You might also like

- LNG ShippingDocument46 pagesLNG ShippingmekulaNo ratings yet

- Presentation MD NGC Developent of Gas Infrastrucure26March2008Document20 pagesPresentation MD NGC Developent of Gas Infrastrucure26March2008emodeye kennethNo ratings yet

- From Oil to Gas and Beyond: A Review of the Trinidad and Tobago Model and Analysis of Future ChallengesFrom EverandFrom Oil to Gas and Beyond: A Review of the Trinidad and Tobago Model and Analysis of Future ChallengesTrevor M. BoopsinghNo ratings yet

- Philippines: Energy Sector Assessment, Strategy, and Road MapFrom EverandPhilippines: Energy Sector Assessment, Strategy, and Road MapNo ratings yet

- Cable Protection Analysis ReportDocument87 pagesCable Protection Analysis ReportsufyanNo ratings yet

- The Global Coal Industry, Nova Scotia's Energy Plan and The Donkin Coal ProjectDocument39 pagesThe Global Coal Industry, Nova Scotia's Energy Plan and The Donkin Coal Projectmystery11No ratings yet

- Predicting the Price of Carbon Supplement 1: Hinkley Point C Nuclear Power Station Enhanced Carbon Audit LCA Case StudyFrom EverandPredicting the Price of Carbon Supplement 1: Hinkley Point C Nuclear Power Station Enhanced Carbon Audit LCA Case StudyNo ratings yet

- J08937A-A-RT-00045 Rev A1 Basis of ScheduleDocument15 pagesJ08937A-A-RT-00045 Rev A1 Basis of ScheduleMathias OnosemuodeNo ratings yet

- Business Analyst ProjectDocument2 pagesBusiness Analyst ProjectMinh Phương NguyễnNo ratings yet

- Stranded - Alpha Coal Project in Australia's Galilee BasinDocument39 pagesStranded - Alpha Coal Project in Australia's Galilee BasinGreenpeace Australia PacificNo ratings yet

- Configuring ATP Check in The Sales and Supplying SystemDocument7 pagesConfiguring ATP Check in The Sales and Supplying SystemaczillaNo ratings yet

- LNG Industry March 2012Document100 pagesLNG Industry March 2012erojaszaNo ratings yet

- World Non US Gasification DatabaseDocument9 pagesWorld Non US Gasification DatabaseKhairi Maulida AzhariNo ratings yet

- Guidelines To Export & Import: As Per Foreign Trade Policy 2015-2020Document109 pagesGuidelines To Export & Import: As Per Foreign Trade Policy 2015-2020manoj chNo ratings yet

- Civil Code Provisions On Common CarriersDocument4 pagesCivil Code Provisions On Common CarriersMichelle Escudero Filart100% (1)

- Orient Refinery Presentation Nov 08Document30 pagesOrient Refinery Presentation Nov 08RaminVali100% (2)

- What Is Happing World ShipyardDocument100 pagesWhat Is Happing World ShipyardLegend Anbu100% (1)

- Petronet Corporate Presentation Jan11Document31 pagesPetronet Corporate Presentation Jan11Ganesh DivekarNo ratings yet

- KPMG - Port Logistics - India Maritime CommunityDocument58 pagesKPMG - Port Logistics - India Maritime CommunityAnonymous EAineTiz100% (2)

- Ao'Neftegazrezerv'Document5 pagesAo'Neftegazrezerv'LegalgsNo ratings yet

- Economics ReactorDocument42 pagesEconomics Reactorian84No ratings yet

- SAP MM Interview Questions and Answers For Freshers - Experienced - Top Companies - MNC Job FAQ - STechiesDocument6 pagesSAP MM Interview Questions and Answers For Freshers - Experienced - Top Companies - MNC Job FAQ - STechiesManas Kumar SahooNo ratings yet

- SAP TM Course GuideDocument5 pagesSAP TM Course GuideP raju100% (1)

- Maersk betting on blockchain to transform international logisticsDocument6 pagesMaersk betting on blockchain to transform international logisticsVaishnav SureshNo ratings yet

- Nat Gas Export Development - CIBC - 11-2011Document7 pagesNat Gas Export Development - CIBC - 11-2011tqswansonNo ratings yet

- US Gasification DatabaseDocument9 pagesUS Gasification DatabaseAhmad DaoodNo ratings yet

- LNC - August 1 2013 - Quarterly Activities ReportDocument38 pagesLNC - August 1 2013 - Quarterly Activities ReportdigifiNo ratings yet

- Revista E&P - Octubre 2011Document110 pagesRevista E&P - Octubre 2011jpsi6No ratings yet

- 2007 03 08 EUCI - Nuclear RenaissanceDocument44 pages2007 03 08 EUCI - Nuclear RenaissanceEdward KeeNo ratings yet

