You might also like

- BEC Mnemonics, Formulas, and Condensed ITDocument5 pagesBEC Mnemonics, Formulas, and Condensed ITmsanghavi1No ratings yet

- PWC Acquisition Deals ServicesDocument1 pagePWC Acquisition Deals Servicessaurabh bansalNo ratings yet

- Cost, Benefit & Risk Assessment For OutsourcingDocument18 pagesCost, Benefit & Risk Assessment For OutsourcingkritikandhariNo ratings yet

- JD - Supply Planner Aug 2019Document3 pagesJD - Supply Planner Aug 2019abhijeet3913No ratings yet

- Togaf 9.2 - RecapDocument7 pagesTogaf 9.2 - RecapkumarNo ratings yet

- CREW: National Aeronautics and Space Administration: NPOESS Nunn-McCurdy Decision Brief To JROCDocument16 pagesCREW: National Aeronautics and Space Administration: NPOESS Nunn-McCurdy Decision Brief To JROCCREWNo ratings yet

- Lecture 9 Part 2 Performance EvaluationDocument3 pagesLecture 9 Part 2 Performance EvaluationAryaman JunejaNo ratings yet

- p3 Acca QaDocument20 pagesp3 Acca QaMujeeb Don-The Fallen-AngelNo ratings yet

- Notes - Class 4Document3 pagesNotes - Class 4Majed Abou AlkhirNo ratings yet

- Balanced Scorecard: OM ER LA TI ON SH IPDocument5 pagesBalanced Scorecard: OM ER LA TI ON SH IPjpereztmpNo ratings yet

- The Framework and IAS 1: Presentation of Financial StatementsDocument24 pagesThe Framework and IAS 1: Presentation of Financial StatementsNeema EzekielNo ratings yet

- Key Presenters: Archita Sarma Parakram Hazarika Sandeep NagarkeDocument8 pagesKey Presenters: Archita Sarma Parakram Hazarika Sandeep NagarkeParakram HazarikaNo ratings yet

- CA Inter SM Memory Trick @CA - Study - NotesDocument9 pagesCA Inter SM Memory Trick @CA - Study - NotesYash SharmaNo ratings yet

- Logi AngleDocument16 pagesLogi AngleLogiangleNo ratings yet

- Memory Techniques: CHP 1: Automated Business ProcessDocument10 pagesMemory Techniques: CHP 1: Automated Business ProcessShubhodeep ChatterjeeNo ratings yet

- Scottish Procurement Competency Framework June 2020Document42 pagesScottish Procurement Competency Framework June 2020መቅዲ ሀበሻዊትNo ratings yet

- COSO PrinciplesDocument22 pagesCOSO PrinciplesA R AdILNo ratings yet

- Mit Quiz 1 ReviewerDocument6 pagesMit Quiz 1 ReviewerEleina Bea BernardoNo ratings yet

- Asset Lifecycle MGMT v6.2Document53 pagesAsset Lifecycle MGMT v6.2shanmugaNo ratings yet

- Diploma in Treasury, Investement and Risk Management Paper I Financial Markets - An OverviewDocument22 pagesDiploma in Treasury, Investement and Risk Management Paper I Financial Markets - An OverviewhvenkiNo ratings yet

- NSSE 2011 Nirmalya Applications of SEDocument48 pagesNSSE 2011 Nirmalya Applications of SEAbhinav GauravNo ratings yet

- Chapter6-Investment DecisionDocument14 pagesChapter6-Investment DecisionchandoraNo ratings yet

- Presentation CIA 2 PDFDocument19 pagesPresentation CIA 2 PDFVaishali MoitraNo ratings yet

- 1) - 1) - 1) Sharing Aftersales Vision and MissionDocument9 pages1) - 1) - 1) Sharing Aftersales Vision and MissionVinay BhiryaniNo ratings yet

- CDD HR Proficiency MappingDocument8 pagesCDD HR Proficiency MappingManaswiNo ratings yet

- Gestion Des Risques Séance 6Document13 pagesGestion Des Risques Séance 6Abdellatif LachoucheNo ratings yet

- Lean Construction - A Guide For Financial ManagersDocument27 pagesLean Construction - A Guide For Financial Managersprasmyth6897No ratings yet

- AIG Hedge Fund Start-Up ChecklistDocument4 pagesAIG Hedge Fund Start-Up ChecklistWilde RosnyNo ratings yet

- Introduction To OR and Linear Algebra: Part-IDocument26 pagesIntroduction To OR and Linear Algebra: Part-Ipiyush kumarNo ratings yet

- SCM Ch-10Document12 pagesSCM Ch-10Teneg82No ratings yet

- Systems Analysis: 1. Analytical 2. InterpersonalDocument10 pagesSystems Analysis: 1. Analytical 2. InterpersonalJARELL HANZ DAMIANNo ratings yet

- Credit Rating: Presented By: Group 3Document13 pagesCredit Rating: Presented By: Group 3urssubhaNo ratings yet

