You might also like

- Practical Industrial Data Networks: Design, Installation and TroubleshootingFrom EverandPractical Industrial Data Networks: Design, Installation and TroubleshootingRating: 5 out of 5 stars5/5 (2)

- The Potential Role of Hydrogen in India - Harnessing The Hype' TERI Report Launch Event December 16, 2020Document13 pagesThe Potential Role of Hydrogen in India - Harnessing The Hype' TERI Report Launch Event December 16, 2020Harinder Mohan SinghNo ratings yet

- European Contract Electronics Assembly Industry - 1993-97: A Strategic Study of the European CEM IndustryFrom EverandEuropean Contract Electronics Assembly Industry - 1993-97: A Strategic Study of the European CEM IndustryNo ratings yet

- Grid Codes With Respect To Distributed Generation: Day 1, 2:45pm, 30 MinsDocument29 pagesGrid Codes With Respect To Distributed Generation: Day 1, 2:45pm, 30 MinsShajahan ShariefNo ratings yet

- Green Hydrogen - UpdatedDocument22 pagesGreen Hydrogen - UpdatedBalasubramani RanganathanNo ratings yet

- L&T SwitchgearDocument40 pagesL&T SwitchgearRemo GagalNo ratings yet

- Datasheet A LV Stack Battery AI W5.1 B V2.0Document3 pagesDatasheet A LV Stack Battery AI W5.1 B V2.0skyfall3744No ratings yet

- Panel Solar Canadian 325 WPDocument2 pagesPanel Solar Canadian 325 WPEdu Lopez GarciaNo ratings yet

- Calculate Price For Production One Cubic Meter Water: Project Name LocationDocument4 pagesCalculate Price For Production One Cubic Meter Water: Project Name LocationȜbd Elrhman QandeelNo ratings yet

- Eni Gas Pipeline Final Report PDFDocument30 pagesEni Gas Pipeline Final Report PDFQudri SaufiNo ratings yet

- Transmission & Distribution Sector - PACRA Research - Jan'23Document13 pagesTransmission & Distribution Sector - PACRA Research - Jan'23JehanzebNo ratings yet

- AU Price List 01 Jul 2021Document40 pagesAU Price List 01 Jul 2021Kushal DixitNo ratings yet

- SD4O - 2 Part 2Document55 pagesSD4O - 2 Part 2Rafa CanoNo ratings yet

- 16kw ManualDocument48 pages16kw ManualJamesBrionesNo ratings yet

- Comprehensive range of MCBs for varied applicationsDocument40 pagesComprehensive range of MCBs for varied applicationsPrasenjit MaityNo ratings yet

- UK Short Mobile 2008Document22 pagesUK Short Mobile 2008solo12344322No ratings yet

- Mains Chokes Optimize Power DeliveryDocument4 pagesMains Chokes Optimize Power DeliveryVlad Gonzalez RamosNo ratings yet

- Manual Motor Weg 22Document44 pagesManual Motor Weg 22Yesid GómezNo ratings yet

- 2SA2099 / 2SC5888: High-Current Switching ApplicationsDocument5 pages2SA2099 / 2SC5888: High-Current Switching ApplicationsnguyenhieuproNo ratings yet

- WEG w22 Three Phase Electric Motor 50029265 Brochure EngliDocument44 pagesWEG w22 Three Phase Electric Motor 50029265 Brochure EngliAmir SafdarNo ratings yet

- Dymond: CS6X-340 - 345 - 350 - 355P-FG High Efficiency Poly ModuleDocument2 pagesDymond: CS6X-340 - 345 - 350 - 355P-FG High Efficiency Poly ModuleRICARDO STIVEN ROA ROANo ratings yet

- Mitsubishi Fra 740 Catalog 193396 - ADocument4 pagesMitsubishi Fra 740 Catalog 193396 - Ajohn solasNo ratings yet

- Wi-Fi Smart Digital Lock With A Built-In Doorbell and OLED ScreenDocument2 pagesWi-Fi Smart Digital Lock With A Built-In Doorbell and OLED ScreenJualtilu TiluNo ratings yet

- Dr. Anoop Singh - 10 - Policy and Regulation For Renewable Energy CertificatesDocument33 pagesDr. Anoop Singh - 10 - Policy and Regulation For Renewable Energy Certificatesramesh kumarNo ratings yet

- New Generation Bifacial Module Provides Up to 30% More Power From BackDocument2 pagesNew Generation Bifacial Module Provides Up to 30% More Power From BackDario del AngelNo ratings yet

- Instructor_Integration_System_Product_Brochure_EN_1101Document14 pagesInstructor_Integration_System_Product_Brochure_EN_1101ajmal0khan-8No ratings yet

- Designand Controlof Modular Multilevel Converterfor Voltage Sag MitigationDocument27 pagesDesignand Controlof Modular Multilevel Converterfor Voltage Sag MitigationĐinh MạnhNo ratings yet

- LEM-2X2 Motor OverviewDocument2 pagesLEM-2X2 Motor OverviewmohiNo ratings yet

- Shanghai Ifc Chiller Plant OptimizationDocument45 pagesShanghai Ifc Chiller Plant OptimizationYen NguyenNo ratings yet