- OAS (Kevin de Cuba), From Vision Towards Bankable Renewable Energy Projects, St. Kitts and Nevis ExampleDocument34 pagesOAS (Kevin de Cuba), From Vision Towards Bankable Renewable Energy Projects, St. Kitts and Nevis ExampleDetlef LoyNo ratings yet

- 2 Indian Ports Key Sector Trends Jan2010Document18 pages2 Indian Ports Key Sector Trends Jan2010kalaiNo ratings yet

- Revista E&P - Diciembre 2011Document91 pagesRevista E&P - Diciembre 2011jpsi6No ratings yet

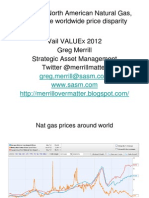

- Exporting North American Natural Gas, Closing The Worldwide Price DisparityDocument35 pagesExporting North American Natural Gas, Closing The Worldwide Price DisparityVitaliyKatsenelsonNo ratings yet

- US Gasification DatabaseDocument9 pagesUS Gasification DatabaseKhairi Maulida AzhariNo ratings yet

- Formulation of Project Report and AppraisalDocument39 pagesFormulation of Project Report and AppraisalSamNo ratings yet

- 1 - Over View of PS - SH BakshiDocument42 pages1 - Over View of PS - SH BakshiNeeraj KumarNo ratings yet

- Wind Power Report 2010Document50 pagesWind Power Report 2010sebascianNo ratings yet

- Oil & Gas Industry Update: NDT Requirements and Rig Utilization TrendsDocument36 pagesOil & Gas Industry Update: NDT Requirements and Rig Utilization TrendsDeanNo ratings yet

- 2 Indian Ports Key Sector Trends Jan2010Document18 pages2 Indian Ports Key Sector Trends Jan2010Manoj DoleyNo ratings yet

- The Shaw Group Inc. J.P. Morgan Diversified Industries ConferenceDocument28 pagesThe Shaw Group Inc. J.P. Morgan Diversified Industries Conferencestavros7No ratings yet

- Daewoo International: December 2010Document38 pagesDaewoo International: December 2010Angelica MeloNo ratings yet

- Coal Company Financial and Operational Data Comps SheetDocument17 pagesCoal Company Financial and Operational Data Comps SheetNs1503No ratings yet

- Suggestions For Timely I Mplementation of HEP'S Including Survey & Investigations, Various Clearances, Geological Surprises, Enabling InfrastructureDocument74 pagesSuggestions For Timely I Mplementation of HEP'S Including Survey & Investigations, Various Clearances, Geological Surprises, Enabling InfrastructureAmarNo ratings yet

- Moving Dirt LatestDocument76 pagesMoving Dirt LatestFrederick Martinez TrujilloNo ratings yet

- 9 STG Gas To Liquids GTLDocument6 pages9 STG Gas To Liquids GTLDiego Bascope MaidaNo ratings yet

- Revista E&P - Mayo 2011Document120 pagesRevista E&P - Mayo 2011jpsi6No ratings yet

- MontneyInitiation 04-16-14 GMP RPTDocument91 pagesMontneyInitiation 04-16-14 GMP RPTresver25No ratings yet

- Director's Cut: Lynn Helms NDIC Department of Mineral ResourcesDocument2 pagesDirector's Cut: Lynn Helms NDIC Department of Mineral ResourcesbakkengeneralNo ratings yet

- Rystad Energy - Forecast For Global Shale - ShortDocument10 pagesRystad Energy - Forecast For Global Shale - Shorttassili17No ratings yet

- 2018-07-24-Wells Fargo Securiti-The Basin Book Supply vs. Takeaway-82461766 PDFDocument5 pages2018-07-24-Wells Fargo Securiti-The Basin Book Supply vs. Takeaway-82461766 PDFDavid SpilkinNo ratings yet

- Han Solar All V1Document32 pagesHan Solar All V1nandaNo ratings yet

- Transportation Projects Under ReviewDocument5 pagesTransportation Projects Under ReviewHartford CourantNo ratings yet

- Oil Gas Uk Development DtiDocument27 pagesOil Gas Uk Development DtiskyporkerNo ratings yet

- CCC PPT 120918Document30 pagesCCC PPT 120918Suvarna GaikwadNo ratings yet

- Preliminary List: Top 25 Strategic Infrastructure Projects in Brazil, 2011Document5 pagesPreliminary List: Top 25 Strategic Infrastructure Projects in Brazil, 2011Marton CavaniNo ratings yet

- North American Shale RevolutionDocument38 pagesNorth American Shale RevolutionLorenzo Antunes GalhardoNo ratings yet

- Ge Shipping Feb 14 PresentationDocument34 pagesGe Shipping Feb 14 PresentationdiffsoftNo ratings yet

