You might also like

- Tax Guide 2022/2023: Right People. Right Size. Right SolutionsDocument60 pagesTax Guide 2022/2023: Right People. Right Size. Right Solutionstinashe mashoyoyaNo ratings yet

- Accenture Calypso Capabilities PDFDocument8 pagesAccenture Calypso Capabilities PDFSergio Vinsennau100% (1)

- Lmia SMT#995098Document4 pagesLmia SMT#995098CAN EXPRESS89% (18)

- LMIADocument4 pagesLMIAmilon haqueNo ratings yet

- Example Tax ReturnDocument6 pagesExample Tax Returnapi-252304176No ratings yet

- P6 ATX UK Summary Notes FA 2019Document58 pagesP6 ATX UK Summary Notes FA 2019Mujeeb Don-The Fallen-Angel100% (1)

- Dubai Internet City (Dic)Document78 pagesDubai Internet City (Dic)Faisal AghaNo ratings yet

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Document1 pageTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Anshul Gupta0% (1)

- Matla Qs Company CVDocument20 pagesMatla Qs Company CVMaha KalaiNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific: 2020 EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific: 2020 EditionNo ratings yet

- Taxation Suggested Solution: LessDocument9 pagesTaxation Suggested Solution: LesskannadhassNo ratings yet

- FM-QA-044 Rev 02 Supplier Evaluation QuestionnaireDocument6 pagesFM-QA-044 Rev 02 Supplier Evaluation QuestionnaireAvoor KhanNo ratings yet

- KWT 5e Supplier DirectoryDocument10 pagesKWT 5e Supplier DirectoryEdwardNo ratings yet

- Managing Successful Projects with PRINCE2 2009 EditionFrom EverandManaging Successful Projects with PRINCE2 2009 EditionRating: 4 out of 5 stars4/5 (3)

- Taxation Law - 2013 Dimaampao Lecture Notes PDFDocument90 pagesTaxation Law - 2013 Dimaampao Lecture Notes PDFPaul Joseph MercadoNo ratings yet

- OrderInvoice - 53821082004769033Document1 pageOrderInvoice - 53821082004769033Yoyo ToyoNo ratings yet

- Accenture Payments PDFDocument4 pagesAccenture Payments PDFSergio VinsennauNo ratings yet

- Accenture Payments PDFDocument4 pagesAccenture Payments PDFSergio VinsennauNo ratings yet

- Accenture Decouple Innovate Updated PDFDocument17 pagesAccenture Decouple Innovate Updated PDFSergio VinsennauNo ratings yet

- Accenture ADP Overview Brochure PDFDocument12 pagesAccenture ADP Overview Brochure PDFSergio VinsennauNo ratings yet

- Accenture Business Transformation Through Multi Cloud PDFDocument12 pagesAccenture Business Transformation Through Multi Cloud PDFSergio Vinsennau0% (1)

- Navigating Taxation: 2021 Ghana Tax Facts and FiguresDocument28 pagesNavigating Taxation: 2021 Ghana Tax Facts and FiguresKobby KatalistNo ratings yet

- TaXavvy-Movement Control Order PDFDocument6 pagesTaXavvy-Movement Control Order PDFBritish Malaysian Chamber of CommerceNo ratings yet

- Finance 2Document13 pagesFinance 2Monika UpadhyayNo ratings yet

- Section 194J - TDS On Fees For Professional or Technical ServicesDocument24 pagesSection 194J - TDS On Fees For Professional or Technical ServicesShaik MastanvaliNo ratings yet

- Corporate Tax Diploma Brochure PWC DIFC AcademyDocument4 pagesCorporate Tax Diploma Brochure PWC DIFC AcademyAditya OmarNo ratings yet

- Kandachipuram Infonet MMFLDocument3 pagesKandachipuram Infonet MMFLkvinoth22No ratings yet

- 4 - MiniCapt Mobile and Accessories IQOQ PDFDocument80 pages4 - MiniCapt Mobile and Accessories IQOQ PDFdian212No ratings yet

- Sales Training - 13.04.2024Document15 pagesSales Training - 13.04.2024bekalu GizachewNo ratings yet

