You might also like

- IA 1 - Chapter 6 Notes Receivable Problems Part 2Document11 pagesIA 1 - Chapter 6 Notes Receivable Problems Part 2John CentinoNo ratings yet

- Sol. Man. - Chapter 6 - Receivables Addtl Concept - Ia Part 1aDocument7 pagesSol. Man. - Chapter 6 - Receivables Addtl Concept - Ia Part 1aJenny Joy Alcantara0% (1)

- Angelica S. Rubios: Problem 10-19Document4 pagesAngelica S. Rubios: Problem 10-19Angel RubiosNo ratings yet

- Problem 11-7 Given:: Date Payment 10% Interest Principal Present ValueDocument2 pagesProblem 11-7 Given:: Date Payment 10% Interest Principal Present ValueDominic RomeroNo ratings yet

- Sol. Man. - Chapter 6 - Teacher's Manual - Ia Part 1aDocument7 pagesSol. Man. - Chapter 6 - Teacher's Manual - Ia Part 1aYamateNo ratings yet

- (Ust-Jpia) Quiz 1 Intermediate Accounting 2 Solution ManualDocument6 pages(Ust-Jpia) Quiz 1 Intermediate Accounting 2 Solution ManualRENZ ALFRED ASTRERONo ratings yet

- 93 - Final Preaboard AFAR SolutionsDocument11 pages93 - Final Preaboard AFAR SolutionsLeiNo ratings yet

- 5 27 LoansDocument9 pages5 27 LoansRengeline LucasNo ratings yet

- Audit of Liabilities SolManDocument3 pagesAudit of Liabilities SolManReyn Saplad PeralesNo ratings yet

- Audit of Long Term Liabilities 2Document5 pagesAudit of Long Term Liabilities 2Cesar EsguerraNo ratings yet

- Chapter 29Document6 pagesChapter 29Shane Ivory ClaudioNo ratings yet

- CPA Review School of The Philippines ManilaDocument4 pagesCPA Review School of The Philippines ManilaSophia PerezNo ratings yet

- Cpa Review School of The Philippines.2Document6 pagesCpa Review School of The Philippines.2Snow TurnerNo ratings yet

- 06 Notes Receivable Sec 2 MCPDocument3 pages06 Notes Receivable Sec 2 MCPkyle mandaresioNo ratings yet

- Intermediate Accounting 2 Millan 221013 124345Document233 pagesIntermediate Accounting 2 Millan 221013 124345Krazy Butterfly100% (1)

- Akm 2Document10 pagesAkm 2Putu DenyNo ratings yet

- Quiz Box 2 - QuestionnairesDocument13 pagesQuiz Box 2 - QuestionnairesCamila Mae AlduezaNo ratings yet

- Receivable Financing Receivable FinancingDocument10 pagesReceivable Financing Receivable FinancingMarjorie PalmaNo ratings yet

- Quiz 2 - Audit of Receivables SolutionDocument1 pageQuiz 2 - Audit of Receivables SolutionmillescaasiNo ratings yet

- Chapter 7 - Teacher's Manual - Ifa Part 1aDocument7 pagesChapter 7 - Teacher's Manual - Ifa Part 1aCharmae Agan CaroroNo ratings yet

- Loan ReceivableDocument10 pagesLoan ReceivableClyde SaladagaNo ratings yet

- Business Combi CH 6 de JesusDocument9 pagesBusiness Combi CH 6 de JesusMerel Rose FloresNo ratings yet

- Ia2 Final Exam A Test Bank - CompressDocument32 pagesIa2 Final Exam A Test Bank - CompressFiona MiralpesNo ratings yet

- FAR Problem Quiz 2Document3 pagesFAR Problem Quiz 2Ednalyn CruzNo ratings yet

- Problem 6-8 Answer A Savage CompanyDocument6 pagesProblem 6-8 Answer A Savage CompanyJurie BalandacaNo ratings yet

- In Acc Chris Jean Paden BsaDocument6 pagesIn Acc Chris Jean Paden BsaJurie BalandacaNo ratings yet

- Finalchapter 17Document4 pagesFinalchapter 17Jud Rossette ArcebesNo ratings yet

