You might also like

- Cost Behaviour: Managerial Accounting Khusnul PrasetyoDocument43 pagesCost Behaviour: Managerial Accounting Khusnul PrasetyoErvian RidhoNo ratings yet

- Cost BehaviourDocument30 pagesCost Behaviourzaelani DriveNo ratings yet

- Activity Cost BehaviorDocument49 pagesActivity Cost BehaviorTheresia RumsowekNo ratings yet

- Activity Cost BehaviorDocument50 pagesActivity Cost BehavioriqbalrzzNo ratings yet

- Akuntansi ManajemenDocument31 pagesAkuntansi ManajemensafiraNo ratings yet

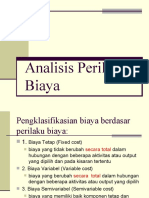

- Analisis Perilaku Biaya4Document21 pagesAnalisis Perilaku Biaya4Alfi AmaliaNo ratings yet

- Regression analysis determines key factors affecting topicDocument9 pagesRegression analysis determines key factors affecting topicaarti saxenaNo ratings yet

- Break-Even Occurs Between The Production Volume Interval of 20,000 To 30,000Document6 pagesBreak-Even Occurs Between The Production Volume Interval of 20,000 To 30,000kripsNo ratings yet

- Illustration1: For The Production of 10000 Units of A Product, The Following Are The Budgeted ExpensesDocument4 pagesIllustration1: For The Production of 10000 Units of A Product, The Following Are The Budgeted ExpensesGabriel BelmonteNo ratings yet

- Department A Cost Analysis and Profitability CalculationsDocument8 pagesDepartment A Cost Analysis and Profitability CalculationsRica PresbiteroNo ratings yet

- DR Rachna Mahalwla - B.Com III Year Management Accounting Flexible BudgetingDocument6 pagesDR Rachna Mahalwla - B.Com III Year Management Accounting Flexible BudgetingSaumya JainNo ratings yet

- Direct Materials Consumed Direct Wages: Particulars Per Unit AmountDocument6 pagesDirect Materials Consumed Direct Wages: Particulars Per Unit AmountYaduNo ratings yet

- Activity Cost BehaviorDocument28 pagesActivity Cost Behaviorangel caoNo ratings yet

- Problems: Fixed Costs BE PR Ice-Variable Cost Per UnitDocument7 pagesProblems: Fixed Costs BE PR Ice-Variable Cost Per UnitPercy JacksonNo ratings yet

- KASUS 6-1: Nomor. 1 PerhitunganDocument21 pagesKASUS 6-1: Nomor. 1 PerhitunganMeita PutriNo ratings yet

- Exhibit 2 Product Class Cost Analysis (Normal Year) : Units UnitsDocument6 pagesExhibit 2 Product Class Cost Analysis (Normal Year) : Units UnitsSangtani PareshNo ratings yet

- Yolla Ervira - 4112101105 - Tugas3Document6 pagesYolla Ervira - 4112101105 - Tugas3advokesmahmmbNo ratings yet

- OjoylanJenny - Charmingly (Case#5)Document5 pagesOjoylanJenny - Charmingly (Case#5)Jenny Ojoylan100% (1)

- Citra Dewi - 4112001008 - AM 4A Pagi - Study Case Chapter 4Document16 pagesCitra Dewi - 4112001008 - AM 4A Pagi - Study Case Chapter 4Citra DewiNo ratings yet

- Cost Analysis of Production Units from 8000 to 14000 with Managerial ImplicationsDocument5 pagesCost Analysis of Production Units from 8000 to 14000 with Managerial ImplicationsrajyalakshmiNo ratings yet

- Class Case 6 - Charmingly, Personalli, YoursDocument5 pagesClass Case 6 - Charmingly, Personalli, Yours9ry5gsghybNo ratings yet

- Absorption Costing QuestionsDocument6 pagesAbsorption Costing Questions田淼No ratings yet

- Accounts - FIFO and WA For FinalDocument11 pagesAccounts - FIFO and WA For FinalRohan SinghNo ratings yet

- Negocio de Palomitas de JasonDocument11 pagesNegocio de Palomitas de JasonElizabeth Sanabria AriasNo ratings yet

- Budgetory Control Flexible Budget With SolutionsDocument6 pagesBudgetory Control Flexible Budget With SolutionsJash SanghviNo ratings yet

- 15 Marginal Costing PDFDocument14 pages15 Marginal Costing PDFSupriyoNo ratings yet

