You might also like

- Emnace FinMa Activity 2Document2 pagesEmnace FinMa Activity 2CASTOR, Vincent PaulNo ratings yet

- TaxationDocument55 pagesTaxationorlandoNo ratings yet

- CASE DOCTRINES - 2020 Jurisprudence Updates (SC and CTA Cases)Document12 pagesCASE DOCTRINES - 2020 Jurisprudence Updates (SC and CTA Cases)Carlota VillaromanNo ratings yet

- Silkair Singapore V. CirDocument6 pagesSilkair Singapore V. CirConie NovelaNo ratings yet

- The Source of An Income Is The Property, Activity or Service That Produced The IncomeDocument10 pagesThe Source of An Income Is The Property, Activity or Service That Produced The IncomeMarianne Hope VillasNo ratings yet

- Dr. Jeannie P. LimDocument38 pagesDr. Jeannie P. LimSHeena MaRie ErAsmoNo ratings yet

- (J. Bersamin) : Code of Services Subject To VAT Is ExclusiveDocument7 pages(J. Bersamin) : Code of Services Subject To VAT Is ExclusiveED RCNo ratings yet

- Tax Lates JurisprudenceDocument19 pagesTax Lates JurisprudenceJoni PurayNo ratings yet

- Income Compilation Tax ReviewDocument13 pagesIncome Compilation Tax ReviewJosiebethAzueloNo ratings yet

- Fort Bonifacio Devt Corp V CIRDocument3 pagesFort Bonifacio Devt Corp V CIRBettina Rayos del SolNo ratings yet

- Cir Vs PLDT (GR No. 140230 December 15, 2005)Document2 pagesCir Vs PLDT (GR No. 140230 December 15, 2005)Rich Lloyd GitoNo ratings yet

- Dayagbil, Escano, Sabdullah, Villablanca EH 406 TAX 1 December 16, 2017 Perino, Benuya, Go, SalvacionDocument5 pagesDayagbil, Escano, Sabdullah, Villablanca EH 406 TAX 1 December 16, 2017 Perino, Benuya, Go, SalvacionVanda Charissa Tibon DayagbilNo ratings yet

- PM Reyes Bar Reviewer On Taxation Supple PDFDocument13 pagesPM Reyes Bar Reviewer On Taxation Supple PDFAnonymous kiom0L1FqsNo ratings yet

- Silkair (Singapore) Pte, Ltd. vs. Commissioner of Internal Revenue 544 SCRA 100Document18 pagesSilkair (Singapore) Pte, Ltd. vs. Commissioner of Internal Revenue 544 SCRA 100BernsNo ratings yet

- Tax Digests On Tax 2Document25 pagesTax Digests On Tax 2John Roel S. VillaruzNo ratings yet

- Silkair Vs CIRDocument16 pagesSilkair Vs CIRJay TabuzoNo ratings yet

- Digest TaxDocument3 pagesDigest TaxAimee MilleteNo ratings yet

- Cir vs. Isabela Cultural Corporation (Icc) : Issue/SDocument5 pagesCir vs. Isabela Cultural Corporation (Icc) : Issue/SMary AnneNo ratings yet

- Dayagbil, Escano, Sabdullah, Villablanca EH 406 TAX 1 December 16, 2017Document4 pagesDayagbil, Escano, Sabdullah, Villablanca EH 406 TAX 1 December 16, 2017Vanda Charissa Tibon DayagbilNo ratings yet

- Word Work File L - 1330700490Document13 pagesWord Work File L - 1330700490Alyza Montilla BurdeosNo ratings yet

- Case Digest On Taxation IDocument65 pagesCase Digest On Taxation IAndrew MarfilNo ratings yet

- CIR Vs Algue Inc Digest OnwardsDocument32 pagesCIR Vs Algue Inc Digest OnwardsMark Jason Crece Ante100% (1)

- Tax Digest CompilationDocument37 pagesTax Digest CompilationVerine SagunNo ratings yet

- Tax 2 Digest (0205) GR l147295 021607 Cir Vs AcesiteDocument2 pagesTax 2 Digest (0205) GR l147295 021607 Cir Vs AcesiteAudrey Deguzman100% (1)

