You might also like

- Economic Indicators for South and Central Asia: Input–Output TablesFrom EverandEconomic Indicators for South and Central Asia: Input–Output TablesNo ratings yet

- Sujata: %age Turnover of ABCDocument7 pagesSujata: %age Turnover of ABCKunikaNo ratings yet

- WWW Entrepreneurindia CoDocument81 pagesWWW Entrepreneurindia CoNanasaheb PatilNo ratings yet

- ICCT Comments Renewable Fuel Standard Program Rvo Noda 20171019Document5 pagesICCT Comments Renewable Fuel Standard Program Rvo Noda 20171019The International Council on Clean TransportationNo ratings yet

- Non Alcoholic Wine in Asia Pacific DatagraphicsDocument3 pagesNon Alcoholic Wine in Asia Pacific DatagraphicsSaloni GawdeNo ratings yet

- 2021-12-13-AR - (ANP) - En-Stable - Outlook - For - Food - and - Beverage - Industry XXXDocument4 pages2021-12-13-AR - (ANP) - En-Stable - Outlook - For - Food - and - Beverage - Industry XXXShinta Litania DuhainNo ratings yet

- Small Scale Liquid Detergent Business PlanDocument22 pagesSmall Scale Liquid Detergent Business PlanĐạt Diệp0% (1)

- Decision Science (Assignment) Chandigarh UniversityDocument7 pagesDecision Science (Assignment) Chandigarh UniversityShubham DwivediNo ratings yet

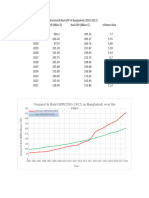

- Nominal & Real GDP (2003-2022) in Bangladesh Over The YearsDocument2 pagesNominal & Real GDP (2003-2022) in Bangladesh Over The Yearssadia TFNo ratings yet

- Astral delivers 73% revenue growth, 332% PBT growth in Q1Document5 pagesAstral delivers 73% revenue growth, 332% PBT growth in Q1Namrata ShahNo ratings yet

- IPO Market Nov-2023Document4 pagesIPO Market Nov-2023Deepan KapadiaNo ratings yet

- Rekap Harga TBS CPODocument98 pagesRekap Harga TBS CPOGlobal MapindoNo ratings yet

- EVALUACION Plaza Jose OlayaDocument140 pagesEVALUACION Plaza Jose OlayaDaNnY VILLACORTANo ratings yet

- Pdfanddoc 538625 PDFDocument76 pagesPdfanddoc 538625 PDFsoumyarm942No ratings yet

- Bottled Water IndustryDocument26 pagesBottled Water IndustrySriramVenkatNo ratings yet

- InfosysDocument13 pagesInfosysMandeep BatraNo ratings yet

- Note On Grain Distillery - 8623577901716260468Document11 pagesNote On Grain Distillery - 8623577901716260468Sourabh DubeyNo ratings yet

- Shantanu FadmDocument12 pagesShantanu FadmHimanshuNo ratings yet

- Trends in The Performance of Telecom IndustryDocument55 pagesTrends in The Performance of Telecom IndustryIshan ShahNo ratings yet

- File 19-Class Wrap-Ups 17Document7 pagesFile 19-Class Wrap-Ups 17alroy dcruzNo ratings yet

- File 19-Class Wrap-Ups 16Document7 pagesFile 19-Class Wrap-Ups 16alroy dcruzNo ratings yet

- Dividend Policy Analysis: Submitted To: Prof. Sougata RayDocument8 pagesDividend Policy Analysis: Submitted To: Prof. Sougata Raysubhasis mahapatraNo ratings yet

- E-Commerce: 27% CAGR and Expected To ReachDocument12 pagesE-Commerce: 27% CAGR and Expected To ReachNAMIT GADGENo ratings yet

- Strategic Marketing & PlanningDocument30 pagesStrategic Marketing & PlanningsalmansaleemNo ratings yet

- Sales Forecast by Hypo. Eg.Document8 pagesSales Forecast by Hypo. Eg.Nawazish KhanNo ratings yet

- DupontDocument8 pagesDupontAnonymous 5m1uMUPaHNo ratings yet

- BF Homes Aquascapes Sales ProjectionDocument98 pagesBF Homes Aquascapes Sales ProjectionJudelNo ratings yet

- Hero Motocorp DCF ValuationDocument66 pagesHero Motocorp DCF ValuationPrabhdeep DadyalNo ratings yet

- Maxime Project ReportDocument60 pagesMaxime Project ReportMOHD GULZARNo ratings yet

- Profitable Investment Opportunity in LPG Filling Plant-896737 PDFDocument64 pagesProfitable Investment Opportunity in LPG Filling Plant-896737 PDFChinyeaka John Onam100% (1)

- Case Study #2 - Ocean CarriersDocument11 pagesCase Study #2 - Ocean CarriersrtrickettNo ratings yet