- Master Minds CA/CWA & MEC/CEC marginal costing solutionsDocument14 pagesMaster Minds CA/CWA & MEC/CEC marginal costing solutionsHaresh KNo ratings yet

- Fa3 ExcelDocument6 pagesFa3 ExcelGretchen MontoyaNo ratings yet

- Anjani Risa Pratiwi - 1801035213 - SPM AK-A-dikonversiDocument14 pagesAnjani Risa Pratiwi - 1801035213 - SPM AK-A-dikonversiAnjani RisaNo ratings yet

- 2) Solution To Problem No 2 On Flexible BudgetDocument7 pages2) Solution To Problem No 2 On Flexible BudgetVikas guptaNo ratings yet

- CH 10 SolDocument7 pagesCH 10 SolNotty SingerNo ratings yet

- Kasus 6-1Document20 pagesKasus 6-1Anggia CahyaningNo ratings yet

- Solutions Chapter 5Document13 pagesSolutions Chapter 5Laila Al Suwaidi100% (2)

- Cox Electric Breakeven Analysis Inputs: One-Way Data TableDocument2 pagesCox Electric Breakeven Analysis Inputs: One-Way Data TablegieNo ratings yet

- Cox Electric Breakeven Analysis Inputs: One-Way Data TableDocument2 pagesCox Electric Breakeven Analysis Inputs: One-Way Data TablegieNo ratings yet

- Kasus 6-1 - Jihan NabilahDocument21 pagesKasus 6-1 - Jihan Nabilahalesha nindyaNo ratings yet

- Constructing A Downtown Parking Lot in DraperDocument7 pagesConstructing A Downtown Parking Lot in DraperWater MelonNo ratings yet

- Activity Based Costing AnalysisDocument3 pagesActivity Based Costing AnalysistutiNo ratings yet

- ABC Costing System Design StepsDocument25 pagesABC Costing System Design StepsMochamad PutraNo ratings yet

- Case Study Whitney Narrative - Jarina and SanapDocument2 pagesCase Study Whitney Narrative - Jarina and SanapJefferson JarinaNo ratings yet

- 20123400024Document7 pages20123400024Phạm Công KiênNo ratings yet

- Full Absorption & Variable Costing Methods (Answers)Document3 pagesFull Absorption & Variable Costing Methods (Answers)Juan FrivaldoNo ratings yet

- MVV - Assignment 1 - ManyaDocument14 pagesMVV - Assignment 1 - ManyaManya SrivastavaNo ratings yet

- Zepher memoDocument2 pagesZepher memoewriteandread.businessNo ratings yet

- Break-Even Analysis Example Excel-TemplateDocument8 pagesBreak-Even Analysis Example Excel-TemplateFernando FlorNo ratings yet

- Tugas ABC PDFDocument4 pagesTugas ABC PDFtutiNo ratings yet

- CVP analysis: Cost-volume-profit analysis guideDocument21 pagesCVP analysis: Cost-volume-profit analysis guiderangoli maheshwariNo ratings yet

- SCM Lec 2Document67 pagesSCM Lec 2Star KerenzaNo ratings yet

- MAE RevisionDocument57 pagesMAE RevisionsaloniNo ratings yet

- Asistensi Akmen Ch.8Document12 pagesAsistensi Akmen Ch.8Irham SistiasyaNo ratings yet

- Study Unit 1- Cost behaviourDocument36 pagesStudy Unit 1- Cost behaviourjoseswartzsr31No ratings yet

- Solution Practice Problems On Differential CostingDocument7 pagesSolution Practice Problems On Differential CostingAkhil NarangNo ratings yet

- Performance Management 41 - Team 1-Hau PHAM - W4Document4 pagesPerformance Management 41 - Team 1-Hau PHAM - W4Phạm Như HậuNo ratings yet

- Solution MaNUALDocument14 pagesSolution MaNUALanasbadboy10No ratings yet

- Project Analysis (NPV)Document20 pagesProject Analysis (NPV)EW1587100% (1)

- Statistics Notes in The British Medical Journal (Bland JM, Altman DG. - NEJ)Document95 pagesStatistics Notes in The British Medical Journal (Bland JM, Altman DG. - NEJ)pegazus_arNo ratings yet

- Talaid Midterm Exam Bem 109Document2 pagesTalaid Midterm Exam Bem 109Elison AngelesNo ratings yet

