You might also like

- Finance Act 2020 changes summaryDocument62 pagesFinance Act 2020 changes summaryhfdghdhNo ratings yet

- Finance Act 2020 - ACCA GlobalDocument65 pagesFinance Act 2020 - ACCA GlobalRaza AliNo ratings yet

- Equity Method: Amortization of Allocated ExcessDocument4 pagesEquity Method: Amortization of Allocated ExcesseiaNo ratings yet

- The Difference in Future Taxable AmountsDocument2 pagesThe Difference in Future Taxable AmountsThư LuyệnNo ratings yet

- Tugas Ch.20Document9 pagesTugas Ch.20Chupa HesNo ratings yet

- Rates of UK income tax for 2018-19 explained in 38 charactersDocument77 pagesRates of UK income tax for 2018-19 explained in 38 charactersSolongo DavaakhuuNo ratings yet

- Chapter 07 - Financial StatementsDocument40 pagesChapter 07 - Financial StatementsMkhonto XuluNo ratings yet

- Inheritance Tax, Part 2: Tax Liability On Lifetime TransfersDocument24 pagesInheritance Tax, Part 2: Tax Liability On Lifetime TransfershfdghdhNo ratings yet

- Part Time Salary Income and Total Income ComputationDocument7 pagesPart Time Salary Income and Total Income ComputationNipun AroraNo ratings yet

- CMPC 131 AnswerDocument5 pagesCMPC 131 AnswerKharen ValdezNo ratings yet

- 01 - Financial StatementsDocument6 pages01 - Financial Statementsjoubert andresNo ratings yet

- Income Statement and Statement of Financial Position for year ended 31 December 2020Document1 pageIncome Statement and Statement of Financial Position for year ended 31 December 2020prince matamboNo ratings yet

- JAWABAN ADVANCE 2 Intercompany TransactionsDocument6 pagesJAWABAN ADVANCE 2 Intercompany TransactionsDANIEL TEJANo ratings yet

- Karachi Institute Assignment 06Document8 pagesKarachi Institute Assignment 06Muhammad AdilNo ratings yet

- Financial Accounting Statements ExplainedDocument2 pagesFinancial Accounting Statements ExplainedPlawan GhimireNo ratings yet

- CAF 2 Spring 2021Document8 pagesCAF 2 Spring 2021Muhammad Ahsan RiazNo ratings yet

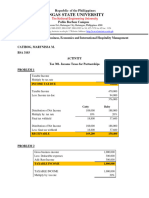

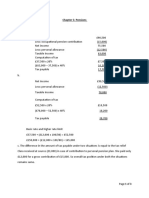

- Catibog, Marynissa M. - Activity On Income Taxes For PartnershipsDocument2 pagesCatibog, Marynissa M. - Activity On Income Taxes For PartnershipsMarynissa CatibogNo ratings yet

- Problem 18.5: Statement of Cash Flows, Direct and Indirect MethodsDocument1 pageProblem 18.5: Statement of Cash Flows, Direct and Indirect MethodsAnh BùiNo ratings yet

- ANSWER KEY Quiz On Tax On Compensation PDFDocument6 pagesANSWER KEY Quiz On Tax On Compensation PDFMeg CruzNo ratings yet

- Financial Ratio Analysis TutorialDocument6 pagesFinancial Ratio Analysis TutorialWEI QUAN LEENo ratings yet

- Notice of Assessment 2021 03 22 15 36 05 837221Document4 pagesNotice of Assessment 2021 03 22 15 36 05 837221Joseph HudsonNo ratings yet

- Cap Buget ProblemsDocument8 pagesCap Buget ProblemsramakrishnanNo ratings yet

- Income taxation and tax computationDocument6 pagesIncome taxation and tax computationJohn Victor Mancilla MonzonNo ratings yet

- Profits & Gains of Business or ProfessionDocument5 pagesProfits & Gains of Business or ProfessionAnushka BiswasNo ratings yet

- Basics Ltd - MemoDocument3 pagesBasics Ltd - Memoewriteandread.businessNo ratings yet

- Assignment No 02 Business Law and Taxation: Tauraira Arshad 16320 SolutionDocument2 pagesAssignment No 02 Business Law and Taxation: Tauraira Arshad 16320 SolutionSYEDA -No ratings yet

- Nokia Corporation: ISIN: FI0009000681 WKN: Nokia Asset Class: StockDocument2 pagesNokia Corporation: ISIN: FI0009000681 WKN: Nokia Asset Class: StockMohtasim Bin HabibNo ratings yet

