You might also like

- Banking Kpi Encyclopedia Preview PDFDocument5 pagesBanking Kpi Encyclopedia Preview PDFAbcd100% (2)

- Consulting Math DrillsDocument15 pagesConsulting Math DrillsHashaam Javed50% (2)

- Chap 013Document19 pagesChap 013Xeniya Morozova Kurmayeva100% (1)

- Exercises IA 2Document7 pagesExercises IA 2Hanna Melody50% (2)

- B - Avle InfoDocument21 pagesB - Avle InfoQuofi SeliNo ratings yet

- Textile Industry Financial Analysis 2013-2017Document12 pagesTextile Industry Financial Analysis 2013-2017Huma HussainNo ratings yet

- Crescent Bahuman shareholding patternDocument3 pagesCrescent Bahuman shareholding patternNazimEhsanMalikNo ratings yet

- Howard CorporationDocument2 pagesHoward CorporationZayuri CRNo ratings yet

- Vietnam Indicator Name: Country Code: VNM Foreign Direct Investment, Net Inflows (Bop, Current Us$)Document6 pagesVietnam Indicator Name: Country Code: VNM Foreign Direct Investment, Net Inflows (Bop, Current Us$)tpqNo ratings yet

- WorkshopDocument26 pagesWorkshopKeuangan RSI PatiNo ratings yet

- HHM - SKMH - Roll No 22010013Document18 pagesHHM - SKMH - Roll No 22010013ZainNawazNo ratings yet

- Savings Simulation TemplateDocument9 pagesSavings Simulation TemplateSubramanian GnanaguruNo ratings yet

- Income Statement: General Selling and Administration ExpensesDocument8 pagesIncome Statement: General Selling and Administration ExpensesShehzadi Mahum (F-Name :Sohail Ahmed)No ratings yet

- Cálculo IndicadoresDocument5 pagesCálculo IndicadoresDaniel RodriguezNo ratings yet

- Restaurant performance data and funding requirementsDocument26 pagesRestaurant performance data and funding requirementsUppada SareesNo ratings yet

- Consolidation Budget FC 2 2018 (Submit 16032018)Document160 pagesConsolidation Budget FC 2 2018 (Submit 16032018)Cliquer's Love BundaNo ratings yet

- Exportadores Periodo 2012 1 2013 2 2014 3 2015 4 2016 5: Demanda en El MundoDocument6 pagesExportadores Periodo 2012 1 2013 2 2014 3 2015 4 2016 5: Demanda en El MundoJenryAvalosNo ratings yet

- ASghar Ali OD Final ProjectDocument10 pagesASghar Ali OD Final ProjectAbdul HadiNo ratings yet

- Valuation Orbita C Crystal Ball AleDocument37 pagesValuation Orbita C Crystal Ball AleAndré FonsecaNo ratings yet

- WASTAGE Analysis: K.P.K Steel HattarDocument3 pagesWASTAGE Analysis: K.P.K Steel HattarDanish RazaNo ratings yet

- Vertical Analysis of Income Statement 0F Blessed TextileDocument208 pagesVertical Analysis of Income Statement 0F Blessed TextileB SNo ratings yet

- Rekapitulasi Bulanan Puskesmas Jatirokeh Feb-18Document4 pagesRekapitulasi Bulanan Puskesmas Jatirokeh Feb-18puskesmas jatirokehNo ratings yet

- Comparitive Financial Statement of Reliance Industries For Last 5 YearsDocument33 pagesComparitive Financial Statement of Reliance Industries For Last 5 YearsPushkraj TalwadkarNo ratings yet

- Project Invest Last UpdateDocument10 pagesProject Invest Last Updateangel patrichiaNo ratings yet

- Car PricesDocument47 pagesCar PricesMajoo SonsNo ratings yet

- ReportDocument15 pagesReportnketu1994No ratings yet

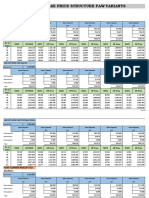

- Hire Purchase Price Structure Toyota Variants: ManualDocument9 pagesHire Purchase Price Structure Toyota Variants: ManualomiNo ratings yet

- Ix. 1. Produk Domestik Bruto Menurut Lapangan Usaha Atas Dasar Harga Berlaku'93 (Miliar RP)Document25 pagesIx. 1. Produk Domestik Bruto Menurut Lapangan Usaha Atas Dasar Harga Berlaku'93 (Miliar RP)Rahmi DiansariNo ratings yet

- Philippine Foreign Direct Investment, Net Inflows (Bop, Current Us$)Document6 pagesPhilippine Foreign Direct Investment, Net Inflows (Bop, Current Us$)tpqNo ratings yet

- Công ty Chi phí phải trả ngắn hạn 2000 2001 2002 2003Document120 pagesCông ty Chi phí phải trả ngắn hạn 2000 2001 2002 2003Tuấn Phạm Nguyễn ĐìnhNo ratings yet

