You might also like

- Withholding Tax Rates Under DTAADocument7 pagesWithholding Tax Rates Under DTAAOM JARWALNo ratings yet

- Tax Rates As Per IT Act Vis A Vis Tax TreatiesDocument14 pagesTax Rates As Per IT Act Vis A Vis Tax TreatiesEswarReddyEegaNo ratings yet

- Tax RatesDocument1 pageTax RatesMariah Jans SasumanNo ratings yet

- Tds Rates As Per DtaaDocument3 pagesTds Rates As Per DtaamahiNo ratings yet

- Tarif Pasal 26Document2 pagesTarif Pasal 26lelaleria11No ratings yet

- Botswana Withholding Tax RatesDocument4 pagesBotswana Withholding Tax Ratesjiwon leeNo ratings yet

- Passive Incomefor Both Individual and Corporation Individual CorporationDocument4 pagesPassive Incomefor Both Individual and Corporation Individual CorporationYrolle Lynart AldeNo ratings yet

- Rangkuman Tarif P3BDocument5 pagesRangkuman Tarif P3BJuni PrastyanggaNo ratings yet

- Tanzania Revenue Authority Taxes and Duties at a Glance 2020-2021Document24 pagesTanzania Revenue Authority Taxes and Duties at a Glance 2020-2021Ibrahim ZachariaNo ratings yet

- TX VNM Examdocs 2018Document3 pagesTX VNM Examdocs 2018hung789No ratings yet

- Ringkasan Tarif P3B: Tax Learning: Tax Resume Ringkasan Tax TreatyDocument2 pagesRingkasan Tarif P3B: Tax Learning: Tax Resume Ringkasan Tax TreatyAchmad MudaniNo ratings yet

- Chapter 05 Final Income Taxation TableDocument4 pagesChapter 05 Final Income Taxation TablejannyNo ratings yet

- Regular Business/Corporate Tax: DC RFC NRFCDocument2 pagesRegular Business/Corporate Tax: DC RFC NRFCGrace Angelie C. Asio-SalihNo ratings yet

- Final income tax rates for individuals and corporationsDocument4 pagesFinal income tax rates for individuals and corporationsJulie Mae Caling MalitNo ratings yet

- Final income tax rates for individuals and corporationsDocument4 pagesFinal income tax rates for individuals and corporationsJulie Mae Caling MalitNo ratings yet

- Taxation Guide for Resident and Nonresident CitizensDocument2 pagesTaxation Guide for Resident and Nonresident CitizensBlezyl A. Dela FuenteNo ratings yet

- f6 Vietnam VNM Specimen Questions Applicable From June 2015Document10 pagesf6 Vietnam VNM Specimen Questions Applicable From June 2015Thị Linh Chi VũNo ratings yet

- Summary of Passive Income and Capital Gains Taxes - MaupoDocument4 pagesSummary of Passive Income and Capital Gains Taxes - MaupoMae MaupoNo ratings yet

- FT TableDocument4 pagesFT TableChantie BorlonganNo ratings yet

- Midterm Assignment No. 3Document3 pagesMidterm Assignment No. 3XaxxyNo ratings yet

- Withholding TaxDocument20 pagesWithholding TaxAngela CanayaNo ratings yet

- Tax Rates Summary Under Philippine Income Tax LawDocument6 pagesTax Rates Summary Under Philippine Income Tax LawJñelle Faith Herrera SaludaresNo ratings yet

- Tarif PPh Pasal 26 untuk P3B yang Berlaku EfektifDocument2 pagesTarif PPh Pasal 26 untuk P3B yang Berlaku EfektifJokoWidodo0% (1)

- f6vnm 2015dec Q PDFDocument16 pagesf6vnm 2015dec Q PDFSinhNo ratings yet

- Dec 18-QDocument15 pagesDec 18-QNguyễn Như DuyNo ratings yet

- Tax TableDocument3 pagesTax TablePhán Tiêu TiềnNo ratings yet

- Ghana - Corporate - Withholding TaxesDocument3 pagesGhana - Corporate - Withholding TaxesFrancisNo ratings yet

- Fit - Tax Table 2Document4 pagesFit - Tax Table 2zipaganermy15No ratings yet

- F6VNM 2015 Jun QDocument14 pagesF6VNM 2015 Jun QMinh Hương TrầnNo ratings yet

- Income Taxation RatesDocument2 pagesIncome Taxation RatesStephen ChuaNo ratings yet

- Summary of FWT ThresholdDocument4 pagesSummary of FWT ThresholdAngel Chane OstrazNo ratings yet

- Passive Income Tax Rates for Residents and Non-ResidentsDocument3 pagesPassive Income Tax Rates for Residents and Non-ResidentsPamela Jean CuyaNo ratings yet

