You might also like

- Stage AnalysisDocument12 pagesStage Analysisanalyst_anil14100% (4)

- Attempt History: Due Mar 16 at 19:45 Available Mar 16 at 17:45 - Mar 16 at 19:45 1 / 1 PtsDocument5 pagesAttempt History: Due Mar 16 at 19:45 Available Mar 16 at 17:45 - Mar 16 at 19:45 1 / 1 PtsmlaNo ratings yet

- Sundaram Global Brand FundDocument8 pagesSundaram Global Brand FundArmstrong CapitalNo ratings yet

- Financial Markets Case Study With AnswersDocument2 pagesFinancial Markets Case Study With AnswersShashi Kumar C G83% (12)

- World of Oil Derivatives A Guide To Financial Oil Trading in A ModernDocument305 pagesWorld of Oil Derivatives A Guide To Financial Oil Trading in A ModernfactknowledgebysatyaNo ratings yet

- Fibonacci StudiesDocument15 pagesFibonacci Studiesupendra1616No ratings yet

- Global State of Crypto in 2022 by GeminiDocument27 pagesGlobal State of Crypto in 2022 by GeminiTrader CatNo ratings yet

- The 10 Keys To Successful TradingDocument16 pagesThe 10 Keys To Successful TradingRajni Kant JaiswalNo ratings yet

- 14 - Safety Resilience As New Safety Thinking (USAHID) - 150720 PDFDocument77 pages14 - Safety Resilience As New Safety Thinking (USAHID) - 150720 PDFawan syafrieNo ratings yet

- t3l Trading 101 Foundation CourseDocument170 pagest3l Trading 101 Foundation CourseSubhash Dhakar100% (1)

- Chapter 7 - Principles of Marketing 2023Document43 pagesChapter 7 - Principles of Marketing 2023nosiphokhanyile85No ratings yet

- Project Iv Sem MbaDocument37 pagesProject Iv Sem MbaLaeeq Ur RahmanNo ratings yet

- IPOs InternationalDocument10 pagesIPOs Internationalpoket 3337No ratings yet

- January December 2018 Table 2 Top 12Document1 pageJanuary December 2018 Table 2 Top 12AprilMartelNo ratings yet

- Portfolio ContempDocument12 pagesPortfolio ContempJim Russel SangilNo ratings yet

- Indonesia'S Capital Market Updates: Akhmad NuranyantoDocument35 pagesIndonesia'S Capital Market Updates: Akhmad NuranyantoSiti Hutami pratiwiNo ratings yet

- DLA Piper - Global - Telehealth - Guide - November 2020Document145 pagesDLA Piper - Global - Telehealth - Guide - November 2020lPiNGUSlNo ratings yet

- Will India Become An Economic Superpower, Does It Matter & What Might Prevent It?Document38 pagesWill India Become An Economic Superpower, Does It Matter & What Might Prevent It?Yashvi TanejaNo ratings yet

- Country Risk Damodaran-AnalysisDocument42 pagesCountry Risk Damodaran-AnalysisSantiago GómezNo ratings yet

- Resultados WoS n57 Tudo + International Business e Global Value ChainDocument20 pagesResultados WoS n57 Tudo + International Business e Global Value Chainjohn doeNo ratings yet

- Acf 2008Document8 pagesAcf 2008Stephan_Burklin1559No ratings yet

- RI Impact of COVID 19 ReportDocument22 pagesRI Impact of COVID 19 ReportSuraj DixitNo ratings yet

- TS - MSCI Indonesia Nov-21 Rebalancing PreviewDocument6 pagesTS - MSCI Indonesia Nov-21 Rebalancing PreviewAdri KhosasihNo ratings yet

- REIT FundsDocument8 pagesREIT FundsArmstrong CapitalNo ratings yet

- Assignment-2 Technomgt TrinathDocument2 pagesAssignment-2 Technomgt TrinathTrinath OjhaNo ratings yet

- Slides Reuters Report 2022Document232 pagesSlides Reuters Report 2022Cristobal FlorenzanoNo ratings yet

- Components of International BusinessDocument39 pagesComponents of International BusinessBramaNo ratings yet

- ObamaDocument23 pagesObamashubhamNo ratings yet

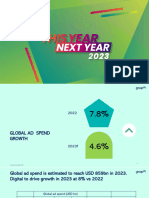

- GROUPM TYNY Report 2023Document10 pagesGROUPM TYNY Report 2023Raghunath ASNo ratings yet

- EIAA Digital Families 2008 Executive Summary: Family Time OnlineDocument7 pagesEIAA Digital Families 2008 Executive Summary: Family Time OnlinegessamiNo ratings yet

- Climate Change (POLIGON)Document16 pagesClimate Change (POLIGON)Nurdayanti SNo ratings yet