- In Acc April Lyn Limsan BsaDocument6 pagesIn Acc April Lyn Limsan BsaJurie BalandacaNo ratings yet

- AC13.1.2 Module 1 Answer KeyDocument6 pagesAC13.1.2 Module 1 Answer KeyDianaNo ratings yet

- Problem 6-8 Answer A Savage CompanyDocument6 pagesProblem 6-8 Answer A Savage CompanyJurie BalandacaNo ratings yet

- Inter AccDocument6 pagesInter AccshaylieeeNo ratings yet

- F7 - Mock A - AnswersDocument6 pagesF7 - Mock A - AnswerspavishneNo ratings yet

- Exercise 14Document11 pagesExercise 14dwitaNo ratings yet

- 188073f7174b4401b2d0a1b25da700e9Document4 pages188073f7174b4401b2d0a1b25da700e9520Sri Wahyuni NgabalinNo ratings yet

- Q3a. Capital Budget AssignmentDocument1 pageQ3a. Capital Budget AssignmentMorgan MunyoroNo ratings yet

- BONEO Pup Receivables3 SRC 2 1Document13 pagesBONEO Pup Receivables3 SRC 2 1hellokittysaranghaeNo ratings yet

- Notes Receivable: Long QuizDocument8 pagesNotes Receivable: Long Quizfinn mertensNo ratings yet

- RecFin AnswerKeySolutionsDocument3 pagesRecFin AnswerKeySolutionsHannah Jane UmbayNo ratings yet

- Loan Receivable ProblemsDocument6 pagesLoan Receivable ProblemsKathleen Frondozo100% (1)

- Chapter 1 - Contingent LiabilitiesDocument6 pagesChapter 1 - Contingent LiabilitiesJoshua AbanalesNo ratings yet

- RECEIVABLESDocument3 pagesRECEIVABLESJACQUELYN PABLITONo ratings yet

- Answers - Chapter 1 - Current LiabilitiesDocument5 pagesAnswers - Chapter 1 - Current LiabilitiesLhica EsterasNo ratings yet

- 02 FAR02-answersDocument18 pages02 FAR02-answersBea GarciaNo ratings yet

- Chapter 1-Problems Problems 1 Problems 2Document3 pagesChapter 1-Problems Problems 1 Problems 2Angela Ricaplaza ReveralNo ratings yet

- FR Mock Exam 4 - SolutionsDocument13 pagesFR Mock Exam 4 - Solutionsiram2005No ratings yet

- Problem SolutionsDocument6 pagesProblem SolutionsLovenia M. FerrerNo ratings yet

- Chapter 29Document19 pagesChapter 29Darlianne Klyne BayerNo ratings yet

- Finman Chapter 7Document6 pagesFinman Chapter 7Maria Kathreena Andrea AdevaNo ratings yet

- (Chapter 1) Sol Man Intermediate Accounting 2 by Zeus MillanDocument8 pages(Chapter 1) Sol Man Intermediate Accounting 2 by Zeus MillanJonathan Villazon Rosales67% (3)

- Batch 17 1st Preboard (P1)Document13 pagesBatch 17 1st Preboard (P1)Jericho Pedragosa100% (1)

- QUESTION 3 (B) - TAXATION OF INCOME - November 30, 2022Document4 pagesQUESTION 3 (B) - TAXATION OF INCOME - November 30, 2022Nathan NakibingeNo ratings yet

- Midterms Quiz 2 Answers PDFDocument7 pagesMidterms Quiz 2 Answers PDFFranz Campued100% (1)

- IFRS16 Lease In-Class PracticesDocument11 pagesIFRS16 Lease In-Class PracticesDAN NGUYEN THENo ratings yet

- Tutor UasDocument13 pagesTutor UasHENDY YUDHA PRAMANANo ratings yet

- Provisions, Contingencies and Other Liabilities ProblemsDocument7 pagesProvisions, Contingencies and Other Liabilities ProblemsGiander100% (1)

- Audit Probs 4 (Final Exam)Document6 pagesAudit Probs 4 (Final Exam)YameteKudasaiNo ratings yet

- Answer Key Final Exam IA 2Document4 pagesAnswer Key Final Exam IA 2Carlos arnaldo lavadoNo ratings yet