- Punjab National Bank: Assets Summary: Mar 2009 - Mar 2018: Non-Annualised: Rs. MillionDocument4 pagesPunjab National Bank: Assets Summary: Mar 2009 - Mar 2018: Non-Annualised: Rs. MillionSaurabGhimireNo ratings yet

- Capital social, Capitaux propres et Chiffre d'Affaires des entreprises marocainesDocument10 pagesCapital social, Capitaux propres et Chiffre d'Affaires des entreprises marocainesYounes BEROUAGANo ratings yet

- Comparative analysis of financial statements for 2017 and 2016Document4 pagesComparative analysis of financial statements for 2017 and 2016DIANA POVEDANo ratings yet

- 037 Rutvi Porwal IMDocument2 pages037 Rutvi Porwal IMRutvi PorwalNo ratings yet

- Business Research FsDocument7 pagesBusiness Research FsJohnric ArtilloNo ratings yet

- Book 1Document5 pagesBook 1HarisCasteeloPartIINo ratings yet

- MQTM - XLSX (Data Entry)Document13 pagesMQTM - XLSX (Data Entry)iqra mumtazNo ratings yet

- BMP Bav Report FinalDocument93 pagesBMP Bav Report FinalThu ThuNo ratings yet

- BMP Bav ReportDocument79 pagesBMP Bav ReportThu ThuNo ratings yet

- Location QuotientDocument11 pagesLocation QuotientNur Arief RamadhanNo ratings yet

- New India Mediclaim Policy Premium Chart-1Document2 pagesNew India Mediclaim Policy Premium Chart-1saiNo ratings yet

- Updated Fcss Receipts & PaymentsDocument6 pagesUpdated Fcss Receipts & PaymentsMubasar khanNo ratings yet

- Fib LevelsDocument7 pagesFib LevelsPushpa VaddadiNo ratings yet

- F&a Cash Collection Report For October 2022Document5 pagesF&a Cash Collection Report For October 2022Esther AkpanNo ratings yet

- Calculating Industry Debt and Equity Ratios Over 6 YearsDocument4 pagesCalculating Industry Debt and Equity Ratios Over 6 YearskajalNo ratings yet

- Fuerza Motors IVA Retention Report December 2009Document10 pagesFuerza Motors IVA Retention Report December 2009JOSE MIGUEL LEMUS ROJASNo ratings yet

- ZerodhaDocument89 pagesZerodhaAarti ParmarNo ratings yet

- Baru Baru - PT X - Study Case 5Document98 pagesBaru Baru - PT X - Study Case 5Kojiro FuumaNo ratings yet

- LC3 AnalysisDocument21 pagesLC3 AnalysistimothyNo ratings yet

- Atlas Battery Limted Balance Sheet As at June 30 2004Document84 pagesAtlas Battery Limted Balance Sheet As at June 30 2004loverboy_q_sNo ratings yet

- 1997-2007 Antioch College BudgetsDocument5 pages1997-2007 Antioch College BudgetsantiochpapersNo ratings yet

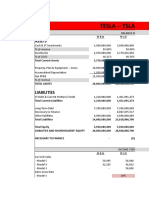

- Tesla ForecastDocument6 pagesTesla ForecastDanikaLiNo ratings yet

- Creditnote - VIZAG 30.09.2023Document6 pagesCreditnote - VIZAG 30.09.2023Raja chNo ratings yet

- New JourneyDocument6 pagesNew JourneyEstmarg EstmargNo ratings yet

- Final Report (Mughal Iron Steel)Document27 pagesFinal Report (Mughal Iron Steel)Pooja MandhanNo ratings yet

- Pricing - Group Case Study Data TablesDocument40 pagesPricing - Group Case Study Data TablesSound StudyNo ratings yet

- Book 2Document2 pagesBook 2Bharathi 3280No ratings yet

- Calculos TotalDocument29 pagesCalculos TotalMaria De Los Angeles YomeyeNo ratings yet

- Founding Team: Sheet1Document6 pagesFounding Team: Sheet1aardg hytNo ratings yet

- HR BudgetDocument5 pagesHR BudgettyagichemNo ratings yet

- Forecast May 03Document3 pagesForecast May 03Anonymous geItmk3No ratings yet

- Tableros de amortización y proyecciones financierasDocument5 pagesTableros de amortización y proyecciones financierasCarolinaa CarreñoNo ratings yet

- Presentation Slide Based On e CommerceDocument18 pagesPresentation Slide Based On e CommerceSumon BiswasNo ratings yet

- ROCKET SlideDocument19 pagesROCKET SlideSumon BiswasNo ratings yet

- SlideDocument18 pagesSlideSumon BiswasNo ratings yet

- Its A Thesis Paper Based On e CommerceDocument34 pagesIts A Thesis Paper Based On e CommerceSumon BiswasNo ratings yet

- Finance Related Topic SlideDocument27 pagesFinance Related Topic SlideSumon BiswasNo ratings yet

- Presentation SlideDocument25 pagesPresentation SlideSumon BiswasNo ratings yet

- Measuring Consumer Attitudes Towards BkashDocument27 pagesMeasuring Consumer Attitudes Towards BkashSumon BiswasNo ratings yet

