You might also like

- 44 Bed Detox and Residential Substance Abuse Treatment Facility Proforma - Chapman TustinDocument4 pages44 Bed Detox and Residential Substance Abuse Treatment Facility Proforma - Chapman TustinDaniel L. Case, Sr.100% (2)

- Transfer and Business Taxes Solutions Manual Tabag Garcia 3rd Edition PDF FreeDocument39 pagesTransfer and Business Taxes Solutions Manual Tabag Garcia 3rd Edition PDF FreePHILLIT CLASS100% (1)

- Using and Introducing Precision MaintenanceDocument13 pagesUsing and Introducing Precision MaintenanceTofan NugrohoNo ratings yet

- Final Dossier IndexDocument2 pagesFinal Dossier IndexTadaya Kasahara50% (2)

- Sundaram Global Brand FundDocument8 pagesSundaram Global Brand FundArmstrong CapitalNo ratings yet

- National Institute of Textile Engineering & Research (Niter)Document100 pagesNational Institute of Textile Engineering & Research (Niter)Mir MD. Musa Ali RezaNo ratings yet

- Strategic Management - IBMDocument20 pagesStrategic Management - IBMPaulArsenieNo ratings yet

- Finance Detective - Rizqi Ghani Faturrahman - 29120382 - YP-64BDocument4 pagesFinance Detective - Rizqi Ghani Faturrahman - 29120382 - YP-64BrizqighaniNo ratings yet

- Statista Report b2b e CommerceDocument103 pagesStatista Report b2b e CommercebNo ratings yet

- Boq Kediri Blawe 3Document34 pagesBoq Kediri Blawe 3Riko ArtsNo ratings yet

- FOREX TRADING - BUY & SELL STRATEGY - All in One eBOOK PDFDocument46 pagesFOREX TRADING - BUY & SELL STRATEGY - All in One eBOOK PDFEmmanuel TemiloluwaNo ratings yet

- Financial Markets (Chapter 6)Document2 pagesFinancial Markets (Chapter 6)Kyla DayawonNo ratings yet

- Nestle Supply ChainDocument9 pagesNestle Supply ChainVedant DeshpandeNo ratings yet

- S&P 500 Earnings Dashboard - Dec. 6Document11 pagesS&P 500 Earnings Dashboard - Dec. 6Anonymous V7Ozz1wnNo ratings yet

- UK Short Mobile 2008Document22 pagesUK Short Mobile 2008solo12344322No ratings yet

- WG Sub Pvtsec MSMEDocument40 pagesWG Sub Pvtsec MSMEVineet SärøjNo ratings yet

- Assessment - Graduates in 2016 - Lu DRDocument29 pagesAssessment - Graduates in 2016 - Lu DRDamien RibonNo ratings yet

- FM - Group 1 - DixonDocument31 pagesFM - Group 1 - DixonJayash KaushalNo ratings yet

- Ifma Om Webinar 1Document58 pagesIfma Om Webinar 1Abu Jamal Mohd FirdausNo ratings yet

- AnalysisDocument5 pagesAnalysisBeugh RiveraNo ratings yet

- Americká Výsledková SezónaDocument12 pagesAmerická Výsledková SezónatomasberanekNo ratings yet

- Accenture-Unlocking-Digital-Value-South Africa-Telecoms-Sector PDFDocument26 pagesAccenture-Unlocking-Digital-Value-South Africa-Telecoms-Sector PDFadityaNo ratings yet

- Analysis IDocument4 pagesAnalysis IBeugh RiveraNo ratings yet

- Value DataDocument41 pagesValue DataWendy FernándezNo ratings yet

- To Reduce Non-Productive Time in Garment IndustryDocument5 pagesTo Reduce Non-Productive Time in Garment Industryabebe adgoNo ratings yet

- Operations ManagementDocument2 pagesOperations ManagementArooj HectorNo ratings yet

- LN1 - Introduction To Industrial AutomationDocument44 pagesLN1 - Introduction To Industrial Automationmeen87No ratings yet

- (In $ Million) : WHX Corporation (WHX)Document3 pages(In $ Million) : WHX Corporation (WHX)Amit JainNo ratings yet

- Product Recall Solutions For Automotive Component Suppliers-11-2014Document8 pagesProduct Recall Solutions For Automotive Component Suppliers-11-2014The PhongNo ratings yet

- Caso 1Document28 pagesCaso 1Daniel CalderónNo ratings yet

- AIA - Part 2Document2 pagesAIA - Part 2Vinay ShahNo ratings yet

- 1 PDFDocument41 pages1 PDFJebin JamesNo ratings yet

- PostAnalytics RamziAljilany 7135857125561401344Document3 pagesPostAnalytics RamziAljilany 7135857125561401344RAMZI ALJILANYNo ratings yet

