You might also like

- The Balanced Scorecard (Review and Analysis of Kaplan and Norton's Book)From EverandThe Balanced Scorecard (Review and Analysis of Kaplan and Norton's Book)Rating: 4 out of 5 stars4/5 (2)

- 02 - Vision, Mission, Objectives, and StrategyDocument15 pages02 - Vision, Mission, Objectives, and StrategyAyushi GargNo ratings yet

- Strategic Balanced Management ScorecardDocument34 pagesStrategic Balanced Management ScorecardKumar ManojNo ratings yet

- Strategy: Five Aspects of Industry AnalysisDocument7 pagesStrategy: Five Aspects of Industry AnalysisAce AceNo ratings yet

- BS ReviewerDocument13 pagesBS ReviewerXyla Marie EstorNo ratings yet

- Balance ScorecardDocument25 pagesBalance ScorecardJia BarrientosNo ratings yet

- Balance Scorecard 11Document46 pagesBalance Scorecard 11Pradee Srinivas GowdaNo ratings yet

- Balanced Scorecard Measures Drive PerformanceDocument15 pagesBalanced Scorecard Measures Drive PerformanceSampat MishraNo ratings yet

- BS Session 1-2Document23 pagesBS Session 1-2Kshitij SharmaNo ratings yet

- 5 Strategic ManagementDocument27 pages5 Strategic ManagementM. Fandyaz KusdianaNo ratings yet

- Balanced Scorecard: Your Company NameDocument32 pagesBalanced Scorecard: Your Company NameSheika SuhailNo ratings yet

- Strategy, Balanced Scorecard and Strategic Profitability AnalysisDocument16 pagesStrategy, Balanced Scorecard and Strategic Profitability AnalysisLưu Hồng Hạnh 4KT-20ACNNo ratings yet

- MSR Strategic Management - 8Document108 pagesMSR Strategic Management - 8AniketkumarNo ratings yet

- Balanced ScorecardDocument72 pagesBalanced ScorecardBalaji Sekar100% (1)

- Balance ScorecardDocument25 pagesBalance Scorecardnikko.emping.20No ratings yet

- Balanced Scorecard 2Document45 pagesBalanced Scorecard 2Balaji SekarNo ratings yet

- MBA Strategic Management ConceptsDocument183 pagesMBA Strategic Management ConceptsNijil JayanNo ratings yet

- Strategic MGMT Chapter 5Document28 pagesStrategic MGMT Chapter 5tewodrosNo ratings yet

- BSG Chpter 4 PDFDocument25 pagesBSG Chpter 4 PDFAgnes KpatinkpoNo ratings yet

- Ch 5- Strategic Mgmt in ActionDocument28 pagesCh 5- Strategic Mgmt in ActionabateNo ratings yet

- Marketing ControlDocument9 pagesMarketing ControlcutegitssNo ratings yet

- Marketing ControlDocument9 pagesMarketing ControlcutegitssNo ratings yet

- SM 5Document28 pagesSM 5Endalkachew Abebe KassuNo ratings yet

- Sir M Visvesvaraya Institute of Management StudiesDocument32 pagesSir M Visvesvaraya Institute of Management StudiesMonil VisariyaNo ratings yet

- Strategic Management and The EntrepreneurDocument16 pagesStrategic Management and The EntrepreneurRaheel MansoorNo ratings yet

- Balanced ScorecardDocument38 pagesBalanced ScorecardJuliana ChavezNo ratings yet

- Models of Improving Operations: Chapter EightDocument35 pagesModels of Improving Operations: Chapter EightAbdiNo ratings yet

- Non-Financial Performance MeasuresDocument41 pagesNon-Financial Performance MeasuresSandeep SonawaneNo ratings yet

- Teaching Strategic Management ProcessDocument37 pagesTeaching Strategic Management ProcessRavi GuptaNo ratings yet

- Balance Scorecard of TcsDocument17 pagesBalance Scorecard of TcsKrishna Chaitanya100% (2)

- Balanced Scorecard: Amara Reboan SharingDocument29 pagesBalanced Scorecard: Amara Reboan Sharingwindra herintyokoNo ratings yet

- Chapter-1 Imperatives For Market Driven StrategyDocument11 pagesChapter-1 Imperatives For Market Driven Strategysajid bhattiNo ratings yet

- 2023 SMA Lecture 10Document47 pages2023 SMA Lecture 10Haniie NguyenNo ratings yet

- Managing Corporate Performance with Balanced ScorecardDocument45 pagesManaging Corporate Performance with Balanced ScorecardHery KurniawanNo ratings yet

- Presentasi Balanced ScorecardDocument43 pagesPresentasi Balanced Scorecardvivi vidya100% (1)

- Implementing Strategies: Marketing, Finance, R&D, and MIS IssuesDocument22 pagesImplementing Strategies: Marketing, Finance, R&D, and MIS IssuesFelicia MonikaNo ratings yet