- Ch.4 Strategies in ActionDocument40 pagesCh.4 Strategies in Actionleondashie143No ratings yet

- BMM 3023 Eng MGT and Safety Module 3Document17 pagesBMM 3023 Eng MGT and Safety Module 3zain asroyNo ratings yet

- 01 Configuration Phase I - Financial AccountingDocument36 pages01 Configuration Phase I - Financial Accountingsumber kocakNo ratings yet

- 2016 0306 Circle of RisksDocument1 page2016 0306 Circle of RisksJonathan WeissNo ratings yet

- Feasibility Study (Compatibility Mode)Document35 pagesFeasibility Study (Compatibility Mode)Deep ShahNo ratings yet

- MOF All Oct08Document1 pageMOF All Oct08Miguel AedoNo ratings yet

- Solution Manual Managerial Economics 7th Edition AllenDocument33 pagesSolution Manual Managerial Economics 7th Edition AllenAlexander Dimalipos100% (2)

- MIDTERM Strategic 11-12Document10 pagesMIDTERM Strategic 11-12nairajaneNo ratings yet

- Agile Project Management: State of The Art in IS Abdullah Khan - Salim GouasmiaDocument31 pagesAgile Project Management: State of The Art in IS Abdullah Khan - Salim GouasmiaAbdullah KhanNo ratings yet

- ISO 9001 ISO 14001 ISO.9186209.powerpointDocument4 pagesISO 9001 ISO 14001 ISO.9186209.powerpointJoséchu AnadónNo ratings yet

- Top Down Goals 5Document53 pagesTop Down Goals 5Sylvia VhetiNo ratings yet

- Management by Objectives: Crafting and Executing StrategyDocument21 pagesManagement by Objectives: Crafting and Executing StrategyvadevalorNo ratings yet

- ENR 405 - Lecture 1posted-1Document150 pagesENR 405 - Lecture 1posted-1sabri karaNo ratings yet

- Michael+Mccaffery CpaDocument2 pagesMichael+Mccaffery CpaMichael McCafferyNo ratings yet

- Dempe - Development, Enhancement, Maintenance, Protection & Exploitation of IntangiblesDocument33 pagesDempe - Development, Enhancement, Maintenance, Protection & Exploitation of IntangiblesharryNo ratings yet

- ForecastingDocument21 pagesForecastingnNo ratings yet

- Entrep Chapter 2 Group 1Document43 pagesEntrep Chapter 2 Group 1abisha samalaNo ratings yet

- Determination For Success Determin: Continuing The Legacy of 50 Years of Excellence Continuing The LDocument94 pagesDetermination For Success Determin: Continuing The Legacy of 50 Years of Excellence Continuing The LHasaan Bin ArifNo ratings yet

- Captive Outsourcing Model DraftDocument14 pagesCaptive Outsourcing Model DraftArchitNo ratings yet

- 8.9.10.decision Analysisi and Portfolio ManagementDocument33 pages8.9.10.decision Analysisi and Portfolio ManagementBuğrahan İlginNo ratings yet

- PRO Ofessiona Al Synopsis SDocument3 pagesPRO Ofessiona Al Synopsis SSupriya patilNo ratings yet

- Presentation - Approach To Zero BreakdownDocument20 pagesPresentation - Approach To Zero Breakdownypchawla50% (4)

- Marketing Management: Group EDocument19 pagesMarketing Management: Group EMohd Tawher Ashraf Siddiqui SadatNo ratings yet

- Memorization Chart (Process Groups & Knowledge Areas)Document3 pagesMemorization Chart (Process Groups & Knowledge Areas)Rounak VijayNo ratings yet

- Analysis of Financial Statements: Wild and Shaw Financial and Managerial Accounting 8th EditionDocument83 pagesAnalysis of Financial Statements: Wild and Shaw Financial and Managerial Accounting 8th EditionDarronNo ratings yet

- Contemporary Management-Assignment 4Document22 pagesContemporary Management-Assignment 4Ramy MoustafaNo ratings yet

- Passive Currency Overlay: How To Effectively Manage Your Currency Risk?Document18 pagesPassive Currency Overlay: How To Effectively Manage Your Currency Risk?남상욱No ratings yet

- How to Select Investment Managers and Evaluate Performance: A Guide for Pension Funds, Endowments, Foundations, and TrustsFrom EverandHow to Select Investment Managers and Evaluate Performance: A Guide for Pension Funds, Endowments, Foundations, and TrustsNo ratings yet

- The Environment and Corporate Culture: True/False QuestionsDocument21 pagesThe Environment and Corporate Culture: True/False QuestionsĐỗ Hiếu ThuậnNo ratings yet

- Accelerating IceCubes Photon Propagation Code WitDocument11 pagesAccelerating IceCubes Photon Propagation Code WitNEed for workNo ratings yet

- Guia de Usuario Sokkia LinkDocument81 pagesGuia de Usuario Sokkia LinkEdwin VelasquezNo ratings yet

