You might also like

- Micro - Economics Notes, RUCO, REC 101, BBA1.BAFITIIDocument431 pagesMicro - Economics Notes, RUCO, REC 101, BBA1.BAFITIIWalton Jr Kobe TZNo ratings yet

- Economic IndicatorsDocument2 pagesEconomic IndicatorsShamsiyyaUNo ratings yet

- How To Estimate Formworks of Columns, Beams, and GirdersDocument9 pagesHow To Estimate Formworks of Columns, Beams, and GirdersTinTinNo ratings yet

- Writing Task 1Document16 pagesWriting Task 1Chaochao NguyenNo ratings yet

- FAO Coffee PublicationDocument106 pagesFAO Coffee PublicationD.WorkuNo ratings yet

- Applied Metrology for Manufacturing EngineeringFrom EverandApplied Metrology for Manufacturing EngineeringRating: 5 out of 5 stars5/5 (1)

- Define The Goals.Document13 pagesDefine The Goals.Simbarashe MupfupiNo ratings yet

- Define The Goals.Document13 pagesDefine The Goals.Simbarashe MupfupiNo ratings yet

- Economic Choices and Decision-Making Economic Choices and Decision-MakingDocument20 pagesEconomic Choices and Decision-Making Economic Choices and Decision-MakingLawrence PazNo ratings yet

- Chapter 1 MicroDocument24 pagesChapter 1 MicroKhouloud bn16No ratings yet

- Scarcity and Choice. Economics As A Science of ChoiceDocument22 pagesScarcity and Choice. Economics As A Science of ChoiceAndreea AnghelNo ratings yet

- International Trade: Made by MathelrainDocument51 pagesInternational Trade: Made by MathelrainHernandez Miguel AngelNo ratings yet

- Lecture #1: Introduction To EconomicsDocument86 pagesLecture #1: Introduction To EconomicsMike Viet Hoa NguyenNo ratings yet

- IntroductionDocument15 pagesIntroductionAGRAWAL UTKARSHNo ratings yet

- Chapter 1 Introduction To EconomicsDocument43 pagesChapter 1 Introduction To EconomicsChen Yee KhooNo ratings yet

- Lecture 1 EconomicsDocument52 pagesLecture 1 EconomicsdaliahashemNo ratings yet

- Bba 1002Document29 pagesBba 1002LouisLimNo ratings yet

- Microeconomics Handouts UpdatedDocument27 pagesMicroeconomics Handouts UpdatedKhalil FanousNo ratings yet

- Assignment 3-PPF and Opportunity CostDocument1 pageAssignment 3-PPF and Opportunity CostAbhishekNo ratings yet

- Chap 6Document52 pagesChap 6nbh167705No ratings yet

- Universidad Autónoma de Nuevo León Facultad de Ingeniería Mecánica y EléctricaDocument70 pagesUniversidad Autónoma de Nuevo León Facultad de Ingeniería Mecánica y EléctricaAngel AlvarezNo ratings yet

- Theory of Consumption Andtheory of ProductionDocument6 pagesTheory of Consumption Andtheory of ProductionMarinale LabroNo ratings yet

- Midterm AssessmentDocument2 pagesMidterm AssessmentWaleed KhalidNo ratings yet

- CII TEXCON'18 - Knowledge PaperDocument28 pagesCII TEXCON'18 - Knowledge PaperNishit ShahNo ratings yet

- Supply Curve: No. of Jeans ('000)Document9 pagesSupply Curve: No. of Jeans ('000)Nilesh kumarNo ratings yet

- The Production Possibility Curve: Curve That Shows The Maximum Combinations of Two OutputsDocument21 pagesThe Production Possibility Curve: Curve That Shows The Maximum Combinations of Two OutputsReemaz SuhailNo ratings yet

- Multimedia University: Final ExaminationDocument5 pagesMultimedia University: Final ExaminationNABILA HADIFAH BINTI MOHAMAD PATHANNo ratings yet

- Nitin SanjDocument21 pagesNitin SanjsanjayfabexportNo ratings yet

- Unit 4 - Socioeconomic Impact StudyDocument20 pagesUnit 4 - Socioeconomic Impact StudyJudy Mar Valdez, CPANo ratings yet

- FinallllDocument5 pagesFinallllYasmeen YasserNo ratings yet

- Chapter-Iii Apparel Market of IndiaDocument13 pagesChapter-Iii Apparel Market of IndiadhariniNo ratings yet

- ECO452 October 2019Document3 pagesECO452 October 2019leonwankwo1No ratings yet

- Single Entry QuizDocument5 pagesSingle Entry QuizRosshaine SaraspeNo ratings yet

- PGDRDM2Document14 pagesPGDRDM2Ye' Thi HaNo ratings yet

- 02 - Chap02Document47 pages02 - Chap02ChavezDNo ratings yet

- How Technology 20210811Document37 pagesHow Technology 20210811Line PhamNo ratings yet

- Metropolitan University, SylhetDocument2 pagesMetropolitan University, SylhetAbdul Muhaymin MahdiNo ratings yet