- Week 3 Strategic Marketing PlanningDocument34 pagesWeek 3 Strategic Marketing PlanningMuhammad AsifNo ratings yet

- Strategic ManagementDocument9 pagesStrategic ManagementAmruta GholbaNo ratings yet

- BFT 509 Accounting for Business Performance Measurement SystemDocument22 pagesBFT 509 Accounting for Business Performance Measurement SystemtcsNo ratings yet

- Strategic PlanningDocument31 pagesStrategic PlanningNURUL QAMARINA AINA' ROZAIMINo ratings yet

- Bee Performance Management Systems ComparedDocument21 pagesBee Performance Management Systems ComparedJigar PatelNo ratings yet

- Trabajo Empresa OrganizationDocument13 pagesTrabajo Empresa OrganizationMishelle Beltran BravoNo ratings yet

- Balanced Scorecard BSC Strategy Map TemplateDocument37 pagesBalanced Scorecard BSC Strategy Map TemplateDereje Woldemichael100% (1)

- L09 Strategic Management Accounting BSC BPR Bench - BSC202401Document54 pagesL09 Strategic Management Accounting BSC BPR Bench - BSC202401Jason TeohNo ratings yet

- Balance Score CardDocument61 pagesBalance Score CardmadhurbvmNo ratings yet

- Customer Market StrategyDocument8 pagesCustomer Market StrategyRahul MandalNo ratings yet

- Managing Corporate Performance with Balanced ScorecardDocument83 pagesManaging Corporate Performance with Balanced ScorecardT Ferdinand S Lumbantobing100% (1)

- Business PlanningDocument36 pagesBusiness PlanningMa. Alene MagdaraogNo ratings yet

- Managing Corporate Performance With Balanced ScorecardDocument13 pagesManaging Corporate Performance With Balanced ScorecardMihir100% (1)

- Fresh Market Business Plan by SlidesgoDocument40 pagesFresh Market Business Plan by Slidesgochizziecheese09No ratings yet

- Steps 2 and 3 Combined Are Called A Swot Analysis. (Strengths, Weaknesses, Opportunities, and Threats)Document6 pagesSteps 2 and 3 Combined Are Called A Swot Analysis. (Strengths, Weaknesses, Opportunities, and Threats)Samuel ArgoteNo ratings yet

- Marketing Planning Process: Prepared By: Ashish Manchanda (07337) Binita Vaidya (07340) Mba - Term Ii KusomDocument21 pagesMarketing Planning Process: Prepared By: Ashish Manchanda (07337) Binita Vaidya (07340) Mba - Term Ii KusomVipin PatilNo ratings yet

- Five Generic StrategiesDocument42 pagesFive Generic Strategiesanon_938204859No ratings yet

- SOPDocument44 pagesSOPDian SugiartoNo ratings yet

- Operations Management For Hospitality ManagemenDocument41 pagesOperations Management For Hospitality ManagemenAngelo Chistian OreñadaNo ratings yet

- LESSON 2 TG 9 Sept 2019Document24 pagesLESSON 2 TG 9 Sept 2019sutresna arintoNo ratings yet

- The Balanced Scorecard ApproachDocument27 pagesThe Balanced Scorecard Approachilsen100% (1)

- Managerial Accounting & Business EnvironmentDocument80 pagesManagerial Accounting & Business EnvironmentKhinwai HoNo ratings yet

- Fresh Market Business Plan by SlidesgoDocument40 pagesFresh Market Business Plan by SlidesgoHuong Hoang DieuNo ratings yet

- Balanced ScorecardDocument13 pagesBalanced ScorecardRajiv NatarajNo ratings yet

- Transfer Pricing: Rodelio S. RoqueDocument19 pagesTransfer Pricing: Rodelio S. Roqueterrence jacob diamaNo ratings yet

- Capital Budgeting ConceptsDocument61 pagesCapital Budgeting Conceptsterrence jacob diamaNo ratings yet

- Transfer Pricing: Rodelio S. RoqueDocument19 pagesTransfer Pricing: Rodelio S. Roqueterrence jacob diamaNo ratings yet

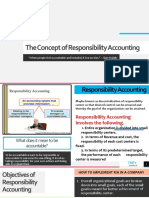

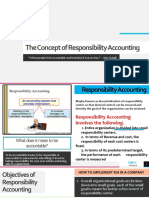

- The Concept of Responsibility AccountingDocument18 pagesThe Concept of Responsibility Accountingterrence jacob diamaNo ratings yet

- Capital Budgeting ConceptsDocument61 pagesCapital Budgeting Conceptsterrence jacob diamaNo ratings yet

- Strategic Cost Management and Balance ScorecardDocument51 pagesStrategic Cost Management and Balance Scorecardterrence jacob diamaNo ratings yet