- 16a. Meta-Analysis - FAITH ToolDocument4 pages16a. Meta-Analysis - FAITH ToolGhany Hendra WijayaNo ratings yet

- Psy524 FinalDocument20 pagesPsy524 FinalWan QENo ratings yet

- Probability Assignment 2Document2 pagesProbability Assignment 2Vijay KumarNo ratings yet

- A Guide to Statistical Methods for Hydrology AnalysisDocument27 pagesA Guide to Statistical Methods for Hydrology AnalysisJohn E Cutipa LNo ratings yet

- Lab 10 WorksheetDocument3 pagesLab 10 WorksheetPohuyist100% (1)

- Week05 - Naive Bayes Tutorial - SolutionsDocument23 pagesWeek05 - Naive Bayes Tutorial - SolutionsRawaf FahadNo ratings yet

- CH 10Document125 pagesCH 10Lisset Soraya Huamán QuispeNo ratings yet

- Exponential Independent Joint Order PDF StatisticsDocument2 pagesExponential Independent Joint Order PDF StatisticsJoeNo ratings yet

- Statistics Module S3: GCE ExaminationsDocument4 pagesStatistics Module S3: GCE ExaminationskrackyournutNo ratings yet

- Data PenjualanDocument8 pagesData PenjualanK PNo ratings yet

- Critical Values For The Durbin-Watson Test: 5% Significance LevelDocument11 pagesCritical Values For The Durbin-Watson Test: 5% Significance Levelvito npNo ratings yet

- Forecasting TechniquesDocument7 pagesForecasting TechniquesaruunstalinNo ratings yet

- Rainfall Homogenity TestDocument13 pagesRainfall Homogenity Testanon_823275197No ratings yet

- BootstrapDocument10 pagesBootstrapLuis IglesiasNo ratings yet

- Q4 Formulating Hypothesis 2Document18 pagesQ4 Formulating Hypothesis 2Rhonalyn Angel GalanoNo ratings yet

- Chap 8 MathscapeDocument53 pagesChap 8 MathscapeHarry LiuNo ratings yet

- AutocorrelationDocument49 pagesAutocorrelationBenazir Rahman0% (1)

- B11Document20 pagesB11smilesprn100% (1)

- Pengaruh Pelatihan Dan Pengembangan Sumber Daya Manusia Terhadap Kinerja Karyawan PT Dirgantara Indonesia (Persero) BandungDocument7 pagesPengaruh Pelatihan Dan Pengembangan Sumber Daya Manusia Terhadap Kinerja Karyawan PT Dirgantara Indonesia (Persero) BandungWilliam FelixNo ratings yet

- Pengaruh Penerapan Akuntansi Sektor Publik Dan Pengawasan Internal Terhadap Kualitass Laporan Keuangan Dinas Perhubungan Kota SemrangDocument16 pagesPengaruh Penerapan Akuntansi Sektor Publik Dan Pengawasan Internal Terhadap Kualitass Laporan Keuangan Dinas Perhubungan Kota SemrangSitti MarhamaNo ratings yet

- Assignment 2 - Composite WACCDocument31 pagesAssignment 2 - Composite WACCIzzah IkramNo ratings yet

- Test of Hypothesis FinalDocument7 pagesTest of Hypothesis Finalaliyah regacho100% (1)

- J. K. Shah Classes Sampling Theory and Theory of EstimationDocument37 pagesJ. K. Shah Classes Sampling Theory and Theory of EstimationGautamNo ratings yet

- Rr220105 Probability and StatisticsDocument10 pagesRr220105 Probability and StatisticsandhracollegesNo ratings yet

- FreqDistS13Slides PDFDocument112 pagesFreqDistS13Slides PDFAmit PoddarNo ratings yet

- Econmetrics - EC4061: t t t−1 0 t t−1 t 2 εDocument2 pagesEconmetrics - EC4061: t t t−1 0 t t−1 t 2 εKabeloNo ratings yet

- Note: No Additional Answer Sheets Will Be Provided.: Probability and Statistics For It (It)Document2 pagesNote: No Additional Answer Sheets Will Be Provided.: Probability and Statistics For It (It)zzzzzNo ratings yet

- Confirmatory Factor Analysis of The Multi-Attitude Suicide Tendency ScaleDocument14 pagesConfirmatory Factor Analysis of The Multi-Attitude Suicide Tendency ScaleEmiNo ratings yet