDocument14 pages1996 Revenue Growth Rate Ebitda Margin Net Working Capital Percent of RevenueRohith ThatchanNo ratings yet

- 17pgp216 ApolloDocument5 pages17pgp216 ApolloVamsi GunturuNo ratings yet

- Data Patterns Income&CashFlow - 4 Years - 19052020Document8 pagesData Patterns Income&CashFlow - 4 Years - 19052020Sundararaghavan RNo ratings yet

- Ratio Analysis TemplateDocument3 pagesRatio Analysis Templateعمر El KheberyNo ratings yet

- Marriott WACC and Divisional Cost of Capital AnalysisDocument15 pagesMarriott WACC and Divisional Cost of Capital AnalysisSaadatNo ratings yet

- DCF ModelDocument51 pagesDCF Modelhugoe1969No ratings yet

- Mehran Sugar Mills - Six Years Financial Review at A GlanceDocument3 pagesMehran Sugar Mills - Six Years Financial Review at A GlanceUmair ChandaNo ratings yet

- DCF Trident 2Document20 pagesDCF Trident 2Jayant JainNo ratings yet

- Exhibit 1: Gross Profit 3,597.1Document15 pagesExhibit 1: Gross Profit 3,597.1Rendy Setiadi MangunsongNo ratings yet

- Peng Plasma Solutions Tables PDFDocument12 pagesPeng Plasma Solutions Tables PDFDanielle WalkerNo ratings yet

- Modelling SolutionDocument45 pagesModelling SolutionLyricsical ViewerNo ratings yet

- MariottDocument6 pagesMariottJunaid SaleemNo ratings yet

- Purchases / Average Payables Revenue / Average Total AssetsDocument7 pagesPurchases / Average Payables Revenue / Average Total AssetstannuNo ratings yet

- BoeingDocument11 pagesBoeingPreksha GulatiNo ratings yet

- Adidas/Reebok Merger: Collin Shaw Kelly Truesdale Michael Rockette Benedikte Schmidt SaravanansadaiyappanDocument27 pagesAdidas/Reebok Merger: Collin Shaw Kelly Truesdale Michael Rockette Benedikte Schmidt SaravanansadaiyappanUdipta DasNo ratings yet

- S9 - XLS069-XLS-ENG MarriottDocument12 pagesS9 - XLS069-XLS-ENG MarriottCarlosNo ratings yet

- P25-15K Flow ChartDocument4 pagesP25-15K Flow ChartAvinash MuralaNo ratings yet

- Income Statement Balance Sheet Cash Flow Ratios FCFF Eva & Roic News Analysis 1 News Analysis 2Document9 pagesIncome Statement Balance Sheet Cash Flow Ratios FCFF Eva & Roic News Analysis 1 News Analysis 2ramarao1981No ratings yet

- RatioDocument11 pagesRatioAnant BothraNo ratings yet

- FedEx (FDX) Financial Ratios and Metrics - Stock AnalysisDocument2 pagesFedEx (FDX) Financial Ratios and Metrics - Stock AnalysisPilly PhamNo ratings yet

- Stock Screener203229Document3 pagesStock Screener203229Sde BdrNo ratings yet

- Leveraged Buyout Valuation and AnalysisDocument5 pagesLeveraged Buyout Valuation and AnalysisfutyNo ratings yet

- Hero Motocorp EvaDocument1 pageHero Motocorp EvaproNo ratings yet

- Lettuce ProductionDocument14 pagesLettuce ProductionJay ArNo ratings yet

- Maruti Suzuki Financial ModellingDocument8 pagesMaruti Suzuki Financial ModellingPooja AdhikariNo ratings yet

- FCF SolutionDocument6 pagesFCF SolutionMarium RazaNo ratings yet

- The Unidentified Industries - Residency - CaseDocument4 pagesThe Unidentified Industries - Residency - CaseDBNo ratings yet

- Ratio Analysis: Growth Ratios 2016Document3 pagesRatio Analysis: Growth Ratios 2016radulescuandrei100No ratings yet

- Projection and Valuation Example - SolutionDocument13 pagesProjection and Valuation Example - SolutionPrince Akonor AsareNo ratings yet

- Nike Inc. Cost of Capital DCF AnalysisDocument6 pagesNike Inc. Cost of Capital DCF AnalysisrizqighaniNo ratings yet

- Government Publications: Key PapersFrom EverandGovernment Publications: Key PapersBernard M. FryNo ratings yet

- GR 11 Accounting P1 (English) November 2022 Answer BookDocument9 pagesGR 11 Accounting P1 (English) November 2022 Answer BookDoryson CzzleNo ratings yet

- Business Management: Chapter 9Document2 pagesBusiness Management: Chapter 9Javier BallesterosNo ratings yet