- Sacred Sun SP Technical ManualDocument18 pagesSacred Sun SP Technical Manualمطابع رواسنNo ratings yet

- Download Arc Welding Processes Handbook 1St Edition Ramesh Singh full chapterDocument67 pagesDownload Arc Welding Processes Handbook 1St Edition Ramesh Singh full chapterreda.whitaker836100% (4)

- 5 Year Annual Transmission Capability Statement 2020-2024Document215 pages5 Year Annual Transmission Capability Statement 2020-2024Green BeretNo ratings yet

- DCS SeriesDocument2 pagesDCS SeriesCharmer JiaNo ratings yet

- MES2 Humidifier O&MDocument54 pagesMES2 Humidifier O&MpabloabelgilsotoNo ratings yet

- Leading energy storage solutions provider presentationDocument25 pagesLeading energy storage solutions provider presentationvenugopalanNo ratings yet

- Service Manual MATRIX 400E HF-englishDocument68 pagesService Manual MATRIX 400E HF-englishJaroslaw BrzozowskiNo ratings yet

- Myanmar Power Sector ReportDocument17 pagesMyanmar Power Sector ReportYupar EainNo ratings yet

- Internship ReportDocument34 pagesInternship ReportDavoud ShalforoushanNo ratings yet

- EPG SprintX 2329371Document104 pagesEPG SprintX 2329371Ivan MiskovicNo ratings yet

- Datasheet Transistor C5476Document4 pagesDatasheet Transistor C5476fchavestaNo ratings yet

- Electrical Design ServicesDocument3 pagesElectrical Design ServicesSharhan KhanNo ratings yet

- Full Description For Battery Lithium 6619 File 04Document29 pagesFull Description For Battery Lithium 6619 File 04Ghizlane MounjimNo ratings yet

- Ciena__C+L Band Business case Model_part-5Document2 pagesCiena__C+L Band Business case Model_part-5Ashish DoraNo ratings yet

- Yagi Rectenna Increases Battery Lifetime of Sensor NodesDocument4 pagesYagi Rectenna Increases Battery Lifetime of Sensor NodesArun KumarNo ratings yet

- WEG ElektromotorjiDocument80 pagesWEG ElektromotorjiGašper JuvanNo ratings yet

- slua565Document6 pagesslua565huonguyenNo ratings yet

- Infineon-Evaluation Board KIT 1EDB AUX SiC-ApplicationNotes-V01 00-EnDocument29 pagesInfineon-Evaluation Board KIT 1EDB AUX SiC-ApplicationNotes-V01 00-EnSergio ImotoNo ratings yet

- 182-72 (1)Document2 pages182-72 (1)Michel ErdmannNo ratings yet

- Portability Vs Economic Portability Vs SustainabilityDocument7 pagesPortability Vs Economic Portability Vs SustainabilityVejay PicsonNo ratings yet

- Lithium SeriesDocument2 pagesLithium SeriesHeider GuimaraesNo ratings yet

- MCCB - Disjuntores Modulados PVDocument67 pagesMCCB - Disjuntores Modulados PVJose mata IIINo ratings yet

- Canadian Solar Datasheet CS6K M enDocument2 pagesCanadian Solar Datasheet CS6K M enJulioCezarAlvesJuniorNo ratings yet

- PTT Am 2q2022Document41 pagesPTT Am 2q2022Apichaya WkksNo ratings yet

- GSA_Report_MultanDocument4 pagesGSA_Report_MultanSyed Wajih HaiderNo ratings yet

- A Feasibility Study On The Supply Chain of CO2-Free Ammonia With CCS and EOR 2019Document27 pagesA Feasibility Study On The Supply Chain of CO2-Free Ammonia With CCS and EOR 2019Ar DiNo ratings yet

- Control Techniques EU 20191781 Ecodesign Regulation - Energy Efficiency Indicators Issue 4Document23 pagesControl Techniques EU 20191781 Ecodesign Regulation - Energy Efficiency Indicators Issue 4arturoNo ratings yet

- IEA G20 Hydrogen report assumptions overviewDocument14 pagesIEA G20 Hydrogen report assumptions overviewpragya89No ratings yet

- Metro Train PrototypeDocument32 pagesMetro Train PrototypemelkamuNo ratings yet

- Closed Coke Slurry System: An Advanced Coke Handling ProcessDocument33 pagesClosed Coke Slurry System: An Advanced Coke Handling ProcessFayaz MohammedNo ratings yet

- Veriflex Intercon 1.8-3kV Cable - 1Document2 pagesVeriflex Intercon 1.8-3kV Cable - 1anastasia abengoaNo ratings yet

- h2sysDocument14 pagesh2sysAFRICA GREEN AGENo ratings yet

- plaquette_commerciale_correction (2)Document2 pagesplaquette_commerciale_correction (2)AFRICA GREEN AGENo ratings yet

- Clean Hydrogen Monitor 10-2022 DIGITALDocument226 pagesClean Hydrogen Monitor 10-2022 DIGITALAFRICA GREEN AGENo ratings yet

