You might also like

- RHB KWK 0722Document2 pagesRHB KWK 0722Besari Md DaudNo ratings yet

- Academic Writing For Publication RELO Jakarta Feb2016 022616 SignatureDocument225 pagesAcademic Writing For Publication RELO Jakarta Feb2016 022616 SignatureNesreen Yusuf100% (1)

- Fixed Deposit - FD 082022Document1 pageFixed Deposit - FD 082022kainingNo ratings yet

- AxisBankStmt205022 PDFDocument2 pagesAxisBankStmt205022 PDFBikash Kumar ChaurasiaNo ratings yet

- YCT 4 Vocabulary ListDocument14 pagesYCT 4 Vocabulary Listhauulty100% (1)

- The List of the Korean Companies in the UAE: Company Name 이름 Off. Tel Off. Fax P.O.BoxDocument34 pagesThe List of the Korean Companies in the UAE: Company Name 이름 Off. Tel Off. Fax P.O.Boxnguyen phuong anh100% (1)

- PR 7887Document2 pagesPR 7887Mohameed Ehteshamuddin QureshNo ratings yet

- Edn - 74577 2Document2 pagesEdn - 74577 2narasimharao gorlaNo ratings yet

- Edn - 74577 3Document2 pagesEdn - 74577 3narasimharao gorlaNo ratings yet

- IDFCFIRSTBankstatement 10027354401 154032854Document6 pagesIDFCFIRSTBankstatement 10027354401 154032854SAGAR YADAVNo ratings yet

- Employees' Provident Fund Organization, India: Challan SummaryDocument1 pageEmployees' Provident Fund Organization, India: Challan SummaryAshish ParmarNo ratings yet

- Pol 129298Document2 pagesPol 129298summu paulNo ratings yet

- 10/05/1979 Guntur Siva Kumari M MEDL/83591 Emp Id:0617221: Name DOB Treasury DDODocument2 pages10/05/1979 Guntur Siva Kumari M MEDL/83591 Emp Id:0617221: Name DOB Treasury DDOADNo ratings yet

- GPF No.: Subscriber's Name Date of Birth:-DDO Code & Name: - Rate of Interest FromDocument4 pagesGPF No.: Subscriber's Name Date of Birth:-DDO Code & Name: - Rate of Interest FromHema SoodNo ratings yet

- HDFC Bank LTDDocument5 pagesHDFC Bank LTDutkarshlegal96No ratings yet

- E Statement Bulan 1 PDFDocument1 pageE Statement Bulan 1 PDFMuhammad ikmail KhusaimiNo ratings yet

- Estatement20220811 000518428Document4 pagesEstatement20220811 000518428Kim ZainurNo ratings yet

- Bank StatementDocument30 pagesBank StatementFerhan IskandarNo ratings yet

- EntityDocument1 pageEntitySto KanigiriNo ratings yet

- HDFC Bank LTDDocument2 pagesHDFC Bank LTDdeyanukul7No ratings yet

- Statement of Account: Blok A2-3-1, Flat Ampang Hilir, Taman Ampang Hilir Ampang 68000 SELANGORDocument2 pagesStatement of Account: Blok A2-3-1, Flat Ampang Hilir, Taman Ampang Hilir Ampang 68000 SELANGORNoriza GhazaliNo ratings yet

- Coi 21-22 TusharDocument4 pagesCoi 21-22 TusharKR FINANCIAL SERVICESNo ratings yet

- Computation 21-22Document3 pagesComputation 21-22Ruloans VaishaliNo ratings yet

- Statement of Account: BLOK 37-02-01 Rumah Pangsa DBKL Sri Langkawi 53100 Gombak, WP Kuala LumpurDocument4 pagesStatement of Account: BLOK 37-02-01 Rumah Pangsa DBKL Sri Langkawi 53100 Gombak, WP Kuala LumpurAsadu Son SolehNo ratings yet

- Blob:Https:/www - Cimbclicks.com - My/7b82b7f6 9ad8 49c6 867d 360cde8a43f8Document2 pagesBlob:Https:/www - Cimbclicks.com - My/7b82b7f6 9ad8 49c6 867d 360cde8a43f8Mohd RiduanNo ratings yet