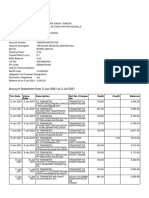

- Account Statement From 3 Jan 2021 To 3 Jul 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument8 pagesAccount Statement From 3 Jan 2021 To 3 Jul 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceSanatan ThakurNo ratings yet

- Live Video Analytics at Scale With Approximation and Delay-ToleranceDocument17 pagesLive Video Analytics at Scale With Approximation and Delay-TolerancejsprchinaNo ratings yet

- Sundaram ClaytonDocument207 pagesSundaram ClaytonReTHINK INDIANo ratings yet

- Sop SampleDocument2 pagesSop Samplearshpreet bhatiaNo ratings yet

- Master Trip Relay PDFDocument2 pagesMaster Trip Relay PDFEr Suraj KumarNo ratings yet

- AERVOE 41197pdsDocument2 pagesAERVOE 41197pdsJamer CruzadoNo ratings yet

- Cryptography and Its Types - GeeksforGeeksDocument2 pagesCryptography and Its Types - GeeksforGeeksGirgio Moratti CullenNo ratings yet

- Lesson 2Document10 pagesLesson 2Anore James IvanNo ratings yet

- 2Kv Hdfpc-Dlo, Rhh/Rhw-2 & Rw90: Flexible Stranded Rope-Lay Class I Tinned Copper Per ASTM B33 and B172Document3 pages2Kv Hdfpc-Dlo, Rhh/Rhw-2 & Rw90: Flexible Stranded Rope-Lay Class I Tinned Copper Per ASTM B33 and B172gerrzen64No ratings yet

- Tray Manual 3.8Document193 pagesTray Manual 3.8Bjorn FejerNo ratings yet

- LG 23MT77V LW50A Schematic Diagram and Service ManualDocument34 pagesLG 23MT77V LW50A Schematic Diagram and Service Manualaze1959No ratings yet

- Perilaku Masyarakat Terhadap Kesehatan Lingkungan (Studi Di Pantai Desa Ketong Kecamatan Balaesang Tanjung Kabupaten Donggala)Document11 pagesPerilaku Masyarakat Terhadap Kesehatan Lingkungan (Studi Di Pantai Desa Ketong Kecamatan Balaesang Tanjung Kabupaten Donggala)Ali BaktiNo ratings yet

- M2 Pre-Task: Application Software - System Software Driver Software Programming SoftwareDocument2 pagesM2 Pre-Task: Application Software - System Software Driver Software Programming SoftwareBee Anne BiñasNo ratings yet

- CAAM-Drone Requirement 2020Document6 pagesCAAM-Drone Requirement 2020nasser4858No ratings yet

- Elektor Electronics 1998-10Document54 pagesElektor Electronics 1998-10Adrian_Andrei_4433No ratings yet

- TM AHU 60R410A Onoff T SA NA 171205Document67 pagesTM AHU 60R410A Onoff T SA NA 171205Sam RVNo ratings yet

- Lecture-13 Indexing and Its Types: Subject: DBMS Subject Code: BCA-S301T Faculty: Saurabh JhaDocument16 pagesLecture-13 Indexing and Its Types: Subject: DBMS Subject Code: BCA-S301T Faculty: Saurabh JhaShivam KushwahaNo ratings yet

- 4150 70-37-3 Requirement AnalysisDocument71 pages4150 70-37-3 Requirement AnalysisSreenath SreeNo ratings yet

- Satellite TTC Module 4Document21 pagesSatellite TTC Module 4AmitNo ratings yet

- Supercars Final Newcastle Destination Management Plan June 19 2013Document59 pagesSupercars Final Newcastle Destination Management Plan June 19 2013api-692698304No ratings yet

- Power Learning Strategies Success College Life 7th Edition Feldman Test BankDocument24 pagesPower Learning Strategies Success College Life 7th Edition Feldman Test BankKathyHernandeznobt100% (32)

- Module 11A.5.2 L1 2016-08-16Document234 pagesModule 11A.5.2 L1 2016-08-16Abdul Aziz KhanNo ratings yet

- Indian Institute of Technology: Delhi Summary Sheet Consumable StoresDocument2 pagesIndian Institute of Technology: Delhi Summary Sheet Consumable StoresSumit SinghNo ratings yet

- Juhi S. Khandekar: Email ID: Contact (M) : +91-7710007972Document1 pageJuhi S. Khandekar: Email ID: Contact (M) : +91-7710007972Reddi SyamsundarNo ratings yet

- Factors Affecting System Complexity: CouplingDocument4 pagesFactors Affecting System Complexity: CouplingJaskirat KaurNo ratings yet

- Kampung Admiralty - A Mix of Public Facilities - UrbanNextDocument7 pagesKampung Admiralty - A Mix of Public Facilities - UrbanNextkohvictorNo ratings yet

- Level Wound Copper TubeDocument1 pageLevel Wound Copper TubeAamer Abdul MajeedNo ratings yet