- IADC - SPE International Drilling Conference Digital ProgramDocument50 pagesIADC - SPE International Drilling Conference Digital ProgrammaicrvNo ratings yet

- Materi BEI 12 Oktober 2022Document25 pagesMateri BEI 12 Oktober 2022Delila Sr.No ratings yet

- Who Is Developed? Who Is Developing: Measurement Problems of DevelopmentDocument42 pagesWho Is Developed? Who Is Developing: Measurement Problems of DevelopmentcopabNo ratings yet

- 2022 Quiz BeeDocument27 pages2022 Quiz BeepatrimoniomicaNo ratings yet

- Deals in India: Annual Review and Outlook For 2021: December 2020Document14 pagesDeals in India: Annual Review and Outlook For 2021: December 2020Nairit MondalNo ratings yet

- 2014 Ranking of Countries For Mining InvestmentDocument10 pages2014 Ranking of Countries For Mining InvestmentmaggioraNo ratings yet

- 1Document6 pages1PhamDKNo ratings yet

- Reference Chapter 2Document29 pagesReference Chapter 2henry CanlasNo ratings yet

- Indian Economics and Foreign Trade Policy Project - Priodarshini LahiriDocument7 pagesIndian Economics and Foreign Trade Policy Project - Priodarshini LahiriDebasmita LahiriNo ratings yet

- Sales Seller Report 2021 - XTXDocument2 pagesSales Seller Report 2021 - XTXHuy Anh HoangNo ratings yet

- 2018 Global R D Funding ForecastDocument43 pages2018 Global R D Funding ForecastYU DANNI / UPMNo ratings yet

- PKT Sir India SuperpowerDocument38 pagesPKT Sir India SuperpowerShraman BanerjeeNo ratings yet

- Innovative Products in International MarketDocument26 pagesInnovative Products in International MarketemaadpatelNo ratings yet

- India 2050 Global Super Power PresentationDocument13 pagesIndia 2050 Global Super Power PresentationlezendNo ratings yet

- 5 City Sectors vs. London Boundary - PRIZM - Environment - Transport - Central LondonDocument11 pages5 City Sectors vs. London Boundary - PRIZM - Environment - Transport - Central London7k6y86z5h8No ratings yet

- WHEATDocument17 pagesWHEATAltaf HussainNo ratings yet

- Management 0002222Document13 pagesManagement 0002222qwer11No ratings yet

- Medical Equipment Inc AmaalDocument4 pagesMedical Equipment Inc AmaalAlaa HamdanNo ratings yet

- How To Identify Business - Opportunities - Daniel - Lagos - June7Document33 pagesHow To Identify Business - Opportunities - Daniel - Lagos - June7Olufela Yomi-LayinkaNo ratings yet

- The Philippine Chemical Industry ProfileDocument7 pagesThe Philippine Chemical Industry ProfileEddie Resurreccion Jr.No ratings yet

- Scheme C - Tier I - 0Document1 pageScheme C - Tier I - 0Kumar AlokNo ratings yet

- 2022 Uce Statement of Release - AmendedDocument8 pages2022 Uce Statement of Release - Amendedsam lubakeneNo ratings yet

- DIY InvestingDocument2 pagesDIY Investingsommer_ronald5741No ratings yet

- 17 - The Role of OHS Expert in The Development of Health & Halal Industry (UNIDA) - 300820Document50 pages17 - The Role of OHS Expert in The Development of Health & Halal Industry (UNIDA) - 300820Dedy ChemistNo ratings yet

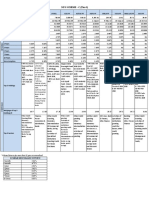

- Table 1: National Venture Capital Pools in Asia by Country and Year, in Billions of U.S. DollarsDocument26 pagesTable 1: National Venture Capital Pools in Asia by Country and Year, in Billions of U.S. DollarsoshimaxNo ratings yet

- New Infographic 2019 enDocument15 pagesNew Infographic 2019 enMinas KhatchadourianNo ratings yet

- Investment Promotion, Strategies, Policies and Practices - Malaysia'S ExperienceDocument33 pagesInvestment Promotion, Strategies, Policies and Practices - Malaysia'S ExperienceGeremew Kefale GobenaNo ratings yet

- 2017YouthWellbeingIndex PDFDocument184 pages2017YouthWellbeingIndex PDFManasviJindalNo ratings yet

- Sec C - Group 04 - IBE - Assignment 3Document6 pagesSec C - Group 04 - IBE - Assignment 3Vipul GhaiNo ratings yet

- BNI Sekuritas 08102021Document14 pagesBNI Sekuritas 08102021Quartantyo WijanarkoNo ratings yet

- World Is Open For BusinessDocument37 pagesWorld Is Open For BusinessSajjad HussainNo ratings yet