- Taxation (Vietnam) : Thursday 7 June 2018Document10 pagesTaxation (Vietnam) : Thursday 7 June 2018SinhNo ratings yet

- RateDocument3 pagesRatemikamiiNo ratings yet

- C. Summary of Final Tax Rates On Different Taxpayers: From PCSO and Lotto Amounting To P10,000 or Less-ExemptDocument1 pageC. Summary of Final Tax Rates On Different Taxpayers: From PCSO and Lotto Amounting To P10,000 or Less-ExemptNajira HassanNo ratings yet

- Double Taxation - Rates of WithholdingDocument6 pagesDouble Taxation - Rates of Withholdingunderstated1313100% (1)

- Tanzania Revenue Authority Taxes and Duties at a GlanceDocument24 pagesTanzania Revenue Authority Taxes and Duties at a GlanceInnocent IssackNo ratings yet

- Tax Notes Aug 10-11Document15 pagesTax Notes Aug 10-11Reiner NuludNo ratings yet

- Final Withholding Tax On Passive IncomeDocument1 pageFinal Withholding Tax On Passive IncomeChelsea Anne VidalloNo ratings yet

- Taxation Tax Rates For Individual Taxpayers, Estates and TrustsDocument5 pagesTaxation Tax Rates For Individual Taxpayers, Estates and TrustsSherri BonquinNo ratings yet

- VNCE CIT ReviewDocument11 pagesVNCE CIT ReviewĐinh Như Thủy HằngNo ratings yet

- Summary of Final Tax Under The Nirc, As Amended Individual Citizen AlienDocument16 pagesSummary of Final Tax Under The Nirc, As Amended Individual Citizen AlienXiaoyu KensameNo ratings yet

- Taxation - Vietnam (TX - VNM) : Applied SkillsDocument16 pagesTaxation - Vietnam (TX - VNM) : Applied SkillsFive FifthNo ratings yet

- Passive Incomes and Capital Gains Tax Rates in the PhilippinesDocument1 pagePassive Incomes and Capital Gains Tax Rates in the PhilippinesChimmy ParkNo ratings yet

- Summary of WHT Rates Under Oman Tax Treaties in Force PDFDocument2 pagesSummary of WHT Rates Under Oman Tax Treaties in Force PDFMoneycomeNo ratings yet

- F6VNM 2014 Jun QDocument7 pagesF6VNM 2014 Jun QNgocduc NgoNo ratings yet

- F6 - 2014 JunDocument11 pagesF6 - 2014 JunphoebeNo ratings yet

- TAXATION in INDIADocument11 pagesTAXATION in INDIAChaitanya PatilNo ratings yet

- Taxation (Vietnam) : Thursday 8 June 2017Document11 pagesTaxation (Vietnam) : Thursday 8 June 2017annarosaNo ratings yet

- Income Category: Summary of Final TaxesDocument3 pagesIncome Category: Summary of Final TaxesKathleen Mae Salenga FontalbaNo ratings yet

- TX VNM Tax Rates 2023 - 230507 - 072553Document4 pagesTX VNM Tax Rates 2023 - 230507 - 072553Nguyễn Hồng NgọcNo ratings yet

- SCHEDULE Withholding Tax RatesDocument3 pagesSCHEDULE Withholding Tax RatesTatianaNo ratings yet

- Reduction in Rate of Tax Deduction at Source (TDS) & Tax Collection at Source (TCS)Document6 pagesReduction in Rate of Tax Deduction at Source (TDS) & Tax Collection at Source (TCS)Kranthi Kumar KatamreddyNo ratings yet

- Foreign Trade UniversityDocument3 pagesForeign Trade UniversityNguyễn HươngNo ratings yet

- No. Tax Source Rate (Resident) Rate (Non-Resident)Document2 pagesNo. Tax Source Rate (Resident) Rate (Non-Resident)Master KihimbwaNo ratings yet

- TX 202Document5 pagesTX 202Pau SantosNo ratings yet

- Withholding VAT & Tax Rates Summary for FY 2019-20 and 2018-19Document3 pagesWithholding VAT & Tax Rates Summary for FY 2019-20 and 2018-19Tanvir TanmoyNo ratings yet

- HRDocument7 pagesHRajithaNo ratings yet

- Adva TVDocument4 pagesAdva TVajithaNo ratings yet

- Treasury Management Sample Questions Dec 18 ExamsDocument114 pagesTreasury Management Sample Questions Dec 18 ExamsajithaNo ratings yet

- Federal Bank Financial Results - Q4 - FY19Document3 pagesFederal Bank Financial Results - Q4 - FY19ajithaNo ratings yet

- Principles & Practices of Banking NotesDocument2 pagesPrinciples & Practices of Banking NotesajithaNo ratings yet

