You might also like

- Enhancing Customer Satisfaction & Efficiency through Smart Utility & DigitalizationDocument20 pagesEnhancing Customer Satisfaction & Efficiency through Smart Utility & DigitalizationSyarif HidayatNo ratings yet

- Calalang, Louise Anne E. EXAM # 1-SE533 AT P. 164 Single Degree of Freedom PropertiesDocument1,713 pagesCalalang, Louise Anne E. EXAM # 1-SE533 AT P. 164 Single Degree of Freedom PropertiesRenzel EstebanNo ratings yet

- Mapúa Institute of Technology: Analysis of Resistive Network: Series-Parallel CircuitsDocument10 pagesMapúa Institute of Technology: Analysis of Resistive Network: Series-Parallel CircuitsJohn FerreNo ratings yet

- Conceptual Integrated Science 2nd Edition Hewitt Test BankDocument19 pagesConceptual Integrated Science 2nd Edition Hewitt Test BankChristianBrownxmstk100% (21)

- VCP-W Vacuum Circuit Breakers (5/15 KV) : Price List PL01301006E1Document40 pagesVCP-W Vacuum Circuit Breakers (5/15 KV) : Price List PL01301006E1vanhalenfernando123100% (1)

- 13Document12 pages13MEOW41No ratings yet

- Power Sector OverviewDocument11 pagesPower Sector OverviewSumiran BansalNo ratings yet

- 1 s2.0 S1755008422000473 MainDocument12 pages1 s2.0 S1755008422000473 MainAshish VoraNo ratings yet

- Energy & Power Sector-2022 FinalDocument6 pagesEnergy & Power Sector-2022 FinalVernon VellozoNo ratings yet

- Climate Action in The Arab RegionDocument22 pagesClimate Action in The Arab RegionMeryemNo ratings yet

- COVID-19 IMPACT ON INDIA'S POWER SECTORDocument6 pagesCOVID-19 IMPACT ON INDIA'S POWER SECTORSurya Teja SarmaNo ratings yet

- IBEF Power SectorDocument36 pagesIBEF Power Sectorshee JNo ratings yet

- Five Trends Reshaping European Power MarketsDocument8 pagesFive Trends Reshaping European Power MarketsMurat ErkiletNo ratings yet

- Infrastructure PDF 2022Document22 pagesInfrastructure PDF 2022Juan Nicolás BarretoNo ratings yet

- Electric Decade: Challenges & OpportunitiesDocument19 pagesElectric Decade: Challenges & OpportunitiesRohit ShenoyNo ratings yet

- Performance Ratio Building in IndiaDocument23 pagesPerformance Ratio Building in IndiahatomiNo ratings yet

- ey-global-champions-for-advancing-renewable-energy-innovation-and-manufacturingDocument96 pagesey-global-champions-for-advancing-renewable-energy-innovation-and-manufacturingsayan.transcuratorsNo ratings yet

- Power Dec 2018Document36 pagesPower Dec 2018ShivaNo ratings yet

- Decarbonising - Part 4Document5 pagesDecarbonising - Part 4AVINASH YADAVNo ratings yet

- Energy Reports: Omar Ellabban, Abdulrahman AlassiDocument17 pagesEnergy Reports: Omar Ellabban, Abdulrahman AlassiFrans AdamNo ratings yet

- 02 KP Red Rev May07Document24 pages02 KP Red Rev May07nishanandNo ratings yet

- Renewable and Sustainable Energy Reviews: SciencedirectDocument12 pagesRenewable and Sustainable Energy Reviews: SciencedirectVivek SaxenaNo ratings yet

- Journal of Cleaner Production: Jagruti Thakur, Basab ChakrabortyDocument12 pagesJournal of Cleaner Production: Jagruti Thakur, Basab ChakrabortyIBHWANGNo ratings yet

- Present and Future Energy Scenario in IndiaDocument8 pagesPresent and Future Energy Scenario in IndiaRomario OinamNo ratings yet

- Electric Vehicles - Motivation & Overview at RIT by DR Vora 030122Document56 pagesElectric Vehicles - Motivation & Overview at RIT by DR Vora 030122Kamal VoraNo ratings yet

- Grid Innovation Fund Portfolio Feb 15 2019Document25 pagesGrid Innovation Fund Portfolio Feb 15 2019randiaNo ratings yet

- Indian Power Sector: Key Imperatives For TransformationDocument40 pagesIndian Power Sector: Key Imperatives For TransformationSweta DeyNo ratings yet

