You might also like

- Corporate Bonds and Structured Financial ProductsFrom EverandCorporate Bonds and Structured Financial ProductsRating: 5 out of 5 stars5/5 (1)

- Prime BrokerageDocument28 pagesPrime BrokeragePrat Don100% (1)

- January 2010 Summit County Real Estate StatsDocument7 pagesJanuary 2010 Summit County Real Estate StatsBreckenridge Grand Real EstateNo ratings yet

- Summit-04-05-06-07-08-09 Full Year Dec.Document1 pageSummit-04-05-06-07-08-09 Full Year Dec.Breckenridge Grand Real EstateNo ratings yet

- Solutions Balancing Process Capacity Simulation Challenge 1 and Challange 2Document29 pagesSolutions Balancing Process Capacity Simulation Challenge 1 and Challange 2Mariam AlraeesiNo ratings yet

- RVA - FTTH Council Presentation 09-2010Document8 pagesRVA - FTTH Council Presentation 09-2010StimulatingBroadband.comNo ratings yet

- Q1 2011 Quarterly EarningsDocument15 pagesQ1 2011 Quarterly EarningsRip Empson100% (1)

- Gross Domestic Product (GDP) at Current PricesDocument4 pagesGross Domestic Product (GDP) at Current PricesChakma MansonNo ratings yet

- Aquarius Company Worksheet August 31, 2018: Unadjusted Trial Balance Debit CreditDocument35 pagesAquarius Company Worksheet August 31, 2018: Unadjusted Trial Balance Debit CreditAdam Cuenca100% (1)

- 2018 Statistical Highlights PDFDocument7 pages2018 Statistical Highlights PDFBernewsAdminNo ratings yet

- MDKA SucorDocument6 pagesMDKA SucorFathan MujibNo ratings yet

- ME CIA3 BepDocument4 pagesME CIA3 BepSanjana A 1910217No ratings yet

- Summit 04-05-06-07-08-09 Nov. 09Document1 pageSummit 04-05-06-07-08-09 Nov. 09Breckenridge Grand Real EstateNo ratings yet

- Solution Manual For Essentials of Corporate Finance 9Th Edition by Ross Westerfield Jordan Isbn 1259277216 9781259277214 Full Chapter PDFDocument36 pagesSolution Manual For Essentials of Corporate Finance 9Th Edition by Ross Westerfield Jordan Isbn 1259277216 9781259277214 Full Chapter PDFethel.gay851100% (12)

- Uts DdaDocument12 pagesUts Ddaqyrf6g5dk7No ratings yet

- DK Profile2010 2K 10mar2011Document48 pagesDK Profile2010 2K 10mar2011kodirNo ratings yet

- MA Newsletter Q1 2024Document12 pagesMA Newsletter Q1 2024Kevin ParkerNo ratings yet

- National Communications Forum: Session PCS 10 Wireless Broadband AccessDocument39 pagesNational Communications Forum: Session PCS 10 Wireless Broadband AccessJoe M. Mera DiazNo ratings yet

- SCA SunsetDocument483 pagesSCA SunsetsunsetmusicvideosNo ratings yet

- Industry Statistics Auto Components 09Document7 pagesIndustry Statistics Auto Components 09ManishNo ratings yet

- Credit Approval Decisions CodedDocument7 pagesCredit Approval Decisions CodedvarunNo ratings yet

- Week 5 Balancing Process Capacity Simulation Slides Challenge1 and Challenge 2 HHv2Document23 pagesWeek 5 Balancing Process Capacity Simulation Slides Challenge1 and Challenge 2 HHv2Mariam AlraeesiNo ratings yet

- Long-Term Care Insurance (Susan Coronel)Document24 pagesLong-Term Care Insurance (Susan Coronel)National Press FoundationNo ratings yet

- Cameron Alexander, Director Metals Demand Asia, GFMS: August 2018Document13 pagesCameron Alexander, Director Metals Demand Asia, GFMS: August 2018Olivia JacksonNo ratings yet

- Aayushi Sharma - Roll No. 487 Nitesh Daryanani - Roll No. 505Document40 pagesAayushi Sharma - Roll No. 487 Nitesh Daryanani - Roll No. 505Gaurav MeenaNo ratings yet

- EMI Calculator - Prepayment OptionDocument18 pagesEMI Calculator - Prepayment Optionpranil deshmukhNo ratings yet

- Zoned To Shrink PresentationDocument33 pagesZoned To Shrink PresentationWVXU NewsNo ratings yet

