You might also like

- Understanding Cryptocurrencies: Bitcoin, Ethereum, and Altcoins As An Asset ClassDocument24 pagesUnderstanding Cryptocurrencies: Bitcoin, Ethereum, and Altcoins As An Asset ClassCharlene KronstedtNo ratings yet

- The Shadow Money Lenders - Significance of Fed's Zirp PolicyDocument8 pagesThe Shadow Money Lenders - Significance of Fed's Zirp Policyasksigma6No ratings yet

- Session 4 - GPB & GAD ARDocument35 pagesSession 4 - GPB & GAD ARDr. Jose N. Rodriguez Memorial Medical CenterNo ratings yet

- Practical Test 5 CesweDocument49 pagesPractical Test 5 CesweNenbon NatividadNo ratings yet

- Barangay transparency monitoring form titleDocument1 pageBarangay transparency monitoring form titleOmar Dizon100% (1)

- BSP Banking RegulationDocument26 pagesBSP Banking RegulationGrace G. ServanoNo ratings yet

- Wages and Salary AdministrationDocument20 pagesWages and Salary AdministrationChhaiyaAgrawal100% (2)

- Practical Test 3Document36 pagesPractical Test 3Nenbon NatividadNo ratings yet

- WillaWare v Jesichris ManufacturingDocument2 pagesWillaWare v Jesichris ManufacturingloschudentNo ratings yet

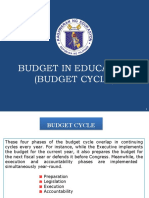

- Budget CycleDocument75 pagesBudget CycleNenbon NatividadNo ratings yet

- Science 10 LAS Quarter 3Document89 pagesScience 10 LAS Quarter 3Christopher John Natividad100% (3)

- Science 10 LAS Quarter 3Document89 pagesScience 10 LAS Quarter 3Christopher John Natividad100% (3)

- Report Budget Preparation and DeliberationDocument27 pagesReport Budget Preparation and DeliberationChristine CerdaNo ratings yet

- Authority To Sell ExtensionDocument1 pageAuthority To Sell ExtensionPaul BaesNo ratings yet

- BPE 112 ModuleDocument193 pagesBPE 112 Modulelorence caneteNo ratings yet

- LABOR STANDARDS REVIEW MCQDocument5 pagesLABOR STANDARDS REVIEW MCQLiza MelgarNo ratings yet

- Complete Notes HRMDocument114 pagesComplete Notes HRMT S Kumar KumarNo ratings yet

- RPMS Design 3Document23 pagesRPMS Design 3Nenbon NatividadNo ratings yet

- Budget Execution, Monitoring and Reporting of Government AccountingDocument13 pagesBudget Execution, Monitoring and Reporting of Government AccountingKathleenNo ratings yet

- Brigada Eskwela 2023 2024 Form 2 School Action Plan RepairedDocument10 pagesBrigada Eskwela 2023 2024 Form 2 School Action Plan RepairedNenbon Natividad100% (1)

- Land Titling Issues in the PhilippinesDocument4 pagesLand Titling Issues in the Philippinesjimmy2019No ratings yet

- Course Syllabus Marketing MGMTDocument7 pagesCourse Syllabus Marketing MGMTNasser Dugasan100% (1)

- Financing Education As Administrative FunctionDocument27 pagesFinancing Education As Administrative Function0717 CartNo ratings yet

- Fiscal Managemant Day 1Document90 pagesFiscal Managemant Day 1C.j. TenorioNo ratings yet

- FINAL 03 Accelerating The DCP Amid The Pandemic 0921023 20210903 2Document17 pagesFINAL 03 Accelerating The DCP Amid The Pandemic 0921023 20210903 2Philip John IlaoNo ratings yet

- The Civil Service Commission and The Salient Features of Ra 6713Document11 pagesThe Civil Service Commission and The Salient Features of Ra 6713Anthea Dominique SanchezNo ratings yet

- Balingasag Briefer Policy AdvocacyDocument14 pagesBalingasag Briefer Policy AdvocacySerge Adever CuaNo ratings yet

- Case Related To TESDADocument15 pagesCase Related To TESDAsilv3rw0lfNo ratings yet

- CHAPTER 4 AutoRecoveredDocument90 pagesCHAPTER 4 AutoRecoveredjohn johnNo ratings yet

- Financial SystemsDocument41 pagesFinancial SystemsAbhinabNo ratings yet

- Teaching GeographyDocument6 pagesTeaching GeographyazeNo ratings yet

- Final Pro-Forma Opcr 3-3-22Document16 pagesFinal Pro-Forma Opcr 3-3-22Abraham JunioNo ratings yet