- UntitledDocument29 pagesUntitledPilly PhamNo ratings yet

- Diwali Picks 2023 NBRRDocument16 pagesDiwali Picks 2023 NBRRSharwan KumarNo ratings yet

- Task 3 by Aditya GuptaDocument7 pagesTask 3 by Aditya GuptaADITYA GUPTANo ratings yet

- Production of Sterile Water For Injection. WFI (Water For Injection) Manufacturing. Water For Pharmaceutical Purposes.-792178 PDFDocument64 pagesProduction of Sterile Water For Injection. WFI (Water For Injection) Manufacturing. Water For Pharmaceutical Purposes.-792178 PDFGajjkNo ratings yet

- AFM PPT FinalDocument45 pagesAFM PPT Final0nilNo ratings yet

- Cement PDFDocument71 pagesCement PDFLikith Kumar100% (1)

- Asset Management Companies: Date: 20 February, 2020Document34 pagesAsset Management Companies: Date: 20 February, 2020Ikp IkpNo ratings yet

- Let’s Go Aero Travel Trailers Sales ProjectionsDocument9 pagesLet’s Go Aero Travel Trailers Sales ProjectionsmanjinderchabbaNo ratings yet

- Study - Id65431 - Domestic Tourism in IndiaDocument58 pagesStudy - Id65431 - Domestic Tourism in IndiaShubham AggarwalNo ratings yet

- JK Tyre One Page ProfileDocument1 pageJK Tyre One Page Profilep9688822No ratings yet

- Musical Muesuem AssignmentDocument12 pagesMusical Muesuem AssignmentiopasdcNo ratings yet

- #BOLD STOP Marketing PlanDocument50 pages#BOLD STOP Marketing PlanAhmed Alaa100% (1)

- Ocean CarriersDocument17 pagesOcean CarriersMridula Hari33% (3)

- INOX Leisure LTD: Equity Research ReportDocument12 pagesINOX Leisure LTD: Equity Research ReportrakeshNo ratings yet

- Store Factsheet: Nama Store: Number of Store: Opening DateDocument8 pagesStore Factsheet: Nama Store: Number of Store: Opening DateNikita Dara AmeliaNo ratings yet

- Feasibility StudyDocument18 pagesFeasibility StudyJessa BallonNo ratings yet

- GDP, Labor Force & FDI Data Over 2010-2019Document8 pagesGDP, Labor Force & FDI Data Over 2010-2019Minh HảiNo ratings yet

- Indian Corrugated Packaging: Good Times AheadDocument4 pagesIndian Corrugated Packaging: Good Times Aheaddear14us1984No ratings yet

- GDP, Labor Force & FDI Data Over 2010-2019Document8 pagesGDP, Labor Force & FDI Data Over 2010-2019Minh HảiNo ratings yet

- Phiroze Jeejeebhoy Towers Dalal Street Mumbai - 400 001.: BSE Limited National Stock Exchange of India LimitedDocument6 pagesPhiroze Jeejeebhoy Towers Dalal Street Mumbai - 400 001.: BSE Limited National Stock Exchange of India LimitedJITHIN KRISHNAN MNo ratings yet

- Vietnam Market Trend Q3 - 2020Document22 pagesVietnam Market Trend Q3 - 2020cosmosmediavnNo ratings yet

- Pencil Industry in India Market AnalysisDocument67 pagesPencil Industry in India Market AnalysisMuhammad SulmanNo ratings yet

- Chapter 4Document22 pagesChapter 4PreethaSureshNo ratings yet

- Earnings Update Q1FY22Document15 pagesEarnings Update Q1FY22sai mohanNo ratings yet

- BDO Unibank 2021 Annual Report Financial SupplementsDocument236 pagesBDO Unibank 2021 Annual Report Financial Supplementssharielles /No ratings yet

- AFM - Latest - LatestDocument23 pagesAFM - Latest - LatestXyz YxzNo ratings yet

- ABM19039 ABM19038 ME Assignment 2 PDFDocument10 pagesABM19039 ABM19038 ME Assignment 2 PDF255KRISHNACHOMWALNo ratings yet

- The Complete Guide to E-Commerce in the Online Food Delivery IndustryDocument9 pagesThe Complete Guide to E-Commerce in the Online Food Delivery IndustryHari HaranNo ratings yet

- Dividend Policy Analysis of Corporates of Last 10 YearsDocument6 pagesDividend Policy Analysis of Corporates of Last 10 YearsRadhika VermaNo ratings yet

- Case Study - Classmate XiaomingDocument9 pagesCase Study - Classmate XiaomingSriramVenkat0% (1)

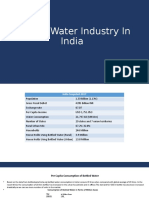

- India's Bottled Water Industry GrowthDocument17 pagesIndia's Bottled Water Industry GrowthSriramVenkat100% (1)

- Bottled WaterDocument2 pagesBottled WaterSriramVenkatNo ratings yet

- AI in Contact Centers Streamlines Customer ExperienceDocument4 pagesAI in Contact Centers Streamlines Customer ExperienceSriramVenkatNo ratings yet