- Villanueva V City of IloiloDocument48 pagesVillanueva V City of Iloiloamun dinNo ratings yet

- 2008 Digest-Sc Taxation CasesDocument19 pages2008 Digest-Sc Taxation Caseschiclets777100% (2)

- 3 Diageo Philippines Vs Commissioner (Excise Tax, Indirect Tax, Taxpayer Definition)Document5 pages3 Diageo Philippines Vs Commissioner (Excise Tax, Indirect Tax, Taxpayer Definition)Robert EspinaNo ratings yet

- Kjaefncl (Complete)Document42 pagesKjaefncl (Complete)Kenzo RodisNo ratings yet

- VAT EXEMPTION UNDER SPECIAL LAWS - CONTEX CORPORATION vs. CIRDocument3 pagesVAT EXEMPTION UNDER SPECIAL LAWS - CONTEX CORPORATION vs. CIRChristine Gel MadrilejoNo ratings yet

- Deductions and Exemptions DigestsDocument16 pagesDeductions and Exemptions DigestsjmclacasNo ratings yet

- Fort Bonifacio Development Corp. vs. Commissioner of Internal Revenue, 679 SCRA 566, September 04, 2012Document3 pagesFort Bonifacio Development Corp. vs. Commissioner of Internal Revenue, 679 SCRA 566, September 04, 2012anajuanitoNo ratings yet

- Dr. LimDocument152 pagesDr. LimJoan BaltazarNo ratings yet

- TAx 2 Final CasesDocument15 pagesTAx 2 Final CasesGellian eve OngNo ratings yet

- Landmark Cases On Value-Added Tax (VAT) : Taxation II Juderick RamosDocument12 pagesLandmark Cases On Value-Added Tax (VAT) : Taxation II Juderick RamosJudeRamosNo ratings yet

- Cir V. Solidbank Corporation: FactsDocument3 pagesCir V. Solidbank Corporation: FactsJustine Jay Casas LopeNo ratings yet

- CIR vs. LA FLOR DEla ISABELA, 2019Document3 pagesCIR vs. LA FLOR DEla ISABELA, 2019Fenina Reyes0% (1)

- CIR vs. Bank of Commerce (2005)Document16 pagesCIR vs. Bank of Commerce (2005)BenNo ratings yet

- Paseo Realty and Development Corp. Vs - Court of Appealsg.R. No. 119286 October 13, 2004FACTSDocument8 pagesPaseo Realty and Development Corp. Vs - Court of Appealsg.R. No. 119286 October 13, 2004FACTSShynnMiñozaNo ratings yet

- Philippine Airlines v. CIR: SummaryDocument4 pagesPhilippine Airlines v. CIR: SummaryL-Shy KïmNo ratings yet

- Philippine Airlines v. CIR: SummaryDocument4 pagesPhilippine Airlines v. CIR: SummaryUnicorns Are RealNo ratings yet

- Taxation Case Digest (Batch 2) Case #1Document7 pagesTaxation Case Digest (Batch 2) Case #1Na AbdurahimNo ratings yet

- FBDC VS CirDocument13 pagesFBDC VS CirRene ValentosNo ratings yet

- PLS Taxation QA FinalDocument24 pagesPLS Taxation QA FinalTAU MU OFFICIALNo ratings yet

- Philex VS CirDocument2 pagesPhilex VS CirNikko Ryan C'zare AbalosNo ratings yet

- c.11. Filipinas Synthetic Fiber Corp v. CADocument1 pagec.11. Filipinas Synthetic Fiber Corp v. CAArbie LlesisNo ratings yet

- Diageo Phils. Inc. vs. CIR GR No. 183553Document3 pagesDiageo Phils. Inc. vs. CIR GR No. 183553ZeusKimNo ratings yet

- Justice Teresita Leonardo-De Castro Cases (2008-2015) : Scope and Limitations of Taxation (Constitutional Limitations)Document4 pagesJustice Teresita Leonardo-De Castro Cases (2008-2015) : Scope and Limitations of Taxation (Constitutional Limitations)jimNo ratings yet