- Application For TMB E-ConnectDocument3 pagesApplication For TMB E-ConnectajithaNo ratings yet

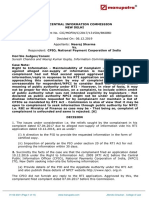

- MANU/CI/0954/2019: RTI Complainant Seeks Info from NPCIDocument10 pagesMANU/CI/0954/2019: RTI Complainant Seeks Info from NPCIBhumica VeeraNo ratings yet

- Spectacular PassionsDocument317 pagesSpectacular Passionsarimanau100% (1)

- Hiv/Aids: Project BackgroundDocument1 pageHiv/Aids: Project BackgroundKristine JavierNo ratings yet

- Deriv Investments (Europe) LimitedDocument9 pagesDeriv Investments (Europe) LimitedİHFKİHHKİCİHCİHCDSNo ratings yet

- Notes On Collective NounsDocument7 pagesNotes On Collective NounsTuisyen Dewan Hj Ali50% (2)

- Ed. Remington, Patrick L. - Chronic Disease Epidemiology, Prevention, and Control-American Public Health Association (2016)Document1,168 pagesEd. Remington, Patrick L. - Chronic Disease Epidemiology, Prevention, and Control-American Public Health Association (2016)Sebastián Ramírez RoldánNo ratings yet

- Confidentiality Agreement GuideDocument11 pagesConfidentiality Agreement GuideSeema WadkarNo ratings yet

- Military History of Slovenians, by Janez J. Švajncer, 2001Document5 pagesMilitary History of Slovenians, by Janez J. Švajncer, 2001Slovenian Webclassroom Topic Resources100% (1)

- UN Supplier Code of Conduct. United Nations.Document4 pagesUN Supplier Code of Conduct. United Nations.Daniel BorrEka MalteseNo ratings yet

- The Influence of The English Language On The Russian Youth SlangDocument10 pagesThe Influence of The English Language On The Russian Youth SlangВасилий БоровцовNo ratings yet

- Reading Report G9Document50 pagesReading Report G9Grade9 2023No ratings yet

- New Ford Endeavour Brochure Mobile PDFDocument13 pagesNew Ford Endeavour Brochure Mobile PDFAnurag JhaNo ratings yet

- DuniaDocument64 pagesDuniaAmith PanickerNo ratings yet

- Tanzania Catholic Directory 2019Document391 pagesTanzania Catholic Directory 2019Peter Temu50% (2)

- Former Ohio Wildlife Officer Convicted of Trafficking in White-Tailed DeerDocument2 pagesFormer Ohio Wildlife Officer Convicted of Trafficking in White-Tailed DeerThe News-HeraldNo ratings yet

- Cpcu 552 TocDocument3 pagesCpcu 552 Tocshanmuga89No ratings yet

- VMF Error LogDocument11 pagesVMF Error LogTest PhaseNo ratings yet

- f5 Pretrial Writing StatusDocument9 pagesf5 Pretrial Writing StatusAwin SeidiNo ratings yet

- Henry VIII, Act of Supremacy (1534) by Caroline BarrioDocument4 pagesHenry VIII, Act of Supremacy (1534) by Caroline BarriocarolbjcaNo ratings yet

- 'SangCup Business Plan Pota-Ca Empanada (Grp. 3 ABM 211)Document56 pages'SangCup Business Plan Pota-Ca Empanada (Grp. 3 ABM 211)jsemlpz0% (1)

- 12th AccountsDocument6 pages12th AccountsHarjinder SinghNo ratings yet

- COMOROS 01 SynopsisDocument99 pagesCOMOROS 01 SynopsisJaswinder SohalNo ratings yet

- POL 100-Introduction To Political Science-Sameen A. Mohsin AliDocument7 pagesPOL 100-Introduction To Political Science-Sameen A. Mohsin AliOsamaNo ratings yet

- Sri Aurobindo's Guidance on Sadhana and the MindDocument8 pagesSri Aurobindo's Guidance on Sadhana and the MindShiyama SwaminathanNo ratings yet

- Birthday Party AnalysisDocument1 pageBirthday Party AnalysisJames Ford100% (1)

- Estmt - 2024 01 05Document8 pagesEstmt - 2024 01 05alejandro860510No ratings yet

- USA2Document2 pagesUSA2Helena TrầnNo ratings yet

- Holly FashionsDocument4 pagesHolly FashionsKhaled Darweesh100% (7)

- Seirei Tsukai No Blade Dance - Volume 12 - Releasing The Sealed SwordDocument284 pagesSeirei Tsukai No Blade Dance - Volume 12 - Releasing The Sealed SwordGabriel John DexterNo ratings yet

- KLTG23: Dec - Mac 2015Document113 pagesKLTG23: Dec - Mac 2015Abdul Rahim Mohd AkirNo ratings yet