You might also like

- 1968 Plymouth Service ManualDocument960 pages1968 Plymouth Service ManualСергей Филиппов100% (1)

- HTMLReportsDocument1 pageHTMLReportsRashmi Awanish PandeyNo ratings yet

- Chapter-21 (Solved Past Papers of CA Mod CDocument67 pagesChapter-21 (Solved Past Papers of CA Mod CJer Rama100% (4)

- The Law of Three StagesDocument7 pagesThe Law of Three StagesAkash KumarNo ratings yet

- REVENUE (Average) : 100.00% Gross Sales 1201000 1,201,000 Less: 0 Net Revenue 116,000Document2 pagesREVENUE (Average) : 100.00% Gross Sales 1201000 1,201,000 Less: 0 Net Revenue 116,000Saiyid Ali Haider RazaNo ratings yet

- The Accounting Cycle: Reporting Financial ResultsDocument8 pagesThe Accounting Cycle: Reporting Financial ResultsOmar KhanNo ratings yet

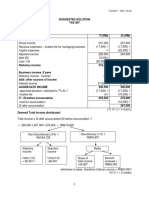

- Advanced Taxation - Solutions To Pilot Questions Suggested Solution To Question 1Document23 pagesAdvanced Taxation - Solutions To Pilot Questions Suggested Solution To Question 1Oyebisi OpeyemiNo ratings yet

- ACC106 Assignment AccountDocument5 pagesACC106 Assignment AccountsyafiqahNo ratings yet

- Ratio Analysis Numericals Including Reverse RatiosDocument6 pagesRatio Analysis Numericals Including Reverse RatiosFunny ManNo ratings yet

- Accounting 621Document2 pagesAccounting 621Sarah Precious NkoanaNo ratings yet

- Home Loan Testing FileDocument2 pagesHome Loan Testing Filejitendra tirthyaniNo ratings yet

- BCom Business Taxation Income Tax and Sales Tax Numerical 2018Document5 pagesBCom Business Taxation Income Tax and Sales Tax Numerical 2018AHSAN LASHARINo ratings yet

- Income Statement (T-Format)Document15 pagesIncome Statement (T-Format)Apryl TaiNo ratings yet

- R2. TAX (M.L) Solution CMA May-2023 ExamDocument5 pagesR2. TAX (M.L) Solution CMA May-2023 ExamSharif MahmudNo ratings yet

- BLT FINAL Assignment (Feb - June 2020) FINALDocument16 pagesBLT FINAL Assignment (Feb - June 2020) FINALSalman SajidNo ratings yet

- IT Assessment of Individuals IllustrationDocument5 pagesIT Assessment of Individuals Illustrationsyedfareed596No ratings yet

- Solved Past Papers Income Tax Numericals of ICMAP STAGE IV - (2003 TO 2015)Document45 pagesSolved Past Papers Income Tax Numericals of ICMAP STAGE IV - (2003 TO 2015)muneeb razaNo ratings yet

- The Statement of Comprehensive Income: Profit For The YearDocument4 pagesThe Statement of Comprehensive Income: Profit For The YearPlawan GhimireNo ratings yet

- Chapter 2 Capsule SessionDocument40 pagesChapter 2 Capsule SessionKshitishNo ratings yet

- 08 Spring 2015 BT AnsDocument8 pages08 Spring 2015 BT Anspabloescobar11yNo ratings yet

- A Practical Introduction To Australian Taxation Pages 301 To 325Document25 pagesA Practical Introduction To Australian Taxation Pages 301 To 325PuffleNo ratings yet

- MR BALIKDocument7 pagesMR BALIKGAMES EMPIRENo ratings yet

- Quiz 2 - Income Tax Concepts and ComplianceDocument3 pagesQuiz 2 - Income Tax Concepts and Compliancelc100% (1)

- Solution Test 2 (1) June 19Document5 pagesSolution Test 2 (1) June 19Nur Dina AbsbNo ratings yet

- Session 8 - Final Accounts - Practice ProblemsDocument16 pagesSession 8 - Final Accounts - Practice ProblemsanandakumarNo ratings yet

- 1 BTAXREV Week 2 Income TaxationDocument48 pages1 BTAXREV Week 2 Income TaxationgatotkaNo ratings yet

- CH 2 TAXATION ON INDIVIDUALS Slide 43 71Document8 pagesCH 2 TAXATION ON INDIVIDUALS Slide 43 71Casandra Nicole AldecoaNo ratings yet

- ACC 503 FinalDocument14 pagesACC 503 FinalFarid UddinNo ratings yet

- Cost Accounting: Rs. Rs. Rs. Rs. Rs. RsDocument8 pagesCost Accounting: Rs. Rs. Rs. Rs. Rs. RsShehrozSTNo ratings yet