- Pay&Save Account 112022Document1 pagePay&Save Account 112022maxNo ratings yet

- Medl 40579Document2 pagesMedl 40579Kasaram NaveenNo ratings yet

- Nirima Sahu ComputationDocument2 pagesNirima Sahu Computationbrs consultancyNo ratings yet

- Statement of Account: DS1 Kampung Seri Damai Batu 7 JLN Gambang Kuantan 25150 PAHANGDocument4 pagesStatement of Account: DS1 Kampung Seri Damai Batu 7 JLN Gambang Kuantan 25150 PAHANGhajarNo ratings yet

- HL Savings - I 102022Document1 pageHL Savings - I 102022CAN YAMANNo ratings yet

- GPF No.: Subscriber's Name Date of Birth:-DDO Code & Name: - Rate of Interest FromDocument8 pagesGPF No.: Subscriber's Name Date of Birth:-DDO Code & Name: - Rate of Interest FromHema SoodNo ratings yet

- Statement of Account: CU 79 Jalan Kuala Pahang Kampung Serandu 26600 PEKAN, PAHANGDocument40 pagesStatement of Account: CU 79 Jalan Kuala Pahang Kampung Serandu 26600 PEKAN, PAHANGAien HasNo ratings yet

- TAC0002 Bank Statements SelfEmployed ReportDocument78 pagesTAC0002 Bank Statements SelfEmployed ReportViren GalaNo ratings yet

- PayslipDocument2 pagesPayslipJtech Connection EnterpriseNo ratings yet

- HLB Receipt 595904Document1 pageHLB Receipt 595904Nurul HazwaniNo ratings yet

- Statement of Account: No. 32A. Tingkat 1 Jalan Bds 2 Bukit Desa Semantan 28000 Temerloh, PahangDocument4 pagesStatement of Account: No. 32A. Tingkat 1 Jalan Bds 2 Bukit Desa Semantan 28000 Temerloh, PahangFerhan IskandarNo ratings yet

- 24-3331 INNOVE-mergedDocument3 pages24-3331 INNOVE-mergedCaloi VillanuevaNo ratings yet

- Employees' Provident Fund Organization, IndiaDocument1 pageEmployees' Provident Fund Organization, IndiaKumar MNo ratings yet

- OrientDocument4 pagesOrientaasthapoddar155No ratings yet

- Statement of Account: PT 632 Desa Darul Naim Pasir Tumboh 16150 Kota Bharu, KelantanDocument8 pagesStatement of Account: PT 632 Desa Darul Naim Pasir Tumboh 16150 Kota Bharu, KelantanFadzianNo ratings yet

- Statement of Account: NO 23 Persiaran Anggerik 1 Taman Anggerik 33000 Kuala Kangsar, PerakDocument3 pagesStatement of Account: NO 23 Persiaran Anggerik 1 Taman Anggerik 33000 Kuala Kangsar, PerakYoga LingamNo ratings yet

- Your Personal Loan Statement: Mev J BernhardtDocument2 pagesYour Personal Loan Statement: Mev J BernhardtJeannine BernhardtNo ratings yet

- Opening Balance - 3967575.73Document10 pagesOpening Balance - 3967575.73DIVYANSHU CHATURVEDINo ratings yet

- 1676983262212PL PDFDocument2 pages1676983262212PL PDFAnuj ChaudharyNo ratings yet

- Cam Ucv WorksheetDocument18 pagesCam Ucv WorksheetBheemrao GNo ratings yet

- Statement of Axis Account No:922010045406544 For The Period (From: 01-09-2022 To: 13-12-2022)Document2 pagesStatement of Axis Account No:922010045406544 For The Period (From: 01-09-2022 To: 13-12-2022)OPERATIONAL WINSTARNo ratings yet

- Statement of Account: No. 32A. Tingkat 1 Jalan Bds 2 Bukit Desa Semantan 28000 Temerloh, PahangDocument4 pagesStatement of Account: No. 32A. Tingkat 1 Jalan Bds 2 Bukit Desa Semantan 28000 Temerloh, PahangFerhan IskandarNo ratings yet