- New Renewable Energy Policies in Germany and Their PerspectivesDocument20 pagesNew Renewable Energy Policies in Germany and Their Perspectivesadnan widyantaraNo ratings yet

- Indian Infrastructure Power SectorDocument21 pagesIndian Infrastructure Power SectorSaurabh SumanNo ratings yet

- EnergyDocument15 pagesEnergyRand KaassamaniNo ratings yet

- Power Update March 2020Document8 pagesPower Update March 2020AshishNo ratings yet

- Qwac 087Document28 pagesQwac 087Marcelo Gustavo MolinaNo ratings yet

- Automotive Powertrain Suppliers Face A Rapidly Electrifying Future v2Document9 pagesAutomotive Powertrain Suppliers Face A Rapidly Electrifying Future v2Ananchai UkaewNo ratings yet

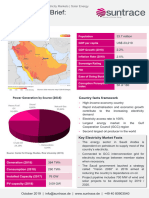

- Market_Brief_Saudi_ArabiaDocument4 pagesMarket_Brief_Saudi_ArabiaregallydivineNo ratings yet

- Wind Electricity Generation in Three States of India: Policies and StatusDocument8 pagesWind Electricity Generation in Three States of India: Policies and StatusPriya SaxenaNo ratings yet

- APICORP Energy Research V03 N13 2018Document4 pagesAPICORP Energy Research V03 N13 2018Rejith MuraleeNo ratings yet

- ENS Part 2Document70 pagesENS Part 2maazdixitNo ratings yet

- Renewable Energy in India: Industry Information Insights 2015Document14 pagesRenewable Energy in India: Industry Information Insights 2015ashutosh2009No ratings yet

- PPA - Electricity Bills in Delhi Go Up With 4% Rise in PPA Cost - The Economic TimesDocument2 pagesPPA - Electricity Bills in Delhi Go Up With 4% Rise in PPA Cost - The Economic TimesstarNo ratings yet

- June 2020: Team InfraeyeDocument10 pagesJune 2020: Team InfraeyedestinationsunilNo ratings yet

- Opportunities For Power Utilities With Electrification of TransportDocument5 pagesOpportunities For Power Utilities With Electrification of TransportAshish JainNo ratings yet

- Strategy Roadmap For Net Zero Energy Buildings in IndiaDocument27 pagesStrategy Roadmap For Net Zero Energy Buildings in IndiaRithik KarunNo ratings yet

- StudyofEnergyConsumptionPatterninResidentialNeighborhood_CaseStudyLucknowDocument9 pagesStudyofEnergyConsumptionPatterninResidentialNeighborhood_CaseStudyLucknownamankarna0No ratings yet

- 07factsheet Mini GridDocument6 pages07factsheet Mini GridSarthak ShuklaNo ratings yet

- White Paper Future Green Investments Beyond RenewablesDocument17 pagesWhite Paper Future Green Investments Beyond RenewablesantochirinNo ratings yet

- Assignment MCOMDocument12 pagesAssignment MCOMNishith GuptaNo ratings yet

- The Greenstory FinalDocument22 pagesThe Greenstory FinalNeha KhandelwalNo ratings yet

- 1 s2.0 S2352484722026841 MainDocument34 pages1 s2.0 S2352484722026841 MainYovi MaguiñaNo ratings yet

- MPPT ModellingDocument5 pagesMPPT ModellingJournalNX - a Multidisciplinary Peer Reviewed JournalNo ratings yet

- Polygeneration For An Off-Grid Indian Village - Optimization by Economic and Reliability AnalysisDocument15 pagesPolygeneration For An Off-Grid Indian Village - Optimization by Economic and Reliability AnalysisSagar KumarNo ratings yet

- Energy Usage in Vietnam and SolutionsDocument13 pagesEnergy Usage in Vietnam and SolutionsVũ Bùi TuấnNo ratings yet

- India's Action Plan for Power Sector DecarbonisationDocument28 pagesIndia's Action Plan for Power Sector DecarbonisationmihirmmbNo ratings yet

- Scrip Code: 540750 Symbol: IEX Subject: Investor Presentation & Press Release On Unaudited Financial Results For The Quarter Ended Tune 30, 2021Document43 pagesScrip Code: 540750 Symbol: IEX Subject: Investor Presentation & Press Release On Unaudited Financial Results For The Quarter Ended Tune 30, 2021shreyashankarpureNo ratings yet

- Tenaga Commitment Towards A Sustainable Future by TenagaDocument10 pagesTenaga Commitment Towards A Sustainable Future by TenagaDennis AngNo ratings yet