- 183553-2012-Diageo Philippines, Inc. v. Commissioner of Internal RevenueDocument7 pages183553-2012-Diageo Philippines, Inc. v. Commissioner of Internal RevenueButch MaatNo ratings yet

- Facts:: 1 CIR vs. Seagate Technology (Philippines) G.R. NO. 153866, February 11, 2005Document5 pagesFacts:: 1 CIR vs. Seagate Technology (Philippines) G.R. NO. 153866, February 11, 2005JV PagunuranNo ratings yet

- Contex Corp vs. CirDocument3 pagesContex Corp vs. CirKath Leen100% (1)

- CIR Vs Commonwealth ManagementDocument3 pagesCIR Vs Commonwealth ManagementGoody100% (1)

- Asia International Vs CirDocument3 pagesAsia International Vs Cirdiamajolu gaygonsNo ratings yet

- Taxation Case DigestsDocument7 pagesTaxation Case DigestszzzNo ratings yet

- Updates On TAX 2014Document127 pagesUpdates On TAX 2014Karen GinaNo ratings yet

- (CASE DIGEST) CIR v. CA and COMASERCO (G.R. No. 125355) : March 30, 2000Document3 pages(CASE DIGEST) CIR v. CA and COMASERCO (G.R. No. 125355) : March 30, 2000j guevarraNo ratings yet

- VAT in General - CIR Vs CA &CMS, GR No. 125355Document2 pagesVAT in General - CIR Vs CA &CMS, GR No. 125355Christine Gel MadrilejoNo ratings yet

- Tax Amnesty Doctrines in Taxation DigestDocument9 pagesTax Amnesty Doctrines in Taxation DigestJuralexNo ratings yet

- Tax Case Digests MidtermsDocument47 pagesTax Case Digests MidtermsJulo R. TaleonNo ratings yet

- Tax 1 Case DigestsDocument50 pagesTax 1 Case Digestso6739No ratings yet

- Tax Digests - Recent JurisprudenceDocument25 pagesTax Digests - Recent JurisprudenceMark Xavier Overhaul LibardoNo ratings yet

- UMak Barops Lopez Cases QAs - POLITICAL LAWDocument13 pagesUMak Barops Lopez Cases QAs - POLITICAL LAWPsychelynne NicolasNo ratings yet

- Reply Lagundi Vs DimayaDocument4 pagesReply Lagundi Vs DimayaPsychelynne NicolasNo ratings yet

- Letter To Invite Zumba DancersDocument2 pagesLetter To Invite Zumba DancersPsychelynne NicolasNo ratings yet

- JCI Sings JudgesDocument2 pagesJCI Sings JudgesPsychelynne NicolasNo ratings yet

- JCI TY Improv Oracle Judges and TeachersDocument2 pagesJCI TY Improv Oracle Judges and TeachersPsychelynne NicolasNo ratings yet

- Hrh-Carganillo, Novagrace Coe Request LetterDocument1 pageHrh-Carganillo, Novagrace Coe Request LetterPsychelynne NicolasNo ratings yet

- Deed of Real Estate MortgageDocument2 pagesDeed of Real Estate MortgagePsychelynne NicolasNo ratings yet

- AcknowledgmentDocument1 pageAcknowledgmentPsychelynne NicolasNo ratings yet

- Comment Opposition Taquiqui Vs JRLDocument4 pagesComment Opposition Taquiqui Vs JRLPsychelynne NicolasNo ratings yet

- Comment Opposition PP Vs ClaroDocument4 pagesComment Opposition PP Vs ClaroPsychelynne NicolasNo ratings yet

- Authorization LetterDocument1 pageAuthorization LetterPsychelynne NicolasNo ratings yet

- Annexure-VII-GCC - Composite Orders1Document105 pagesAnnexure-VII-GCC - Composite Orders1Bhageerathi SahuNo ratings yet

- Pestel Analyses BarbadosDocument1 pagePestel Analyses BarbadosClodevreuxNo ratings yet