- Basic Business Statistics 13th Edition Berenson Solutions ManualDocument26 pagesBasic Business Statistics 13th Edition Berenson Solutions ManualJoshuaMartinezmqjp100% (57)

- FEDERAL RESERVE Statistical Release: For Release at 9:15 A.M. (EDT) April 16, 2024Document19 pagesFEDERAL RESERVE Statistical Release: For Release at 9:15 A.M. (EDT) April 16, 2024andre.torresNo ratings yet

- Consumer Behaviour in Selecting Mobile PhonesDocument24 pagesConsumer Behaviour in Selecting Mobile PhonesPriyank_Vishar_470No ratings yet

- S&P 500 Earnings Scorecard: Proprietary ResearchDocument11 pagesS&P 500 Earnings Scorecard: Proprietary ResearchWill AdefehintiNo ratings yet

- 2-1 Audit Report 2019 For SPV TrainingDocument20 pages2-1 Audit Report 2019 For SPV Training'Bernard Fernando Xav Monroe'No ratings yet

- TelecomDocument8 pagesTelecomVaibhav JainNo ratings yet

- AIA - Part 1Document5 pagesAIA - Part 1Vinay ShahNo ratings yet

- JTC Quarterly Market Report For 1Q2022Document45 pagesJTC Quarterly Market Report For 1Q2022MingYaoNo ratings yet

- Data For Ratio Detective ExerciseDocument1 pageData For Ratio Detective ExercisemaritaputriNo ratings yet

- Profile For Coir Fiber or Dust Moulding UnitDocument7 pagesProfile For Coir Fiber or Dust Moulding UnitAnandh SharavanNo ratings yet

- Impact of Global Recession On InformatioDocument7 pagesImpact of Global Recession On InformatioRishabh SangariNo ratings yet

- Full Download Basic Business Statistics 13th Edition Berenson Solutions ManualDocument36 pagesFull Download Basic Business Statistics 13th Edition Berenson Solutions Manualjosephefwebb100% (23)

- Project Information SO-33011 1. Sample Identification: Test Report For Sieve Analysis ASTM D-422Document1 pageProject Information SO-33011 1. Sample Identification: Test Report For Sieve Analysis ASTM D-422civillabNo ratings yet

- 10.716633 2 2711Document15 pages10.716633 2 2711Frank Joel Herrera ApaesteguiNo ratings yet

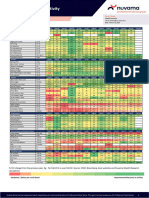

- Economic Spotlight - Nuvama ReportDocument8 pagesEconomic Spotlight - Nuvama Reportsonika.arora1417No ratings yet

- Crowe Horwath 2013 Hotel Survey ResultsDocument2 pagesCrowe Horwath 2013 Hotel Survey ResultsVassos KoutsioundasNo ratings yet

- Design, Fabrication and Performance Evaluation of A Maize ShellerDocument13 pagesDesign, Fabrication and Performance Evaluation of A Maize ShellerPeter AjewoleNo ratings yet

- Zero Waste Policy For Municipal Solid Waste in TaiwanoTHBDocument5 pagesZero Waste Policy For Municipal Solid Waste in TaiwanoTHBjoshlamNo ratings yet

- Equity Portfolio SGDocument208 pagesEquity Portfolio SGdharmendra_kanthariaNo ratings yet

- Month-to-Date: Index MTD 3M YTD 12MDocument4 pagesMonth-to-Date: Index MTD 3M YTD 12MEric ReyesNo ratings yet

- Bhopal Report - May 16 - 20160613Document17 pagesBhopal Report - May 16 - 20160613V. GopichandNo ratings yet

- S Curve Dilg Laguna OfficeDocument1 pageS Curve Dilg Laguna OfficeJohn Miguel FloraNo ratings yet

- An Entity Has The Following Operating Segments For The Year Ended 30 June 2018Document4 pagesAn Entity Has The Following Operating Segments For The Year Ended 30 June 2018Anas AjwadNo ratings yet

- Full Report 1Document10 pagesFull Report 1Kajune ChithilaphaNo ratings yet

- The Unidentified Industries - Residency - CaseDocument4 pagesThe Unidentified Industries - Residency - CaseDBNo ratings yet

- BOPP AdhesiveDocument8 pagesBOPP AdhesivePuneet AgarwalNo ratings yet

- Merrill Lynch TMT Conference: Robert Lerwill, Group Ceo Robert Lerwill, Group Ceo Tuesday 3 June 2008Document13 pagesMerrill Lynch TMT Conference: Robert Lerwill, Group Ceo Robert Lerwill, Group Ceo Tuesday 3 June 2008N2OMNo ratings yet

