You might also like

- Asia Small and Medium-Sized Enterprise Monitor 2020: Volume I: Country and Regional ReviewsFrom EverandAsia Small and Medium-Sized Enterprise Monitor 2020: Volume I: Country and Regional ReviewsNo ratings yet

- Task 1 - Email Template v2Document2 pagesTask 1 - Email Template v2Mamata PatraNo ratings yet

- Task 1Document2 pagesTask 1Subhav GoyalNo ratings yet

- Task 1 - Email Template v2Document2 pagesTask 1 - Email Template v2zf8dkk8fnzNo ratings yet

- Task 1 - Email Template v2Document2 pagesTask 1 - Email Template v2Amardeep TayadeNo ratings yet

- Task 1 - Email Prepared by Nandhu PMDocument2 pagesTask 1 - Email Prepared by Nandhu PMNandhu PMNo ratings yet

- Potential M&A Targets From WorldWide BrewingDocument2 pagesPotential M&A Targets From WorldWide BrewinggogunikhilNo ratings yet

- Task 1 - Email Template v2Document2 pagesTask 1 - Email Template v2aKSHAT sHARMANo ratings yet

- Task 1 - Email Template v2Document2 pagesTask 1 - Email Template v2Hitesh NaikNo ratings yet

- IntershipDocument2 pagesIntershiparjunshinoj2002No ratings yet

- Task 1 - Email Model Answer v2Document2 pagesTask 1 - Email Model Answer v2Siddhant Aggarwal100% (1)

- Task 1Document2 pagesTask 1Aakash GuliaNo ratings yet

- ProjectDocument2 pagesProjectYash YashNo ratings yet

- Task 1 - Email Template v2Document2 pagesTask 1 - Email Template v2paragjindal703No ratings yet

- ProjectDocument2 pagesProjectYash YashNo ratings yet

- Task 1 - Email Template v2Document2 pagesTask 1 - Email Template v2sasta jiNo ratings yet

- To: From: Subject:: Spirit Bay RecommendDocument2 pagesTo: From: Subject:: Spirit Bay Recommendtony montanaNo ratings yet

- To: From: SubjectDocument2 pagesTo: From: SubjectMaxime JeanNo ratings yet

- Task 1 - Email Template v2Document2 pagesTask 1 - Email Template v2PriyanshulNo ratings yet

- Task 1Document4 pagesTask 1aNo ratings yet

- Task 1 - Email Template v2 PDFDocument2 pagesTask 1 - Email Template v2 PDFtannushokeen66No ratings yet

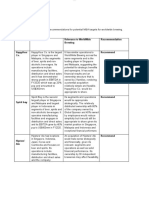

- Happy Hour Co.: Company Description Relevance RecommendationDocument2 pagesHappy Hour Co.: Company Description Relevance RecommendationMansi VermaNo ratings yet

- Task 1 ForageDocument2 pagesTask 1 ForageAditya KatareNo ratings yet

- Task 1 - Email Template v2Document2 pagesTask 1 - Email Template v2Study HardNo ratings yet

- Task 1 - EmailDocument2 pagesTask 1 - EmailIshrak ZamanNo ratings yet

- Happyhour Co. Recommend: To: From: SubjectDocument2 pagesHappyhour Co. Recommend: To: From: SubjectAyush ChandwaniNo ratings yet

- Task 1 - Email Template v2 WORLDWIDE BREWINGDocument2 pagesTask 1 - Email Template v2 WORLDWIDE BREWINGbilalzahid1969No ratings yet

- Task 1 - Email Template v2 - To Anna From Muhammad Ahmed Subject Potential M&Amp A Targets For - StudocuDocument1 pageTask 1 - Email Template v2 - To Anna From Muhammad Ahmed Subject Potential M&Amp A Targets For - Studocugannusingh1112No ratings yet

- To: From: SubjectDocument3 pagesTo: From: SubjectHephzibah LeannaNo ratings yet