- Opening Balance - 4204276.88Document40 pagesOpening Balance - 4204276.88DIVYANSHU CHATURVEDINo ratings yet

- Ua STMT 0012052802901Document3 pagesUa STMT 0012052802901Gayan HewageNo ratings yet

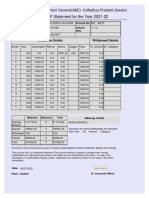

- GPF Statement For The Year 2021-22: O/o The Pr. Accountant General (A&E) - II, Madhya Pradesh, GwaliorDocument1 pageGPF Statement For The Year 2021-22: O/o The Pr. Accountant General (A&E) - II, Madhya Pradesh, GwaliorSHIVGOPAL KULHADENo ratings yet

- 919020094783017Document9 pages919020094783017BalaKrishna BadimelaNo ratings yet

- Savings Account - 07770100004804 Devendra Singh So Vikram S SolankiDocument2 pagesSavings Account - 07770100004804 Devendra Singh So Vikram S Solankianirudh singh solankiNo ratings yet

- Computation of Total Income Income From Business or Profession (Chapter IV D) 300000Document4 pagesComputation of Total Income Income From Business or Profession (Chapter IV D) 300000ramanNo ratings yet

- Girdhar51 1603693312542 PDFDocument2 pagesGirdhar51 1603693312542 PDFjignesh parmarNo ratings yet

- Unknown 2Document2 pagesUnknown 2Ketum XuanNo ratings yet

- Request For Payment: Payee InformationDocument3 pagesRequest For Payment: Payee InformationCaloi VillanuevaNo ratings yet

- Estatement20220609 000035402Document7 pagesEstatement20220609 000035402RamZee RoxNo ratings yet

- CSOAStatement 103769173Document4 pagesCSOAStatement 103769173Hasan AliNo ratings yet

- Credit Card Statement-5Document3 pagesCredit Card Statement-5ShraddhaNo ratings yet

- Employees' Provident Fund Organization, India: Challan SummaryDocument1 pageEmployees' Provident Fund Organization, India: Challan SummaryAshish ParmarNo ratings yet

- Satender NewDocument34 pagesSatender NewShivam SinghNo ratings yet

- Settlement Letter - 100000000468058Document3 pagesSettlement Letter - 100000000468058gajala jamirNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific-Seventh EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific-Seventh EditionNo ratings yet

- Jumla IsmiyyahDocument5 pagesJumla IsmiyyahHorticulture Sericulture GadwalNo ratings yet

- CamScanner 05-27-2022 10.56Document2 pagesCamScanner 05-27-2022 10.56Horticulture Sericulture GadwalNo ratings yet

- CamScanner 05-22-2022 21.07Document3 pagesCamScanner 05-22-2022 21.07Horticulture Sericulture GadwalNo ratings yet

- O.O No.65 Dt. 14.02.2022Document8 pagesO.O No.65 Dt. 14.02.2022Horticulture Sericulture GadwalNo ratings yet

- Ism PropertiesDocument8 pagesIsm PropertiesHorticulture Sericulture GadwalNo ratings yet

- TapScanner 04-28-2022-10 26Document71 pagesTapScanner 04-28-2022-10 26Horticulture Sericulture GadwalNo ratings yet

- Minhajul Arabiya Part 2Document81 pagesMinhajul Arabiya Part 2Horticulture Sericulture GadwalNo ratings yet

- Mihajul Arabiya Part 1Document68 pagesMihajul Arabiya Part 1Horticulture Sericulture GadwalNo ratings yet

- BNR English SlidesDocument67 pagesBNR English SlidesHorticulture Sericulture GadwalNo ratings yet

- یسرنا القران (رومن انگلش میں)Document65 pagesیسرنا القران (رومن انگلش میں)Horticulture Sericulture GadwalNo ratings yet

- Civil Service Exam Reviewer For Professional and Sub-Professional LevelsDocument6 pagesCivil Service Exam Reviewer For Professional and Sub-Professional LevelsSherylyn Cruz0% (1)