- EOR: Promesa Incumplida o Un Gran Futuro?: Fernando Cabrera Eduardo ManriqueDocument25 pagesEOR: Promesa Incumplida o Un Gran Futuro?: Fernando Cabrera Eduardo ManriqueFernando Montes de OcaNo ratings yet

- Xcite Oil Reserve NewsDocument9 pagesXcite Oil Reserve NewsthunderNo ratings yet

- Gas Shale 1Document20 pagesGas Shale 1Jinhichi Molero RodriguezNo ratings yet

- REC Market Outlook and Price ForecastDocument14 pagesREC Market Outlook and Price Forecastpatanjali9No ratings yet

- Maximizing Utilization of Light Tight Oils Economics and Technology SolutionsDocument26 pagesMaximizing Utilization of Light Tight Oils Economics and Technology SolutionsM Scott GreenNo ratings yet

- Sound Transit - Program Realignment Illustrative Scenarios Presentation - February 2021Document32 pagesSound Transit - Program Realignment Illustrative Scenarios Presentation - February 2021The UrbanistNo ratings yet

- A Strength: QR NATIONAL Share Offer DocumentDocument3 pagesA Strength: QR NATIONAL Share Offer Documentgy5115123No ratings yet

- RBS Round Up: 09 September 2010Document8 pagesRBS Round Up: 09 September 2010egolistocksNo ratings yet

- Watershed Tungsten Project - Optimisation Studies Boost ValueDocument12 pagesWatershed Tungsten Project - Optimisation Studies Boost ValueCarlosP.TesénNo ratings yet

- AcadianEnergyInc2012 03 01Document3 pagesAcadianEnergyInc2012 03 01likeme_arpit09No ratings yet

- Adapting To Climate Change-Suncor Energy IncorporationDocument8 pagesAdapting To Climate Change-Suncor Energy IncorporationSai VishnuNo ratings yet

- Petronet LNG - A ProfileDocument30 pagesPetronet LNG - A ProfileWaghela ManishNo ratings yet

- Avenue Supermarts LTDDocument11 pagesAvenue Supermarts LTDashok yadavNo ratings yet

- Reduce: Beauty Community Beauty TBDocument12 pagesReduce: Beauty Community Beauty TBashok yadavNo ratings yet

- Hua Hong Semiconductor: Lower Target Price To HK$20.00 On Expected Macro Slowdown in 2019Document10 pagesHua Hong Semiconductor: Lower Target Price To HK$20.00 On Expected Macro Slowdown in 2019ashok yadavNo ratings yet

- Margin Concerns Should Take Precedence Over Improved OutlookDocument15 pagesMargin Concerns Should Take Precedence Over Improved Outlookashok yadavNo ratings yet

- Hindustan Zinc Companyname: The Silver' LiningDocument11 pagesHindustan Zinc Companyname: The Silver' Liningashok yadavNo ratings yet

- India - Diagnostics: Leaders Need To Keep The InitiativeDocument4 pagesIndia - Diagnostics: Leaders Need To Keep The Initiativeashok yadavNo ratings yet

- Hua Hong Semiconductor: Lower Target Price To HK$20.00 On Expected Macro Slowdown in 2019Document10 pagesHua Hong Semiconductor: Lower Target Price To HK$20.00 On Expected Macro Slowdown in 2019ashok yadavNo ratings yet

- Avenue Supermarts LTDDocument11 pagesAvenue Supermarts LTDashok yadavNo ratings yet

- ICICI Securities maintains Buy on Dish TV with revised target price of Rs71Document8 pagesICICI Securities maintains Buy on Dish TV with revised target price of Rs71ashok yadavNo ratings yet

- India - Diagnostics: Leaders Need To Keep The InitiativeDocument4 pagesIndia - Diagnostics: Leaders Need To Keep The Initiativeashok yadavNo ratings yet

- Healthia Limited: Fill Your Boots!Document31 pagesHealthia Limited: Fill Your Boots!ashok yadavNo ratings yet

- Hindustan Zinc Companyname: The Silver' LiningDocument11 pagesHindustan Zinc Companyname: The Silver' Liningashok yadavNo ratings yet

- Reduce: Beauty Community Beauty TBDocument12 pagesReduce: Beauty Community Beauty TBashok yadavNo ratings yet

- Margin Concerns Should Take Precedence Over Improved OutlookDocument15 pagesMargin Concerns Should Take Precedence Over Improved Outlookashok yadavNo ratings yet

- Wipro LTD (WIPRO) : Growth and Margin Visibility Improving..Document13 pagesWipro LTD (WIPRO) : Growth and Margin Visibility Improving..ashok yadavNo ratings yet