- Ratio ExercisesDocument23 pagesRatio ExercisesPhumzile MpanzaNo ratings yet

- Corporate Financial Reporting PDFDocument3 pagesCorporate Financial Reporting PDFIshan SharmaNo ratings yet

- Business Examples 2021Document12 pagesBusiness Examples 2021Faizan HyderNo ratings yet

- PGP I 2021 Fra Quiz 1Document3 pagesPGP I 2021 Fra Quiz 1Pulkit SethiaNo ratings yet

- Solution Tax667 - Dec 2016Document7 pagesSolution Tax667 - Dec 2016Aiyani NabihahNo ratings yet

- Name of Company:-Madhura EnterprisesDocument39 pagesName of Company:-Madhura EnterprisesTaur VishalNo ratings yet

- CP9 - Contract CostingDocument15 pagesCP9 - Contract CostingesaiinternalauditNo ratings yet

- 2023 Hacc421hspac427 Supplementary ExaminationDocument6 pages2023 Hacc421hspac427 Supplementary Examinationagrippa [OrleanNo ratings yet

- Tax - Osman Gani - 22-23Document1 pageTax - Osman Gani - 22-23M N Sharif MintuNo ratings yet

- 2015 - Question 2 ANSWERDocument1 page2015 - Question 2 ANSWERTan TaylorNo ratings yet

- IT AssignmentDocument7 pagesIT AssignmentNipun AroraNo ratings yet

- Support Material Financial Statement PDFDocument6 pagesSupport Material Financial Statement PDFsanele dlaminiNo ratings yet

- MGT 101Document13 pagesMGT 101MuzzamilNo ratings yet

- Offer BreakUpDocument1 pageOffer BreakUpNaveenKumar S NNo ratings yet

- Corporate Taxes Part 1 (VAT, EWT and Income Tax) CaseDocument4 pagesCorporate Taxes Part 1 (VAT, EWT and Income Tax) CaseMikaela L. RoqueNo ratings yet

- REVENUE MODEL (Pilot Study) : Interest Expenses Sales Distribution Items PriceDocument1 pageREVENUE MODEL (Pilot Study) : Interest Expenses Sales Distribution Items PriceProtyay ChakrabortyNo ratings yet

- Tutorial 4 QAsDocument6 pagesTutorial 4 QAsJin HueyNo ratings yet

- 2017 BGSS 4E5N Prelim P2 AnsDocument6 pages2017 BGSS 4E5N Prelim P2 AnsDamien SeowNo ratings yet

- Suggested Answers TAX667 - DEC 2016Document7 pagesSuggested Answers TAX667 - DEC 2016diysNo ratings yet

- Week 10Document3 pagesWeek 10xinghe666No ratings yet

- Spiceland FA 6e Chap01 PPTDocument62 pagesSpiceland FA 6e Chap01 PPTkongvalerie7No ratings yet

- CAF 06 - TaxationDocument7 pagesCAF 06 - TaxationKhurram ShahzadNo ratings yet

- 2021 GeneralDocument8 pages2021 GeneralWajiha HaroonNo ratings yet

- Principles of Taxation Suggested Solution # 12 - (Mock Solution)Document9 pagesPrinciples of Taxation Suggested Solution # 12 - (Mock Solution)Ali OptimisticNo ratings yet

- Adjusting Entries - ProblemDocument1 pageAdjusting Entries - ProblemRianne NavidadNo ratings yet

- Solution Tax667 - Dec 2016Document7 pagesSolution Tax667 - Dec 2016Zahiratul QamarinaNo ratings yet

- Statement of Profit or Loss For The Year Ended 31 March 2009Document1 pageStatement of Profit or Loss For The Year Ended 31 March 2009Plawan GhimireNo ratings yet

- Mashood K ITR COMPUTATION AY 2022-23Document3 pagesMashood K ITR COMPUTATION AY 2022-23sidvikventuresNo ratings yet

- UBFI Resit Exam PaperDocument7 pagesUBFI Resit Exam PaperAdv Sailja Rohit DhootNo ratings yet

- Fabm2 Learning-Activity-2Document5 pagesFabm2 Learning-Activity-2Cha Eun WooNo ratings yet

- Taxation Solution 2018 SeptemberDocument9 pagesTaxation Solution 2018 SeptemberIffah NasuhaaNo ratings yet

- Rise School of Accountancy: Suggested Solution Test 08Document2 pagesRise School of Accountancy: Suggested Solution Test 08iamneonkingNo ratings yet

- MGN 341 Ca 03Document11 pagesMGN 341 Ca 03Akash KumarNo ratings yet

- Auditing Assignment 03Document12 pagesAuditing Assignment 03Akash KumarNo ratings yet

- Lecture From 17 To 22 SOCIOLOGYDocument42 pagesLecture From 17 To 22 SOCIOLOGYAkash KumarNo ratings yet