- 20160204-mahytec-d-hyvolution-hydrogen-storage-solutions-workshop-revujlh (1)Document18 pages20160204-mahytec-d-hyvolution-hydrogen-storage-solutions-workshop-revujlh (1)AFRICA GREEN AGENo ratings yet

- Clean_Hydrogen_Monitor_11-2023_DIGITAL_231122_171414 (1)Document168 pagesClean_Hydrogen_Monitor_11-2023_DIGITAL_231122_171414 (1)Diego MaportiNo ratings yet

- 01 MyriamOlivierAliMesbah Tropicals 85Document12 pages01 MyriamOlivierAliMesbah Tropicals 85AFRICA GREEN AGENo ratings yet

- Maths Question - How To Calculate Fuel Consumption Rates?: Best AnswerDocument1 pageMaths Question - How To Calculate Fuel Consumption Rates?: Best Answermohammad_shahzad_iiuiNo ratings yet

- Clean Energy: The European Green DealDocument2 pagesClean Energy: The European Green DealZhen Kai OngNo ratings yet

- Storable Renewable and Non-Storable Renewable ResourcesDocument29 pagesStorable Renewable and Non-Storable Renewable ResourcesSandip GadhiyaNo ratings yet

- OPEC and The Seven SistersDocument2 pagesOPEC and The Seven SistersrioesvaldinoNo ratings yet

- Kajaria Ceramics LTD PpaDocument37 pagesKajaria Ceramics LTD PpaVinay GhuwalewalaNo ratings yet

- BEE Final Report - 1Document148 pagesBEE Final Report - 1PROGETTO GKNo ratings yet

- Daily - Report - 14 - 06 - 2022 00 - 00 - 17 - 06 - 2022 23 - 59Document33 pagesDaily - Report - 14 - 06 - 2022 00 - 00 - 17 - 06 - 2022 23 - 59Mihai PopNo ratings yet

- BP Energy Outlook 2023Document66 pagesBP Energy Outlook 2023Danna Lizeth Rueda ParedesNo ratings yet

- Colorful Modern Geometric Fun Zero Waste InfographicDocument1 pageColorful Modern Geometric Fun Zero Waste InfographicvNo ratings yet

- BONDS1Document170 pagesBONDS1mariel corderoNo ratings yet

- Efe Matrix - BermudezDocument6 pagesEfe Matrix - BermudezEunice BermudezNo ratings yet

- 2222Document5 pages2222Roberto UrrutiaNo ratings yet

- Net Zero Operational CarbonDocument1 pageNet Zero Operational CarbonZaiinab taherNo ratings yet

- WindWorks: Powering a Sustainable CommunityDocument8 pagesWindWorks: Powering a Sustainable Communitywakin pmntlNo ratings yet

- Energy Usage Tracking Spreadsheet 11092022Document70 pagesEnergy Usage Tracking Spreadsheet 11092022VikasNehraNo ratings yet

- List of Petroleum and Oil CompanyDocument21 pagesList of Petroleum and Oil CompanySAnkit SinghNo ratings yet

- SJG Energy Assistance Fact Sheet 2021Document2 pagesSJG Energy Assistance Fact Sheet 2021MsLuNaMOoNNo ratings yet

- Argus Crude (2023-01-03) PDFDocument41 pagesArgus Crude (2023-01-03) PDFJaffar MazinNo ratings yet

- 21 - Asset Financials and ValuationDocument210 pages21 - Asset Financials and ValuationHasan AliNo ratings yet

- Dubai TariffsDocument1 pageDubai TariffsNishan MahanamaNo ratings yet

- Fuel Prices Effective March 01 2019 PDFDocument17 pagesFuel Prices Effective March 01 2019 PDFMuhammad YaqoobNo ratings yet

- 22nd NCE EA TopperList RevisedDocument2 pages22nd NCE EA TopperList RevisedKahkashanNo ratings yet

- Types of OilDocument14 pagesTypes of OilkirpaNo ratings yet

- Project 1 (Save Electricity)Document5 pagesProject 1 (Save Electricity)varun prajapatiNo ratings yet

- Energy management organization structureDocument1 pageEnergy management organization structureKimlukmanhNo ratings yet

- Ioana Ramona JurcaDocument1 pageIoana Ramona JurcaDaia SorinNo ratings yet

- Uttara Loadshaed 17Document18 pagesUttara Loadshaed 17azanNo ratings yet

- Approved Oils Mack Mdrive TransmissionsDocument4 pagesApproved Oils Mack Mdrive TransmissionsDavid PomaNo ratings yet

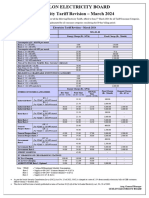

- Tariff Revision March 2024 - Web UploadDocument1 pageTariff Revision March 2024 - Web UploadRukshan JayasingheNo ratings yet

- CAPE Green Engineering Unit 2 Green Engineering SolutionsDocument18 pagesCAPE Green Engineering Unit 2 Green Engineering SolutionsTahj ThomasNo ratings yet