- Oracle® Inventory: Consigned Inventory From Supplier Process Guide Release 12.1Document76 pagesOracle® Inventory: Consigned Inventory From Supplier Process Guide Release 12.1Guillermo ToddNo ratings yet

- How To Write SpecificationsDocument9 pagesHow To Write SpecificationsLeilani ManalaysayNo ratings yet

- Mess Total TransectionsDocument92 pagesMess Total TransectionsFaisal ParachaNo ratings yet

- Searchinger Et Al Nature 2018Document4 pagesSearchinger Et Al Nature 2018Bjart HoltsmarkNo ratings yet

- Full Text 01Document115 pagesFull Text 01Datu Harrief Kamenza LaguiawanNo ratings yet

- Gender Inequality in Bangladesh PDFDocument20 pagesGender Inequality in Bangladesh PDFshakilnaimaNo ratings yet

- Habeas CorpusDocument67 pagesHabeas CorpusButch AmbataliNo ratings yet

- Plot Journey - Brett MacDonell PDFDocument4 pagesPlot Journey - Brett MacDonell PDFBrett MacDonellNo ratings yet

- Lirik KoreaDocument6 pagesLirik KoreaSabrina Winyard ChrisNo ratings yet

- Ball Lesson PlanDocument3 pagesBall Lesson Planapi-350245383No ratings yet

- Global ScriptDocument4 pagesGlobal ScriptAubrey Andrea OliverNo ratings yet

- Group BehaviourDocument13 pagesGroup Behaviourtasnim taherNo ratings yet

- PAL v. CIR (GR 198759)Document2 pagesPAL v. CIR (GR 198759)Erica Gana100% (1)

- Metabolic-Assessment-Form FullDocument6 pagesMetabolic-Assessment-Form FullOlesiaNo ratings yet

- Islamic Gardens: The Model of Alhambra Gardens in Granada: October 2020Document29 pagesIslamic Gardens: The Model of Alhambra Gardens in Granada: October 2020Yuna yasillaNo ratings yet

- Mision de Amistad Correspondence, 1986-1988Document9 pagesMision de Amistad Correspondence, 1986-1988david_phsNo ratings yet

- Propulsive PowerDocument13 pagesPropulsive PowerWaleedNo ratings yet

- Political Law Reviewer Bar 2019 Part 1 V 20 by Atty. Alexis Medina ACADEMICUSDocument27 pagesPolitical Law Reviewer Bar 2019 Part 1 V 20 by Atty. Alexis Medina ACADEMICUSalyamarrabeNo ratings yet

- Colin Campbell - Interview The Lady in WhiteDocument1 pageColin Campbell - Interview The Lady in WhiteMarcelo OlmedoNo ratings yet

- Caning Should Not Be Allowed in Schools TodayDocument2 pagesCaning Should Not Be Allowed in Schools TodayHolyZikr100% (2)

- Operating BudgetDocument38 pagesOperating BudgetRidwan O'connerNo ratings yet

- 90 + 100 + 5 - 7. 5 Tens, 3 Hundreds, 8 Ones - 8. 400 + 1000 + 20 + 8 - 9. 5 Hundreds, 6 Tens, 9 Ones - 10. 1 Hundred, 1 Thousands, 3 OnesDocument2 pages90 + 100 + 5 - 7. 5 Tens, 3 Hundreds, 8 Ones - 8. 400 + 1000 + 20 + 8 - 9. 5 Hundreds, 6 Tens, 9 Ones - 10. 1 Hundred, 1 Thousands, 3 OnesLorna HerillaNo ratings yet

- Walt Disney OutlineDocument9 pagesWalt Disney Outlineapi-234693246No ratings yet

- McDonald's RecipeDocument18 pagesMcDonald's RecipeoxyvilleNo ratings yet

- Developer GuideDocument313 pagesDeveloper GuideFradi EssilNo ratings yet

- A Scientific Report.: Daftar PustakaDocument3 pagesA Scientific Report.: Daftar PustakaFemmy FahiraNo ratings yet