- WJ Keller Paper 2Document34 pagesWJ Keller Paper 2sesha94No ratings yet

- ECO Assignment - 1Document10 pagesECO Assignment - 1Nilesh kumarNo ratings yet

- Problem Set 1: Exercise 1 - Opportunity Cost and PPFDocument2 pagesProblem Set 1: Exercise 1 - Opportunity Cost and PPFRoy SarkisNo ratings yet

- Economics of Markets: Cost Functions: ObjectivesDocument6 pagesEconomics of Markets: Cost Functions: Objectivesshandil7No ratings yet

- AppEco Q2 Mod4 PDFDocument8 pagesAppEco Q2 Mod4 PDFMaria Elaine SorianoNo ratings yet

- BCG Matrix: - Market ShareDocument2 pagesBCG Matrix: - Market Sharewisnu pranata adhiNo ratings yet

- METRO Group: Metro Cash and CarryDocument6 pagesMETRO Group: Metro Cash and CarrypanboNo ratings yet

- S1 4 SampleQDocument3 pagesS1 4 SampleQAzail SumNo ratings yet

- Applied Economics: Quarter 3 - Module 3 Market Demand, Market Supply and Market EquilibriumDocument10 pagesApplied Economics: Quarter 3 - Module 3 Market Demand, Market Supply and Market EquilibriumRon TabioloNo ratings yet

- Workshop 5 Labour Market and The Distribution of IncomeDocument5 pagesWorkshop 5 Labour Market and The Distribution of IncomeEcoteach09No ratings yet

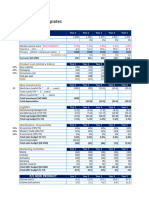

- State Budget Implications & CG 2024-25Document21 pagesState Budget Implications & CG 2024-25newalliance commerceNo ratings yet

- Advance Microeconomics CHP 01 Introduction 39857 645Document31 pagesAdvance Microeconomics CHP 01 Introduction 39857 645Irfan ShinwariNo ratings yet

- ICL Post-Graduate Diploma in Business: Report-1: Fundamental Economic Problems and Decision MakingDocument4 pagesICL Post-Graduate Diploma in Business: Report-1: Fundamental Economic Problems and Decision MakingRanvir SinghNo ratings yet

- Commodity Price Outlook: How Long Can The High Prices Be Sustained?Document40 pagesCommodity Price Outlook: How Long Can The High Prices Be Sustained?Ben ZhongNo ratings yet

- Raft and Longline Culture of Green MusselDocument57 pagesRaft and Longline Culture of Green MusselOnie BerolNo ratings yet

- Newrobe: Rent! Return! Repeat!Document9 pagesNewrobe: Rent! Return! Repeat!Naitik JainNo ratings yet

- Tutorial Business Case - Key - Apr22Document6 pagesTutorial Business Case - Key - Apr22Minh Phuong DangNo ratings yet

- Solution Problem 1 Problems Handouts MicroDocument25 pagesSolution Problem 1 Problems Handouts MicrokokokoNo ratings yet

- Tutorial Exercises 7: Perfect Competition: Essential Readings: Chapter 7Document18 pagesTutorial Exercises 7: Perfect Competition: Essential Readings: Chapter 7tahmeemNo ratings yet

- Tutorial 3 Cost Behaviour AnalysisDocument3 pagesTutorial 3 Cost Behaviour AnalysisDashania GregoryNo ratings yet

- NHÓM 3 - BIỂU ĐỒDocument21 pagesNHÓM 3 - BIỂU ĐỒtrangNo ratings yet

- NEEMADOCDocument3 pagesNEEMADOCnyimbilene23No ratings yet

- Flakiness and Elongation Index of Aggregate PDFDocument4 pagesFlakiness and Elongation Index of Aggregate PDFSK Abdul KaiumNo ratings yet

- AEB 212 Introduction To Agricultural Economics: Test 1 (Total Marks 50 Marks)Document5 pagesAEB 212 Introduction To Agricultural Economics: Test 1 (Total Marks 50 Marks)Thabo ChuchuNo ratings yet

- Forecasting Revenue, Expenses - Scenario AnalysisDocument26 pagesForecasting Revenue, Expenses - Scenario AnalysisPREKSHA MALHOTRANo ratings yet

- New Product DevelopmentDocument22 pagesNew Product Developmentsreeram_muralidhar_1No ratings yet

- Inventory ManagementDABMDocument60 pagesInventory ManagementDABMbhavyaNo ratings yet

- Embarrassment of Product Choices 2: Towards a Society of Well-beingFrom EverandEmbarrassment of Product Choices 2: Towards a Society of Well-beingNo ratings yet

- ECS 1125 Lecture 2 Demand 2Document33 pagesECS 1125 Lecture 2 Demand 2Simbarashe MupfupiNo ratings yet

- ECS 1125 Module Handbook - 2017 - 18Document26 pagesECS 1125 Module Handbook - 2017 - 18Simbarashe MupfupiNo ratings yet

- 2017 May Exam SolutionDocument9 pages2017 May Exam SolutionSimbarashe MupfupiNo ratings yet

