You might also like

- Credit Scoring HangoutDocument10 pagesCredit Scoring Hangoutdilinhtinh04No ratings yet

- Credit Scoring HangoutDocument5 pagesCredit Scoring Hangoutdilinhtinh04No ratings yet

- Group 2 - Credit ScoringDocument3 pagesGroup 2 - Credit ScoringPhạm Quỳnh TrangNo ratings yet

- Credit Risk Grading Score SheetDocument3 pagesCredit Risk Grading Score SheetMd. ZubaerNo ratings yet

- Ponderation Bale IIDocument5 pagesPonderation Bale IIzouhair melloukNo ratings yet

- 01 Case Risk Parameters: Risk Scoring of A Borrower: Financial Risk Considerations OptionsDocument2 pages01 Case Risk Parameters: Risk Scoring of A Borrower: Financial Risk Considerations OptionsdeadlsweetyNo ratings yet

- Credit Risk Grading For LoanDocument12 pagesCredit Risk Grading For LoanSaid Ur RahmanNo ratings yet

- Decision Tree Exercise 2 SolDocument5 pagesDecision Tree Exercise 2 SoljitenNo ratings yet

- Credit Risk Grading Score Sheet Reference No.Document12 pagesCredit Risk Grading Score Sheet Reference No.Antora HoqueNo ratings yet

- Bank CRG ScoreSheetDocument3 pagesBank CRG ScoreSheetMd. Zubaer100% (1)

- Aging of Accounts (Individual Assessment)Document1 pageAging of Accounts (Individual Assessment)Mary Ann PacariemNo ratings yet

- Prudential Norms Relating To Capital AdequacyDocument19 pagesPrudential Norms Relating To Capital AdequacyVishwas tomarNo ratings yet

- Credit RiskDocument78 pagesCredit RiskcarinaNo ratings yet

- Credit Risk Grading Score SheetDocument3 pagesCredit Risk Grading Score Sheetmr9_apeceNo ratings yet

- Business Credit Scoring Model NewDocument17 pagesBusiness Credit Scoring Model NewRatna NisaaNo ratings yet

- FIN534 HW Set 2 - RubricDocument1 pageFIN534 HW Set 2 - RubricSwapan Kumar SahaNo ratings yet

- Minimum Capital Requirement:: Credit, Market and Operational RiskDocument34 pagesMinimum Capital Requirement:: Credit, Market and Operational RiskMohammad FaizuNo ratings yet

- The Jammu & Kashmir Bank LTD: AccountDocument5 pagesThe Jammu & Kashmir Bank LTD: AccountĒxçlūsìvē SympãthētìçNo ratings yet

- Credit Rating To Customers in Commercial Banks: Rationality and IssuesDocument40 pagesCredit Rating To Customers in Commercial Banks: Rationality and IssuesMaiChi PhamNo ratings yet

- Icrrs 11Document1 pageIcrrs 11Sadia HossainNo ratings yet

- I: Multiple Choice (30 Points) : These Statements Are True or False? (25 Points/correct Answer)Document4 pagesI: Multiple Choice (30 Points) : These Statements Are True or False? (25 Points/correct Answer)Mỹ Dung PhạmNo ratings yet

- Credit Scoring MTB 113Document6 pagesCredit Scoring MTB 113Mojeed KasheemNo ratings yet

- Parameter Score: Criteria Weight A. Financial RiskDocument7 pagesParameter Score: Criteria Weight A. Financial RiskAgotoNo ratings yet

- Current and Savings Account Interest Rate: Personal AccountsDocument2 pagesCurrent and Savings Account Interest Rate: Personal AccountsMd.Rashidul Alam Sorker RifatNo ratings yet

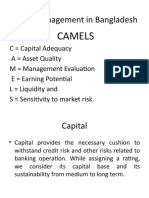

- Credit Management in BangladeshDocument13 pagesCredit Management in BangladeshPrasenjit SahaNo ratings yet

- Global Financial Management: Debt Policy, Capital Structure, and Capital BudgetingDocument40 pagesGlobal Financial Management: Debt Policy, Capital Structure, and Capital BudgetingahmedmtNo ratings yet

- CRG Neptune PropertiesDocument2 pagesCRG Neptune PropertiesZayed Mohammad JohnyNo ratings yet