- EmailDocument3 pagesEmailbhartisoni292No ratings yet

- Task 1 - Email Template v2Document2 pagesTask 1 - Email Template v2mohak guptaNo ratings yet

- Task 1 - SolutionDocument3 pagesTask 1 - SolutionJoan PujolNo ratings yet

- Task 1 - EmailDocument2 pagesTask 1 - EmailLouis P0% (1)

- Task 1Document2 pagesTask 1blobNo ratings yet

- Task 1 - Email Template v2Document3 pagesTask 1 - Email Template v2dkaisabekovNo ratings yet

- Email To AnnaDocument2 pagesEmail To AnnaShravan DeshmukhNo ratings yet

- Task 1 - Email Template v2Document2 pagesTask 1 - Email Template v2Chin Ying SiawNo ratings yet

- Task 1 Forage JPDocument2 pagesTask 1 Forage JPrevanth tNo ratings yet

- JPMorgan 1Document2 pagesJPMorgan 1ajayrajachoosNo ratings yet

- Task 1Document2 pagesTask 1Sire desireNo ratings yet

- Task 1 - Email Template v2Document2 pagesTask 1 - Email Template v2Stuti MathurNo ratings yet

- Task 1 Solution JP Morgan Investment Banking Virtual ExperienceDocument3 pagesTask 1 Solution JP Morgan Investment Banking Virtual ExperiencePiyush KumarNo ratings yet

- Task 1 - Email Template v2Document2 pagesTask 1 - Email Template v2IshitaNo ratings yet

- Task 1 - DavinDocument3 pagesTask 1 - Davindavin nathanNo ratings yet

- Task 1 - Email Template v2Document2 pagesTask 1 - Email Template v2李式奇No ratings yet

- Task 1 M&A (Aman Upadhyay)Document2 pagesTask 1 M&A (Aman Upadhyay)Aman UpadhyayNo ratings yet

- Task 1 - Email Template v2Document2 pagesTask 1 - Email Template v2Sakin KhanNo ratings yet

- To: From: SubjectDocument3 pagesTo: From: SubjectserisvsNo ratings yet

- Task 1 - Email Template v2Document2 pagesTask 1 - Email Template v2ashirwad modiNo ratings yet

- Carlos Johnson: To: From: SubjectDocument2 pagesCarlos Johnson: To: From: SubjectsukeshNo ratings yet

- Task 1 - Email Template v2Document2 pagesTask 1 - Email Template v2Jatin SinghNo ratings yet

- Task 1 - Email Template v2Document2 pagesTask 1 - Email Template v2AKANSHA100% (1)

- Task 1 - Email JP MorganDocument2 pagesTask 1 - Email JP MorganWilliam100% (1)

- JP Morgan IB TaskDocument2 pagesJP Morgan IB TaskDhanush JainNo ratings yet

- To Whom It May Concern, Below Is A Table Stating Recommendations For A Merger or Acquisition Deal For Worldwide Brewing CoDocument2 pagesTo Whom It May Concern, Below Is A Table Stating Recommendations For A Merger or Acquisition Deal For Worldwide Brewing Cokrishnavgupta74No ratings yet

- M&A TargetDocument2 pagesM&A Targetthomasenvrai2005No ratings yet

- Task 1Document3 pagesTask 1Soham AherNo ratings yet

- Task 1 - Email Template v2Document5 pagesTask 1 - Email Template v2Alberto Maroto ZamoranoNo ratings yet

- Task 1Document4 pagesTask 1Pratik WadgaonkarNo ratings yet

- Progress Test 3Document7 pagesProgress Test 3Mỹ Dung PntNo ratings yet

- Motion For Forensic Examination - Cyber CasedocxDocument5 pagesMotion For Forensic Examination - Cyber CasedocxJazz Tracey100% (1)

- (Your Business Name Here) - Safe Work Procedure Metal LatheDocument1 page(Your Business Name Here) - Safe Work Procedure Metal LatheSafety DeptNo ratings yet