- Seminar Questions Supply Decision (Seminar 5)Document5 pagesSeminar Questions Supply Decision (Seminar 5)Simbarashe MupfupiNo ratings yet

- ECS 1125 Seminar 4, Week 5Document4 pagesECS 1125 Seminar 4, Week 5Simbarashe MupfupiNo ratings yet

- 2018 Financial Modeling Competition Winner Model Yu OliverDocument58 pages2018 Financial Modeling Competition Winner Model Yu OliverSimbarashe MupfupiNo ratings yet

- 02.define The Present StateDocument1 page02.define The Present StateSimbarashe MupfupiNo ratings yet

- Introduction-Perspective: 1. ConflictDocument3 pagesIntroduction-Perspective: 1. ConflictSimbarashe MupfupiNo ratings yet

- 02.define The Present StateDocument1 page02.define The Present StateSimbarashe MupfupiNo ratings yet

- Question 1dDocument4 pagesQuestion 1dSimbarashe MupfupiNo ratings yet

- Quiz 3 SolutionsDocument6 pagesQuiz 3 SolutionsNgsNo ratings yet

- Macro SolutionsDocument22 pagesMacro SolutionsIbrahim RegachoNo ratings yet

- Report On Employment in Africa (Re-Africa) : Tackling The Youth Employment ChallengeDocument92 pagesReport On Employment in Africa (Re-Africa) : Tackling The Youth Employment ChallengecubadesignstudNo ratings yet

- Economics PT-1 Section A AnswersDocument5 pagesEconomics PT-1 Section A AnswersJANARTHANAN MNo ratings yet

- COVID ReportDocument23 pagesCOVID ReportAnonymous 6f8RIS6No ratings yet

- Employment Unemployment in IndiaDocument31 pagesEmployment Unemployment in IndiaAbhishek gupta100% (11)

- HR OutDocument29 pagesHR OutShweta GuravNo ratings yet

- Sponsorship SpeechesDocument31 pagesSponsorship SpeechesArangkada PhilippinesNo ratings yet

- Mann Hardware Has Four Employees Who Are Paid On An Hourly BasisDocument6 pagesMann Hardware Has Four Employees Who Are Paid On An Hourly BasisDoreenNo ratings yet

- Michigan Child Development and Care (CDC) Handbook - CDC - Handbook - 7-2013Document32 pagesMichigan Child Development and Care (CDC) Handbook - CDC - Handbook - 7-2013Lobster JonesNo ratings yet

- Fill in The Gaps With One of The Linking Words On The Right. Some Can Be RepeatedDocument2 pagesFill in The Gaps With One of The Linking Words On The Right. Some Can Be RepeatedLeysiNo ratings yet

- 09 - Chapter 2 PDFDocument42 pages09 - Chapter 2 PDFAnwarul MirzaNo ratings yet

- The Dignity of Work and The Rights of Workers: NotesDocument4 pagesThe Dignity of Work and The Rights of Workers: Notes김나연No ratings yet

- Toaz - Info Business Studies Notes PRDocument116 pagesToaz - Info Business Studies Notes PRمحمد عبداللہNo ratings yet

- Principles of Macroeconomics Brief Edition 3rd Edition Frank Test Bank 1Document56 pagesPrinciples of Macroeconomics Brief Edition 3rd Edition Frank Test Bank 1erin100% (53)

- Eco 2Document5 pagesEco 2ZENITH EDUSTATIONNo ratings yet

- Tóm tắt TQTMDocument52 pagesTóm tắt TQTMOanh Lăng PhươngNo ratings yet

- Decent Work Indicators in Africa - A First Assessment Based On National SourcesDocument160 pagesDecent Work Indicators in Africa - A First Assessment Based On National SourcesJin SiclonNo ratings yet

- Health Economics: Economics - Definition - Characteristics - Components - Macroeconomics and MicroeconomicsDocument9 pagesHealth Economics: Economics - Definition - Characteristics - Components - Macroeconomics and Microeconomicscyrene gabaoNo ratings yet

- Chapter 3 Assignment Cost AccountingDocument2 pagesChapter 3 Assignment Cost AccountingSydnei HaywoodNo ratings yet

- Midterm (ONLINE) Autumn 2020 - Tayabur - RahmanDocument9 pagesMidterm (ONLINE) Autumn 2020 - Tayabur - RahmanTayabur RahmanNo ratings yet

- Activity 5 - Beyond Printed LettersDocument3 pagesActivity 5 - Beyond Printed LettersSheena RodriguezNo ratings yet

- A Tale of Four EconomiesDocument3 pagesA Tale of Four EconomiesAnis NajwaNo ratings yet

- Measurement of Unemployment in IndiaDocument33 pagesMeasurement of Unemployment in Indiasandeepkumarbaranwal100% (3)

- German ModelDocument422 pagesGerman ModelDan-Alexandru PetriaNo ratings yet

- A - Analyzing The Task: Ielts Writing 2 Describing TrendsDocument7 pagesA - Analyzing The Task: Ielts Writing 2 Describing TrendsPhương LyNo ratings yet

- Nguyen Bich Loan - Individual WorkDocument10 pagesNguyen Bich Loan - Individual WorkloanNo ratings yet