- All NotebookDocument88 pagesAll NotebookmsjoyevangelistaNo ratings yet

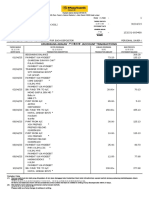

- Nurul Jannah Binti Rossli Stament Bank 2Document7 pagesNurul Jannah Binti Rossli Stament Bank 2nurul jannah rossliNo ratings yet

- Shareholder's Equity 2 - PracAccDocument19 pagesShareholder's Equity 2 - PracAccClyn CFNo ratings yet

- Ceat B - SDocument2 pagesCeat B - SRashesh GajeraNo ratings yet

- Strategic Financial ManagementDocument5 pagesStrategic Financial Managementranjitghosh684No ratings yet

- bcca-6-sem-company-law-and-secretarial-practice-5543-summer-2019Document2 pagesbcca-6-sem-company-law-and-secretarial-practice-5543-summer-2019kambleprathamesh008No ratings yet

- Accruals & Prepayment-1Document3 pagesAccruals & Prepayment-1Kopanang LeokanaNo ratings yet

- Dwnload Full Corporate Partnership Estate and Gift Taxation 2013 7th Edition Pratt Solutions Manual PDFDocument36 pagesDwnload Full Corporate Partnership Estate and Gift Taxation 2013 7th Edition Pratt Solutions Manual PDFlinzigaumond2915z100% (13)

- Part 6Document8 pagesPart 6Amr YoussefNo ratings yet

- Accounting For Special TransactionDocument5 pagesAccounting For Special TransactionNicole Gole CruzNo ratings yet

- FABM Q3 L5. SLEM 5 - W5 - 2S - Q3 - Books of AccountsDocument14 pagesFABM Q3 L5. SLEM 5 - W5 - 2S - Q3 - Books of AccountsSophia MagdaraogNo ratings yet

- Gr11 Acc P1 (English) November 2019 Marking GuidelinesDocument8 pagesGr11 Acc P1 (English) November 2019 Marking GuidelinesShriddhi MaharajNo ratings yet

- DeAngelo - 1990 - Equity Valuation and Corporate ControlDocument21 pagesDeAngelo - 1990 - Equity Valuation and Corporate ControlAna Luisa EisenlohrNo ratings yet

- A Comparative Study On Tata Consultancy Services LTD and Infosys LTD in The Information Technology IndustryDocument7 pagesA Comparative Study On Tata Consultancy Services LTD and Infosys LTD in The Information Technology IndustryDebasmita Pr RayNo ratings yet

- David Ruiz Tarea 12-13Document33 pagesDavid Ruiz Tarea 12-131006110950No ratings yet

- ICICI Prudential Balanced Advantage Fund - Hybrid Funds - Dynamic Asset Allocation FundDocument6 pagesICICI Prudential Balanced Advantage Fund - Hybrid Funds - Dynamic Asset Allocation FundSandeep JainNo ratings yet

- Net ProfitDocument2 pagesNet ProfitemprotNo ratings yet

- 3.2 Dual Nature of Merch BusDocument6 pages3.2 Dual Nature of Merch BusNAOL BIFTUNo ratings yet

- Speciality ChemicalsDocument32 pagesSpeciality ChemicalsKeshav KhetanNo ratings yet

- Fabm 1 SG 11 Q4 0905Document45 pagesFabm 1 SG 11 Q4 0905James Kirby CuervoNo ratings yet

- GCB - 2qcy23Document6 pagesGCB - 2qcy23gee.yeap3959No ratings yet

- Ias 33 Earning Per Share (Eps) Review Questions Question One (Basic EPS)Document7 pagesIas 33 Earning Per Share (Eps) Review Questions Question One (Basic EPS)Anjel JosephNo ratings yet

- CFAR Time Variation in The Equity Risk PremiumDocument16 pagesCFAR Time Variation in The Equity Risk Premiumpby5145No ratings yet

- Contract Drafting Assignment - ShreeyanshiDocument3 pagesContract Drafting Assignment - ShreeyanshiShreeyanshiNo ratings yet

- Stakeholder Objectives and Financial RatiosDocument2 pagesStakeholder Objectives and Financial RatiosSteven Patrick YuNo ratings yet

- A Presentation On CompanyDocument15 pagesA Presentation On CompanyanishNo ratings yet

- ASENSO RURAL BANK OF BAUTISTA INC - HTMDocument2 pagesASENSO RURAL BANK OF BAUTISTA INC - HTMJim De VegaNo ratings yet

- Tracking assets, liabilities, equity over timeDocument3 pagesTracking assets, liabilities, equity over timeSana LeeNo ratings yet