- Some People Say That Having Jobs Can Be of Great Benefit To TeensDocument2 pagesSome People Say That Having Jobs Can Be of Great Benefit To Teensmaia sulavaNo ratings yet

- 7diesel 2016Document118 pages7diesel 2016JoãoCarlosDaSilvaBrancoNo ratings yet

- CFP The 17th International Computer Science and Engineering Conference (ICSEC 2013)Document1 pageCFP The 17th International Computer Science and Engineering Conference (ICSEC 2013)Davy SornNo ratings yet

- Assessment Task 2 2Document10 pagesAssessment Task 2 2Pratistha GautamNo ratings yet

- 1Document6 pages1Vignesh VickyNo ratings yet

- Oxy150 BrochureDocument2 pagesOxy150 BrochureSEC MachinesNo ratings yet

- Lecture 02 Running EnergyPlusDocument29 pagesLecture 02 Running EnergyPlusJoanne SiaNo ratings yet

- Plaxis Products 2010 EngDocument20 pagesPlaxis Products 2010 EngAri SentaniNo ratings yet

- LT32567 PDFDocument4 pagesLT32567 PDFNikolayNo ratings yet

- SafeShop Business Plan PDFDocument16 pagesSafeShop Business Plan PDFkalchati yaminiNo ratings yet

- PDFs/Sprinker NFPA 13/plan Review Sprinkler Checklist 13Document5 pagesPDFs/Sprinker NFPA 13/plan Review Sprinkler Checklist 13isbtanwir100% (1)

- 5c X-Tend FG Filter InstallationDocument1 page5c X-Tend FG Filter Installationfmk342112100% (1)

- Health Tech Industry Accounting Guide 2023Document104 pagesHealth Tech Industry Accounting Guide 2023sabrinaNo ratings yet

- Conceptual Framework For Financial Reporting: Student - Feedback@sti - EduDocument4 pagesConceptual Framework For Financial Reporting: Student - Feedback@sti - Eduwaeyo girlNo ratings yet

- SWP-10 Loading & Unloading Using Lorry & Mobile Crane DaimanDocument2 pagesSWP-10 Loading & Unloading Using Lorry & Mobile Crane DaimanHassan AbdullahNo ratings yet

- Door LockDocument102 pagesDoor LockNicolás BozzoNo ratings yet

- 115 Landslide Hazard PDFDocument5 pages115 Landslide Hazard PDFong0625No ratings yet

- American Bar Association American Bar Association JournalDocument6 pagesAmerican Bar Association American Bar Association JournalKarishma RajputNo ratings yet

- BOM For Solar Water PumpDocument11 pagesBOM For Solar Water PumpNirat PatelNo ratings yet

- Purchase Invoicing Guide AuDocument17 pagesPurchase Invoicing Guide AuYash VasudevaNo ratings yet

- Stanley Diamond Toward A Marxist AnthropologyDocument504 pagesStanley Diamond Toward A Marxist AnthropologyZachNo ratings yet

- S.No Company Name Location: Executive Packers and MoversDocument3 pagesS.No Company Name Location: Executive Packers and MoversAli KhanNo ratings yet

- Yrc1000 Options InstructionsDocument36 pagesYrc1000 Options Instructionshanh nguyenNo ratings yet

- Goran BULDIOSKI THINK TANKS IN CENTRAL AND EASTERN EUROPE AND THE QUALITY OF THEIR POLICY RESEARCHDocument31 pagesGoran BULDIOSKI THINK TANKS IN CENTRAL AND EASTERN EUROPE AND THE QUALITY OF THEIR POLICY RESEARCHCentre for Regional Policy Research and Cooperation StudiorumNo ratings yet

- Grundfosliterature 3081153Document120 pagesGrundfosliterature 3081153Cristian RinconNo ratings yet

- Tracer Survey Manual - Final 2Document36 pagesTracer Survey Manual - Final 2nesrusam100% (1)

- Mergers and Acquisitions in Pharmaceutical SectorDocument37 pagesMergers and Acquisitions in Pharmaceutical SectorAnjali Mehra100% (2)