- Analysis of Market Characteristi Cs and Promoti On Strategy of Rooftop PVDocument103 pagesAnalysis of Market Characteristi Cs and Promoti On Strategy of Rooftop PVSonu PathakNo ratings yet

- Current Scenario of Electricity Sector in India and RestructuringDocument7 pagesCurrent Scenario of Electricity Sector in India and RestructuringIbon KatakiNo ratings yet

- PV Cell ModelingDocument12 pagesPV Cell Modelingtran duyNo ratings yet

- SolarStorageReport - JMK Research - Jan 2020 2 PDFDocument32 pagesSolarStorageReport - JMK Research - Jan 2020 2 PDFiyer34No ratings yet

- BEE Star Rating For BuildingsDocument3 pagesBEE Star Rating For BuildingsanshulNo ratings yet

- Obj Function LossDocument12 pagesObj Function LossRohit GarudNo ratings yet

- Digitalization Report Energy Management PagesDocument8 pagesDigitalization Report Energy Management PagesNetrino QuarksNo ratings yet

- Innovation Landscape brief: Behind-the-meter batteriesFrom EverandInnovation Landscape brief: Behind-the-meter batteriesNo ratings yet

- Renewable Energy Tariffs and Incentives in Indonesia: Review and RecommendationsFrom EverandRenewable Energy Tariffs and Incentives in Indonesia: Review and RecommendationsNo ratings yet

- Deployment of Hybrid Renewable Energy Systems in MinigridsFrom EverandDeployment of Hybrid Renewable Energy Systems in MinigridsNo ratings yet

- COVID-19 and Energy Sector Development in Asia and the Pacific: Guidance NoteFrom EverandCOVID-19 and Energy Sector Development in Asia and the Pacific: Guidance NoteNo ratings yet

- Alibaba Investors Gamble On Rise of 'Ecosystem Internet' in Record Breaking IPODocument3 pagesAlibaba Investors Gamble On Rise of 'Ecosystem Internet' in Record Breaking IPObajrangkaswanNo ratings yet

- Five Reasons Buffett Should Buy AlibabaDocument5 pagesFive Reasons Buffett Should Buy AlibababajrangkaswanNo ratings yet

- Amazon Is The World's Most Valuable Brand, But Alibaba and Facebook Have Better Financials - MarketWatchDocument5 pagesAmazon Is The World's Most Valuable Brand, But Alibaba and Facebook Have Better Financials - MarketWatchbajrangkaswanNo ratings yet

- Five Reasons Buffett Should Buy AlibabaDocument5 pagesFive Reasons Buffett Should Buy AlibababajrangkaswanNo ratings yet

- What Is The Likelihood of A Rise in Alibaba's StockDocument5 pagesWhat Is The Likelihood of A Rise in Alibaba's StockbajrangkaswanNo ratings yet

- Is Alibaba The Better Buy Over AmazonDocument6 pagesIs Alibaba The Better Buy Over AmazonbajrangkaswanNo ratings yet

- Alibaba's $2.8 Billion Mistake-What CFOs Should Know About Antitrust RegulationsDocument7 pagesAlibaba's $2.8 Billion Mistake-What CFOs Should Know About Antitrust RegulationsbajrangkaswanNo ratings yet

- China Imposes $2.8 BN Penalty On Jack Ma's Alibaba Group in Monopoly ProbeDocument6 pagesChina Imposes $2.8 BN Penalty On Jack Ma's Alibaba Group in Monopoly ProbebajrangkaswanNo ratings yet

- What Are The Key Sources of Revenue For AlibabaDocument3 pagesWhat Are The Key Sources of Revenue For AlibababajrangkaswanNo ratings yet

- Alibaba's Huge Browser Business Is Harvesting The Private' Web Activity of Millions of Android and Iphone UsersDocument6 pagesAlibaba's Huge Browser Business Is Harvesting The Private' Web Activity of Millions of Android and Iphone UsersbajrangkaswanNo ratings yet

- Why Jack Ma's Legacy Is Larger Than AlibabaDocument6 pagesWhy Jack Ma's Legacy Is Larger Than AlibababajrangkaswanNo ratings yet

- Reading Balance SheetDocument25 pagesReading Balance SheetbajrangkaswanNo ratings yet

- How I Did It - Jack Maa?Document4 pagesHow I Did It - Jack Maa?bajrangkaswanNo ratings yet