- Triple - M-Trading - SARAYDocument10 pagesTriple - M-Trading - SARAYLaiza Cristella SarayNo ratings yet

- Q4 2010 Quarterly EarningsDocument15 pagesQ4 2010 Quarterly EarningsAlexia BonatsosNo ratings yet

- Investments: Analysis and Behavior: Chapter 1-IntroductionDocument26 pagesInvestments: Analysis and Behavior: Chapter 1-IntroductionJeralyn MacarealNo ratings yet

- Harrisons 2022 Annual Report Final CompressedDocument152 pagesHarrisons 2022 Annual Report Final Compressedarusmajuenterprise80No ratings yet

- 2020 Annual Report JamaicaDocument156 pages2020 Annual Report JamaicaJasmine JacksonNo ratings yet

- November 2022Document14 pagesNovember 2022yudha palaganNo ratings yet

- Bank Recon Seatwork PDFDocument2 pagesBank Recon Seatwork PDFhfjhdjhfjdeh100% (1)

- Bank Recon SeatworkDocument2 pagesBank Recon SeatworkhfjhdjhfjdehNo ratings yet

- Breakeven-Analysis 2Document1 pageBreakeven-Analysis 2walterNo ratings yet

- PNB Housing Finance Liquidity Update - 1st Oct 18Document9 pagesPNB Housing Finance Liquidity Update - 1st Oct 18swanand samantNo ratings yet

- Revised Alfalah Solar Financing - Mr. JahanzaibDocument3 pagesRevised Alfalah Solar Financing - Mr. JahanzaibChaudhary Muhammad Suban TasirNo ratings yet

- BDO Unibank 2019-Annual-Report-Financial-Supplements PDFDocument228 pagesBDO Unibank 2019-Annual-Report-Financial-Supplements PDFCristine AquinoNo ratings yet

- Google Q3 2008 Quarterly Earnings SummaryDocument15 pagesGoogle Q3 2008 Quarterly Earnings SummaryEd McManus100% (1)

- PYN Elite Presentation - EN 2Document18 pagesPYN Elite Presentation - EN 2Đặng Xuân HiểuNo ratings yet

- State of Venture Q1'24 ReportDocument222 pagesState of Venture Q1'24 Reportikhan809No ratings yet

- FM AssignmentDocument27 pagesFM AssignmentMuhammad AkbarNo ratings yet

- Google PresentationDocument22 pagesGoogle Presentationcia100% (10)

- EMI Calculator - Prepayment OptionDocument15 pagesEMI Calculator - Prepayment OptionPrateekSorteNo ratings yet

- 3 Mining Platform Mike Da CostaDocument20 pages3 Mining Platform Mike Da CostaJEAN MICHEL ALONZEAUNo ratings yet

- Ae211 Finals QuizDocument20 pagesAe211 Finals QuizDJAN IHIAZEL DELA CUADRANo ratings yet

- US Agency Mortgage Backed Securities FINAL YB v04Document24 pagesUS Agency Mortgage Backed Securities FINAL YB v04shahzaib100% (1)

- Rich HS Community Options Presentation 62019Document38 pagesRich HS Community Options Presentation 62019Burton PhillipsNo ratings yet

- Natasha Kingery CaseDocument5 pagesNatasha Kingery CaseAlan BublathNo ratings yet

- Invest EarlyDocument2 pagesInvest EarlymetaldwarfNo ratings yet

- NP EX19 9b JinruiDong 2Document10 pagesNP EX19 9b JinruiDong 2Ike DongNo ratings yet

- Bsais 4JDocument18 pagesBsais 4JArjay DeausenNo ratings yet

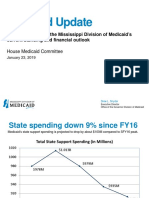

- Medicaid House PresentationDocument11 pagesMedicaid House PresentationRuss LatinoNo ratings yet

- Ujjaval Modi 1Document6 pagesUjjaval Modi 1Barrett M82No ratings yet

- MTDrill 2Document17 pagesMTDrill 2Cedric Legaspi TagalaNo ratings yet

- Merchant Acquiring: How To Win in A Digital World: White PaperDocument13 pagesMerchant Acquiring: How To Win in A Digital World: White PaperMuumini De Souza NezzaNo ratings yet

- Draft Presentation Meeting Pak KomsanDocument2 pagesDraft Presentation Meeting Pak KomsantatosumartoNo ratings yet