- Bottled Water IndustryDocument26 pagesBottled Water IndustrySriramVenkatNo ratings yet

- AI in Contact Centers Streamlines Customer ExperienceDocument4 pagesAI in Contact Centers Streamlines Customer ExperienceSriramVenkatNo ratings yet

- Claim I CiciDocument9 pagesClaim I Cicipallavi dholeNo ratings yet

- International Trade Law: SEMESTER IX - B.A. LL.B. (Hons.) Syllabus (Session: July-December 2022)Document13 pagesInternational Trade Law: SEMESTER IX - B.A. LL.B. (Hons.) Syllabus (Session: July-December 2022)shiviNo ratings yet

- Siebel Order Management Guide PDFDocument414 pagesSiebel Order Management Guide PDFDebjyoti RakshitNo ratings yet

- Dhan Ki BaatDocument12 pagesDhan Ki Baattest hrmNo ratings yet

- UjyhDocument3 pagesUjyhditiNo ratings yet

- Are Important For Exam Purpose. This Question Bank and Questions Marked Important Herein Are JustDocument3 pagesAre Important For Exam Purpose. This Question Bank and Questions Marked Important Herein Are JustRamprakash vishwakarmaNo ratings yet

- Kaegi StatementDocument2 pagesKaegi StatementCrainsChicagoBusinessNo ratings yet

- Answer Key For MarketingDocument3 pagesAnswer Key For Marketingtammy a. romuloNo ratings yet

- Portofoliu Tradeville Mai 2023Document2 pagesPortofoliu Tradeville Mai 2023fk6dfdxjkhNo ratings yet

- ENTREPRENEURSHIP Module 1 - First SemDocument25 pagesENTREPRENEURSHIP Module 1 - First SemKarla CarbonelNo ratings yet

- List of Nodal OfficersDocument52 pagesList of Nodal OfficersSunny SinghNo ratings yet

- Paschim Gujarat Vij Co. LTD: PGVCLDocument7 pagesPaschim Gujarat Vij Co. LTD: PGVCLHardikNo ratings yet

- AR Jawattie 2019 PDFDocument233 pagesAR Jawattie 2019 PDFSyafira AdeliaNo ratings yet

- List of Contestable Customers As of February 2020Document41 pagesList of Contestable Customers As of February 2020dexterbautistadecember161985No ratings yet

- Diya GDocument45 pagesDiya GDiya goyalNo ratings yet

- TOEFL Reading Comprehension Lesson 3: Đọc đoạn văn sau và trả lời các câu hỏiDocument3 pagesTOEFL Reading Comprehension Lesson 3: Đọc đoạn văn sau và trả lời các câu hỏiThành PhạmNo ratings yet

- M&E-TOR (Rev - May2015)Document53 pagesM&E-TOR (Rev - May2015)Sara Ikhwan Nor SalimNo ratings yet

- CLTD 2022-Module 2 - APICSDocument67 pagesCLTD 2022-Module 2 - APICSΙωαννης ΠαρμακηςNo ratings yet

- Statement of Account: Date: Soa: Client Code: Account NameDocument2 pagesStatement of Account: Date: Soa: Client Code: Account NameDaisy E SolivaNo ratings yet

- Restructuring Egypt's Railways - Augst 05 PDFDocument28 pagesRestructuring Egypt's Railways - Augst 05 PDFMahmoud Abo-hashemNo ratings yet

- Survey On Customer Satisfaction of Medical Tourism in INDIA With Special Reference To Kerela StateDocument41 pagesSurvey On Customer Satisfaction of Medical Tourism in INDIA With Special Reference To Kerela Statebapunritu0% (1)

- Strategic Management GuideDocument168 pagesStrategic Management GuideShriram DawkharNo ratings yet

- Accounting & Marketing Students ListDocument9 pagesAccounting & Marketing Students ListJustine Brylle DomantayNo ratings yet

- Roshani Meghjee & Co LTD Appeal No 49 of 2008.28 Desemba 2012Document20 pagesRoshani Meghjee & Co LTD Appeal No 49 of 2008.28 Desemba 2012ismailnyungwa452No ratings yet

- Renewable Energy 2018 StatisticsDocument29 pagesRenewable Energy 2018 StatisticsJanapareddy Veerendra KumarNo ratings yet

- Aa Equipments and SuppliesDocument10 pagesAa Equipments and SuppliesAkshata BansodeNo ratings yet

- TB ch05Document25 pagesTB ch05ajaysatpadi83% (6)

- Bangladesh Leasing Industry OverviewDocument22 pagesBangladesh Leasing Industry OverviewAyesha SiddikaNo ratings yet

- FS Final OutputDocument62 pagesFS Final OutputMariael PinasoNo ratings yet

- Ingersoll RandDocument14 pagesIngersoll Randakadityakapoor100% (1)