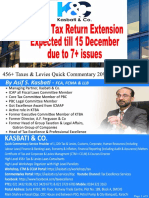

- IT Return Extension Expected Till 15 DecemberDocument8 pagesIT Return Extension Expected Till 15 DecemberMuhammad Wisal AhmedNo ratings yet

- Villiyanur MMFL InfonetDocument3 pagesVilliyanur MMFL Infonetkvinoth22No ratings yet

- Update To SIA 2016Document6 pagesUpdate To SIA 2016limegreensNo ratings yet

- China Furniture Revised Profile PDFDocument25 pagesChina Furniture Revised Profile PDFGkou DojkuNo ratings yet

- Jul 2020 WWW - Mybuilder.com - SGDocument30 pagesJul 2020 WWW - Mybuilder.com - SGkulNo ratings yet

- FinanceDocument12 pagesFinanceMonika UpadhyayNo ratings yet

- Divine Alloys & Power Co.-R-23042012Document3 pagesDivine Alloys & Power Co.-R-23042012Dhirendra SinghNo ratings yet

- Ripley and Co-R-21072016Document3 pagesRipley and Co-R-21072016rahulbhelwa24No ratings yet

- MM & J Prequalification 24 June 2017Document7 pagesMM & J Prequalification 24 June 2017Moses Utumbe namandwaNo ratings yet

- Cutterz PH: "Entrepreneurship Is All About Your Irritation." An Answer To An Irritation Leads To InspirationDocument5 pagesCutterz PH: "Entrepreneurship Is All About Your Irritation." An Answer To An Irritation Leads To InspirationJazehl Joy ValdezNo ratings yet

- Ghana Tax Facts and Figures 2019Document32 pagesGhana Tax Facts and Figures 2019kok kuan wongNo ratings yet

- Microsoft Cloud Support Services PricingDocument5 pagesMicrosoft Cloud Support Services PricingAddis AbabaNo ratings yet

- KH Tax Business Tax Alerts Cambodia Updates On e Commerce Laws RegulationsDocument5 pagesKH Tax Business Tax Alerts Cambodia Updates On e Commerce Laws RegulationsRoland NomadsNo ratings yet

- Magiclamp Sales Quotation - BW EPIC KOSAN LTDDocument4 pagesMagiclamp Sales Quotation - BW EPIC KOSAN LTDim.erickonNo ratings yet

- A00F100e Rv15 03.18 QuestionnaireDocument4 pagesA00F100e Rv15 03.18 QuestionnaireShiella BagalacsaNo ratings yet

- Quote QU0499 ABA - Xero Accounting Software - Sales and Accounting Module Set UpDocument5 pagesQuote QU0499 ABA - Xero Accounting Software - Sales and Accounting Module Set UpYuni SartikaNo ratings yet

- MRK - Spring 2022 - MGTI620 - 3 - BS180202234Document91 pagesMRK - Spring 2022 - MGTI620 - 3 - BS180202234pakaffairs27No ratings yet

- QSCert RFO ISO ImplementationDocument3 pagesQSCert RFO ISO ImplementationMUHAMMED KHANNo ratings yet

- Profile FintuneDocument6 pagesProfile FintuneSachin KulkarniNo ratings yet

- Tax & Asset Management Officer - PT Taka Turbomachinery Indonesia - 3734489 JobStreetDocument1 pageTax & Asset Management Officer - PT Taka Turbomachinery Indonesia - 3734489 JobStreetMochammad TaufikNo ratings yet

- Speedo ISP: Business Plan OnDocument10 pagesSpeedo ISP: Business Plan OnSyed Shahan AliNo ratings yet

- PWC News Alert 21 October 2014 Mca Clarification Trust or Trustee Not Barred From Being A Partner in An LLP PDFDocument2 pagesPWC News Alert 21 October 2014 Mca Clarification Trust or Trustee Not Barred From Being A Partner in An LLP PDFMayank TripathiNo ratings yet

- India Factoring - R-31122016Document3 pagesIndia Factoring - R-31122016Kumar KnNo ratings yet

- Company Profile FinewestDocument10 pagesCompany Profile Finewestal lakwenaNo ratings yet