- Bank Market PowerDocument18 pagesBank Market PowerWahyutri IndonesiaNo ratings yet

- All Sister Concern ProfileDocument15 pagesAll Sister Concern Profileanowar hossainNo ratings yet

- Demystifying The ICT Questionnaire 1 2Document3 pagesDemystifying The ICT Questionnaire 1 2Thar RharNo ratings yet

- Trades About To Happen - David Weiss - Notes FromDocument3 pagesTrades About To Happen - David Weiss - Notes FromUma Maheshwaran100% (1)

- PTron Tangent Duo Neckband (Amazon) InvoiceDocument1 pagePTron Tangent Duo Neckband (Amazon) InvoiceSydney DmelloNo ratings yet

- The Fiscal Impact and Policy Response To Covid 19 in VietnamDocument19 pagesThe Fiscal Impact and Policy Response To Covid 19 in VietnamNGHIÊM NGUYỄN MINHNo ratings yet

- LearnEnglish Reading B2 The Sharing Economy PDFDocument4 pagesLearnEnglish Reading B2 The Sharing Economy PDFKhaled MohmedNo ratings yet

- 2018 10 Exam FM Sample QuestionsDocument137 pages2018 10 Exam FM Sample QuestionsRuoyuNo ratings yet

- Birzeit University Department of Economics Public Finance, ECON 434Document2 pagesBirzeit University Department of Economics Public Finance, ECON 434Dina OdehNo ratings yet

- JAIIB 2024 BrochureDocument13 pagesJAIIB 2024 BrochureSUBRAMANIAN NAGANo ratings yet

- ARL-300 EU Declaration of Conformity - enDocument3 pagesARL-300 EU Declaration of Conformity - enSamir Ben RomdhaneNo ratings yet

- Medyo FPLDocument10 pagesMedyo FPLJade Anne Mercado BalmesNo ratings yet

- Ecuador's Ministry of Tourism's Seeks Foreign Investment in The Galapagos IslandsDocument4 pagesEcuador's Ministry of Tourism's Seeks Foreign Investment in The Galapagos IslandsSalvaGalapagosNo ratings yet

- Criteria For The Choice of Business OrganizationDocument2 pagesCriteria For The Choice of Business OrganizationKavita SinghNo ratings yet

- Econs Notes AusmatDocument49 pagesEcons Notes Ausmatashleymae19No ratings yet

- Gen Math - Q2 - SLM - WK3Document9 pagesGen Math - Q2 - SLM - WK3Floraville Lamoste-MerencilloNo ratings yet

- July Allegheny County Employee Executive ActionsDocument71 pagesJuly Allegheny County Employee Executive ActionsAllegheny JOB WatchNo ratings yet

- Chapter 3Document14 pagesChapter 3phan hàNo ratings yet

- Determinants of Interest Rate Spreads Among Licensed Commercial Banks in KenyaDocument8 pagesDeterminants of Interest Rate Spreads Among Licensed Commercial Banks in KenyaViverNo ratings yet

- Securities ProjectDocument7 pagesSecurities ProjectShwetha PrakashNo ratings yet

- Tourism Statistics2019Document10 pagesTourism Statistics2019Atish KissoonNo ratings yet

- APO Workshop On Implementing KMDocument14 pagesAPO Workshop On Implementing KMmehdiNo ratings yet

- Man 307 Business Finance Study Questions and Answers xd3dDocument5 pagesMan 307 Business Finance Study Questions and Answers xd3dCallie NguyenNo ratings yet

- OPMT 5701 Multivariable Optimization: 1 Two Variable MaximizationDocument21 pagesOPMT 5701 Multivariable Optimization: 1 Two Variable MaximizationJulian CamiloNo ratings yet

- GE 11 Third ExamDocument2 pagesGE 11 Third ExamJENDRI ELLORINNo ratings yet

- Financial Ratio Analysis (ACI)Document17 pagesFinancial Ratio Analysis (ACI)Rayhan MamunNo ratings yet

- Poa T - 13Document3 pagesPoa T - 13SHEVENA A/P VIJIANNo ratings yet

- Financial Inclusion - RBI - S InitiativesDocument12 pagesFinancial Inclusion - RBI - S Initiativessahil_saini298No ratings yet

- Capacity and Constraint ManagementDocument30 pagesCapacity and Constraint ManagementtayerNo ratings yet

- RECEIPT UTILITIES 20210312 Elektrik EapDocument1 pageRECEIPT UTILITIES 20210312 Elektrik EapTahap TeknikNo ratings yet