- RBI Format ROI PCDocument8 pagesRBI Format ROI PCom vermaNo ratings yet

- Cost of Debt Calculations PDFDocument2 pagesCost of Debt Calculations PDFhukaNo ratings yet

- Sovereign Loan PricingDocument3 pagesSovereign Loan PricingWilliam LauNo ratings yet

- RBI Format ROI PDocument8 pagesRBI Format ROI PSrikanth ReddyNo ratings yet

- Credit Rating FinalDocument12 pagesCredit Rating FinalRawan SaberNo ratings yet

- Index Rate Sheet 4-29-09Document2 pagesIndex Rate Sheet 4-29-09PFINo ratings yet

- Icrrs 10Document2 pagesIcrrs 10Sadia HossainNo ratings yet

- Brac Bank Deposit Interest RateDocument2 pagesBrac Bank Deposit Interest RateSohel RanaNo ratings yet

- Answer To Mock ExamDocument4 pagesAnswer To Mock Examnga vuNo ratings yet

- Rbi Format Roi PCDocument10 pagesRbi Format Roi PCsriramNo ratings yet

- Portfolio Credit RiskDocument37 pagesPortfolio Credit RisksgjatharNo ratings yet

- SBM VAlidation FormDocument2 pagesSBM VAlidation FormamerizaNo ratings yet

- RBI Format ROI PC PDFDocument9 pagesRBI Format ROI PC PDFmohana sundaram pNo ratings yet

- Excel FunctionsDocument31 pagesExcel FunctionsMUSHU GUPTANo ratings yet

- Live Wire June 28 XDocument933 pagesLive Wire June 28 Xapi-3855182100% (2)

- Sample SBM Validation FormDocument3 pagesSample SBM Validation FormMC MirandaNo ratings yet

- AIA ELITE ACADEMY Profiling QuestionnaireDocument1 pageAIA ELITE ACADEMY Profiling QuestionnaireKen LeeNo ratings yet

- Prepare Quiz 1Document11 pagesPrepare Quiz 1Fransiskus AdityaNo ratings yet

- Credit Scoring ChecklistDocument2 pagesCredit Scoring ChecklistBhaskar GarimellaNo ratings yet

- KRA Sales TeamDocument7 pagesKRA Sales TeamAnuNo ratings yet

- Credit Advisory Services 2019: Ken StreyDocument9 pagesCredit Advisory Services 2019: Ken StreykenNo ratings yet

- Restructuring Debt and Equity - Problems and SolutionsDocument5 pagesRestructuring Debt and Equity - Problems and SolutionsGjmNo ratings yet

- Notification Regarding Spring 2024 Semester or Trimester Final Examinations and Grade SubmissionDocument9 pagesNotification Regarding Spring 2024 Semester or Trimester Final Examinations and Grade SubmissionMahmudul HasanNo ratings yet

- AvanzaDocument9 pagesAvanzaAdnan Al ShahidNo ratings yet

- Avanse International FinancingDocument3 pagesAvanse International FinancinggoanfidalgosNo ratings yet

- Bond Rating SYSTEMDocument6 pagesBond Rating SYSTEMkamranskNo ratings yet

- Personal Account Interest Rate: (Golden Benefits)Document4 pagesPersonal Account Interest Rate: (Golden Benefits)Md Ashikur RahmanNo ratings yet

- RBI - ROI FormatDocument9 pagesRBI - ROI Formatranajoy biswasNo ratings yet

- CRM Unit 4 DCDocument67 pagesCRM Unit 4 DCdac_101No ratings yet

- Camels LongerDocument39 pagesCamels LongerAbed HossainNo ratings yet

- Grading: Submitted To:-Dr. Rita Saini Dr. B.S YadavDocument11 pagesGrading: Submitted To:-Dr. Rita Saini Dr. B.S YadavVijayNo ratings yet

- Repair and Boost Your Credit Score in 30 Days: How Anyone Can Fix, Repair, and Boost Their Credit Ratings in Less Than 30 DaysFrom EverandRepair and Boost Your Credit Score in 30 Days: How Anyone Can Fix, Repair, and Boost Their Credit Ratings in Less Than 30 DaysNo ratings yet