- Revisiting Pest AnalysisDocument2 pagesRevisiting Pest Analysistosh321830No ratings yet

- 2009 February GeodesicDocument2 pages2009 February GeodesicG.VenkatasubramanianNo ratings yet

- Proposal For CBG Society - ElitraDocument3 pagesProposal For CBG Society - ElitraTyagi BalaNo ratings yet

- Fam Sararis KenyaDocument40 pagesFam Sararis KenyaOCHIENG NICHOLASNo ratings yet

- E-Service Business Proposal 2003Document28 pagesE-Service Business Proposal 2003Aaradhya JoshiNo ratings yet

- ST On Software LicenseDocument2 pagesST On Software LicenseSrinivasulu TummalapentaNo ratings yet

- Paysquare - Proposal For LMSDocument6 pagesPaysquare - Proposal For LMSanimeshsenNo ratings yet

- Cpim FlyerDocument12 pagesCpim FlyerHusseinIsmailNo ratings yet

- Rotodyne Eng-R-25052016Document3 pagesRotodyne Eng-R-25052016Soupan SenNo ratings yet

- EC - Survey No 417 - Not AvailableDocument3 pagesEC - Survey No 417 - Not AvailableporlluxNo ratings yet

- JD For Quality Kiosk 2024Document1 pageJD For Quality Kiosk 2024pimapeh666No ratings yet

- Company Profile...Document15 pagesCompany Profile...tahirNo ratings yet

- The Institute of Chartered Accountants of Nigeria: May 2023 Diet Professional ExaminationsDocument5 pagesThe Institute of Chartered Accountants of Nigeria: May 2023 Diet Professional ExaminationsJadesola AdeoyeNo ratings yet

- WelcomeDocument3 pagesWelcomeSinethemba RonaldNo ratings yet

- ATO Phone ListDocument35 pagesATO Phone Listrani.christine91No ratings yet

- About The ExaminationDocument2 pagesAbout The ExaminationMarcellin MarcaNo ratings yet

- Bookkeeping ServicesDocument7 pagesBookkeeping Servicesmaitri voraNo ratings yet

- Wiley Practitioner's Guide to GAAS 2006: Covering all SASs, SSAEs, SSARSs, and InterpretationsFrom EverandWiley Practitioner's Guide to GAAS 2006: Covering all SASs, SSAEs, SSARSs, and InterpretationsRating: 2 out of 5 stars2/5 (2)

- Accenture Microsoft Collaboration Capabilities PDFDocument2 pagesAccenture Microsoft Collaboration Capabilities PDFSergio VinsennauNo ratings yet

- Accenture Mywizard Video Transcript PDFDocument1 pageAccenture Mywizard Video Transcript PDFSergio VinsennauNo ratings yet

- Accenture Digital Ecosystems POV PDFDocument11 pagesAccenture Digital Ecosystems POV PDFSergio VinsennauNo ratings yet

- Accenture Skype For Business PDFDocument4 pagesAccenture Skype For Business PDFSergio VinsennauNo ratings yet

- Accenture AIR Cargo Flyer PDFDocument2 pagesAccenture AIR Cargo Flyer PDFSergio VinsennauNo ratings yet

- Accenture Reformx PDFDocument8 pagesAccenture Reformx PDFSergio VinsennauNo ratings yet

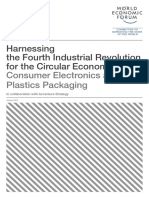

- Accenture-WEF Harnessing 4IR Circular Economy Report 2018 PDFDocument29 pagesAccenture-WEF Harnessing 4IR Circular Economy Report 2018 PDFSergio VinsennauNo ratings yet

- Accenture-WEF Harnessing 4IR Circular Economy Report 2018 PDFDocument29 pagesAccenture-WEF Harnessing 4IR Circular Economy Report 2018 PDFSergio VinsennauNo ratings yet

- Accenture HANA Credential PDFDocument4 pagesAccenture HANA Credential PDFSergio VinsennauNo ratings yet

- Accenture Disruptability POV PDFDocument13 pagesAccenture Disruptability POV PDFSergio VinsennauNo ratings yet