- The World Is Open For Business. Yours.: An Overview of The U.S. Commercial ServiceDocument37 pagesThe World Is Open For Business. Yours.: An Overview of The U.S. Commercial ServiceSyaibatul HamdiNo ratings yet

- Life Expectancy and Economic Well-Being in Nigeria 1234Document24 pagesLife Expectancy and Economic Well-Being in Nigeria 1234Chisom IbezimNo ratings yet

- nCoV Presentations (Consolidated)Document194 pagesnCoV Presentations (Consolidated)R'mon Ian Castro SantosNo ratings yet

- Final Suggestion RMG BusinessDocument5 pagesFinal Suggestion RMG BusinessMoniruzzamanNo ratings yet

- Investment Analysis.Document11 pagesInvestment Analysis.Eric AwinoNo ratings yet

- Country ReviewCote d'Ivoire: A CountryWatch PublicationFrom EverandCountry ReviewCote d'Ivoire: A CountryWatch PublicationNo ratings yet

- Country ReviewSolomon Islands: A CountryWatch PublicationFrom EverandCountry ReviewSolomon Islands: A CountryWatch PublicationNo ratings yet

- 1 Handout - Intro To FM PDFDocument84 pages1 Handout - Intro To FM PDFFaith BariasNo ratings yet

- Impact of FII's On Indian Mutual FundsDocument57 pagesImpact of FII's On Indian Mutual FundsAadil KakarNo ratings yet

- CLI Components and Turning PointsDocument52 pagesCLI Components and Turning PointsSijia JiangNo ratings yet

- MNJMN RetailDocument8 pagesMNJMN Retail067Rafli Faiz AqmalNo ratings yet

- 2023 Annual US VC Valuations ReportDocument28 pages2023 Annual US VC Valuations ReportJuan LNo ratings yet

- NISM Chap 2Document14 pagesNISM Chap 2Amarjeet SinghNo ratings yet

- International FinanceDocument252 pagesInternational FinanceARUNSANKAR NNo ratings yet

- International Financial Management Eun Resnick 5th Edition Test BankDocument3 pagesInternational Financial Management Eun Resnick 5th Edition Test BankLisa Beighley100% (35)

- TanishChaudhary InternshalaResumeDocument2 pagesTanishChaudhary InternshalaResumeTanish ChaudharyNo ratings yet

- Minutes of The Extraordinary Meeting of The Board of DirectorsDocument9 pagesMinutes of The Extraordinary Meeting of The Board of DirectorsUsiminas_RINo ratings yet

- Investment in The Era of Unintended Bets: Joseph Mezrich Nomura Securities International, IncDocument23 pagesInvestment in The Era of Unintended Bets: Joseph Mezrich Nomura Securities International, IncblacksmithMGNo ratings yet

- Statement 1700313960560Document28 pagesStatement 1700313960560Arun MuniNo ratings yet

- Bali, T. G., Cakici, N., Fabozzi, F. J., & Goyal, G. (2014) - Practical Applications of Book-To-Market and The Cross-Section of Expected Returns in International Stock Markets.Document6 pagesBali, T. G., Cakici, N., Fabozzi, F. J., & Goyal, G. (2014) - Practical Applications of Book-To-Market and The Cross-Section of Expected Returns in International Stock Markets.firebirdshockwaveNo ratings yet

- IDFC Infrastructure Bond Tranche 3 Application Form 2012Document8 pagesIDFC Infrastructure Bond Tranche 3 Application Form 2012Prajna CapitalNo ratings yet

- Emerging Markets Sovereign Strategy Daily: Implications of The Package On Asset Prices and The CurveDocument6 pagesEmerging Markets Sovereign Strategy Daily: Implications of The Package On Asset Prices and The CurveAlex DiazNo ratings yet

- Third Eye CM BrochureDocument22 pagesThird Eye CM Brochureabc testerNo ratings yet

- Understanding Financial Management: A Practical Guide: Guideline Answers To The Concept Check QuestionsDocument11 pagesUnderstanding Financial Management: A Practical Guide: Guideline Answers To The Concept Check QuestionsManuel BoahenNo ratings yet

- Fed Monetary Policy Report March 2023Document71 pagesFed Monetary Policy Report March 2023Tim MooreNo ratings yet

- Tfef One Pager Nov 2019 PDFDocument2 pagesTfef One Pager Nov 2019 PDFABDUL MALIKNo ratings yet

- Analisis Laporan Keuangan PT. Goodyear Indonesia TBK TAHUN 2016 DAN 2017Document34 pagesAnalisis Laporan Keuangan PT. Goodyear Indonesia TBK TAHUN 2016 DAN 2017Tri AmbarNo ratings yet

- WEIR011258 SuperCrypto 3 Online Report 010621Document5 pagesWEIR011258 SuperCrypto 3 Online Report 010621Bill100% (1)