- From Bad to Good Credit: A Practical Guide for Individuals with Charge-Offs and CollectionsFrom EverandFrom Bad to Good Credit: A Practical Guide for Individuals with Charge-Offs and CollectionsNo ratings yet

- An Introduction To Trade Credit InsuranceDocument4 pagesAn Introduction To Trade Credit InsuranceBizic Maria LaviniaNo ratings yet

- 3 AnnuitiesDocument17 pages3 Annuitiesdmvalencia422No ratings yet

- Kyc Aml CFTDocument201 pagesKyc Aml CFTkunal tyagi100% (2)

- Chapter 6Document57 pagesChapter 6Can BayirNo ratings yet

- Economics-And-Finance-Video-Quiz-Questions 1Document3 pagesEconomics-And-Finance-Video-Quiz-Questions 1api-550118775No ratings yet

- Part 3 - Understanding Financial Statements and ReportsDocument7 pagesPart 3 - Understanding Financial Statements and ReportsJeanrey AlcantaraNo ratings yet

- The Effects of Changes in Foreign Exchange Rates PDFDocument13 pagesThe Effects of Changes in Foreign Exchange Rates PDFChelsy SantosNo ratings yet

- Transcript 1820115Document2 pagesTranscript 1820115Wasifa Tahsin AraniNo ratings yet

- Xsig 1227511 PDFDocument12 pagesXsig 1227511 PDFAchim HelmstedtNo ratings yet

- Cash Balances Quantity Theory of MoneyDocument8 pagesCash Balances Quantity Theory of MoneyAppan Kandala VasudevacharyNo ratings yet

- Aston SoloDocument2 pagesAston SoloVonny LamorenNo ratings yet

- The Impact of External Debt On Economic Growth in Egypt 1Document8 pagesThe Impact of External Debt On Economic Growth in Egypt 1Walaa IbrahimNo ratings yet

- Buffet Bid For Media GeneralDocument21 pagesBuffet Bid For Media Generalshivam chughNo ratings yet

- Assignment 2 PFMDocument3 pagesAssignment 2 PFMWasif Imran RARE0% (1)

- A DokumentDocument2 pagesA Dokumentamberjain41No ratings yet

- Equicapita Signs Agreement With ATB Corporate Financial Services For Acquisition FacilityDocument2 pagesEquicapita Signs Agreement With ATB Corporate Financial Services For Acquisition FacilityEquicapita Income TrustNo ratings yet

- Developing The Asian Markets For Non-Performing Assets - India's ExperienceDocument32 pagesDeveloping The Asian Markets For Non-Performing Assets - India's ExperienceRAJESH MAHTO 2058No ratings yet

- Philippine School of Business Administration: Cpa ReviewDocument6 pagesPhilippine School of Business Administration: Cpa ReviewYukiNo ratings yet

- Questions CH 10Document4 pagesQuestions CH 10Maria DevinaNo ratings yet

- Chapter 4 PAS 7 Statement of Cash FlowsDocument20 pagesChapter 4 PAS 7 Statement of Cash FlowsSimon RavanaNo ratings yet

- SAP FICO Transaction CodesDocument38 pagesSAP FICO Transaction Codesdjtaz13100% (1)

- Governmental Accounting Test QuestionsDocument2 pagesGovernmental Accounting Test QuestionstcsaulsNo ratings yet

- Test AnswersDocument4 pagesTest AnswersM Ferdian Ibnu RezaNo ratings yet

- Assignment 4 - Sec JDocument9 pagesAssignment 4 - Sec JRafayGhafoorNo ratings yet

- Payment SlipDocument2 pagesPayment SlipAlphie PabloNo ratings yet

- Chapter 05 - AnswerDocument36 pagesChapter 05 - AnswerAgentSkySkyNo ratings yet

- Narayana Engineering College: Nellore: A Study On Capital Budgeting in Sagar Cements PVT LTD, HyderbadDocument65 pagesNarayana Engineering College: Nellore: A Study On Capital Budgeting in Sagar Cements PVT LTD, Hyderbadsaryumba5538No ratings yet

- Confirmation NoteDocument1 pageConfirmation NoteReZa Fauzi CNNo ratings yet

- Cusdec Final SADDocument5 pagesCusdec Final SADSamantha Swift0% (1)