- The Concept of Responsibility Accounting: "When People Feel Accountable and Included, It Is More Fun." - Alan MulallyDocument18 pagesThe Concept of Responsibility Accounting: "When People Feel Accountable and Included, It Is More Fun." - Alan Mulallyterrence jacob diamaNo ratings yet

- HIRARCDocument13 pagesHIRARCfaizNo ratings yet

- Resume Jessica Sánchez MierDocument1 pageResume Jessica Sánchez MierJessica MierNo ratings yet

- Chapter 2, Leadership For TQMDocument32 pagesChapter 2, Leadership For TQMRameez Ramzan Ali88% (24)

- Pay Scales - 01 Apr 2022 - 31 Mar 2023 V3Document1 pagePay Scales - 01 Apr 2022 - 31 Mar 2023 V3Laurence ParkinsonNo ratings yet

- MTP April 2019 Cost & Management AnswersDocument15 pagesMTP April 2019 Cost & Management AnswersAisha MalhotraNo ratings yet

- Introduction To AccountingDocument12 pagesIntroduction To AccountingJasmine SainiNo ratings yet

- Iso 9001 2015Document1 pageIso 9001 2015kafi piyalNo ratings yet

- Operations Strategy in A Global EnvironmentDocument17 pagesOperations Strategy in A Global EnvironmentjacobblackNo ratings yet

- Manage and Maintain Small Business OperationDocument155 pagesManage and Maintain Small Business OperationRafez JoneNo ratings yet

- ISO 9000 VS 9001 ADocument2 pagesISO 9000 VS 9001 AJanieNo ratings yet

- Time Value of Money &capital Budgeting DecisionsDocument13 pagesTime Value of Money &capital Budgeting DecisionspreetiNo ratings yet

- Unlocking The Productivity CodeDocument42 pagesUnlocking The Productivity CodeTechmanJNo ratings yet

- Publix Invoice for Fresh Produce ShipmentDocument1 pagePublix Invoice for Fresh Produce ShipmentArmando BroncasNo ratings yet

- CB Lesson 2Document35 pagesCB Lesson 2Deche TevesNo ratings yet

- Engagement EmployeeDocument19 pagesEngagement EmployeeMeryem HARMAZNo ratings yet

- Sly Landscaping Company RevisedDocument32 pagesSly Landscaping Company Revisedlex tecNo ratings yet

- Pt. Rekayasa Industri: Subcontractor Hse Key Performance Indicator Health Safety & EnvironmentDocument5 pagesPt. Rekayasa Industri: Subcontractor Hse Key Performance Indicator Health Safety & EnvironmentDondy Zobitana100% (1)

- 2008 - Boon, K., McKinnon, J., & Ross, P. Audit Service Quality in Compulsory Audit TenderingDocument32 pages2008 - Boon, K., McKinnon, J., & Ross, P. Audit Service Quality in Compulsory Audit TenderingTâm Nguyễn NgọcNo ratings yet

- Portfolio Evaluation: Hap Te RDocument18 pagesPortfolio Evaluation: Hap Te RGauravNo ratings yet

- Introduction to Quality Assurance in the Analytical Chemistry LaboratoryDocument25 pagesIntroduction to Quality Assurance in the Analytical Chemistry LaboratoryLily ERc Peter100% (3)

- PFIP21220001666 - 1152021 - PT. Megahlestari Printing PackindoDocument7 pagesPFIP21220001666 - 1152021 - PT. Megahlestari Printing PackindoJumairyNo ratings yet

- Dave BrothersDocument6 pagesDave BrothersSangtani PareshNo ratings yet

- Sa 7918 2Document2 pagesSa 7918 2junaid ShahNo ratings yet

- 5 General Spec SAWS Small Caliber Ammunition 1 January 2019Document18 pages5 General Spec SAWS Small Caliber Ammunition 1 January 2019BotondNo ratings yet

- Supply Chain Management at Cattle Feedlot CompanyDocument3 pagesSupply Chain Management at Cattle Feedlot CompanyAmanda Viona Shafitri 3006No ratings yet

- PublicationsDocument2 pagesPublicationsSava KovacevicNo ratings yet

- Feedwater LCA Statement of ComplianceDocument5 pagesFeedwater LCA Statement of ComplianceTarundeep Singh100% (1)

- Nature of OrganizationDocument4 pagesNature of Organizationravikaran123100% (1)

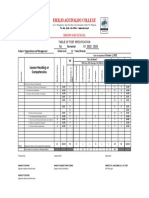

- Table of Test Specifications SY 2022 2023Document1 pageTable of Test Specifications SY 2022 2023Leomar CabandayNo ratings yet

- Eastern Refinery Limited Eastern Refinery LimitedDocument1 pageEastern Refinery Limited Eastern Refinery LimitedMuntasir MunirNo ratings yet