- Ia 2 Final Exam Answer KeyDocument17 pagesIa 2 Final Exam Answer KeyIrene Grace Edralin AdenaNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionNo ratings yet

- Finding Balance 2023: Benchmarking Performance and Building Climate Resilience in Pacific State-Owned EnterprisesFrom EverandFinding Balance 2023: Benchmarking Performance and Building Climate Resilience in Pacific State-Owned EnterprisesNo ratings yet

- TILADocument1 pageTILACJ IbaleNo ratings yet

- REFLECTIONDocument16 pagesREFLECTIONFiona MiralpesNo ratings yet

- ResearchDocument4 pagesResearchFiona MiralpesNo ratings yet

- ActivityDocument3 pagesActivityFiona MiralpesNo ratings yet

- Integration Course2Document61 pagesIntegration Course2Fiona MiralpesNo ratings yet

- Module 8 - ReviewerDocument8 pagesModule 8 - ReviewerFiona MiralpesNo ratings yet

- ResearchDocument5 pagesResearchFiona MiralpesNo ratings yet

- Module 8 - TheoriesDocument3 pagesModule 8 - TheoriesFiona MiralpesNo ratings yet

- Bsa Ii B Group 2 Music DanceDocument51 pagesBsa Ii B Group 2 Music DanceFiona MiralpesNo ratings yet

- Research Questionnaire GROUP-3Document1 pageResearch Questionnaire GROUP-3Fiona MiralpesNo ratings yet

- Rizal Commercial Bank v. Hi-Tri Devt. Corp.Document1 pageRizal Commercial Bank v. Hi-Tri Devt. Corp.Aiza OrdoñoNo ratings yet

- Module 8 - TheoriesDocument3 pagesModule 8 - TheoriesFiona MiralpesNo ratings yet

- MDL April 19Document1 pageMDL April 19Fiona MiralpesNo ratings yet

- Module 8 - THEORIESDocument5 pagesModule 8 - THEORIESFiona MiralpesNo ratings yet

- Module 8 - TheoriesDocument3 pagesModule 8 - TheoriesFiona MiralpesNo ratings yet

- Renato Dalomias: ExperienceDocument2 pagesRenato Dalomias: ExperienceFiona MiralpesNo ratings yet

- AIS Chapter 1 17feb24 ClassDocument35 pagesAIS Chapter 1 17feb24 ClassFiona MiralpesNo ratings yet

- AEAIS Module 2 Overview of Transaction Processing and Enterprise Resource Planning SystemsDocument28 pagesAEAIS Module 2 Overview of Transaction Processing and Enterprise Resource Planning SystemsFiona MiralpesNo ratings yet

- CASE #15 Spouses Danilo Clarita German Vs Spouses Benjamin and Editha Santuyo and Helen S. Mariano, Deceased Substituted by Heirs G.R. No. 210845 July 3, 2020 FactsDocument1 pageCASE #15 Spouses Danilo Clarita German Vs Spouses Benjamin and Editha Santuyo and Helen S. Mariano, Deceased Substituted by Heirs G.R. No. 210845 July 3, 2020 FactsHarlene HemorNo ratings yet

- Philippine Deposit Insurance Corporation (PDIC)Document4 pagesPhilippine Deposit Insurance Corporation (PDIC)Angelo Raphael B. DelmundoNo ratings yet

- ACTIVITY 10 - Ramirez, Jerrald Cliff S.Document3 pagesACTIVITY 10 - Ramirez, Jerrald Cliff S.Fiona MiralpesNo ratings yet

- Test Bank 1 - Ia 2Document18 pagesTest Bank 1 - Ia 2Xiena100% (2)

- AIS Chapter 1 17feb24 ClassDocument35 pagesAIS Chapter 1 17feb24 ClassFiona MiralpesNo ratings yet

- Sales LawDocument191 pagesSales LawFiona MiralpesNo ratings yet

- Intacc Answer KeyDocument232 pagesIntacc Answer KeyFiona MiralpesNo ratings yet

- Debt Restructuring Group ActDocument8 pagesDebt Restructuring Group ActYaka Waka100% (1)

- Black White Minimalist CV ResumeDocument1 pageBlack White Minimalist CV ResumeFiona MiralpesNo ratings yet