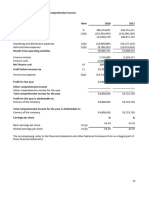

- Income Statement and Balance Sheet ExerciseDocument2 pagesIncome Statement and Balance Sheet ExerciseMujieh NkengNo ratings yet

- S&P BielarskiDocument2 pagesS&P Bielarskiryan turbeville100% (1)

- Microsoft Word - Module 1Document4 pagesMicrosoft Word - Module 1sshreyasNo ratings yet

- Oligopolistic Nature and Competition in The Telecom SectorDocument9 pagesOligopolistic Nature and Competition in The Telecom SectorErikaNo ratings yet

- Revised - 2020-SPRING-EFDA-International Business-Hanna - GaneshDocument9 pagesRevised - 2020-SPRING-EFDA-International Business-Hanna - GaneshRamneek JainNo ratings yet

- Top 30 MCQ - Banking Reform & NationalizationDocument4 pagesTop 30 MCQ - Banking Reform & NationalizationEthan HuntNo ratings yet

- Real Feel Test 1Document50 pagesReal Feel Test 1Pragati Yadav100% (2)

- Bloomberg: US Equity Corporate Action MethodologyDocument32 pagesBloomberg: US Equity Corporate Action MethodologyEdwin ChanNo ratings yet

- Haier's Rendanheyi 2.0Document8 pagesHaier's Rendanheyi 2.0Hieu NguyenNo ratings yet

- Problem Set 1 - Basics of Spreadsheet ModelingDocument2 pagesProblem Set 1 - Basics of Spreadsheet ModelingRitabhari Banik RoyNo ratings yet

- Strama ReviewerDocument4 pagesStrama ReviewerKimmy PaulNo ratings yet

- Handout-Pallas, Bisnis Strategy PDF (27aug2022)Document27 pagesHandout-Pallas, Bisnis Strategy PDF (27aug2022)josephNo ratings yet

- Deed of Absolute SaleDocument3 pagesDeed of Absolute SaleRae Marie Cadeliña ManarNo ratings yet

- Handout 2 - Banking Products and ServicesDocument5 pagesHandout 2 - Banking Products and Servicescarolina manotasNo ratings yet

- Chile and The Chilean Wine IndustryDocument39 pagesChile and The Chilean Wine IndustryRiad-us SalehinNo ratings yet

- State of Competition EthiopiaDocument232 pagesState of Competition EthiopiaFisehaNo ratings yet

- Case Study Challenges of Online Travel AgentsDocument2 pagesCase Study Challenges of Online Travel AgentsJOHN PAUL AQUINONo ratings yet

- Kartik - Double EnteryDocument17 pagesKartik - Double EnterySathya SeelanNo ratings yet

- Person's Name With Whom Telecall Was Made His Designation (With Deptt, User/Procurement/ Fin)Document8 pagesPerson's Name With Whom Telecall Was Made His Designation (With Deptt, User/Procurement/ Fin)Arun YashodharanNo ratings yet

- Practice QuestionsDocument11 pagesPractice QuestionsMichaella PangilinanNo ratings yet

- Part 1Document42 pagesPart 1Dipesh KumarNo ratings yet

- Case Study To Read Ahead of The Start of SMPA Module 601528Document3 pagesCase Study To Read Ahead of The Start of SMPA Module 601528Janda YeeNo ratings yet

- FNACDocument7 pagesFNACMOHIT SINGH0% (1)

- Asia Moods - 74th Edition October 2021Document10 pagesAsia Moods - 74th Edition October 2021ShivaNo ratings yet

- SASOL InSociety 2021 V17 29nov Single 0 0 0Document86 pagesSASOL InSociety 2021 V17 29nov Single 0 0 0Kseniya SergeevaNo ratings yet

- Join Life: Social Audit Environmental AssessmentDocument2 pagesJoin Life: Social Audit Environmental AssessmentFakrul Hasan Khan RussellNo ratings yet

- Introduction To Cost Accounting: MeaningDocument11 pagesIntroduction To Cost Accounting: MeaningTejas YeoleNo ratings yet