- Amazon vs Alibaba - Key Difference in Business ModelsDocument5 pagesAmazon vs Alibaba - Key Difference in Business ModelsbajrangkaswanNo ratings yet

- Is Alibaba The Better Buy Over Amazon?Document6 pagesIs Alibaba The Better Buy Over Amazon?bajrangkaswanNo ratings yet

- Coal Transition in IndiaDocument20 pagesCoal Transition in IndiaSaahil Hasan KhanNo ratings yet

- Fme Balance SheetDocument35 pagesFme Balance SheetMai ÊmNo ratings yet

- Optimise Pump MaintenanceDocument5 pagesOptimise Pump MaintenancebajrangkaswanNo ratings yet

- Reading Balance SheetDocument25 pagesReading Balance SheetbajrangkaswanNo ratings yet

- Phy 12th GyangangaDocument4 pagesPhy 12th GyangangabhartiyaanujNo ratings yet

- ABE 315 - Module 2 - CoursepackDocument18 pagesABE 315 - Module 2 - CoursepackRouge WintersNo ratings yet

- Parameter EstimationDocument8 pagesParameter EstimationhezugNo ratings yet

- Sample PBLDocument10 pagesSample PBLMABINI Hanna SchaneNo ratings yet

- Motion of Charged Particles in Magnetic Fields and ApplicationsDocument21 pagesMotion of Charged Particles in Magnetic Fields and ApplicationsMircea PanteaNo ratings yet

- ch5 Phy PDFDocument39 pagesch5 Phy PDFStar Packs Print SolutionNo ratings yet

- 1106Document312 pages1106Daniel MolanoNo ratings yet

- PFA 14.04.2017 Signed CRISIL Final Ver00Document122 pagesPFA 14.04.2017 Signed CRISIL Final Ver00Niraj KumarNo ratings yet

- Class 12 Physics Investigatory Project TopicsDocument2 pagesClass 12 Physics Investigatory Project TopicsRohit SharmaNo ratings yet

- 1ZSE 2750-105 en Rev 9 - Low ResDocument36 pages1ZSE 2750-105 en Rev 9 - Low ResCesar Candelaria ChavezNo ratings yet

- Solar Water PumpsDocument15 pagesSolar Water Pumpsmakaliza2005100% (1)

- Class 12 Chapterwise PYQs Shobhit NirwanDocument65 pagesClass 12 Chapterwise PYQs Shobhit NirwanHimanshu92% (13)

- Book - 2-345-423Document81 pagesBook - 2-345-423poornarithikNo ratings yet

- Resonance in RLC CircuitsDocument62 pagesResonance in RLC CircuitsAjit TripathyNo ratings yet

- Borehole No.: ABH 39 Water Table For Calculation: 6.15 M Zone Factor (Zone-III) 0.16Document4 pagesBorehole No.: ABH 39 Water Table For Calculation: 6.15 M Zone Factor (Zone-III) 0.16debapriyoNo ratings yet

- Chapter 5: Principle of ConvectionDocument45 pagesChapter 5: Principle of ConvectionA.N.M. Mominul Islam MukutNo ratings yet

- Selec 800 Xu Timer CatalogDocument1 pageSelec 800 Xu Timer CatalogfarooquesherinNo ratings yet

- INDUSTRIAL DRYERS CLASSIFICATION AND PROBLEM SOLVINGDocument26 pagesINDUSTRIAL DRYERS CLASSIFICATION AND PROBLEM SOLVINGMei Lamfao100% (1)

- Ch-2 Force & Power in Metal CuttingDocument43 pagesCh-2 Force & Power in Metal CuttingNimish JoshiNo ratings yet

- 3 Instrumentation - Bridge CircuitsDocument17 pages3 Instrumentation - Bridge CircuitsWanjala WilliamNo ratings yet

- 03 LS InverterDocument16 pages03 LS InverterNovita IndrayaniNo ratings yet

- SH203-C20 Product DetailsDocument4 pagesSH203-C20 Product DetailsBilalNo ratings yet

- Ee4020 - Insulation Co-Ordination: Level 4 - Semester 1 Examination 2008Document6 pagesEe4020 - Insulation Co-Ordination: Level 4 - Semester 1 Examination 2008Shashini VimansaNo ratings yet

- 7 Simple Ways To Find CT PolarityDocument2 pages7 Simple Ways To Find CT PolaritysrifaceNo ratings yet

- Expander Boosts Ethylene Recovery: CompressorsDocument2 pagesExpander Boosts Ethylene Recovery: Compressorsmsh16000No ratings yet