- Pfmat IntroDocument12 pagesPfmat IntroBernNo ratings yet

- ACT1110 Governance, Business Ethics, Risk Management, and Internal Control - Summer - FINALDocument9 pagesACT1110 Governance, Business Ethics, Risk Management, and Internal Control - Summer - FINALJules TNo ratings yet

- School Memos 2022 2023Document22 pagesSchool Memos 2022 2023Hazel Dela PeñaNo ratings yet

- MODULE 4 Profit Planning - BudgetingDocument30 pagesMODULE 4 Profit Planning - BudgetingNil Justeen GarciaNo ratings yet

- Changes in Personnel StatusDocument16 pagesChanges in Personnel StatusMASSO CALINTAAN100% (1)

- Pamantasan NG Cabuyao: The Problem and Its BackgroundDocument155 pagesPamantasan NG Cabuyao: The Problem and Its Backgroundpnc RequirementsNo ratings yet

- Thesis Manuscript 1.5Document72 pagesThesis Manuscript 1.5Aljon Andol OrtegaNo ratings yet

- Planning CycleDocument25 pagesPlanning CycleJennifer OestarNo ratings yet

- Capital Structure, Capitalisation and LeverageDocument53 pagesCapital Structure, Capitalisation and LeverageCollins NyendwaNo ratings yet

- Aip FormDocument80 pagesAip FormNelette JumawanNo ratings yet

- 09 BIR Stand On Cooperative CTEDocument52 pages09 BIR Stand On Cooperative CTEClaudio Jr OlaritaNo ratings yet

- Your Results For: "Multiple-Choice Questions: B"Document4 pagesYour Results For: "Multiple-Choice Questions: B"Ravi SatyapalNo ratings yet

- DLL Math Grade1 Quarter2 Week6 (Palawan Division)Document5 pagesDLL Math Grade1 Quarter2 Week6 (Palawan Division)STEPHANIE RELATADONo ratings yet

- Annex C AO II Job DescriptionDocument3 pagesAnnex C AO II Job Descriptionmrol dela cruzNo ratings yet

- Accomplishment of Long-Term Projects Towards Ambisyon Natin 2040 and Sustainable Development Goal "ALPAS" FrameworkDocument45 pagesAccomplishment of Long-Term Projects Towards Ambisyon Natin 2040 and Sustainable Development Goal "ALPAS" FrameworkNFAR1 ORM100% (1)

- Test Bank MID CH 1234 Laith Bushnaq SERVICEDocument18 pagesTest Bank MID CH 1234 Laith Bushnaq SERVICEahdhib jwNo ratings yet

- Tax Exempt de Minimis Benefits Under TRAIN RA 10963 Philippines - Tax and Accounting Center, Inc.Document7 pagesTax Exempt de Minimis Benefits Under TRAIN RA 10963 Philippines - Tax and Accounting Center, Inc.Nicale JeenNo ratings yet

- A Case Study About The Naia Expressway ProjectDocument24 pagesA Case Study About The Naia Expressway ProjectAngel YuNo ratings yet

- Safe Space ActDocument40 pagesSafe Space Actdilg baniNo ratings yet

- SODPRMDP-Makaguro Loans (1) (2) (1) - 1Document13 pagesSODPRMDP-Makaguro Loans (1) (2) (1) - 1MaximusNo ratings yet

- Project - Research and DevelopmentDocument9 pagesProject - Research and DevelopmentNasser DugasanNo ratings yet

- 1globe Telecom Inc Chap 3Document6 pages1globe Telecom Inc Chap 3John Cedrick TaguibaoNo ratings yet

- Checklist of Requirements and Omnibus Sworn StatementDocument1 pageChecklist of Requirements and Omnibus Sworn StatementMarenz FerrerNo ratings yet

- 45 Key InitiativesDocument2 pages45 Key InitiativesCoLavs Avenue100% (1)

- Research Planning EilaneDocument26 pagesResearch Planning EilaneEilane Dabi-SilverioNo ratings yet

- Correlation Between Accountancy Student Performance and Board Exam ResultsDocument17 pagesCorrelation Between Accountancy Student Performance and Board Exam Resultskarl cruzNo ratings yet

- LITE ReviewerDocument14 pagesLITE ReviewerJanna Alyana CuaresmaNo ratings yet

- Accounting For VAT in Th... Accounting Center, Inc.Document4 pagesAccounting For VAT in Th... Accounting Center, Inc.Martin EspinosaNo ratings yet