- Sales LawDocument191 pagesSales LawFiona MiralpesNo ratings yet

- Untitled SpreadsheetDocument5 pagesUntitled SpreadsheetFiona MiralpesNo ratings yet

- 3 - Valuation of Equity Shares - Assignment (26-04-19)Document4 pages3 - Valuation of Equity Shares - Assignment (26-04-19)AakashNo ratings yet

- Chapter 6 Exclusions From Gross Income PDFDocument12 pagesChapter 6 Exclusions From Gross Income PDFkimberly tenebroNo ratings yet

- NissanDocument31 pagesNissanRomilio CarpioNo ratings yet

- Part 5555Document2 pagesPart 5555RhoizNo ratings yet

- Warren Buffett's Mini Unofficial) BiographyDocument8 pagesWarren Buffett's Mini Unofficial) Biographydeepak150383No ratings yet

- Capital Structure Policy I Ebit-Eps Analysis: Page 1 of 2Document2 pagesCapital Structure Policy I Ebit-Eps Analysis: Page 1 of 2Danzo ShahNo ratings yet

- Banking RatiosDocument7 pagesBanking Ratioszhalak04No ratings yet

- Negen Angel Fund FAQsDocument8 pagesNegen Angel Fund FAQsAnil Kumar Reddy ChinthaNo ratings yet

- Module 4 - Executive Summary 6110Document7 pagesModule 4 - Executive Summary 6110auwal0112No ratings yet

- CFA Level 1 (Book-C)Document51 pagesCFA Level 1 (Book-C)butabuttNo ratings yet

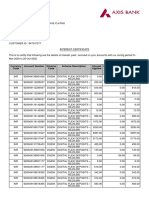

- Interest CertificateDocument2 pagesInterest CertificatesumitNo ratings yet

- LO3 ProblemsDocument11 pagesLO3 ProblemsKayla SheltonNo ratings yet

- Chapter 4 Cost AccountingDocument17 pagesChapter 4 Cost AccountingMel TrincheraNo ratings yet

- Learning Objectives: Assets Liabilities + EquityDocument13 pagesLearning Objectives: Assets Liabilities + EquityAira AbigailNo ratings yet

- Introduction To Debits and CreditsDocument8 pagesIntroduction To Debits and CreditsMJ Dulin100% (1)

- 40 Most Important Questions Business Studies SPCCDocument14 pages40 Most Important Questions Business Studies SPCCtwisha malhotraNo ratings yet

- Axis Smallcap FundDocument1 pageAxis Smallcap FundManoj JainNo ratings yet

- IAS 8 - Accounting Policies, Changes in Accounting Estimates and ErrorsDocument3 pagesIAS 8 - Accounting Policies, Changes in Accounting Estimates and ErrorsMarc Eric RedondoNo ratings yet

- IBO 3 - 10yearsDocument28 pagesIBO 3 - 10yearsManuNo ratings yet

- How To Secure A Bank Account From Levy 1Document5 pagesHow To Secure A Bank Account From Levy 1api-374440897% (124)

- Average Age of InventoryDocument10 pagesAverage Age of Inventoryrakeshjha91No ratings yet

- A B C D: 02 Objective / Objektif 2Document5 pagesA B C D: 02 Objective / Objektif 2foryourhonour wongNo ratings yet

- Us Engineering Construction Ma Due DiligenceDocument52 pagesUs Engineering Construction Ma Due DiligenceOsman Murat TütüncüNo ratings yet

- Time Value of MoneyDocument22 pagesTime Value of Moneyshubham abrolNo ratings yet

- Ali UblDocument135 pagesAli UblMuhammad SajidNo ratings yet

- Arvog Finance Corporate Presentation 2022Document9 pagesArvog Finance Corporate Presentation 2022Dinesh KandpalNo ratings yet

- COGM5 Final RequirementDocument24 pagesCOGM5 Final RequirementLadignon IvyNo ratings yet

- Case Study Vijay Mallya - Another Big NaDocument10 pagesCase Study Vijay Mallya - Another Big Najai sri ram groupNo ratings yet

- Write A Note On Previous Year and Assessment YearDocument2 pagesWrite A Note On Previous Year and Assessment YearBhaskar BhaskiNo ratings yet