- Financial Analysis For WorlducationDocument2 pagesFinancial Analysis For WorlducationParth PrajapatiNo ratings yet

- Income Taxes SolutionsDocument1 pageIncome Taxes SolutionsSleepy marshmallowNo ratings yet

- Solution To Module 1: Practice Problem Set #1Document1 pageSolution To Module 1: Practice Problem Set #1ArmandoNo ratings yet

- Taxation Assignment 1Document2 pagesTaxation Assignment 1Alviya FatimaNo ratings yet

- 3.1 Workshop 7 Capital Structure 2021Document2 pages3.1 Workshop 7 Capital Structure 2021bobhamilton3489No ratings yet

- Partnership Reviewer 2021Document78 pagesPartnership Reviewer 2021Miquel Villamarin100% (1)

- Lecture Notes - Financial Statement AnalysisDocument56 pagesLecture Notes - Financial Statement AnalysisRajnishKumarRohatgiNo ratings yet

- Questions - Cost of Capital and Sources of FinanceDocument3 pagesQuestions - Cost of Capital and Sources of Financepercy mapetereNo ratings yet

- Homework Chapter 22Document5 pagesHomework Chapter 22namhua54No ratings yet

- DeanDocument16 pagesDeanJames De TorresNo ratings yet

- Ques 3:: Less: Management Cost Add: Capital ExpenditureDocument2 pagesQues 3:: Less: Management Cost Add: Capital ExpenditurearunNo ratings yet

- Finance Act 2021 - ACCA GlobalDocument56 pagesFinance Act 2021 - ACCA GlobalhfdghdhNo ratings yet

- Model Solution: Page 1 of 6Document6 pagesModel Solution: Page 1 of 6ShuvonathNo ratings yet

- Solutions To Exercises P Class2-2022Document7 pagesSolutions To Exercises P Class2-2022Angel MéndezNo ratings yet

- Tax Calculator AY 2021-22Document1 pageTax Calculator AY 2021-22mehedi hasanNo ratings yet

- Amended Tax Credit Certificate 2022: 9371000KA Pps NoDocument2 pagesAmended Tax Credit Certificate 2022: 9371000KA Pps NoJose ArevaloNo ratings yet

- Revision Questions - CH 17 - SolutionsDocument4 pagesRevision Questions - CH 17 - SolutionsMinh ThưNo ratings yet

- BookDocument1 pageBookHealt FitNo ratings yet

- Midterm Problem - DocmDocument2 pagesMidterm Problem - Docmpippen venegasNo ratings yet

- Accounting For Income TaxDocument3 pagesAccounting For Income TaxDaniel Kahn GillamacNo ratings yet

- Calculating Income Tax ExpenseDocument21 pagesCalculating Income Tax ExpenseDhiananda zhuNo ratings yet

- Safari - 12 Aug 2019 at 1:00 PM PDFDocument1 pageSafari - 12 Aug 2019 at 1:00 PM PDFPauline BiancaNo ratings yet

- Chapter 2 - SolutionDocument12 pagesChapter 2 - SolutionAk AlNo ratings yet

- Revision Questions - CH 17 - QuestionsDocument3 pagesRevision Questions - CH 17 - QuestionsMinh ThưNo ratings yet

- Salaries Tax / Personal Assessment: Allowances, Deductions and Tax Rate TableDocument1 pageSalaries Tax / Personal Assessment: Allowances, Deductions and Tax Rate TableMaria PapNo ratings yet

- TK4 AkuntasniDocument7 pagesTK4 AkuntasniSarah NurfadilahNo ratings yet

- Assignment 4 - SolutionsDocument2 pagesAssignment 4 - SolutionsstoryNo ratings yet

- Chapter 5: Pensions Question 5.1-AnswerDocument3 pagesChapter 5: Pensions Question 5.1-AnswerAk AlNo ratings yet

- Sample Payroll Edited r6Document17 pagesSample Payroll Edited r6Regie DayritNo ratings yet

- Financial Accounting Statement of Cash FlowsDocument4 pagesFinancial Accounting Statement of Cash FlowsPlawan GhimireNo ratings yet

- Taxation AssessmentDocument8 pagesTaxation AssessmentBhanumati BhunjunNo ratings yet

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- Understanding IFRS Fundamentals: International Financial Reporting StandardsFrom EverandUnderstanding IFRS Fundamentals: International Financial Reporting StandardsNo ratings yet