- Industryweekwebinaraug252020v10pdfdownload1598361464248 PDFDocument38 pagesIndustryweekwebinaraug252020v10pdfdownload1598361464248 PDFRUDY VOGELNo ratings yet

- Kotak Consolidated Earnings EstimatesDocument50 pagesKotak Consolidated Earnings EstimatesAnkit JainNo ratings yet

- Current Status of Industry Issues and ChallengesDocument38 pagesCurrent Status of Industry Issues and ChallengesHimanshiNo ratings yet

- Transformation and Insurance Growth in Nigeriav0.3Document15 pagesTransformation and Insurance Growth in Nigeriav0.3Rishi ReshamwalaNo ratings yet

- Redington India A LTDDocument9 pagesRedington India A LTDNagarajan GNo ratings yet

- HotelDocument55 pagesHotelcarolNo ratings yet

- i4482eDocument11 pagesi4482eFarhan WasimNo ratings yet

- Chemistry Optional 78cfc1e5Document7 pagesChemistry Optional 78cfc1e5Farhan WasimNo ratings yet

- SPF 2018 Grant Papers Revisiting The Past and Unveiling The Gendered LegacyDocument32 pagesSPF 2018 Grant Papers Revisiting The Past and Unveiling The Gendered LegacyFarhan WasimNo ratings yet

- CASE STUDY by Apala MishraDocument1 pageCASE STUDY by Apala MishraFarhan WasimNo ratings yet

- Export And/or Import: Evidence 8Document4 pagesExport And/or Import: Evidence 8Luis Enrique Hernandez RodriguezNo ratings yet

- SBI Life - Smart Platina Plus - Policy Document - Website Upload - 628Document73 pagesSBI Life - Smart Platina Plus - Policy Document - Website Upload - 628SUNEET KUMARNo ratings yet

- 10 1108 - Ebr 03 2022 0051Document28 pages10 1108 - Ebr 03 2022 0051Solihin SolihinNo ratings yet

- GST 307Document300 pagesGST 307Lawal OlanrewajuNo ratings yet

- Final exam.QT Chiến LượcDocument19 pagesFinal exam.QT Chiến LượcSnow NhiNo ratings yet

- 08 Bond InvestmentDocument3 pages08 Bond InvestmentAllegria Alamo100% (1)

- LMM Jjs PPT 2a Basics of LeanDocument116 pagesLMM Jjs PPT 2a Basics of LeanAby Reji ChemmathuNo ratings yet

- Unit - X (Macro Economics)Document15 pagesUnit - X (Macro Economics)Omisha SinghNo ratings yet

- Lesson 3 Customer Relationship ManagementDocument36 pagesLesson 3 Customer Relationship ManagementKyla Mae Fulache LevitaNo ratings yet

- The Directors ReportDocument1 pageThe Directors ReportTENDEKAI MASOKANo ratings yet

- Consumer Information:: Name: Date of Birth: GenderDocument3 pagesConsumer Information:: Name: Date of Birth: GendermohitNo ratings yet

- Logistics 1Document36 pagesLogistics 1Quỳnh Nguyễn NhưNo ratings yet

- Comparative Vs Absolute AdvantageDocument9 pagesComparative Vs Absolute AdvantageJayesh Kumar YadavNo ratings yet

- Evonik Company Presentation (January 2018)Document94 pagesEvonik Company Presentation (January 2018)Yang Sunman100% (1)

- Women I Deposit Account (Zehrah)Document2 pagesWomen I Deposit Account (Zehrah)kefiyalew BNo ratings yet

- IFRA Final Exam Write-UpDocument2 pagesIFRA Final Exam Write-UpHealth ResultsNo ratings yet

- Sdo Batangas: Department of EducationDocument10 pagesSdo Batangas: Department of EducationJomarie LagosNo ratings yet

- School Based Assessment: To Assess The Cause and Effects of Inflation On Small Businesses in The Greater Portmore RegionDocument22 pagesSchool Based Assessment: To Assess The Cause and Effects of Inflation On Small Businesses in The Greater Portmore RegionOniel BryanNo ratings yet

- 01 Gen Prov & Proc OrgDocument63 pages01 Gen Prov & Proc Orgmac ceeNo ratings yet

- Revision Questions 2020 Part VDocument18 pagesRevision Questions 2020 Part VJeffrey KamNo ratings yet

- Investment FunctionDocument18 pagesInvestment FunctionRishab Jain 2027203No ratings yet

- DepreciationDocument20 pagesDepreciationRan HorngNo ratings yet

- 12th Economics Minimum Study Materials English Medium PDF DownloadDocument12 pages12th Economics Minimum Study Materials English Medium PDF DownloadSenthil KathirNo ratings yet