- Change Pointer in The Material Master in SAP ECCDocument1 pageChange Pointer in The Material Master in SAP ECCTaufik KadarusmanNo ratings yet

- Composite - Resin MatrixDocument62 pagesComposite - Resin MatrixNISHANT YADAVNo ratings yet

- M24-Plate Heat ExcahngerDocument16 pagesM24-Plate Heat ExcahngerAlexNo ratings yet

- Arvel Gentry-8-Checking - Trim - On - The - WindDocument3 pagesArvel Gentry-8-Checking - Trim - On - The - WindTom BeeNo ratings yet

- The Therapeutic Potential of Restoring Gamma Oscillations in Alzheimer's DiseaseDocument9 pagesThe Therapeutic Potential of Restoring Gamma Oscillations in Alzheimer's DiseaseCarlos Hernan Castañeda RuizNo ratings yet

- SPGMI Preview Fintech 2024 FINALDocument15 pagesSPGMI Preview Fintech 2024 FINALVignesh RaghunathanNo ratings yet

- A Critical Review On The Chemical and Biological Assessment of Current Wastewater Treatment (PDFDrive)Document120 pagesA Critical Review On The Chemical and Biological Assessment of Current Wastewater Treatment (PDFDrive)Edyazuan ChannelNo ratings yet

- Dirk Kruger MacroTheoryDocument308 pagesDirk Kruger MacroTheoryGurjot SinghNo ratings yet

- Chapter 9: Myths and LegendsDocument7 pagesChapter 9: Myths and LegendsLia TNo ratings yet

- Unitronics PLC InterfacingDocument4 pagesUnitronics PLC InterfacingJesse Rujel CorreaNo ratings yet

- George Bernard Shaw by Chesterton, G. K. (Gilbert Keith), 1874-1936Document75 pagesGeorge Bernard Shaw by Chesterton, G. K. (Gilbert Keith), 1874-1936Gutenberg.orgNo ratings yet

- Safe CitiesDocument20 pagesSafe CitiesSS DanushNo ratings yet

- Data Mining Comprehensive Exam - Regular PDFDocument3 pagesData Mining Comprehensive Exam - Regular PDFsrirams007No ratings yet

- Charlie-Rose Evans ResumeDocument3 pagesCharlie-Rose Evans Resumeapi-309085679No ratings yet

- Literature ReviewDocument14 pagesLiterature Reviewniftiangautam70% (2)

- Transition TheoryDocument36 pagesTransition TheoryMatty Jolbitado100% (1)

- Maharashtra State Board Class XII Chemistry Board Paper - 2016 SolutionDocument17 pagesMaharashtra State Board Class XII Chemistry Board Paper - 2016 SolutionSaniya MujawarNo ratings yet

- PHP Architect - 2017 01 JanuaryDocument52 pagesPHP Architect - 2017 01 JanuaryRafi SMNo ratings yet

- AIC Plans - All Key Characters and Responsibility Apr. 23Document26 pagesAIC Plans - All Key Characters and Responsibility Apr. 23Tiran AsawrusNo ratings yet

- AGTM12 09 Guide To Traffic Management Part 12 Traffic Impacts of DevelopmentsDocument115 pagesAGTM12 09 Guide To Traffic Management Part 12 Traffic Impacts of DevelopmentsSubhash ChavaNo ratings yet

- Page 1 of 5: Guidelines/green-Top-Guidelines/gtg - 67 - Endometrial - Hyperplasia PDFDocument5 pagesPage 1 of 5: Guidelines/green-Top-Guidelines/gtg - 67 - Endometrial - Hyperplasia PDFfitrah fajrianiNo ratings yet

- BTB Template Er-IntakeDocument3 pagesBTB Template Er-IntakeBoy MadNo ratings yet

- A Suitability Analysis: Spatial Analyst, Raster Data, and DemsDocument41 pagesA Suitability Analysis: Spatial Analyst, Raster Data, and DemsSTEPHANIE ELIZABETH MEDINA PONCENo ratings yet

- 11 Chapter 3Document72 pages11 Chapter 3Swati SagvekarNo ratings yet

- The Negative Impact of Cigarette Smoking: Mapeh (Health) 8-Quarter 4Document60 pagesThe Negative Impact of Cigarette Smoking: Mapeh (Health) 8-Quarter 4JOHN FRITS GERARD MOMBAYNo ratings yet

- FINAN204-21A - Tutorial 5 Week 6Document4 pagesFINAN204-21A - Tutorial 5 Week 6Danae YangNo ratings yet

- Xobni User ManualDocument31 pagesXobni User ManualBob Hails100% (1)

- Biot Savart LawDocument7 pagesBiot Savart LawTornadoNo ratings yet

- Task 1 Sla Interview QuestionsDocument2 pagesTask 1 Sla Interview QuestionsTESL10621 Jihan Syahirah Binti AzliNo ratings yet