- DepEd Educator Requests Leave for TrainingDocument3 pagesDepEd Educator Requests Leave for TrainingCharity Anne Camille PenalozaNo ratings yet

- 2022 Updates From The PEAC 1Document69 pages2022 Updates From The PEAC 1Jude MontoyaNo ratings yet

- CDA-OJT Manual (August2018) StudentEd PDFDocument31 pagesCDA-OJT Manual (August2018) StudentEd PDFJohnelle Ashley Baldoza TorresNo ratings yet

- OUA Memo 1221030 Google Workspace Training Program 2021.12.06 1Document8 pagesOUA Memo 1221030 Google Workspace Training Program 2021.12.06 1jesper tabarNo ratings yet

- Cultural Clothing Hybridization Among BSU StudentsDocument71 pagesCultural Clothing Hybridization Among BSU StudentsJoseph MagsinoNo ratings yet

- Daily Lesson Log for MathematicsDocument10 pagesDaily Lesson Log for MathematicsLorefe Delos SantosNo ratings yet

- AIP Operations GuideDocument147 pagesAIP Operations Guidevarachartered283No ratings yet

- 1.1 Budgeting in Public Sector - Micaela GuerzoDocument50 pages1.1 Budgeting in Public Sector - Micaela GuerzoSahra PajarillaNo ratings yet

- Magna Carta .Ra 4670Document38 pagesMagna Carta .Ra 4670SkyNayvieNo ratings yet

- UNIT 1 Business EthicsDocument29 pagesUNIT 1 Business EthicsOlive AsuncionNo ratings yet

- Impact of Financial Statements To The Decision-Making of Small and Medium EnterprisesDocument108 pagesImpact of Financial Statements To The Decision-Making of Small and Medium EnterprisesJanna Mari FriasNo ratings yet

- CSE SES SY 2022 2023 Implementation PlanDocument5 pagesCSE SES SY 2022 2023 Implementation PlanRizalina LaysonNo ratings yet

- RAPANAN, MIKAELA S. - School FinanceDocument7 pagesRAPANAN, MIKAELA S. - School FinanceMika RapananNo ratings yet

- C Drift Seafloor PPT 2010Document21 pagesC Drift Seafloor PPT 2010Nenbon NatividadNo ratings yet

- 1ST Mod. DLL 3RD QRTR G9Document5 pages1ST Mod. DLL 3RD QRTR G9Nenbon NatividadNo ratings yet

- BE Form 2 SCHOOL WORK PLANDocument2 pagesBE Form 2 SCHOOL WORK PLANNenbon NatividadNo ratings yet

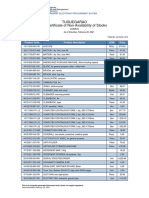

- Tuguegarao Certificate of Non-Availability of Stocks: Product Code Product Description UOM PriceDocument7 pagesTuguegarao Certificate of Non-Availability of Stocks: Product Code Product Description UOM PriceNenbon NatividadNo ratings yet

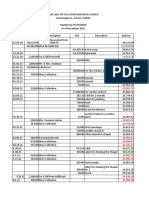

- Financial Staement 2021Document4 pagesFinancial Staement 2021Nenbon NatividadNo ratings yet

- Pre-Post-Conference-Forms 2Document5 pagesPre-Post-Conference-Forms 2Nenbon NatividadNo ratings yet

- BE Form 1 PHYSICAL FACILITIES AND MAINTENANCE NEEDS ASSESSMENT FORMDocument2 pagesBE Form 1 PHYSICAL FACILITIES AND MAINTENANCE NEEDS ASSESSMENT FORMNenbon NatividadNo ratings yet

- VolcanoDocument40 pagesVolcanoCarl LoretoNo ratings yet

- BE Form 4 DAILY ATTENDANCE OF VOLUNTEERSDocument1 pageBE Form 4 DAILY ATTENDANCE OF VOLUNTEERSNenbon NatividadNo ratings yet

- BE Form 3 RESOURCE MOBILIZATION FORMDocument3 pagesBE Form 3 RESOURCE MOBILIZATION FORMNenbon NatividadNo ratings yet

- BE Form 5 RECORD OF DONATIONS RECEIVEDDocument1 pageBE Form 5 RECORD OF DONATIONS RECEIVEDNenbon NatividadNo ratings yet

- Grade 6 NAT Scores in Filipino and Science Were Below The National Passing Rate of 75%Document3 pagesGrade 6 NAT Scores in Filipino and Science Were Below The National Passing Rate of 75%Nenbon NatividadNo ratings yet

- Complete PartnershipDocument5 pagesComplete PartnershipNenbon NatividadNo ratings yet