- Grade 9: International Junior Math OlympiadDocument13 pagesGrade 9: International Junior Math OlympiadLong Văn Trần100% (1)

- Document PDFDocument16 pagesDocument PDFnelson_herreraNo ratings yet

- Chem 6AL Syllabus Winter 2021Document5 pagesChem 6AL Syllabus Winter 2021John SmithNo ratings yet

- Conciliar Post Reference GuideDocument9 pagesConciliar Post Reference GuideBenjamin WinterNo ratings yet

- Laughing at Heads in the CloudsDocument2 pagesLaughing at Heads in the Cloudsmatfox2No ratings yet

- Juice in PakistanDocument9 pagesJuice in Pakistanrize1159100% (1)

- QuestionnaireDocument15 pagesQuestionnaireNaveen GunasekaranNo ratings yet

- 07 - Toshkov (2016) Theory in The Research ProcessDocument29 pages07 - Toshkov (2016) Theory in The Research ProcessFerlanda LunaNo ratings yet

- Dzone Trend Report Containers 2021Document52 pagesDzone Trend Report Containers 2021Diacamo MankungiNo ratings yet

- Medicard Phil Inc. vs. CIRDocument2 pagesMedicard Phil Inc. vs. CIRhigoremso giensdksNo ratings yet

- 03 IoT Technical Sales Training Industrial Wireless Deep DiveDocument35 pages03 IoT Technical Sales Training Industrial Wireless Deep Divechindi.comNo ratings yet

- Magh Bihu or Maghar DomahiDocument8 pagesMagh Bihu or Maghar Domahihackdarenot4No ratings yet

- Density Functional Theory Investigations of Bismuth VanadateDocument7 pagesDensity Functional Theory Investigations of Bismuth VanadateNurSalahuddinNo ratings yet

- FTI-Forming SuiteDocument2 pagesFTI-Forming SuiteMithun RajuNo ratings yet

- CPSC5125 - Assignment 3 - Fall 2014 Drawing Polygons: DescriptionDocument2 pagesCPSC5125 - Assignment 3 - Fall 2014 Drawing Polygons: DescriptionJo KingNo ratings yet

- Bankruptcy Judge Imposes Sanctions On CounselDocument17 pagesBankruptcy Judge Imposes Sanctions On Counsel83jjmackNo ratings yet

- TELENGANA BUSINESS DIRECTORY PENEL D-PanelDocument65 pagesTELENGANA BUSINESS DIRECTORY PENEL D-Panelamandeep100% (4)

- Micro-Finance: 16 Principles of Grameen BankDocument5 pagesMicro-Finance: 16 Principles of Grameen BankHomiyar TalatiNo ratings yet

- B&A Performance AnalysisDocument16 pagesB&A Performance AnalysisNathalia Caroline100% (1)

- Mena Vat 2018Document32 pagesMena Vat 2018Mukesh SharmaNo ratings yet

- Mental Health and Mental Disorder ReportDocument6 pagesMental Health and Mental Disorder ReportBonJovi Mojica ArtistaNo ratings yet

- Explosive Ordnance Disposal & Canine Group Regional Explosive Ordnance Disposal and Canine Unit 3Document1 pageExplosive Ordnance Disposal & Canine Group Regional Explosive Ordnance Disposal and Canine Unit 3regional eodk9 unit3No ratings yet

- Gold V Essex CCDocument11 pagesGold V Essex CCZACHARIAH MANKIRNo ratings yet

- Types of EquityDocument2 pagesTypes of EquityPrasanthNo ratings yet

- Three Days To SeeDocument2 pagesThree Days To SeeMae MejaresNo ratings yet

- 47 Syeda Nida Batool Zaidi-1Document10 pages47 Syeda Nida Batool Zaidi-1Eiman ShahzadNo ratings yet

- Midea R410A T3 50Hz Split Type Top-Dishcharge Series Technical Manual - V201707Document157 pagesMidea R410A T3 50Hz Split Type Top-Dishcharge Series Technical Manual - V201707kaleabNo ratings yet

- 201335688Document60 pages201335688The Myanmar TimesNo ratings yet

- Ken Scott - Metal BoatsDocument208 pagesKen Scott - Metal BoatsMaxi Sie100% (3)

- Tugas B.INGGRIS ALANDocument4 pagesTugas B.INGGRIS ALANAlan GunawanNo ratings yet