- RahulDocument24 pagesRahulSumon BiswasNo ratings yet

- Hasib Final ReportDocument44 pagesHasib Final ReportSumon BiswasNo ratings yet

- (Slide)Document31 pages(Slide)Sumon BiswasNo ratings yet

- Full ThesisDocument50 pagesFull ThesisSumon BiswasNo ratings yet

- ThesisDocument45 pagesThesisSumon BiswasNo ratings yet

- Shohan SlideDocument17 pagesShohan SlideSumon BiswasNo ratings yet

- RCR Onboarding Module Day 1 - Intro To Collection Measurements and Techniques)Document116 pagesRCR Onboarding Module Day 1 - Intro To Collection Measurements and Techniques)Akmal HaziqNo ratings yet

- Difference Between Microfinance and MicrocreditDocument3 pagesDifference Between Microfinance and MicrocreditShantkumar IBMRNo ratings yet

- Commercial Banking System and Role of RBIDocument9 pagesCommercial Banking System and Role of RBIRishi exportsNo ratings yet

- Annual Report Avenue CapitalDocument44 pagesAnnual Report Avenue CapitalJoel CintrónNo ratings yet

- Professional Plumbing Products CatalogDocument196 pagesProfessional Plumbing Products CatalogFeruel PatalagsaNo ratings yet

- Hsslive XII Eco Macro ch3 MONEY - AND - BANKINGDocument9 pagesHsslive XII Eco Macro ch3 MONEY - AND - BANKINGSarammaNo ratings yet

- Msmes' Role in Economic Growth - A Study On India'S PerspectiveDocument16 pagesMsmes' Role in Economic Growth - A Study On India'S PerspectiveManas KumarNo ratings yet

- Y12.U5.30 - Forecasting and Managing Cash FlowsDocument3 pagesY12.U5.30 - Forecasting and Managing Cash FlowsRuxandra ZahNo ratings yet

- MOST IMPORTANT TERMS AND CONDITIONS - Citi Credit CardsDocument6 pagesMOST IMPORTANT TERMS AND CONDITIONS - Citi Credit CardsMohd AtNo ratings yet

- 125 Years of Digital Transformation in IndiaDocument45 pages125 Years of Digital Transformation in Indiabskanwar6376No ratings yet

- SIP Report Neeraj Gour FinanceDocument59 pagesSIP Report Neeraj Gour Financeadishitole106No ratings yet

- Financial Statement Analysis of TCS and INFOSYSDocument43 pagesFinancial Statement Analysis of TCS and INFOSYSRitwik Subudhi100% (1)

- Aviation Finance More To The LRF Than Meets The Eye 120718Document5 pagesAviation Finance More To The LRF Than Meets The Eye 120718a_sharafiehNo ratings yet

- Referral InformationDocument2 pagesReferral Informationabe madridNo ratings yet

- Accounting For Partnerships: What Is A Partnership?Document12 pagesAccounting For Partnerships: What Is A Partnership?nuggsNo ratings yet

- Kuya Junar's Tricycle Contract Draft - Doc (Mark Lozano Gwapo)Document3 pagesKuya Junar's Tricycle Contract Draft - Doc (Mark Lozano Gwapo)Emjay Sollano DejadaNo ratings yet

- Loan AmortizationDocument20 pagesLoan AmortizationMariano CinarogluNo ratings yet

- Improve Your Working Capital ManagementDocument16 pagesImprove Your Working Capital ManagementSudip BaruaNo ratings yet

- Project On Banker and CustomersDocument85 pagesProject On Banker and Customersrakesh9006No ratings yet

- Factors Affecting Investment Project Success in GondarDocument6 pagesFactors Affecting Investment Project Success in Gondarabraham admassieNo ratings yet

- Statutory Declaration of Common-Law Union: (Dual Signatures)Document2 pagesStatutory Declaration of Common-Law Union: (Dual Signatures)Jan AllemanNo ratings yet

- Tsehay Eco122Document30 pagesTsehay Eco122Tamirat KifleNo ratings yet

- Course Structure and Content for Class X Social ScienceDocument12 pagesCourse Structure and Content for Class X Social ScienceDarsh AroraNo ratings yet

- Methods of Payment in International TradeDocument13 pagesMethods of Payment in International Tradelovepreet singhNo ratings yet

- Tutorial 1 - Introduction To Treasury ManagementDocument2 pagesTutorial 1 - Introduction To Treasury ManagementTACN-4TC-19ACN Nguyen Thu HienNo ratings yet

- FM DJB - RTP Nov 21Document14 pagesFM DJB - RTP Nov 21shubhamsingh143deepNo ratings yet

- AI-Based ML Models Predict Credit Risk of India's Nifty 50 FirmsDocument11 pagesAI-Based ML Models Predict Credit Risk of India's Nifty 50 FirmsB. Hari Babu Assistant Professor, Dept. of Business ManagementNo ratings yet