- Jyothy Laboratories (JYOLAB) : Dishwashing & Fabric Care Support GrowthDocument10 pagesJyothy Laboratories (JYOLAB) : Dishwashing & Fabric Care Support Growthashok yadavNo ratings yet

- PC Partner: (01263.HK/1263 HK)Document6 pagesPC Partner: (01263.HK/1263 HK)ashok yadavNo ratings yet

- L&T Infotech: Strong Operational PerformanceDocument12 pagesL&T Infotech: Strong Operational Performanceashok yadavNo ratings yet

- Oceanagold Corporation: Sepq Report - First LookDocument5 pagesOceanagold Corporation: Sepq Report - First Lookashok yadavNo ratings yet

- Reduce: Bharti Infratel Bhin inDocument11 pagesReduce: Bharti Infratel Bhin inashok yadavNo ratings yet

- Far LTD: SNE Development Plan SubmittedDocument6 pagesFar LTD: SNE Development Plan Submittedashok yadavNo ratings yet

- Blackberry: Margins Strong Maintain Market PerformDocument11 pagesBlackberry: Margins Strong Maintain Market Performashok yadavNo ratings yet

- Encana Corp.: San Juan Sale Further Improves Balance SheetDocument6 pagesEncana Corp.: San Juan Sale Further Improves Balance Sheetashok yadavNo ratings yet

- Encana Corp.: San Juan Sale Further Improves Balance SheetDocument6 pagesEncana Corp.: San Juan Sale Further Improves Balance Sheetashok yadavNo ratings yet

- Medifast, Inc.: October 8, 2018 Med - NasdaqDocument8 pagesMedifast, Inc.: October 8, 2018 Med - Nasdaqashok yadavNo ratings yet

- Blackberry: Margins Strong Maintain Market PerformDocument11 pagesBlackberry: Margins Strong Maintain Market Performashok yadavNo ratings yet

- Icpo ModelDocument2 pagesIcpo ModelDiego CardonaNo ratings yet

- Ocean Freight USA - Glossary of Shipping Terms PDFDocument9 pagesOcean Freight USA - Glossary of Shipping Terms PDFshivam_dubey4004No ratings yet

- AGX Logistics Air & Sea Freight ServicesDocument5 pagesAGX Logistics Air & Sea Freight ServicesLaurensius SheldyNo ratings yet

- Masood Textile Mills LTD.: Supply Chain ManagementDocument11 pagesMasood Textile Mills LTD.: Supply Chain ManagementTàlhà Bïn TàrïqNo ratings yet

- ACTBAS 2 - Lecture 2a FreightDocument2 pagesACTBAS 2 - Lecture 2a FreightJason Robert MendozaNo ratings yet

- DG Job AidDocument22 pagesDG Job AidSHERIEFNo ratings yet

- SGN 1793532Document2 pagesSGN 1793532Hai Thang BaNo ratings yet

- Guidance on IHM certificates and maintenanceDocument6 pagesGuidance on IHM certificates and maintenancefarid asadiNo ratings yet

- REVISED - Red Dog Owners Book 2021.7Document13 pagesREVISED - Red Dog Owners Book 2021.7niknik73100% (1)

- TARRIFFDocument4 pagesTARRIFFAnoop KalathillNo ratings yet

- CJ Darcl LogisticsDocument2 pagesCJ Darcl LogisticsCJ DarclNo ratings yet

- Laws On Transportation and Public UtilitiesDocument9 pagesLaws On Transportation and Public UtilitiesRoji Belizar HernandezNo ratings yet

- Sample of Report For Ship Security Assessment: S ParticularDocument26 pagesSample of Report For Ship Security Assessment: S ParticularGP ExamNo ratings yet

- Philam Insurance Co. Vs Heung-A Shipping Corp.Document9 pagesPhilam Insurance Co. Vs Heung-A Shipping Corp.Romy Ian LimNo ratings yet

- FedEx Ship Manager User Guide v.2350 (English) 6Document230 pagesFedEx Ship Manager User Guide v.2350 (English) 6Abhinaba DasguptaNo ratings yet

- Bachelor of CommerceDocument33 pagesBachelor of CommerceManjunath NagarajanNo ratings yet

- Assignment-2 TPDocument2 pagesAssignment-2 TPvivek singhNo ratings yet

- Capt. PanigrahiDocument17 pagesCapt. PanigrahiPramod JadhavNo ratings yet

- Lubricants Storage and TransportationDocument9 pagesLubricants Storage and TransportationKommoju Naga Venkata SubrahmanyamNo ratings yet

- OperationsNote 10 2006Document5 pagesOperationsNote 10 2006gaurav nirbanNo ratings yet

- Matrix Doc NIFTDocument61 pagesMatrix Doc NIFTSiddhesh GautamNo ratings yet