- Accenture HANA Credential PDFDocument4 pagesAccenture HANA Credential PDFSergio VinsennauNo ratings yet

- Accenture Digital Worker PDFDocument4 pagesAccenture Digital Worker PDFSergio VinsennauNo ratings yet

- Accenture Reformx PDFDocument8 pagesAccenture Reformx PDFSergio VinsennauNo ratings yet

- Accenture-Compressive Disruption Slideshare PDFDocument18 pagesAccenture-Compressive Disruption Slideshare PDFSergio Vinsennau100% (1)

- 170203-Digital Economy SeminarDocument1 page170203-Digital Economy SeminarSergio VinsennauNo ratings yet

- Accenture 2016 Consolidated EEO 1 PDFDocument1 pageAccenture 2016 Consolidated EEO 1 PDFSergio VinsennauNo ratings yet

- BDO Knows FASB Alert Income Tax DisclosuresDocument3 pagesBDO Knows FASB Alert Income Tax DisclosuresSergio VinsennauNo ratings yet

- Please Take A Moment To Read and Acknowledge The Following Terms and ConditionsDocument1 pagePlease Take A Moment To Read and Acknowledge The Following Terms and ConditionsMary MurphyNo ratings yet

- VAT CERTIFICATE Al JazeeraDocument3 pagesVAT CERTIFICATE Al JazeeraSyedFarhanNo ratings yet

- DT 2 New Question PaperDocument11 pagesDT 2 New Question Paperneha manglaniNo ratings yet

- Deed of Admission Cum RetirementDocument3 pagesDeed of Admission Cum RetirementgulshanNo ratings yet

- Richard Pieris Exports PLCDocument9 pagesRichard Pieris Exports PLCDPH ResearchNo ratings yet

- Paurashava Budgeting in BangladeshDocument15 pagesPaurashava Budgeting in BangladeshMd Musiur Rahaman ShawonNo ratings yet

- ACC 430 Chapter 8Document19 pagesACC 430 Chapter 8vikkiNo ratings yet

- (DIGEST) Dominium Realty & Construction Corporation v. CIRDocument2 pages(DIGEST) Dominium Realty & Construction Corporation v. CIRYodh Jamin OngNo ratings yet

- OD224490938272355000Document2 pagesOD224490938272355000Swati SharmaNo ratings yet

- Depreciation: Historical MethodsDocument19 pagesDepreciation: Historical MethodsKiran PatilNo ratings yet

- Lecture 2 - Audit Plan PDFDocument24 pagesLecture 2 - Audit Plan PDFMoud KhalfaniNo ratings yet

- What Is Tax EvasionDocument3 pagesWhat Is Tax EvasionJee AlmanzorNo ratings yet

- Income From SalaryDocument26 pagesIncome From SalaryAkash VisputeNo ratings yet

- Test 3 Review - Part 1Document10 pagesTest 3 Review - Part 1Mariola AlkuNo ratings yet

- Financial Accounting 2 Semester Level 1Document3 pagesFinancial Accounting 2 Semester Level 1Folegwe FolegweNo ratings yet

- InvoiceDocument1 pageInvoiceSachin SinghNo ratings yet

- Itr 2Document9 pagesItr 2Arvind PaulNo ratings yet

- Rmo 22 01Document20 pagesRmo 22 01Maria Leonora Bornales100% (1)

- Taxation Laws in IndiaDocument3 pagesTaxation Laws in IndiasankalpmiraniNo ratings yet

- Tax System PDFDocument6 pagesTax System PDFpalak asatiNo ratings yet

- VAHAN 4.0 (Citizen Services) Onlineapp02 150 8013 FDocument1 pageVAHAN 4.0 (Citizen Services) Onlineapp02 150 8013 Fmdneyaz9831No ratings yet

- Scrutiny Report SajasDocument2 pagesScrutiny Report SajasSAHAL SHAJAHANNo ratings yet

- Responsible Leadership: Tax-Free Savings AccountDocument2 pagesResponsible Leadership: Tax-Free Savings AccountbaxterNo ratings yet

- LOI BSL BhilaiDocument1 pageLOI BSL BhilaiRakesh SinghNo ratings yet