- DepEd All-in-One Book Guide for School LeadersDocument7 pagesDepEd All-in-One Book Guide for School LeadersNenbon NatividadNo ratings yet

- Department UpdatesDocument3 pagesDepartment UpdatesNenbon NatividadNo ratings yet

- Callang National High School Mid-Year Virtual InsetDocument56 pagesCallang National High School Mid-Year Virtual InsetNenbon NatividadNo ratings yet

- DepEd Guidelines on Special Hardship Allowance for TeachersDocument92 pagesDepEd Guidelines on Special Hardship Allowance for TeachersJoan Cala-or ValonesNo ratings yet

- Division Memorandum No. 66, s.2020 - Online or Virtual Assessment For Various Vacant PositionsDocument4 pagesDivision Memorandum No. 66, s.2020 - Online or Virtual Assessment For Various Vacant PositionsNenbon NatividadNo ratings yet

- Inset Cert.2Document17 pagesInset Cert.2Nenbon NatividadNo ratings yet

- Tax credit claim form guideDocument2 pagesTax credit claim form guideVivian KongNo ratings yet

- Max AR Final 130812 PDFDocument731 pagesMax AR Final 130812 PDFsnjv2621No ratings yet

- Romania Pestel Analysis Comprehensive Country OutlookDocument6 pagesRomania Pestel Analysis Comprehensive Country OutlookAtharva UppalwarNo ratings yet

- Final Executive SummaryDocument19 pagesFinal Executive Summarydas_s13No ratings yet

- Pelangi 2019 PDFDocument194 pagesPelangi 2019 PDFTharshanraaj RaajNo ratings yet

- Contracts II AssignmentDocument16 pagesContracts II AssignmentIsha PuthettuNo ratings yet

- Inside Flipkart A High-Pressure Workplace Thanks To IPO DreamsDocument1 pageInside Flipkart A High-Pressure Workplace Thanks To IPO DreamsRama Kant0% (1)

- Masinde Muliro University of Science & Technology: School of Computing & InformaticsDocument2 pagesMasinde Muliro University of Science & Technology: School of Computing & InformaticsBrandon JaphetNo ratings yet

- Motion To Reduce BondDocument4 pagesMotion To Reduce Bonderika barbaronaNo ratings yet

- Jollisavers Meals TV Ad DeconstructedDocument4 pagesJollisavers Meals TV Ad DeconstructedMa. Rhona Faye MedesNo ratings yet

- Market Research and Analysis of Favorite Plus Ceramic Tiles Pvt. LtdDocument46 pagesMarket Research and Analysis of Favorite Plus Ceramic Tiles Pvt. LtdMahendra PatadiaNo ratings yet

- Cost Accounting: Level 3Document19 pagesCost Accounting: Level 3Hein Linn Kyaw100% (1)

- Diamond Doctor Suit Against ManookianDocument41 pagesDiamond Doctor Suit Against ManookianThe Dallas Morning News100% (1)

- Grade 9 TLE LCPDocument8 pagesGrade 9 TLE LCPMJ Andrade67% (3)

- Contractors Registration Board Issues Registration CertificateDocument3 pagesContractors Registration Board Issues Registration CertificateEnock richardNo ratings yet

- Shell Pakistan Limited Analysis FinalDocument17 pagesShell Pakistan Limited Analysis FinalMuhammad Sheharyar TariqNo ratings yet

- FMCSA Rules on Marking Commercial Motor VehiclesDocument3 pagesFMCSA Rules on Marking Commercial Motor VehiclesfreeNo ratings yet

- FSA Guide 20Document16 pagesFSA Guide 20David DangNo ratings yet

- Real-Estate Investor's Psychology: Heuristics and Prospect FactorsDocument6 pagesReal-Estate Investor's Psychology: Heuristics and Prospect Factors03217925346No ratings yet

- MSc Sales & Marketing Statement of PurposeDocument1 pageMSc Sales & Marketing Statement of PurposeDaud LawrenceNo ratings yet

- SSRN Id4207171Document39 pagesSSRN Id4207171Nhat LinhNo ratings yet

- JPMorgan Chase London Whale GDocument15 pagesJPMorgan Chase London Whale GMaksym ShodaNo ratings yet

- 3.5 Additional Changes To Support Merchant and Acquirer Address in Visa Direct TransactionsDocument15 pages3.5 Additional Changes To Support Merchant and Acquirer Address in Visa Direct TransactionsYasir RoniNo ratings yet

- Accounts PaperDocument2 pagesAccounts PaperRohan Ghadge-46No ratings yet